Steve Jennings/Getty Images Entertainment

Dear readers/followers

In this article, we’re going to be taking a look at the Dutch company Prosus N.V. (OTCPK:PROSY). Following a recent request to look at the company and deliver a stance for investment, I did some research and reached a conclusion. The CEO has recently come out and bought more shares because he believes the company to be substantially undervalued.

This article is an elaboration of that conclusion and the beginning of my following Prosus N.V.

Enjoy!

Prosus Logo Prosus Corporate

What does the company do & how has it been doing?

So, Prosus is a tech investment company. A software disrupter that makes its money by investing in businesses in the relatively early stages of funding, and targets returns in the thousands of percentages. On a high level, the company has a lot of similarities with a venture capital firm.

It essentially tries to invest in a lot of companies. Most of them never really go anywhere and stay small investments/holdings until they are divested or picked up by others.

Other investments are extremely profitable and history-making. Such is the case with its investment in Tencent (OTCPK:TCEHY). The risk/reward for a company like Prosus is absolutely core to its operations. Back in 2001, the company invested in relatively early funding in Tencent, buying nearly 45% (under 30% today) of the company for less than $35 million. For almost half of the company. Given the company’s size today, you can start guessing what’s happened to that asset value – or I can show you.

It was one of the most lucrative bets in corporate history.

The Tencent stake, as of the latest reported transparent NAV from Prosus, is worth $164.3B. That is a 20-year RoR of ~500,000.00% or an annualized RoR of 20 years of 53.00%.

That’s Bitcoin levels of returns – and the comparison is valid on several levels.

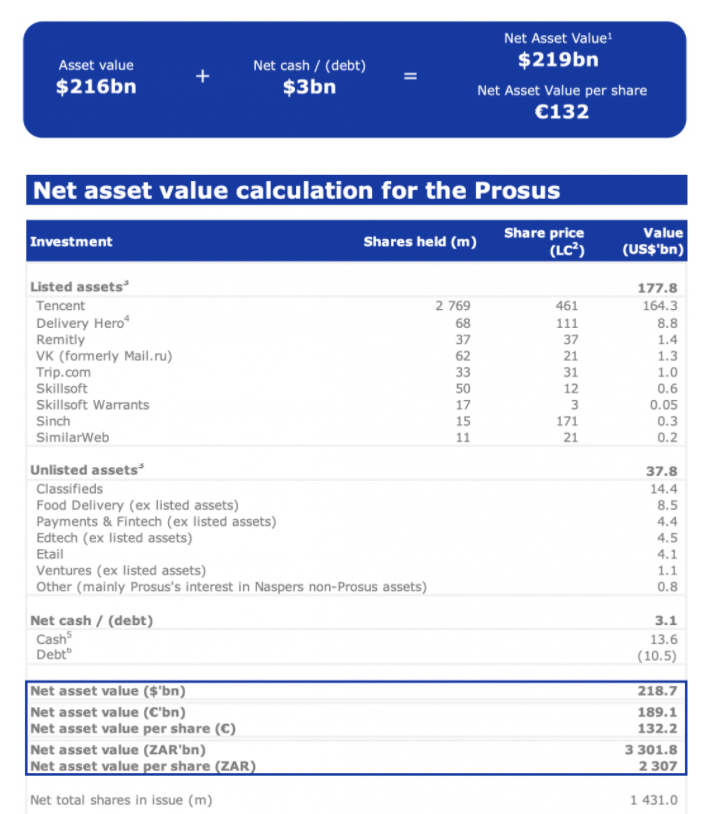

I am focusing on this investment a great deal because this is really quite significant for the company. Prosus’ net asset value, or assets overall, are primarily made up of Tencent at this point.

Prosus Assets Prosus Corporate Homepage

At a total less-net cash/(debt) NAV of $216 billion, the Tencent stake makes up more than 76% of the company’s NAV – 75%, if we include the 3Q21 net cash position of around $3B. This means that even including cash and the other investments with not-insignificant market value, I will argue in this article that an investment in Prosus is mostly an investment in Tencent.

