Holding court in the back of upper Manhattan’s famed Hungarian Pastry Shop, a famous chess master once told me that the “best move is the move that does the most things for you.” It works both offensively and defensively, and ideally within several scenarios of each.

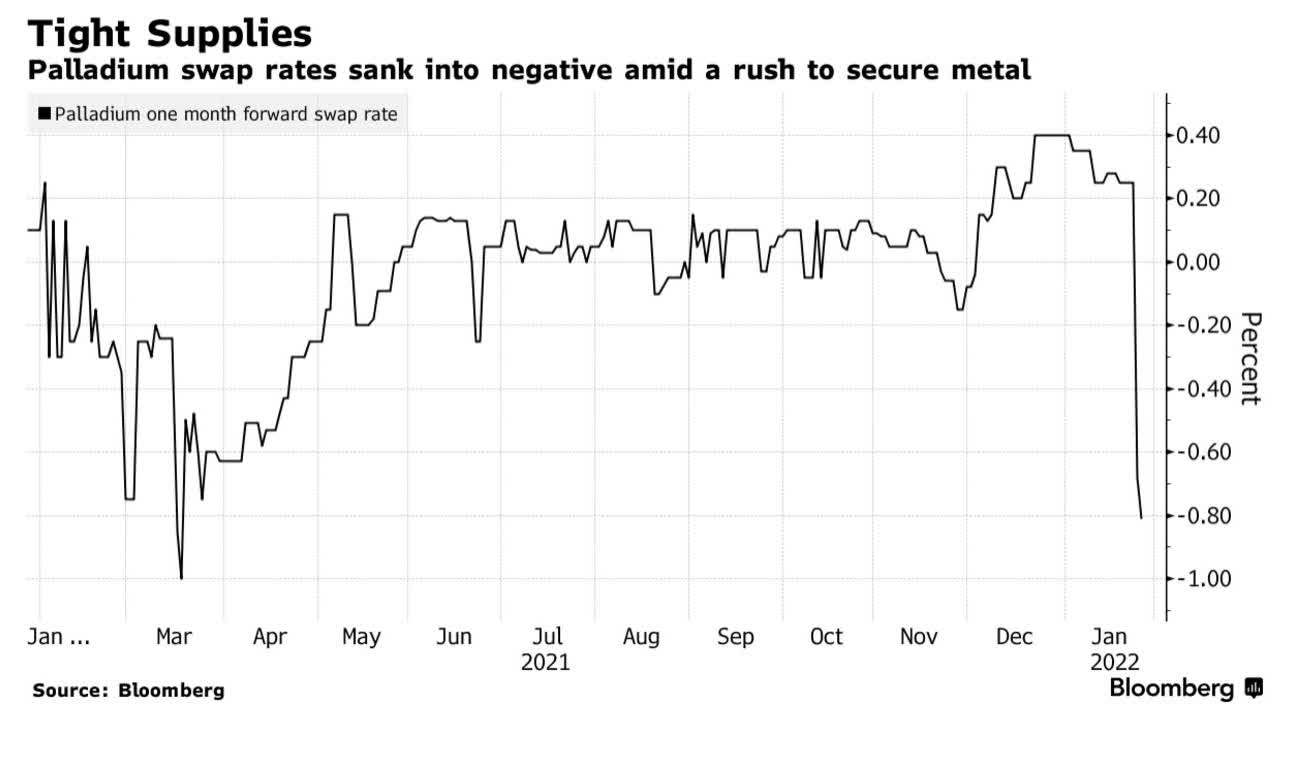

At this juncture, I see a long position in PALL – the Aberdeen Standard Physical Palladium Shares ETF (PALL) – as the proverbial best move. Palladium forwards recently dropped below the spot price as the market has tightened dramatically. PALL is the perfect vehicle to hedge geopolitical concerns, sidestep any further tech drawdown, and ride the expected bounce in auto production in late ’22 following the cessation of the chip shortage.

