AvigatorPhotographer/iStock via Getty Images

Providing Perspective

After the Great Financial Crisis, the container sector entered a massive depressionary phase because of an oversupply of container ships, which were built in the prior globalization boom. Investor interests were dwindling over the years after the Great Financial Crisis. Many companies went bankrupt and had to be restructured. Shareholder returns were deeply negative. After the fundamentals turned around in 2019, COVID hit and caused massive disruptions in supply chains. Global congestion primarily hit the Container Industry due to outsized demand for goods instead of services, and governmental stimulus funded by global central banks. The container shipping industry was one of the best places to be in 2021. The monetary expansion provided massive tailwinds for the demand of goods. The overhang of container ships cleared up as orderbooks reached historical lows. With supply restrained, and demand surging, freight rates went ballistic. The returns of Lessors and Liners were outstanding:

It goes without saying that the easy money has been made. Danaos (NYSE:DAC) went from facing bankruptcy in 2019-2020 to securing profitable long-term charter rates for several years while cleaning up their balance sheet. ZIM (ZIM) went on to earn $1,4B in Q3/2021 and $1,7B in Q4/2021 due to operating leverage which propelled the net margin close to 50%.

Mixed Circumstances – The Supply Side

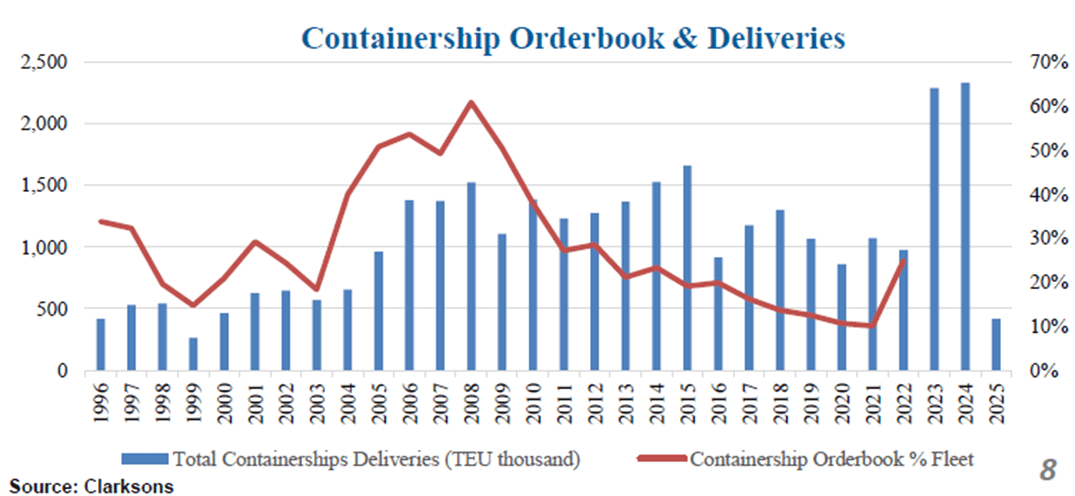

In 2022, investors face a mixed picture of the global container market. The global containership orderbook & deliveries remain low in 2022. But 2023 and 2024 looks scary. The orderbook reached ~26% of the fleet size for the first time since 2014, and combined with YTD 2022 deliveries, 6,2M TEU are now scheduled to be delivered during 2022-2024.

Containership Orderbook & Deliveries (CPLP Investor Presentation)

Sector experts believe that ~15% of the global containership fleet is still tied up by congestion (around 2M TEU). Assuming congestion eases during the next few years, the additional supply will exceed 8M TEU for 2022-2025. This represents 33% of the current global fleet size in 3 years.