Prosus is BBB-rated in terms of credit rating and has ~15000 employees working across most continents. The company is headquartered in Amsterdam, Switzerland, and listed on the Euronext stock market as a native share.

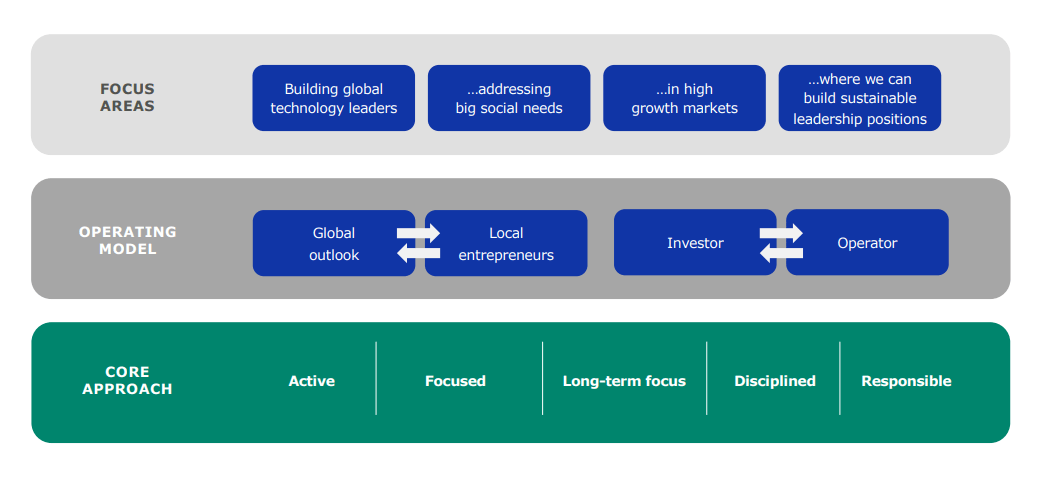

Prosus Strategy Prosus Investor Presentation

Prosus itself is the international asset division of the South African parent company Naspers (OTCPK:NPSNY) (OTCPK:NAPRF). This is very relevant to understand because the relationship between Naspers and Prosus is unique and quite complicated. If you take your time and read through the corporate statutes – or a few of the recent news reports, you will find that Naspers cannot, under normal circumstances and no matter what their actual stake is, lose control of Prosus due to the following little rule in its current statutes.

There are two classes of shares in Naspers. The N ordinary shares have one vote per share and are listed on the JSE. At 31 March 2021, there were 435,511,058 such shares in issue. There are also unlisted A shares, which carry one thousand votes per share but only have one-fifth economic participation. At the same date, there were 961,193 such shares in issue.

“Naspers is entitled to exercise at least 50%+ of all the voting rights in Prosus, if Naspers voting rights fall below this threshold, they are entitled to exchange their A2 shares into A1 shares with 1000 votes each.”

So, if we count voting rights, there were a total of 1,396,704,058 available votes of which the A shares control 961,193,000 or 69%. Clearly, the A shares control Naspers. Even if you held an outright majority of the listed N shares in Naspers, you wouldn’t control the company.

(Source: Interconnect.Za/Prosus)

Even if Naspers’s actual stake were to drop to minuscule levels, they would still retain majority ownership over the company. This has been a hot button issue, not the least of which during 2021 because there have been pushes by activist investors to dispel this unique relationship and create something more “normal”. (Source)

While this doesn’t necessarily make the company uninvestable, it certainly raises a few eyebrows, as such a thing is very rarely done.

So, let’s return to brass tacks here.

Prosus is a tech-focused investment company whose primary target is acquiring companies early in their growth cycle in order to make a big payoff. In order to do this, they typically invest large amounts of money into many smaller investments (as you can see by their balance sheet), in the hope that such investments will be the “next Tencent”.

Such an approach to investing bears a lot of likenesses to “Angel Investments” or Venture Capital approaches.