Palladium Swap Rates (Bloomberg)

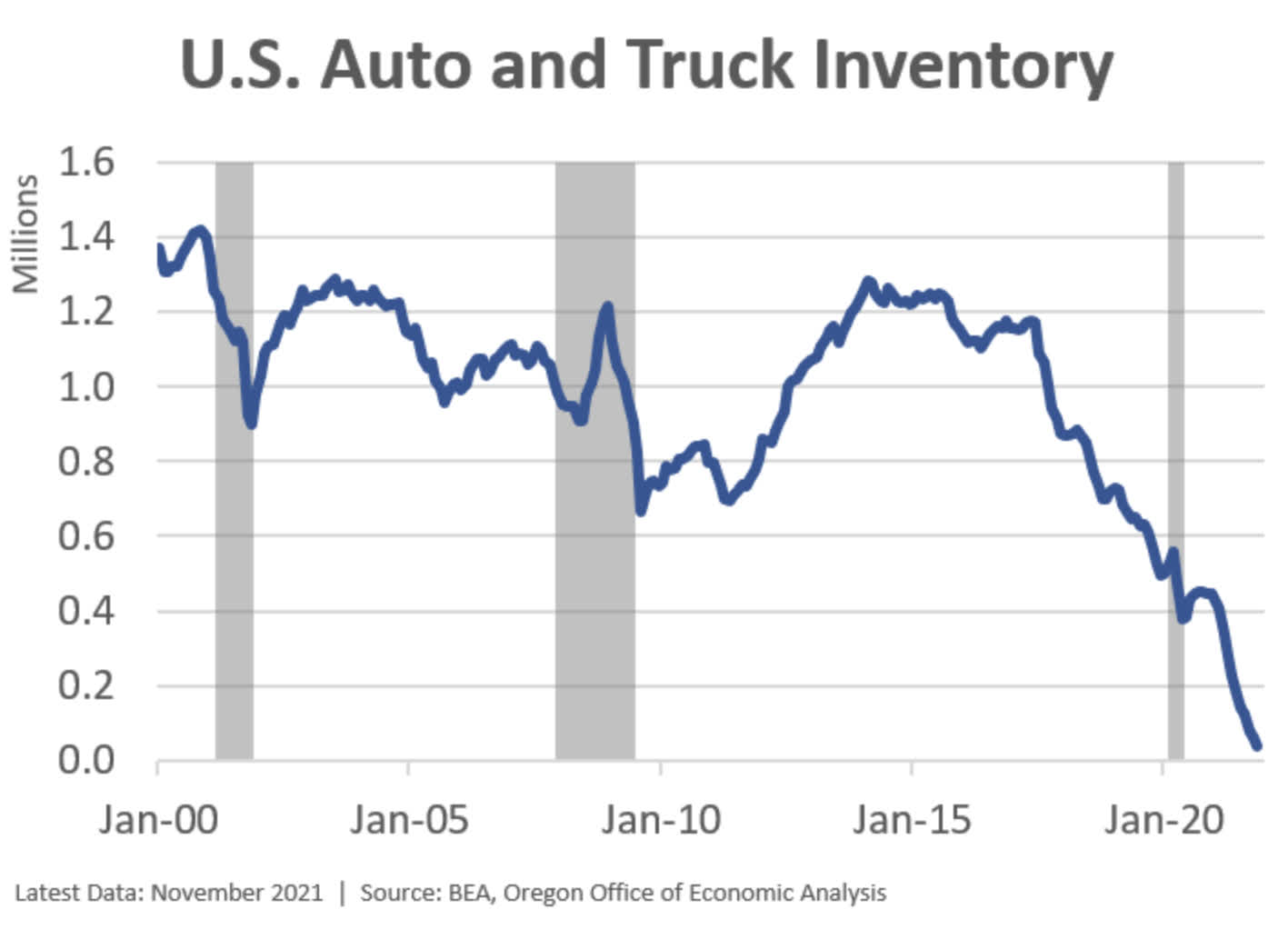

There are two structural issues at work. From the demand side: US auto inventory levels are at historic lows – in desperate need of replenishment – and gas-powered vehicles, which use palladium for their catalytic convertors, will remain more than 94% of the US market for the next three years. From the supply side: 78% of the world’s palladium comes from two nations that are experiencing acute operational risk at this very moment.

Also of note: the technical picture also looks auspicious.

