Written by

William C. Vantuono, Editor-in-Chief

Eric Starks, President and CEO, FTR Associates.

RAILWAY AGE AT REF 2020, LA QUINTA, CALIFORNIA: FTR Associates President and CEO Eric Starks provided his usual high-energy observations on the global supply chain, the uncertainties of the current market and their implications for the North American rail industry. Following are key takeaways from Starks’ presentation on the near-term future for loadings, railroad growth and car demand.

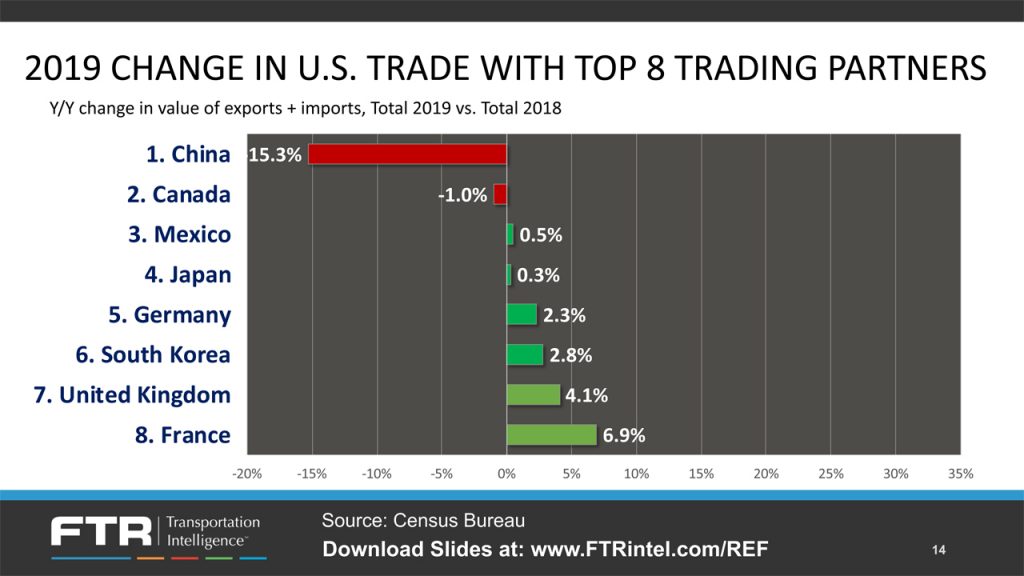

• On trade disruption:

Global supply chains are in transition, and there is movement toward smaller

trading partners to fill the gaps. This is impacting Asia and Europe. On the

positive side, this may make the COVID-19 (Corona) Virus impact not as severe

as it could have been due to changes in supply chains from the trade war. On

the negative side, “near-shoring” does not appear to be taking hold, because smaller

