Panuwat Dangsungnoen/iStock via Getty Images

We have covered Flaherty & Crumrine Preferred Income Fund (NYSE:PFD) and Flaherty & Crumrine Preferred Income Opportunity Fund (NYSE:PFO) previously. Both funds did not make our buy list the last time we spoke about them. With another recently announced distribution cut, we jump right into the outlook for these two and tell you whether we have seen enough pain for a pivot.

The Cuts

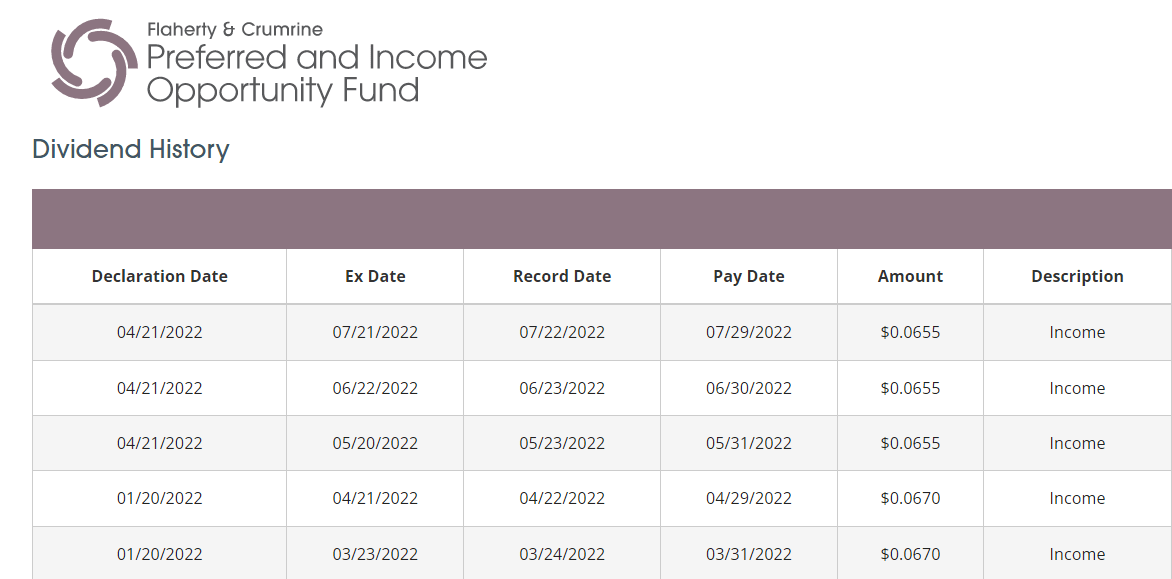

Both funds announce three months of distributions at a time and PFO delivered the news of a small and subtle 3% distribution cut, starting with the May payment.

PFO Distributions (Flaherty & Crumrine)

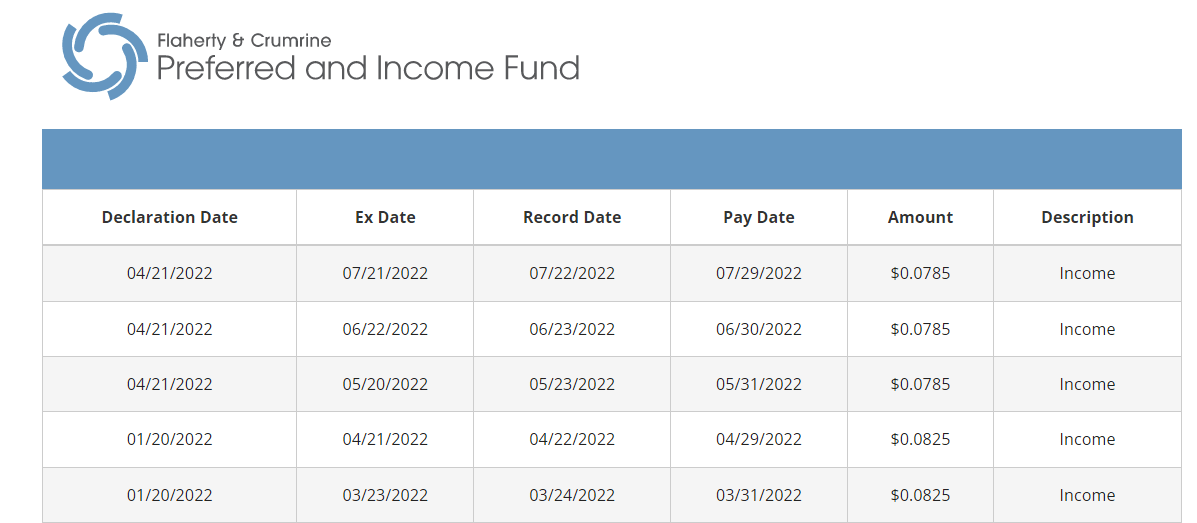

PFD took this message to a higher level and cut its distribution by 4.9%.