The Demand Backdrop: Auto Production in 2022

The current auto chip shortage started primarily with devices – such as microcontrollers, power management, and display devices – made on legacy nodes at 8-inch foundry fab plants. The shortage then extended to other venues, with capacity constraints developing for substrates, wire bonding, passives, and materials, all of which were a part of the supply chain beneath actual chip fabrication.

There is little flexibility and excess capacity in these highly commoditized supply chains; this explains 2021’s suffocating constraints. But across most categories, chip shortages are expected to wane by the second quarter, with only some capacity crimps possibly extending to Q4 2022.

Ultimately, strong consumer demand and industry replenishment should make for a strong year, particularly in the second half. Again, US inventories are at historic lows:

US Auto and Truck Inventory – Nov 2021 (Oregon Office of Economic Analysis )

According to the National Auto Dealers Association: inventory levels at the end of December 2021 totaled 1.12 million units. Compared to December 2020’s 2.75 million units, this is down 59.1%!

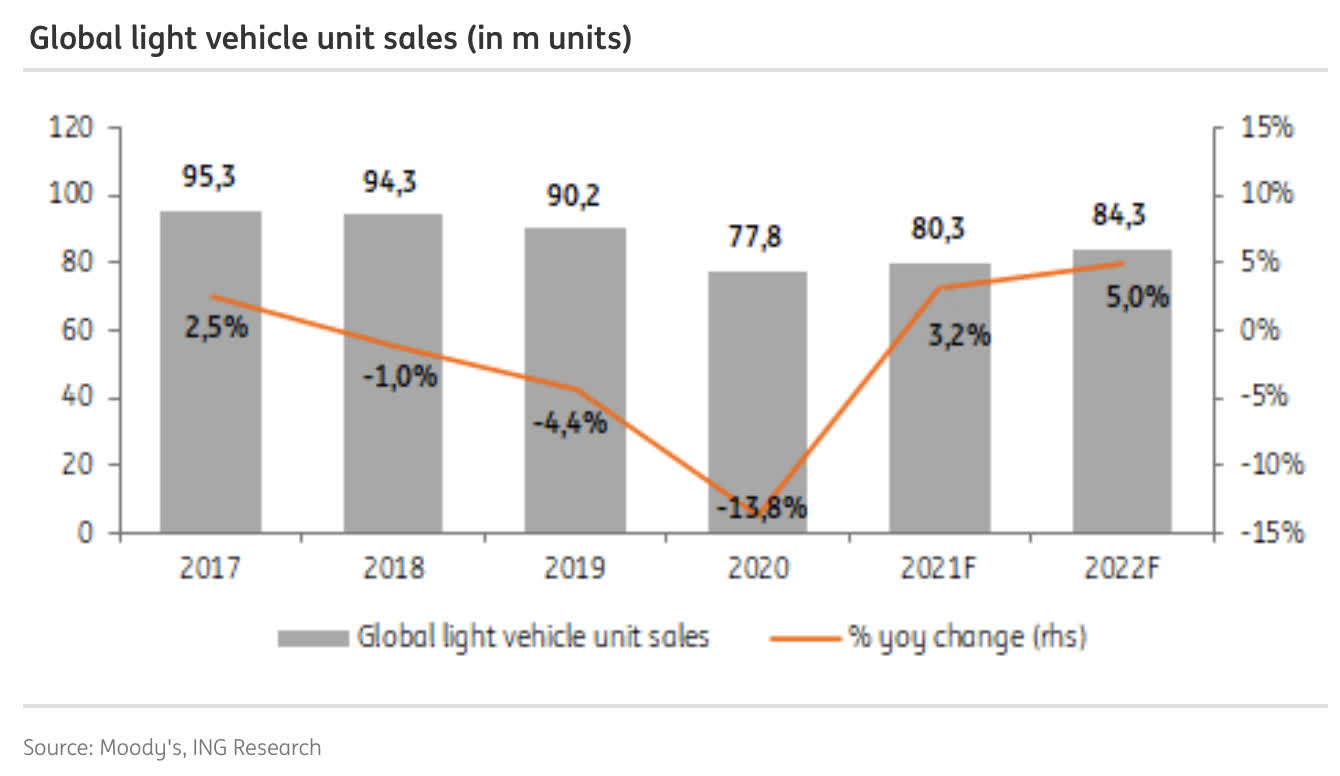

With the above backdrop in mind, late 2022 should see a vigorous recovery. Several analysts see global vehicle sales growing in the range of 4% to 6%, with production growth exceeding these rates by 2% to 3% in order to catch up from the lost volumes of 2021.