trading partners do not have the infrastructure to handle all of the shift in

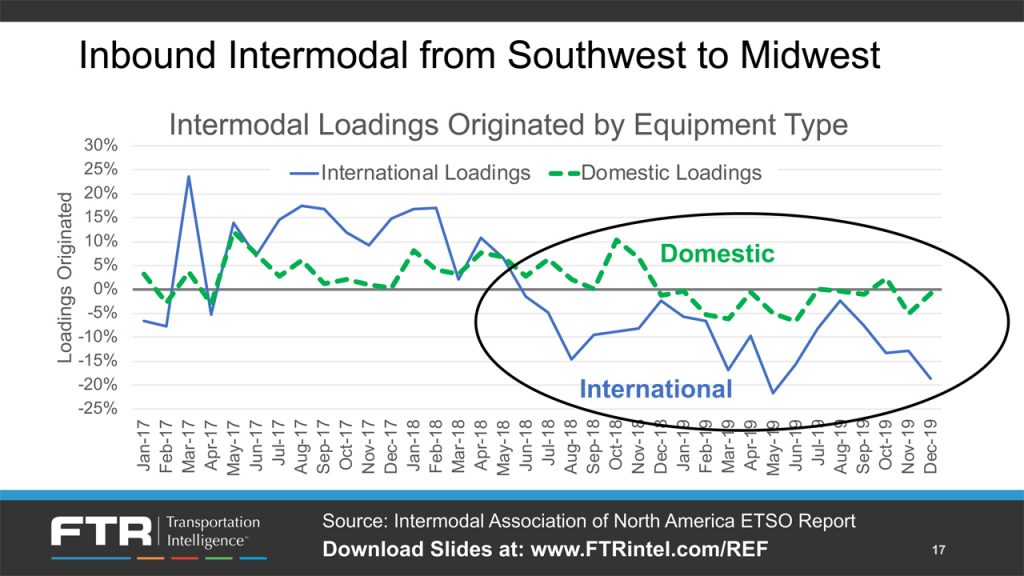

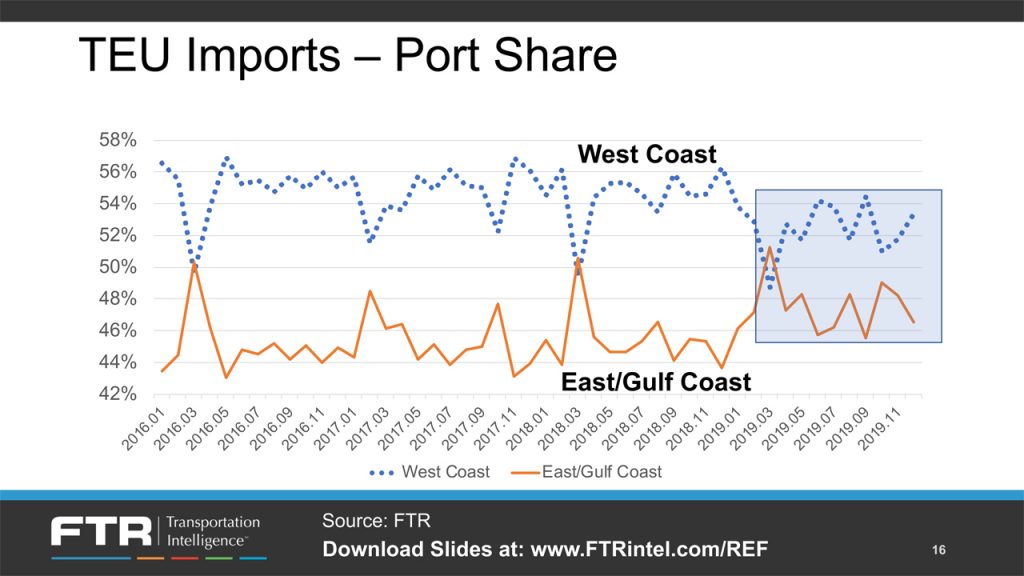

supply chain demands. The market is shifting toward moving more TEUs through

East and Gulf Coast ports. This is having a noticeable impact on rail

intermodal business.

• On crude oil: Falling oil prices

“leads you down a rabbit hole.” They indicate concerns of slowing global growth.

If so, there would be less pressure for domestic production. As well a lower

pricing point also puts pressure on domestic producers’ pocketbooks. For

fracking, there is a move toward “local brown sand” to save money. However, slowing

global growth, or lower prices for domestic oil, may lead to less domestic crude

oil production. This means that less sand and crude oil will need to be moved

by rail.

• On USMCA (United

States-Mexico-Canada Agreement) opportunities for rail: Ratification created business

certainty in the market. Companies are now willing to move forward with

investment in Mexico that had been previously put on hold. Growth opportunities

include finished autos and parts, refined petroleum products, and bulk commodities

and grain.