PFD Distributions (Flaherty & Crumrine)

Both funds have always emphasized NAV preservation and paying out what they earn over time. In other words, they don’t care for the “I want my regular distribution, principal be damned” crowd. Going into 2022, with the Federal Reserve being about as far behind the curve as you could get, the writing was on the wall for a long time.

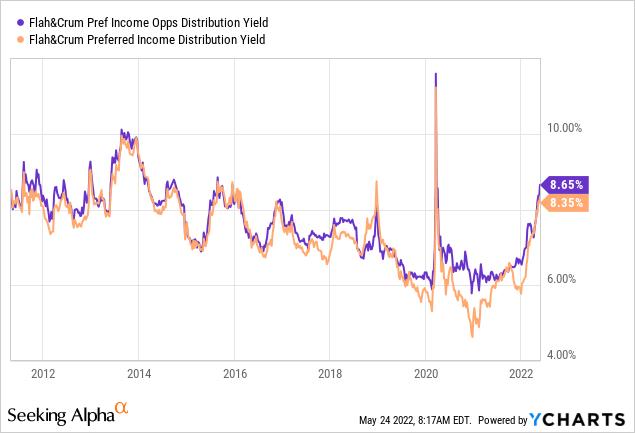

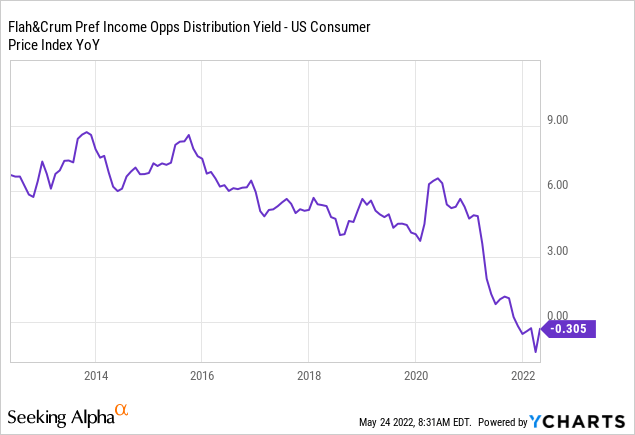

Current Yields

The funds still yield a pretty penny though. PFD yields 7.88%. PFO distributing 78.6 cents annually yields 8.26%. We want to note here that Y-charts is still looking at the trailing 12-month yield and has not factored in the cut yet. Nonetheless, the chart below gives context on the current yield relative to the last decade.

There are a couple of things we want to note here. The first being that while yields look high, compared to 2020 and 2021, they are not high in relation to the last decade. This is especially true if you adjust them down to their forward yields. We want investors to avoid the price anchoring for the last two years where the Federal Reserve and of course investors, blew the largest fixed income bubble known to man. The unwinding of that bubble has just put yields back to the center.

As anyone who has followed our work knows, we don’t believe that things ever stop at the mean. What was extremely overvalued will become extremely undervalued. So if you have not enjoyed the white-knuckled ride so far, too bad. It is going to get worse.