Global Light Vehicle Sales (in millions of units) (Moody’s; ING Research)

Analysts at Melbourne’s ANZ Bank suggest that palladium demand for auto catalysts will increase by 449,000 ounces this year, with a widening deficit in supply.

To address one cautionary note: some analysts expect a shift to platinum in gas-powered catalytic converters due to high palladium prices. As I have discussed elsewhere, platinum prices, the catalytic converter choice for diesel vehicles, have fallen along with their general ban in Europe. But palladium is preferred for gas-powered vehicles, and from a manufacturing standpoint this shift is not easily done. In addition, U.S. produces more than three times as much palladium as it does platinum, and Canada produces almost twice as much. Therefore, in case of a severe supply disruption from South Africa or Russia, global automakers recognize that they would have even more difficulty dealing with crimps in platinum than they would with palladium.

One final positive for the metals group as a whole: last week China decided to cut interest rates for the first time in two years, a day after PBOC Governor Liu said the central bank will “open the monetary policy toolbox wider, maintain stable overall money supply and avoid a collapse in credit.” Metal prices will be bolstered by Chinese efforts to maintain industrial growth while scripting a needed “soft landing” in housing.

The Supply Backdrop 1: Eskom Repairs

There is significant operational risk in the palladium market. Only 16% is mined in countries considered to have “low risk jurisdictions” like the US or Canada. Impala (IMPUY) has its sizable Lac des Iles Mine near Thunder Bay and speculative Canadian Palladium Resources (OTCQB:DCNNF) has its East Bull project in Gerow Township, Ontario.

In contrast, mines in “high risk” South Africa and Russia produce 78% of the world’s total supply. 2022 may be a perilous year for both nations.

South Africa is blessed with enormous PGM wealth and 38% of palladium is mined there. There is a problem, however: SA miners are inextricably linked to both a single utility – Eskom – for their electricity as well as higher platinum prices for their profitability. (Palladium makes up only about a third of the platinum-group output from South African mines.)