If you look at recent historical EBITDA levels, you will see that the company has shifted specifically to investing in food and payment companies, but the increases in NAV in its legacy portfolio (including Tencent) has not been or barely been able to make up the losses initially suffered in these investments.

On a pre-tax/interest/D&A basis, the company has been operating at a loss for many quarters, showcasing the risk-reward ratio of such an approach. For every ten investments you make, perhaps one turns out with a profit, and for every thousand, one turns out to be a “Tencent”.

If you, as the investor, want to make the argument that Prosus’ previous investment in Tencent gives them some sort of success guarantee…well, be my guest – but that’s not how I see the market working.

The company has solid fundamentals, and I don’t see any near-term risks given that the company can simply unload more Tencent shares if it needs the capital, but my question is about future growth and investments here. It’s not that the company has had “bad” growth over the past few years, but the question that comes to mind is how sustainable this will be in the market environment we’re moving into. None of the company’s investments thus far have shown the sort of potential we’ve seen from Tencent, and while a 20% e-commerce IRR is impressive, it also occurred during one of the tech-heaviest bear markets we’ve seen.

Not to put too fine a point on it, but there are companies who’ve done better during this recent bull market – especially in tech.

Prosus targets a total 2025 NAV of $100B from its e-commerce segment, which would at that point start to rival Tencent – something that’s desperately needed, looking at the current asset/NAV split.

None of the company’s other current assets are as appealing. The payment solutions sector lags behind peers like PayPal (PYPL), Adyen (OTCPK:ADYEY) (OTCPK:ADYYF), and others despite superb growth. Edtech/Education is showing impressive growth since investments, but again, few of these companies (Stack Overflow, Udemy, Skillsoft, etc.) have the potential to be the next Tencent for the company.