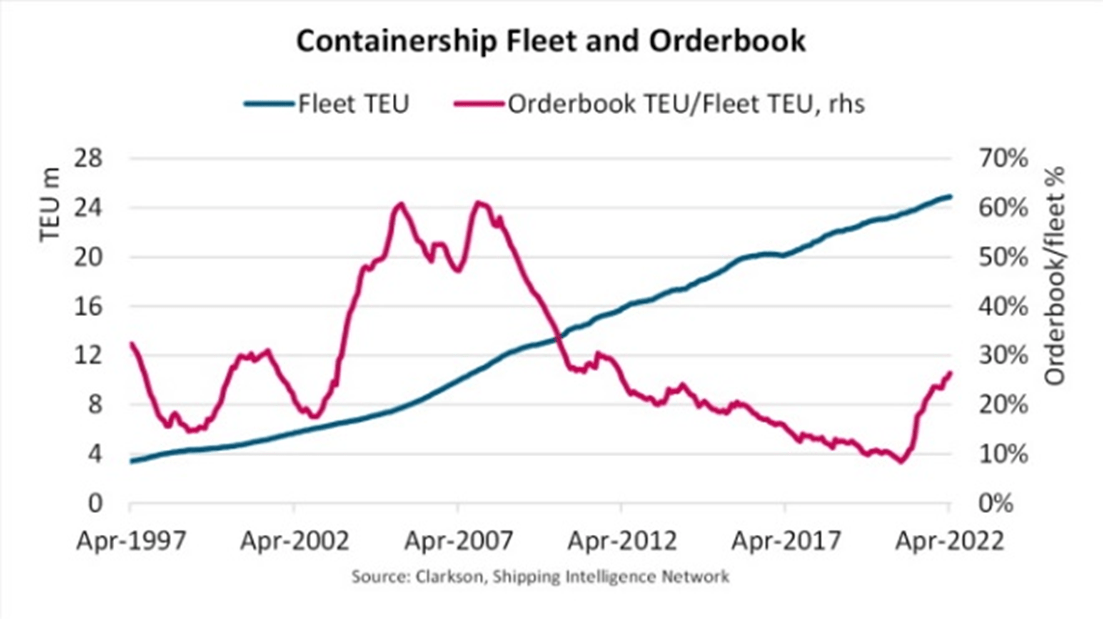

Containership Fleet and Orderbook (Hellenic Shipping News Worldwide)

On a positive note, current supply-sided tailwinds exist until the ordered vessels are delivered, with the majority of deliveries approaching mid-2023. That’s still a whole year of outsized returns for Liners and Lessors. If congestion remains high until 2023, Freight rates are likely to stay elevated.

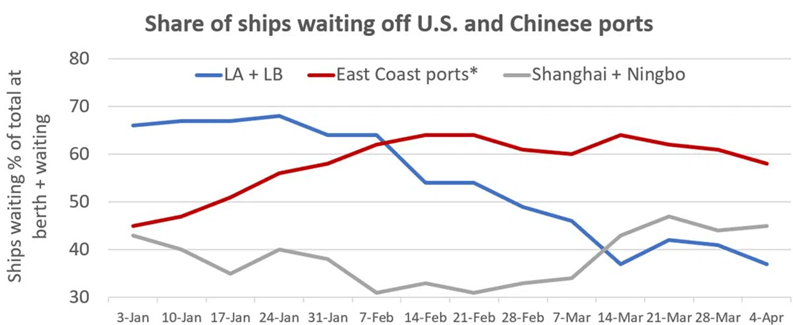

Recently, there has been buzz about another supply chain disruption in Shanghai due to the lockdowns imposed by the CCP. But as much as some investors want that to happen, the Shanghai port remains in operation, and there is no significant vessel congestion insight. Instead, vessel congestion eased on the east side of America, but many of these ships were directed to the west side, resulting in a net zero effect in terms of congestion levels.

Share of ships waiting off U.S. and Chinese ports (FreightWaves)

Environmental regulations (EEXI, CII, ETS), which begin to affect global shipping from 2023 onwards, could lead to a material slowdown of ships and/or increased scrapping. The concrete results of the environmental regulations are hard to estimate. I could even see these regulations being postponed if the current political crisis prevails, similar to ESG-related policies (e.g., nuclear reactors, oil & gas drilling in Europe) after a material increase in energy costs. Because of the impossibility of quantifying the environmental regulations, I regard them as advantageous for the supply side, but I wouldn’t build a bull case around it. Especially when taking into account the orderbook in 2023.