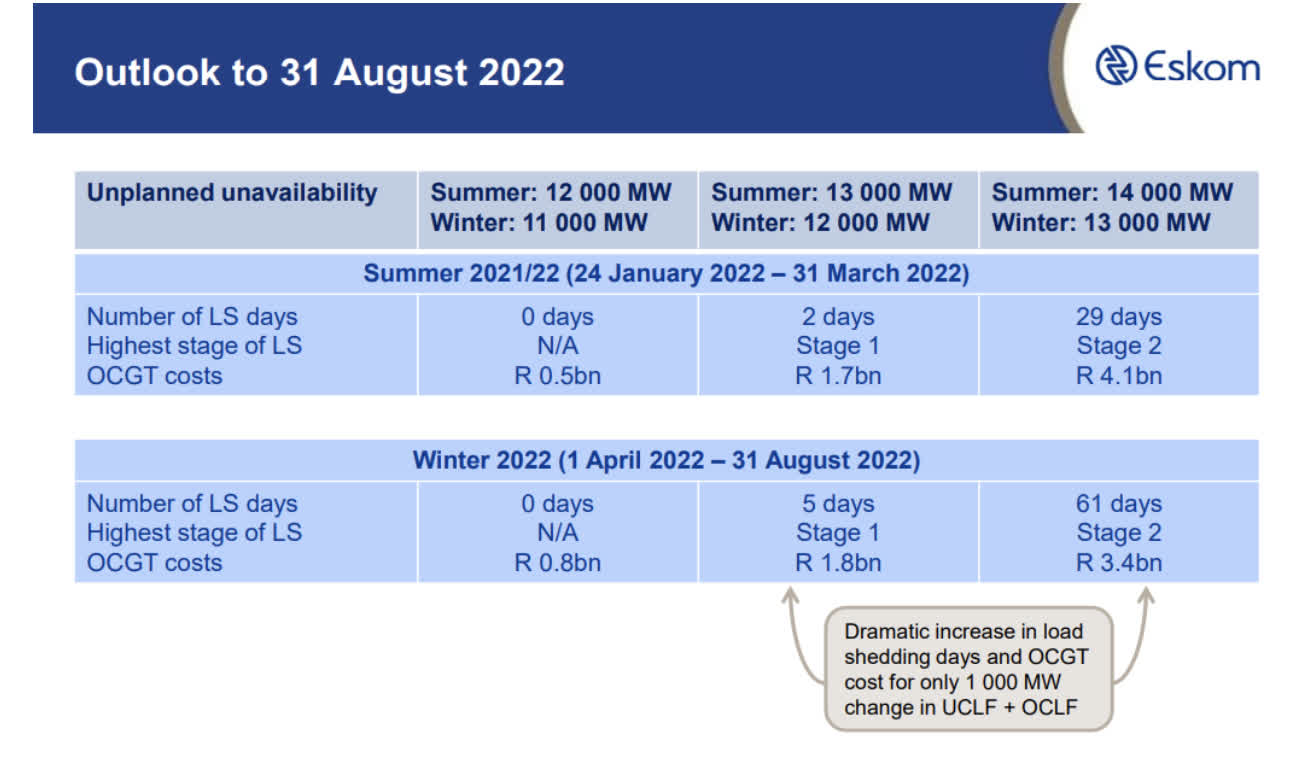

Eskom’s ongoing structural issues are well-documented in my 2019 report (back when PALL was $122!), but things haven’t improved. This public entity is still responsible for 95% of all electricity in the nation. Their “extend and pretend” policies of the past 15 years have clearly reached an impasse. In 2021, South Africa saw 51 days of load shedding – the highest on record.

Two weeks ago, Eskom revealed a plan for the staggered shutdown of two units at its Koeberg nuclear power station, an aging asset that probably would have been retired if in any other country.

The scheduled refueling and maintenance at Koeberg will occur over the next 10 months and add additional strain on an already overburdened power system. Unit 2 would be offline for five months before Unit 1 is switched off, also for a period of five months.

As it stands, most of Eskom’s power stations fail to meet South Africa’s energy demand and many fear the staggered repairs at Koeberg will only exacerbate an already dire situation. Vandalism is also a new issue: Eskom says vandalism cost it R200 million in the past year.

2022 will be a tough year for electricity use in South Africa with a lot of load shedding expected this summer. The utility has just stated it expects at least 80 days of load shedding by August 31. This could be disruptive for the local mines.

Eskom Load Shedding Schedule (Businesstech.co.za)

The Supply Backdrop 2: Russian Sanctions

Russia is the other wild card. It generates 40% of the world’s palladium and one can only imagine the commodity dislocation that might occur if a Ukrainian invasion precipitates the broad sanctions suggested by Washington.