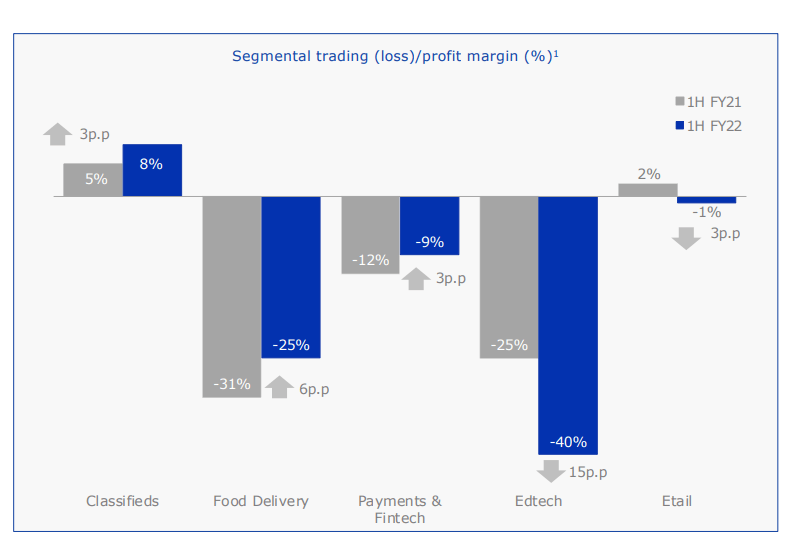

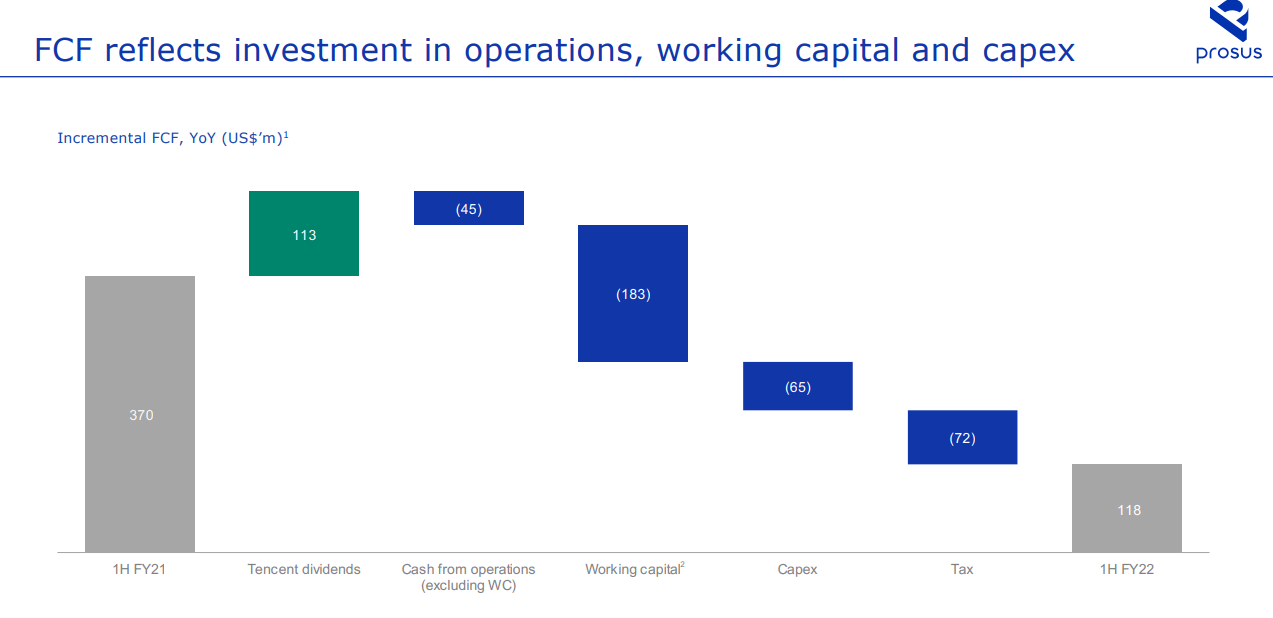

While half-year revenue during 1H22 was up nearly 31%, FCF was down to almost zero on a YoY basis. Food delivery isn’t growing as fast as it once was, and Edtech’s growth is flat. Results and margins show poor trends here.

Prosus Segmental Trading Loss/Profit margin Prosus 1H22 results

Prosus speaks a lot of doubling revenue and margin growth – but what quickly becomes apparent is that these margins, despite almost double revenues, are still negative, and justified by further investments towards an integrated ecosystem. Improved “scale margins” in food delivery are, for instance, around 6%, up to a negative 25% margin.

These are just examples. It’s clear that the company has very few recent successes to point to, because the key takeaways from the recent half-year are that the business remains “strong believers in a growth trajectory for Tencent”, and focuses on its excellent track record of capital allocation.

Prosus FCF Prosus 1H22 results

I want to be clear that there is no issue with this. Why? Because Prosus is essentially a venture capital investment firm. These sorts of investments are integral parts of its strategy. It’s how it made Tencent a success – by suffering through years of poor performance, betting on seeing that superb profitability at the end of the tunnel.

I have no issue with VC companies or Prosus. Provided you understand these things, this company could be a great investment.

What do I want you to understand?

- Prosus is mostly Tencent. 75%+ is the Chinese company here.

- Prosus isn’t as much of an investment giant in established businesses, but a Venture Capital firm with a tech focus. Understand the ups and downs of the VC world, because they most assuredly apply here. You need a strong stomach, especially once we start going into a downturn.

- Prosus is owned by Naspers, which has a very special relationship with the company – and not a popular one.

With that out of the way, I believe that 1H22 did show some promise in some sectors and challenges in others.

Let’s look at the most important question of all – valuation.

What is the valuation?

Here we come to what I believe to be one of the easier portions of this company.

Not because valuing the company is all that easy, but because the variables involved in the exercise are, to me, fairly simple to understand and apply.

Because Prosus is an investment company, its share price will have some sort of variance to its net asset value (NAV). When I invest in investment conglomerates (and I do, over 9% of my portfolio is allocated to several of them), I do so on the basis of NAV taking center stage here.

