Irina Gutyryak/iStock via Getty Images

Most people love a good party from time to time. Though it may seem surprising at first, there are some companies dedicated solely to providing the goods and services often needed to make a party the best that it can be. One such company that happens to be publicly traded is a retailer and wholesaler called Party City (PRTY). Although the company has had a rocky operating history in recent years, and operating history that was made significantly worse in the near term by the COVID-19 pandemic, the overall picture for the business looks fairly solid. Shares are trading at levels that are fundamentally appealing. But this does not mean the company is a strong opportunity presently. Despite the low price that shares are trading at, the company does have some problems. And those problems appear to be largely related to management and what management is trying to make the company into as opposed to what the company should be.

A valuable company; confused management

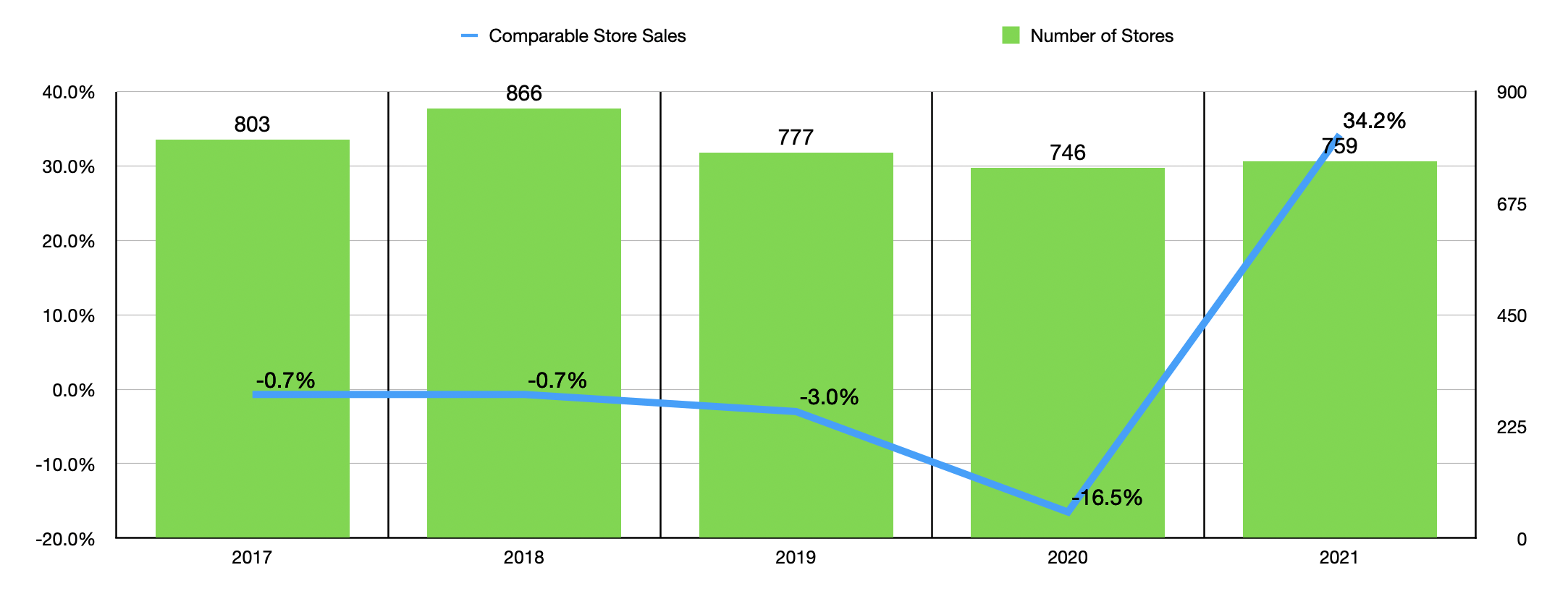

Today, Party City operates as a major retailer and wholesaler of party products and related offerings. As of the end of the company’s 2021 fiscal year, it operated 759 company-owned retail party stores throughout North America. On top of this, it also had approximately 72 locations that are franchised. These stores operate under the names ‘Party City’ and ‘Halloween City’, plus the business also has its own e-commerce websites that provide the same goods that their stores do and more. Through these retail concepts, consumers can buy a wide array of products. These include, but are not limited to, balloons, costumes, tableware, decorations, stationery, gift wrap, party favors, bouquets, and much more. On average, these locations each have about 25,000 SKUs, while their online platform provides 40,000.