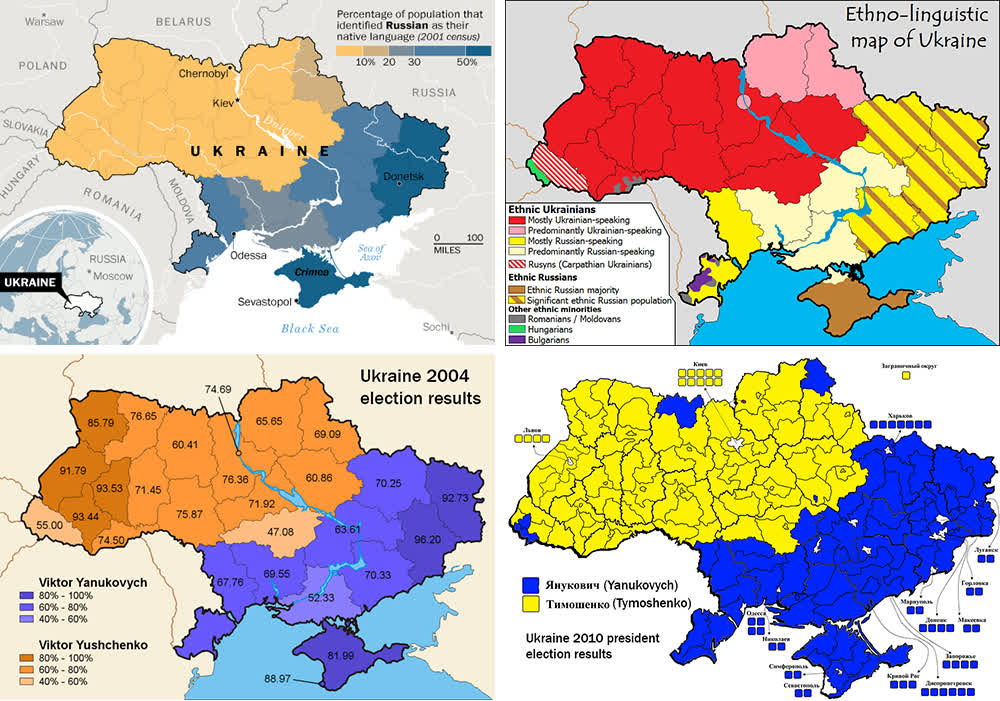

If you have studied the history of Ukraine, you will know that every election since 1994 has been a struggle between the true ethnic Ukrainian heartland of the Northwest and the Russian-speaking provinces of the East and South. Whether it be Kuchma / Kravchuk (1994) or Yushchenko / Yanukovych (2004) or the Euromaidan Revolution’s ouster of the pro-Russian Yanukovych (2014), there are enduring cultural rivalries at work. The following maps from Vox convey how the ethnolinguistic divide and the electoral divide essentially match up:

Ukraine’s Linguistic and Electoral Divide Overlap (Vox)

A recent Ukraine language law has only inflamed the issue. The new legislation promotes the use of Ukrainian in all public spheres, essentially enshrining it as the state language, a drastic departure from Yanukovych’s prior bilingual policy. An ambitious effort to eventually unify the country and culturally integrate the East and South, it has – at least in the near term – certainly alienated those regions and stoked Russian revanchism.

A Russian invasion that enacts de-facto control of eastern and southern Ukraine (particularly its Black Sea ports) via proxies is probably the goal of Putin’s efforts. Ukraine is expected to be the world’s fourth largest exporter of wheat and third largest exporter of corn in 2021/22 season, and most of its grain exports ship from the port cities of Mykolaiv and Odessa. Russia gets enhanced leverage over food and energy supplies at precisely the same moment as the West is roiling in temporary inflation and the Fed is managing an asset bubble.

Though there is no indication that metal exports will be sanctioned, the U.S. and EU have been weighing severe penalties on Russian banks. These include blacklisting Sberbank and VTB, crimping their ability to convert rubles for dollars and – most drastically – denying them use of the SWIFT messaging system. It is estimated that this could crater the Russian GDP by 5%.

That would certainly impact Russian exports. Indeed, Moscow itself might even use a halt in oil, gas, and metal transfers to Europe’s industrial heartland to coerce Germany from abiding by Washington’s harshest efforts. China will certainly work to re-route Russia’s exports if but to destabilize a Western Consensus and render Washington ineffectual.

Putin’s pre-war gambit could last through February, pressuring commodity prices. An outright war could spike the dollar and crash equities worldwide at least temporarily, but oil, natural gas, and palladium – in particular – should provide a hedge.

The Technical Backdrop:

The technical setup for palladium looks very good. It is sort of a Dogs of the Dow scenario.

Palladium was the worst performing commodity in 2021 – down 22%. Looking at a 3-year weekly chart, you can see that PALL endured a serious bottoming in mid-December 2021 – with an “abandoned baby doji” and midday action on Dec 15 that touched a major March 2019 support/resistance line around $143.

3 Year Weekly PALL Chart (StockCharts.com)

More tactically, there was a recent gap-up on Jan 26 that cleanly broke above a $205 Nov 17th resistance line. This creates the impression of an island reversal, lurching out of the Nov/Dec/early Jan lows.

For the coming weeks, PALL should consolidate and trade raggedly within the same broad channel between $210 and $230 that it established from Oct 2020 to Feb 2021. Better clarity on the chip shortage might drive this thinly traded precious metal ETF to $245 by mid-May.

claffra/iStock via Getty Images