Usually, I like about a 1:1 NAV/share to Share price ratio as a guidance mark.

However, that is possible because all of my investment holdings have 90%+ listed portfolios of quality companies often going back 100+ years. They pay a yield. They’re not flighty or sudden with their allocation or investments. They have very specific strategies for holdings and holding times (usually forever) that I agree with.

This makes any discount, or premium, relatively forecastable and easy to spot.

With Prosus, this is different.

Not only is the majority of the company’s investments a 75%+ Tencent stake, but the company also relies on shifting in and out of markets, pushing capital into loss-making ventures to pick out those that may make it over time. It’s not a bad way to go – if you have the money – but it brings about a lot of risk, a lot of volatility, and if the market climate turns against you, years and years of poor performance.

Valuing Prosus is therefore a question of:

- How much do you want to/should you discount the company’s NAV/share in terms of risk/reward for its strategy?

- How much should you discount the company’s NAV/share to reflect its stake in Tencent, given the geopolitical risks of China and the current market situation?

- How much premium or discount do you believe should be applied for management capabilities or expertise, given historical performance?

- What should the discount be for the company’s shareholder relationship with Naspers, which means that Prosus is never really in charge?

These are the four points that matter the most.

If you look at the market, it speaks loudly as to the discount that it believes the situation warrants based on these situations. Prosus is currently trading at a ~50% discount to its NAV.

If this was a standard investment company, I’d be jumping for joy and investing.

But it’s not, so I’m not.

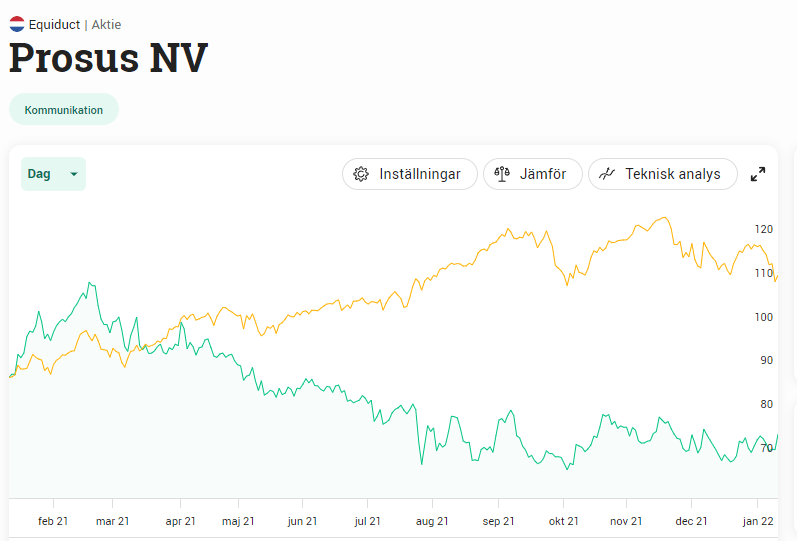

Prosus has had a terrible 1-year performance, underperforming by negative ~15%.

Avanza – Prosus Share Price Avanza

Even on a 2-year basis with the Nasdaq-superb 2020, the company has barely managed to keep up with a total 2-year return of around 20%. Not a good performance – but it reflects the way the market views this stock.

The company’s share price development does not reflect its NAV growth over time – or at least, there’s no development available that compares what the company has done with its Tencent asset since 2001.

At best, you’ve come away with low-double-digit returns in investment here. During the best of times, the company has roughly traded at a 10-20% discount to its NAV, which should be considered its ATHs.

So, on a strictly factual basis, the CEO is correct in the sense that the share is trading at close to or above a 50% NAV discount at current levels.

However, the CEO is omitting most of the risks or structures behind the company, which are applied by the market in this case.

For myself, I would not even look at Prosus unless it was discounted 60-70% to NAV – the same discount rate I apply to most Chinese or high-risk businesses to reflect what I view as outsized political risk. There is nothing taking way the fact that investing in Prosus is essentially investing in Tencent, with little else productive that to me is interesting.