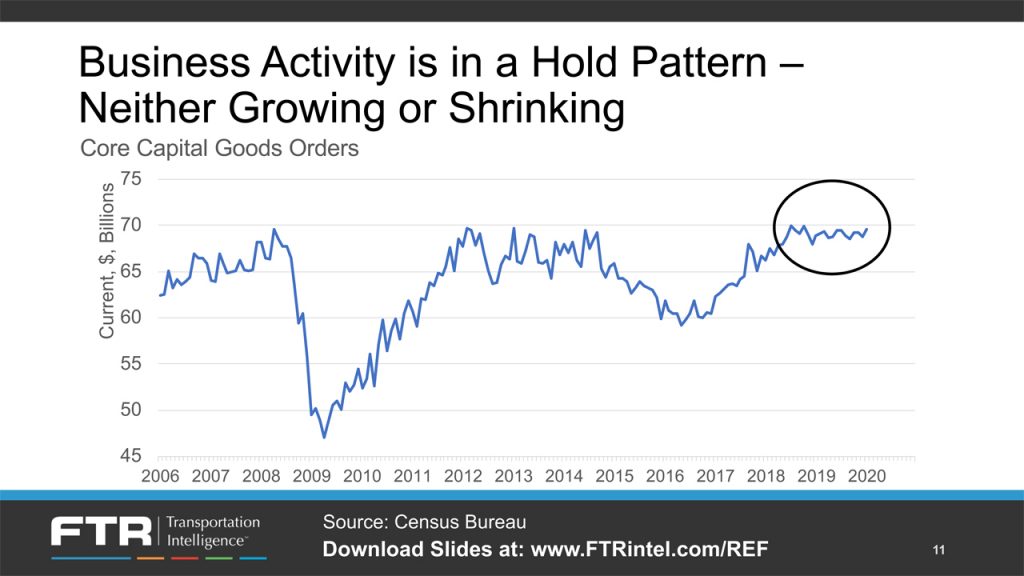

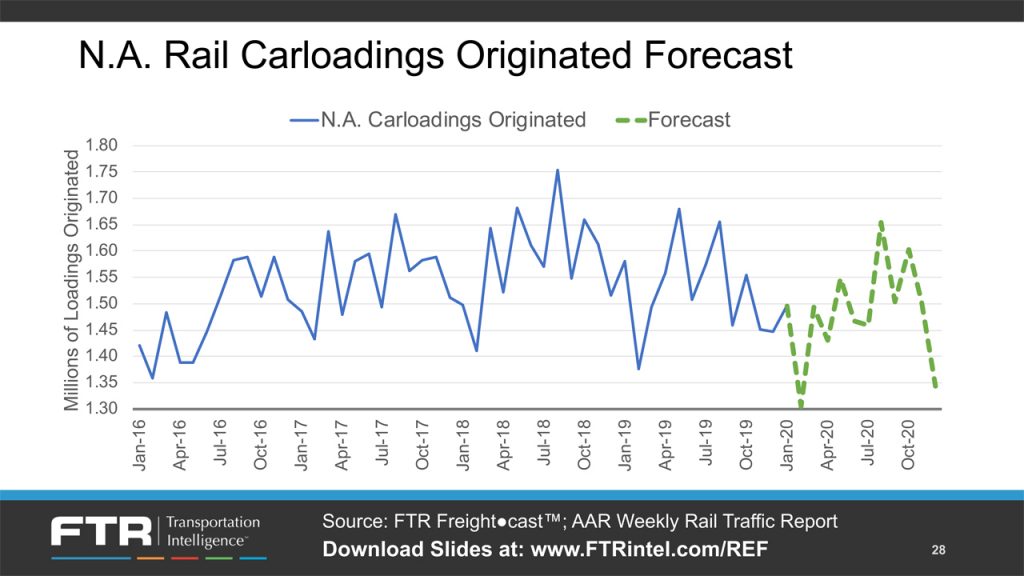

• Short-term outlook: Where will

additional rail freight come from? We know that, roughly, the next two months

will remain weak due to global supply chain disruptions. However, there is an

“upside opportunity surge,” since supply chain disruption will run down

inventories that will need to be replenished, with a base demand will need to

be backfilled that could lead to a surge in freight demand by late 2Q2020. The

downside risk is that if the Coronavirus is not contained by mid-summer and

there is no bounce back, global demand weakens further.

Download Eric Starks’ full REF 2020 presentation: