David Becker/Getty Images News

Investment Thesis

Panasonic’s (OTCPK:PCRFY) shares have corrected 25% since our last piece in April 2021. We believe high input costs and continued Capex in the battery business will place pressure on margins and free cash flow generation in FY3/2023, and consensus estimates remain too bullish. However, with market expectations being generally low and the shares trading at book value, we upgrade our rating from sell to neutral.

Quick Primer

Panasonic Holdings Corporation is a Japanese electronics manufacturer. Its product lines span home appliances, lighting, auto parts, industrial systems, and automotive batteries. In April 2021, the company bought the remaining 80% interest in Blue Yonder Group (a leader in supply chain management software and SaaS) from Blackstone Group and New Mountain Capital for USD7.1 billion which was debt-funded.

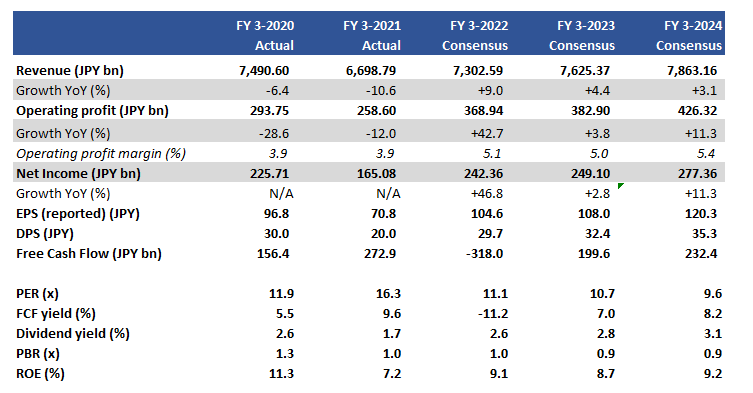

Key Financials With Consensus Estimates

Key financials (Refinitiv, Company)

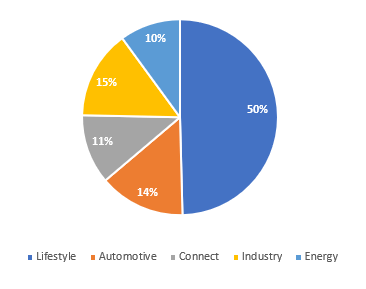

Q3 FY3/2022 YTD Sales Split By Business Segment

Q3 FY3/2022 sales split by business segment (Company)

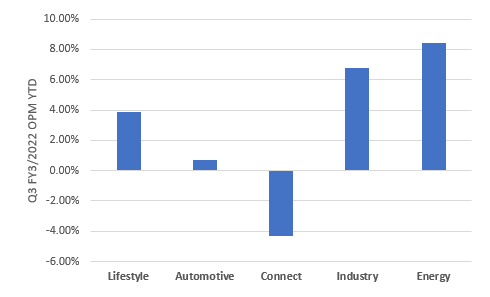

Q3 FY3/2022 YTD operating margin by business segment

Q3 FY3/2022 YTD operating margin by business segment (Company)

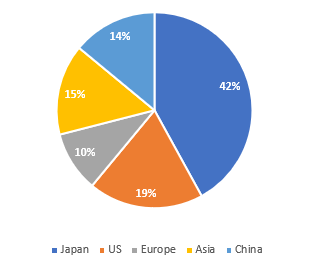

Q3 FY3/2022 YTD Sales Split By Geography

Q3 FY3/2022 sales split by geography (Company)

Our Objectives

The shares have seen a 25% drawdown since our last comment in April 2021. We want to assess the following:

- Understand why despite an earnings recovery YoY estimated for FY3/2022, the market has acted negatively toward the shares.

- The company has announced its latest group strategy on April 1st, 2022 to a muted response, and an IR day is planned for June 2022. What is the outlook for the company?

We will take each one in turn.

Unattractive Cash Burn

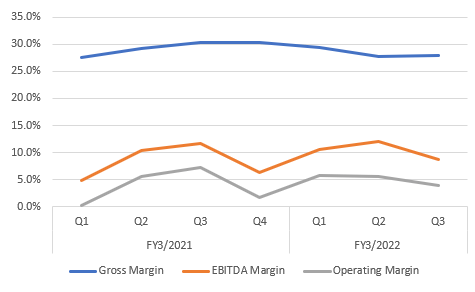

FY3/2022 was supposed to be a recovery year for Panasonic and initial signs were relatively positive. Despite a jump in profitability YoY in the Energy business (EV batteries), rising prices for raw materials began to dampen margins in the core Lifestyle (home appliances) and Connect (notebook PCs) businesses. We saw profit margins coming off in Q3 FY3/2022 which is a seasonally strong period.