The Demand Side

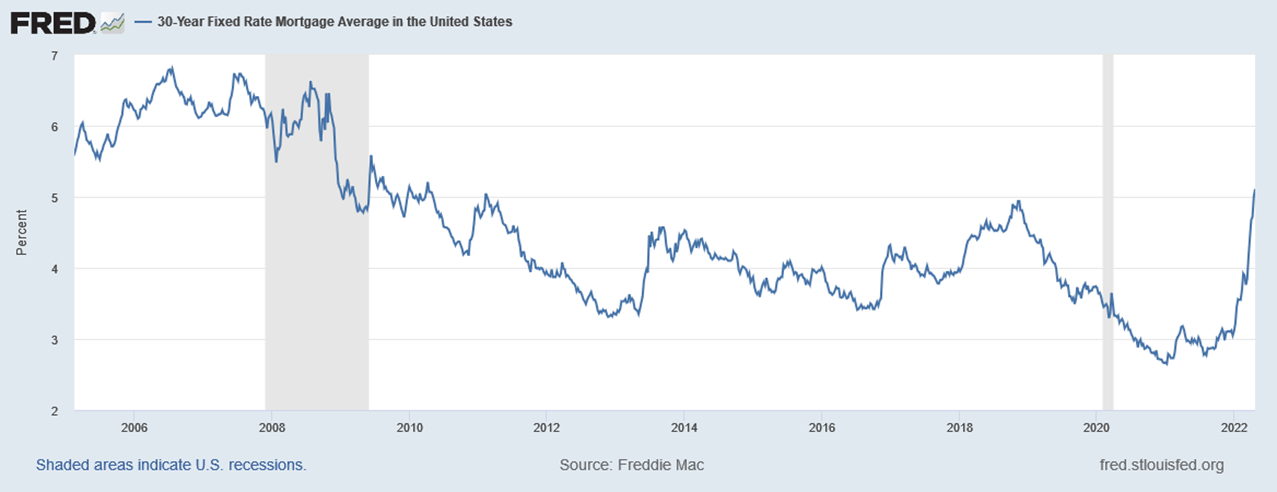

Currently, dwindling demand is the major concern for global container shipping. The monetary policy of the Federal Reserve, combined with fiscal stimulus after the COVID Crash in 2020 provided massive tailwinds for consumer demand and therefore freight rates. The FED is expected to hike interest rates and continue the monetary tightening by selling some of their previously purchased bonds. There is no further stimulus from the US government insight. The catalysts that sent global Container Shipping zooming in 2021 are fading. Rising Oil Prices, historical inflation rates, and higher interest rates could start slowing global demand for consumer discretionary goods, which would be terrible for container demand. Additionally, 30-Year fixed mortgage rates recently reached the 5% mark with incredibly strong momentum.

30-Year Fixed Rate Mortgage Average in the US (FRED)

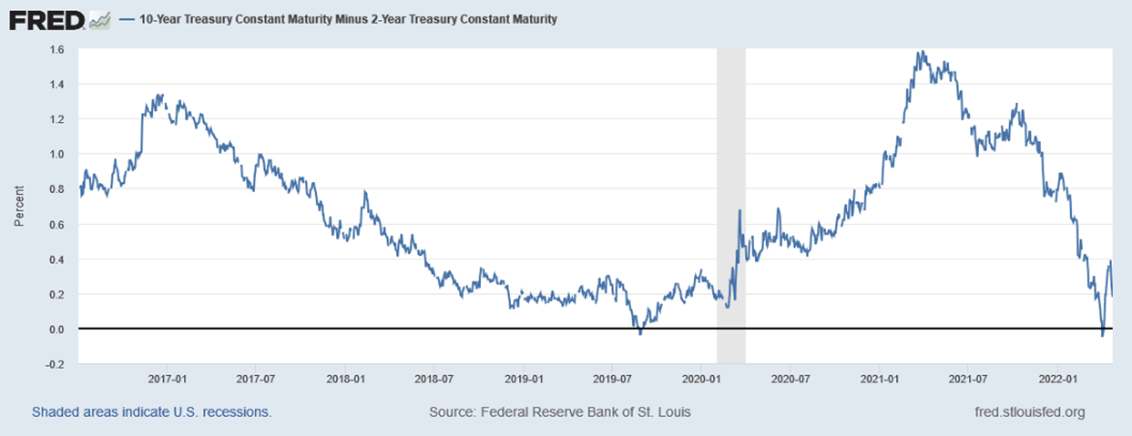

If the elevated housing prices start to fall because of high debt burdens, then ripple effects will certainly hurt US equities. Additionally, the 10Y-2Y Treasury Yield Spread recently went negative for a short time. Other yield curves inverted similarly.