Author – SEC EDGAR Data

Operationally, the company has two key segments. One of these is the Retail segment. This covers the control of all of the company’s retail stores, and all of the activities that go along with them. During the company’s 2021 fiscal year, this particular segment accounted for 81.5% of the firm’s overall revenue and more than all of its profits. The other segment the company operates is the Wholesale segment. Through this, the business provides Products ranging from tableware to accessories to novelties to balloons and more to the company’s various clients. For the most part, clients include its own owned stores and website, as well as its franchised locations and other domestic retailers. However, a small portion of revenue is attributable to domestic balloon distributors and retailers, as well as to various international clients.

Author – SEC EDGAR Data

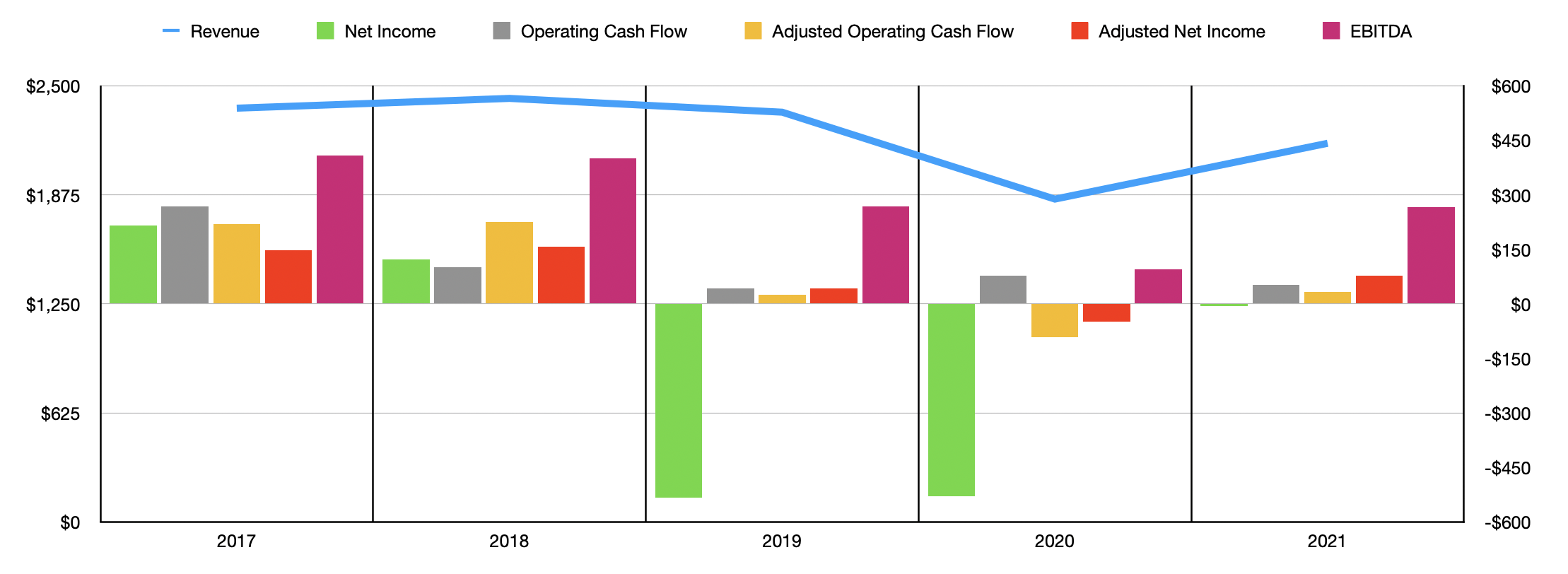

The past few years for Party City have been a bit rocky. Revenue fluctuated between a low point of $2.35 billion and a high point of $2.43 billion in the three years ending in 2019. Then, in 2020, revenue plunged to $1.85 billion before recovering to $2.17 billion in 2021. Some of this volatility has been driven by a change in store count over time. Company-owned locations grew from 803 in 2017 to 866 in 2018 before dropping ultimately to a low point of 746 in 2020. Then, in 2021, this count increased slightly to 759 stores. The company has also suffered from volatility from a comparable store sales perspective. Comparable store sales were negative in each of the three years ending in 2019, ranging from negative 0.7% to negative 3%. Then, in 2020, comparable store sales were negative to the tune of 16.5% before turning positive in the amount of 34.2% in 2021 as the economy reopened.

Profitability has also been rather mixed over the years. After seeing income drop from a positive $215.3 million in 2017 to a negative $532.5 million in 2019, it came in negative to the tune of $528.2 million in 2020. But in 2021, the company did see a narrowing of its losses, with net income totaling negative $6.5 million for the