Quarterly Margin Trend

Quarterly margin trend (Company)

Pressures over procurement meant an inability to complete production, placing working capital under pressure as inventories skyrocketed – there was also an element of hoarding parts and supplies. This led to operating cash flows declining to JPY104 billion/USD0.8 billion in Q3 FY3/2022 YTD, from JPY330 billion/USD3.0 billion in Q3 FY3/2021 YTD.

Both falling profitability and negative working capital have led to an estimated negative free cash flow of JPY318 billion/USD2.5 billion for FY3/2022. Investing activities have also risen as a result of the Blue Yonder acquisition as well as last FY benefitting from a one-time net positive transfer of assets.

As Panasonic entered H2 FY3/2022 it became evident that its business has limitations over how it can manage increasing input costs. Despite the majority of sales derived overseas, it is unable to benefit as an exporter (unlike Nintendo (OTCPK:NTDOY) and Sony (SONY)).

Although commodity prices are beginning to stabilize, we believe Panasonic will remain under pressure to manage working capital YoY. Next, we look at the outlook for the company.

Positive Messaging May Be Difficult

Consensus estimates show FY3/2023 to be a mild year of growth (4% sales and OP growth YoY), with a return to positive free cash flow generation. We believe this view is too positive for the following reasons.

Although prices may eventually revert to the mean, raw materials such as iron and copper prices show no signs of subsiding. Parts and materials shortages in semiconductors continue. Consequently, we expect to see margin pressure continue YoY with limited product price hikes – non-discretionary item prices (for example food and gas) tend to rise quicker than discretionary items (such as home appliances) which are more price elastic.

The group strategy presentation this month highlighted Panasonic’s appeal to be seen as an ESG play. The battery angle is fully involved in the push toward decarbonization, but despite this, the MSCI Implied Temperature Rise classifies the company as being ‘Misaligned‘. MSCI’s overall ESG rating is a respectable ‘AA’, but we note Refinitiv gives a lowly ‘C+’ rating in FY3/2021 due to a controversy over the loss of personal data from a breach after hackers gained access to its network. Another data breach was announced this month as the Canadian operation fell victim to a ransomware attack. Panasonic has been keen to stress its efforts to cut fixed costs, but these efforts may be misdirected.

The acquisition of Blue Yonder is expected to transform the company into a market-leading supply chain player in the age of IoT and edge services. We were slightly nervous to see that Panasonic has had to ‘re-evaluate assets and liabilities‘ (page 23) at Blue Yonder which meant higher amortization costs in Q3 FY3/2022. Although Blue Yonder’s Q3 FY3/2022 sales grew 11.8% YoY, we have some concerns that the net revenue retention (NRR) rate fell to 108% from 119% QoQ (page 24), denoting that existing customers are experiencing a sudden decline in satisfaction levels.

The most positive note is the Energy segment becoming the highest margin business in the company. Panasonic’s ties with Tesla (TSLA) are well-documented, but its joint venture with Toyota Motor (TM) to produce solid-state batteries may be the long-term kicker to earnings that the company needs. Although the product release will be for hybrids by 2025, it should enable Panasonic to scale its operations although it will inevitably require more investment. The 49% holding in the joint venture will also mean a limited impact on earnings.

Overall, we do not expect major negative surprises from Panasonic in the short to medium term but neither are we expecting much in terms of positive developments.

Debt Rating

Fitch Ratings affirmed its ‘BBB-‘ debt rating with a stable outlook for Panasonic in March 2022. It has had concerns previously with increasing leverage from the Blue Yonder acquisition and continued car battery investments, and rates the company with a weaker credit profile versus Sony, LG Electronics (066570.KS), and Lenovo Group (OTCPK:LNVGY). Interestingly, it is expecting a free cash flow deficit in FY3/2022 and FY3/2023.

Valuations

On consensus estimates the shares are trading on PER FY3/2023 10.7x and a free cash flow yield of 7.0%. These valuations are attractive. However, we believe consensus is being optimistic.

With the shares trading at book value, this looks like a fair valuation to us.

Risks

Upside risk comes from the Lifestyle and Connect segments seeing a major improvement in raw material prices. With improving supply chains, the company will see better working capital as well as recovering profitability.

In the short term, management may make some bold and positive announcements about future growth at the IR Day in June 2022. However, we believe the market will be in ‘wait-and-see’ mode.

Downside risk comes from continued raw material pressure, combined with a sustained need for Capex to scale the battery business. Both will have negative implications for free cash flow generation.

If management execution is seen to be inadequate, the market may take a dim view of how the company is being run.

Conclusion

Panasonic remains a work-in-progress in our view. The battery business is showing positive signs of recovery but the overall picture remains a low-return business with limited scope for improvement. Blue Yonder remains a key opportunity to remodel the business but the initial results are not conclusive.

Current consensus estimates and their resultant valuations look too positive. However, with a stabilized balance sheet and the shares trading at book value, we believe the shares are now fairly valued. We rate the shares as neutral.