10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity (FRED)

Historically, an inversion of the yield curve predicted a recession within the next 6-18 months. That is because the surge in demand for longer-term bonds signals risk aversion. A Risk-Off scenario would be bad for global container shipping, as the demand side of the equation can be roughly estimated by GDP growth. A recession could send Container stocks down the drain.

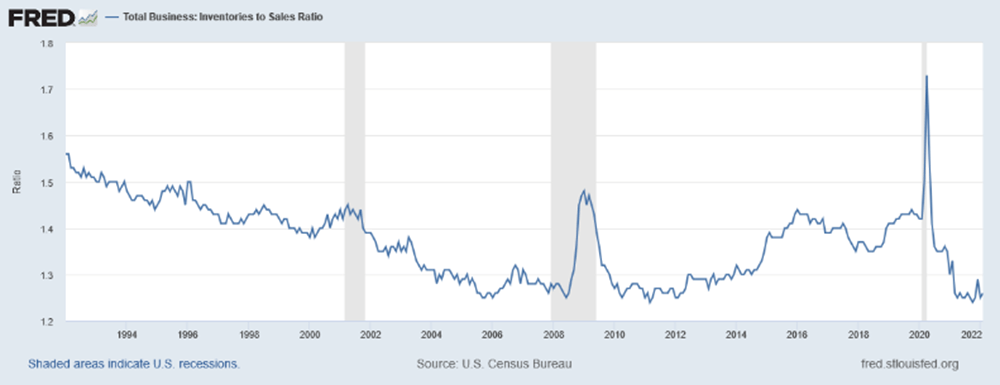

On a positive note, the total inventories to sales ratio remains relatively low. But if total Sales fall, this ratio could change too.

Total Business: Inventories to Sales Ratio (FRED)

Is this still a bullish article?

In essence, I believe the current supply-side remains favorable, until either port congestion is fully resolved or newbuilds enter the market materially in mid-2023. The demand side remains the biggest question mark, as per usual. I don’t believe the economic slowdown is imminent. But I see significant headwinds going into 2023.

If the current market remains favorable until 2023, there is still money to be made in container shipping, given the current valuations of most shipping companies. I’m still invested and quite bullish on the Container sector. Although with a caveat.

Freight rates and charter rates remain stubbornly elevated throughout what would normally be a seasonally weak first quarter.

FBX: Global Container Freight Index (Freight Rate Index)

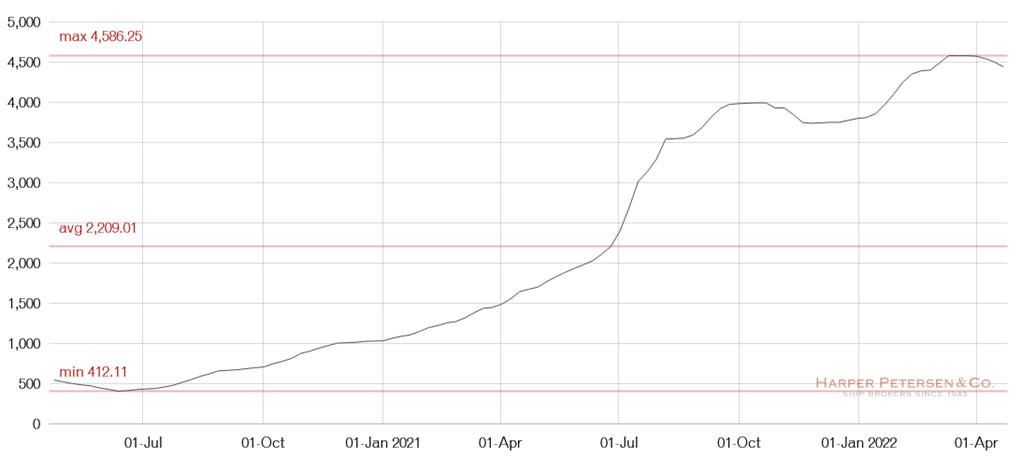

Charter Rates remain even stronger.

Harpex (Harper Petersen)

Charter Rates and freight rates should normalize during the next few years – the only question is with how much momentum and how soon. Even with the current headwinds, I believe the discount at which some companies in the sector are trading is too significant to be ignored.