year. Operating cash flow has been similarly volatile, but the general trend has been in the direction of weakening cash flow over the years. Even if we adjust for changes in working capital, the picture has been strained, with cash flow dropping from a high of $226.3 million in 2018 to a low point of negative $92 million two years earlier. Then, in 2021, it ticked up slightly to a positive $33 million. Other profitability metrics, such as adjusted net profits and EBITDA, have been similarly volatile over the years.

Despite this volatility and pain, management has decided to resume growing the company. For instance, during the firm’s 2022 fiscal year, they hope to open between 100 and 125 new locations. It’s worth noting that this number is inclusive of remodels. As a result of this, combined with brand comparable sales increasing by between 2% and 4%, the company expects revenue to be between $2.275 billion and $2.35 billion for the year. In order to fund these additional locations, the company expects to spend between $120 million and $130 million. They anticipate net income of between $64.2 million and $82.5 million for the year, with EBITDA ranging from between $275 million and $300 million. Management provided no estimates when it came to operating cash flow. But if we assume that this metric will increase at the same rate that EBITDA will for the year, then a reading of around $35.6 million is not unrealistic.

This is fine and all, but the problem with the company is that management, after spending the years of 2018 through 2020 closing many of its stores, is now seeking to expand again. This is at a time when comparable store sales are weak (excluding the post-pandemic recovery period), when the net leverage ratio of the business, using forecasted EBITDA at the midpoint for 2022, is 4.83, and with the company regularly generating net losses year after year. Instead of emphasizing increasing its store count when it had previously spent a few years reducing it, the company should be focused on improving its supply chains in order to reduce costs and it should be looking at other efficiencies and focusing on debt reduction.