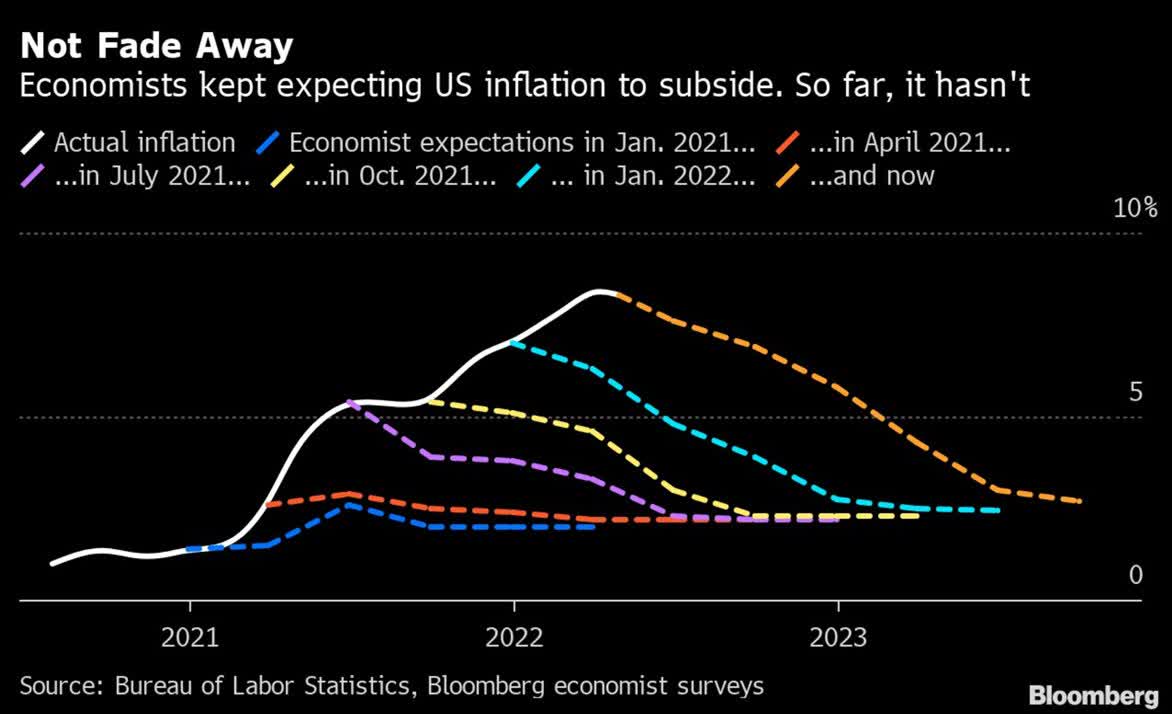

The second aspect here is that the last decade did not feature 8% CPI inflation at any point. So whatever yield you got paid in the last decade, just logically you should expect more. The last year has all been about economists and bond bulls (you know who you are), constantly issuing apologies for getting the outlook completely wrong.

– (Bloomberg)

So we have seen a slow and steady selling on bonds and other fixed income instruments as they have come to grips with reality. After all that reality sinking in and all that selling, these funds still yield under the official CPI rate, whereas they regularly yielded 5-6% more than the CPI rate.

Outlook

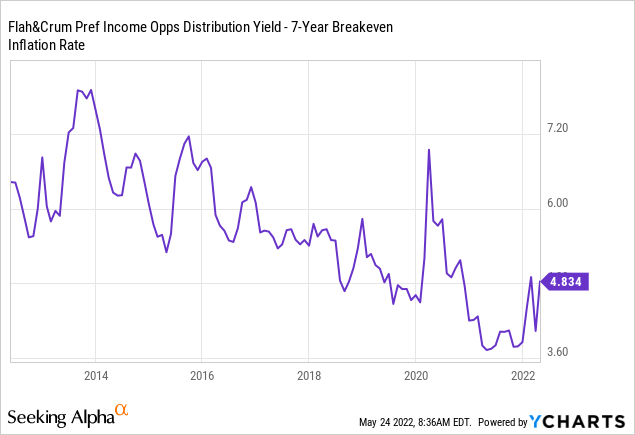

We have often criticized investors for focusing on a single year of earnings for stocks. The idea of buying The Walt Disney Company (DIS) for example, based on one year of “reopening earnings” ranks among the silliest we have ever heard. Long-duration securities should be valued on the weighted average outlook over time. The same applies to preferred shares. While they look ridiculously overvalued in relationship to CPI, we don’t believe that CPI will average close to these levels over the next few years. A good way to look at fair value though is to see the spread between the distribution yields of these two and the 7-year breakeven inflation rate. The latter is a measure of what the market expects inflation to average over the next seven years.

By this measure things don’t look as bad as when you benchmark these yields against CPI. But they don’t look extremely cheap either.

Verdict

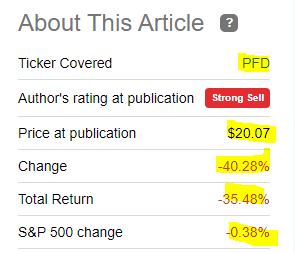

Mean reversion is extremely painful. When we first wrote about PFD, it was one of the most overvalued securities in the income space. The returns that followed were justified.

Returns Since First Article on PFD (A Preferred Fund Valued For Exceptionally Poor Returns)

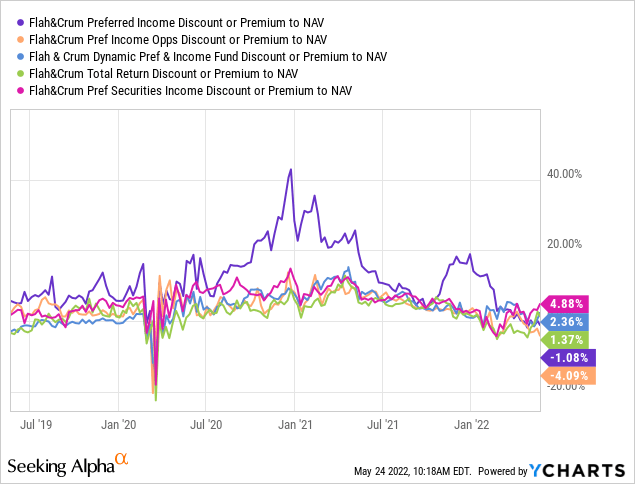

One reason for the horrendous performance from that point was the premium to NAV (see big spike in purple line at beginning of 2021). At present though, both funds are actually at discounts to NAV.

The three other funds from the same outfit, Flaherty & Crumrine/Claymore Total Return Fund (FLC), Flaherty & Crumrine Preferred and Income Securities Fund Incorporated (FFC) and Flaherty & Crumrine Dynamic Preferred and Income Fund, Inc. (DFP), are at modest premiums. So PFD and PFO have a slight relative advantage here. That said, historically, we have seen 10-15% discounts to NAV pop up during periods of high stress. With the Federal Reserve decidedly hostile, we would look for a double-digit discount to NAV to issue a buy rating. We currently rate both funds, at neutral/hold.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.