What the Market is missing

The market is not blind to the risks I laid out above. During the last week and today (25th of April), Cyclicals sold off massively. Naturally, Shipping stocks are off their previously reached highs too:

However, the market is missing that virtually every container lessor (DAC, GSL, CMRE, ATCO, ESEA) has locked in fixed charter rates for several years ahead. A drawdown in freight rates and charter rates doesn’t matter for these companies until the fixtures expire. What matters is the counterparty risk of Liners going bankrupt. But Liners have been printing free cash flow during the last year. Many of them are net-debt-free and without any risk of defaulting any time soon. The market historically values lessors based on their FCF/Earnings and Shareholder Returns.

Many Lessors have finished acquiring Newbuilds and Secondhand Ships and are likely to return capital to their shareholders at an increased rate. Obviously, companies outside of a specific European country are preferred in that regard.

As I have outlined in my previous article about ZIM Integrated Shipping, Liners could suffer materially from falling freight rates due to spot exposure. Therefore, the selloff due to the above-outlined question marks about demand seems somewhat appropriate (although in my opinion, overly harsh).

But not only ZIM or other Liners like Matson (MATX) sold off during the last days/weeks, but Lessors like Global Ship Lease and Danaos too.

ZIM declined by 29% over the last few weeks and MATX by 30%. DAC and GSL moved in simulacrum declining 23% and 24%, respectively. Due to comparable volatility, the market assigns DAC and GSL similar risk levels as ZIM and MATX. I believe the market is wrongly treating Lessors in comparison to Liners, disregarding the differences of their business models.

DAC and GSL have fixed much of their revenues for several years. Falling freight rates and charter rates do not matter for them during their charter duration. The market is blindly selling off shipping stocks in the container segment without adequately discounting the vastly different risks for Lessors and Liners.