Author – SEC EDGAR Data

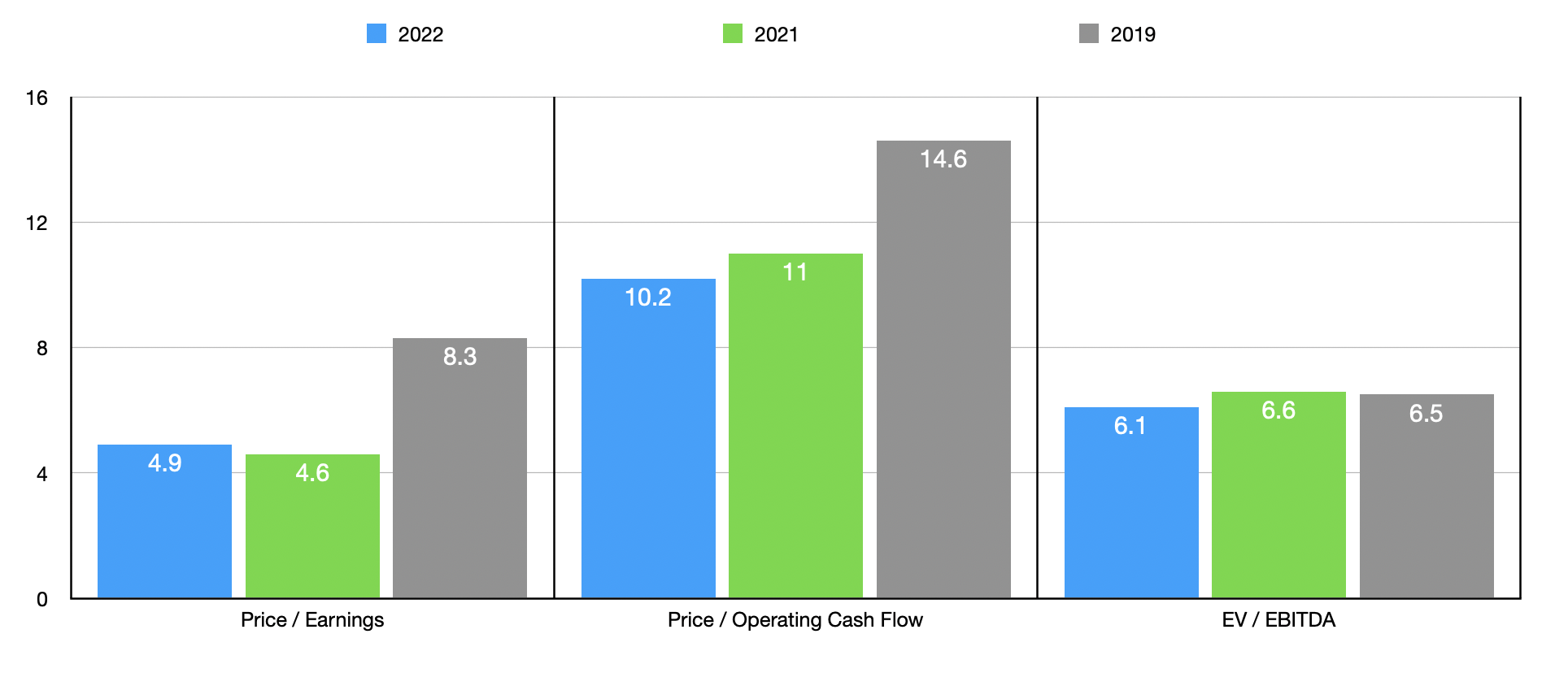

The fact that management is not doing these things reflects in the company’s low trading price. In the chart above, you can see pricing data estimated for the company’s 2022 fiscal year, as well as see historical data based on financials from 2021 and 2019. Using the data from the 2021 fiscal year, the company is trading at a price-to-earnings multiple of 4.6. The price to adjusted operating cash flow multiple is 11. And the EV to EBITDA multiple is 6.6. To put this in perspective, I decided to compare the company to five similar firms. On a price-to-earnings basis, four of the five firms had a positive reading, with a range of between 3.6 and 9.8. Only one of the prospects was cheaper than Party City. Using the price to operating cash flow approach, the range was from 3.2 to 30.5. Two of the five companies that had positive results were cheaper than our prospect. And using the EV to EBITDA approach, the range for the four companies with a positive reading was from 1.7 to 4.5. In this case, Party City was the most expensive of the group.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Party City | 4.6 | 11.0 | 6.6 |

| Big 5 Sporting Goods (BGFV) | 3.6 | 3.2 | 1.7 |

| The Container Store (TCS) | 4.7 | 11.1 | 3.4 |

| Build-A-Bear Workshop (BBW) | 9.8 | 11.3 | 4.5 |

| Sportsman’s Warehouse Holdings (SPWH) | 6.4 | 30.5 | 4.0 |

| Barnes & Noble Education (BNED) | N/A | 7.7 | N/A |

Takeaway

Based on the data provided, I can say that, while Party City has had a shaky operating history, the company could offer investors a nice amount of upside. Having said that, it appears to me as though management does not know quite what to do. They seem to be overly focused on growth at a time when they should be focused on cost-cutting and on lowering debt. Doing these things will have a much more positive impact on the company, especially as the risk level for it decreases in response to their actions. Generally speaking, I still find myself slightly bullish on the company. But if management were to make some necessary changes, I think that it could warrant a significant upgrade in terms of outlook.