That’s not to say the company doesn’t have interesting investments – it’s that the company’s investments aren’t exactly producing great returns – except its legacy positions. Investors are paying the company to keep pushing capital to work in these newer businesses (as a VC should), but with little overall visibility when they turn cash flow positive.

Add to this the fact that the market situation is shifting. We’re moving away from a low-rate environment into a higher-rate situation. The speed at which this move is being made is of course the question, but I don’t believe it will be long until the first moves and rate increases are made.

This will put pressure not only on Prosus, but all companies in the tech space/growth space, making them inherently less appealing investments as rates rise.

I don’t call it “wrong” as such to discount Prosus to a lower degree than I do. I would caution you, dear reader, if that is what you want to do, to be very aware of the risk-reward ratios of such an investment.

To be frank, I believe that if you wanted Tencent exposure, the company’s ADR might be a better bet than Prosus due to the lack of shareholder control in Naspers. Of course, if you’re looking for a player with experience in the space that also pays a dividend, Prosus isn’t bad per se.

The company has done quite well in an environment characterized by essentially “free money”.

I would very clearly caution you, however, that recent 2-year history shows the very real potential of a NAV discount of over 60% at its highest levels.

So while the CEO might believe the company to be undervalued here, and should be lauded for buying shares for investor confidence (and his own benefit), remember that just because a multi-millionaire is buying shares does not mean you should put your hard-earned cash to work in the same investments.

The Prosus ADR is OTCPK:PROSY, and it’s a 0.2X ADR, that’s relatively thinly traded, adding to the risk here.

I also want to mention that Prosus is forecasted to massively grow its revenues in both FY22 and FY23, at 47% and 30% respectively. However, this does not trickle down to affect cash flows or EBITDA positively to many major extents. Company’s EBITDA margins are forecasted to remain negative until 2023, at which point a 1.4% positive EBITDA margin is expected, with pre-tax earnings margins still remaining negative at -2.6% for the 2023E period. (Source: S&P Global)

Again, none of this should be seen as odd for a VC – but it’s maybe not what you’re looking for.

In the case that you are looking for this sort of company, and you’re prepared to put money on the table for the potential of finding the “next Tencent”, then I believe that Prosus might be one of your better bets, given its history and global scale.

However, this is a comparison that comes dangerously close to gambling to my mind, which is why I don’t invest here.

When would I be interested in Prosus?

Give me a 70% NAV discount.

Because we’re investing in a 75%+ Tencent portfolio, and my view on the Chinese market and geopolitical risks are less than favorable, I discount my NAV price target as I would discount any Chinese business. Nothing is 100% “uninvestable” – but I’ll want it for pennies on the dollar.

So when the company goes below €40/share, that’s sort of the initial indication for me that the bottom is in.

I may not even buy at this valuation – but I might be interested if the market doesn’t present any other great alternatives.

Thesis

My thesis on Prosus is as follows:

- Prosus is an investment that’s inherently different from buys I would consider due to its almost Venture Capital-like approach to investments and targets.

- The shareholder structure is unappealing and inherently disadvantageous to Prosus investors. While the company is fundamentally sound and has a great track record, there are too many fundamental question marks to really make this an option for me.

- I would be interested in Prosus if the market decided to discount it more than 79% to its current NAV. That currently comes to below €40/share but would change depending on the impact of Tencent. If Tencent drops, the company’s NAV drops with it – and quickly. A 50% drop in Tencent NAV would drop the company’s NAV by around 38%, showcasing just how tightly the company is tied to Tencent.

- I consider it a “HOLD” here.

Remember, I’m all about :

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

This process has allowed me to triple my net worth in less than 7 years – and that is all I intend to continue doing (even if I don’t expect the same rates of return for the next few years).

If you’re interested in significantly higher returns, then I’m probably not for you. If you’re interested in 10% yields, I’m not for you either.

If you however want to grow your money conservatively, safely, and harvest well-covered dividends while doing so, and your timeframe is 5-30 years, then I might be for you.

Prosus is a “HOLD” here.