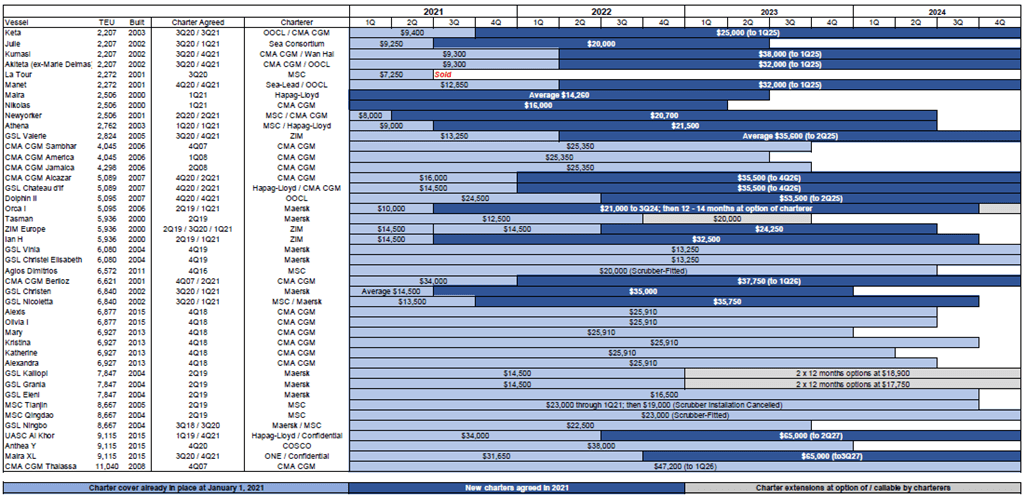

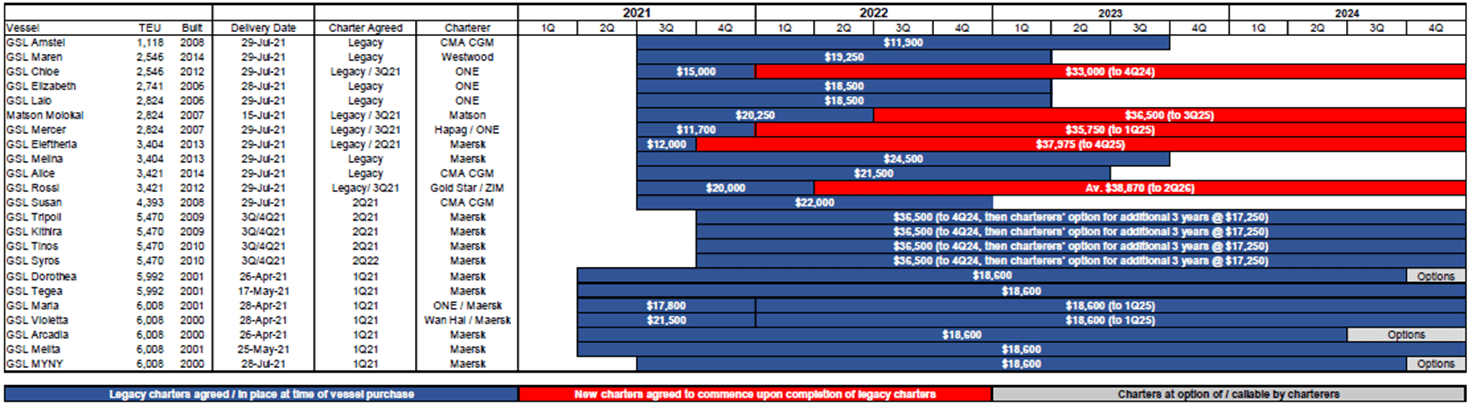

Global Ship Lease

GSL fixed the majority of their Charter Agreements until 2025-2027. 100 % of the revenues of 2022 are already locked in.

GSL Investor Presentation Q4/2021 (Global Ship Lease) GSL Investor Presentation Q4/2021 (Global Ship Lease)

The fixtures of the fleet of GSL amount $1,8B of contracted revenue and $1,17B EBITDA, compared to a market capitalization of ~$850M. No matter how the market turns in 2022, GSL will earn ~$586M of EBITDA and ~$418-517M EBITDA in 2023. I expect higher operating expenses in 2022, compared to 2021, around ~$260-285M.

GSL sits on ~$200M of cash and has no debt maturities before May 2024. Total debt outstanding is at ~$1,86B, with an average interest rate of 4,70%, which amounts to ~$87,4M in annual interest payments. My estimate for the EBT of GSL in 2022 is ~$215-240M or $6-6,7/share. That represents a P/E FWD ratio of ~3,2-3,5x.

The company will distribute dividends of $1,5/share, currently representing an attractive dividend yield of ~6,8%. Furthermore, GSL is pursuing opportunistic share buybacks. In Q1/2022 GSL had a $40M buyback authorization.

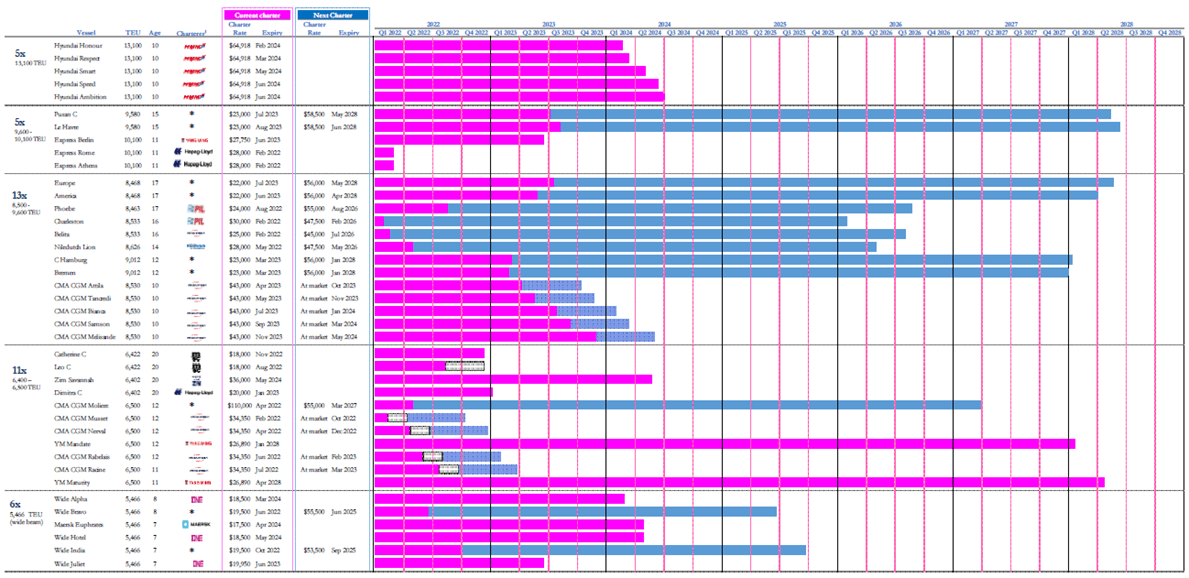

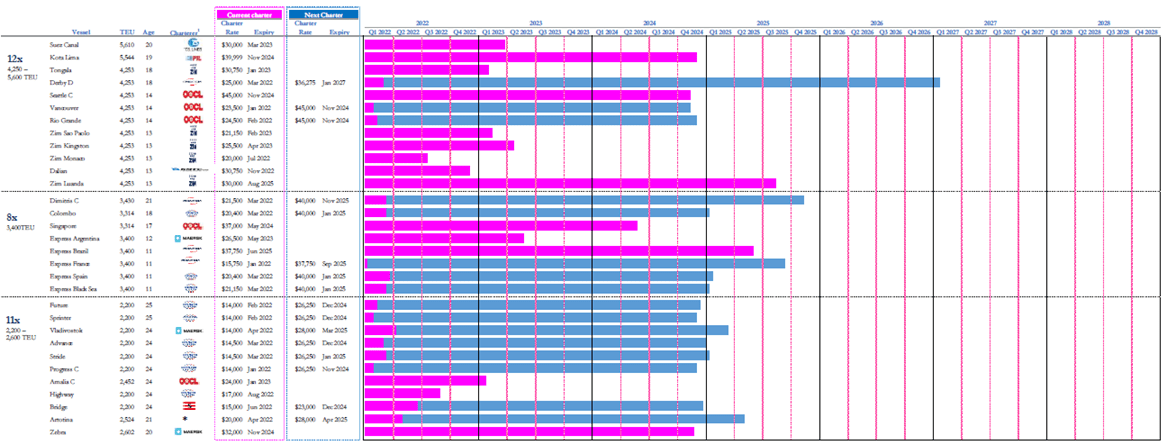

Danaos Corporation

DAC has a Charter backlog of $2,8B through to 2028 and an average charter duration of ~4 years. DAC also has locked in almost 100% of the revenues for 2022, ~77% of revenues for 2023 and ~57% of revenues for 2024. As of December 2021, contracted revenues for 2020 were $850M, and contracted revenues for 2023-2024 were $1,3B.

DAC Investor Presentation Q4/2021 (Danaos Corporation) DAC Investor Presentation Q4/2021 (Danaos Corporation)

I expect contracted revenues in 2022 to come in at ~$885M and operating expenses of ~$385-405M. With expected interest rate expenses at ~$60M, this would amount EBT of $400-420M or $19,5-20,5/share, representing a P/E FWD ratio of 3,8-4x.

DAC sits on ~$130M of cash. Long-term debt is at ~$1B. Debt maturities in 2022 amount to $96M, and $194M of debt repayments are due in 2023-2024. The weighted average interest rate of this debt is 4,4%.

DAC has been quite restrictive with their dividend policy, raising the Quarterly by only 50% to $0,75/share. Currently, this represents a dividend yield of ~3,8%. DAC remains hesitant on share buybacks.

Volatility vs. Business Risk

The container shipping equities will remain as volatile as they always have been. Investors should not see the forest for the trees and locate the underlying business risk instead of relying on implied volatility. By selling off the whole sector because of recession fears, the market is disregarding that Lessors operate a more robust business than Liners. Irrespective of the validity of recession fears, Container Lessors trade at cheap multiples and provide secured cash flow for years to come.

In this article, I provided my view on the container shipping industry, using my favorite Lessors, GSL and DAC. However, with recent market volatility, high-quality Container Lessors, which aim for longer fixtures than the two I picked, have sold off materially too. Risk-averse investors who want to profit in the Container Sector, could also seek exposure through investing in Atlas Corp. and Costamare (CMRE). Even non-cyclical Box Lessor Companies like Textainer Group (TGH) and Triton International (TRTN) sold off recently. These companies seem preferable for long-term buy-and-hold investors.

On a personal note:

Thanks for the great comments on my last article about ZIM and the overall container market. The feedback was astonishing! I’ve seen some healthy and respectful discussions and want to express my gratitude for that.

“Stock market profits are compensation for pain and suffering. First comes pain, then comes money” – André Kostolany