Occidental Petroleum (OXY) has been severely punished by the market for its acquisition of Anadarko for $38 billion. Since Occidental prevailed over Chevron in the bidding war in May, the former has plunged 30% and is now trading around its 14-year lows. Despite the increased risk that has resulted from the excessive debt load of the company, it seems that the market has overreacted and has thus led the stock to bargain territory, particularly given its 7.7% dividend yield.

Debt

As the aforementioned cost of the acquisition was slightly higher than the current market cap of Occidental ($37 billion), it is only natural that the market feared that the acquisition may prove too large for the company to assimilate. This acquisition has greatly increased the debt load of the oil producer. As per the latest quarterly report, the net debt of Occidental (as per Buffett, net debt = total liabilities – cash – receivables) currently stands at $73.7 billion. As this amount is essentially twice as much as the market cap of the stock, it is alarming, at least on the surface.

However, it is critical to note that Occidental executed the acquisition from an exceptionally strong financial position. To be sure, the oil producer enjoyed an A/A3/A credit rating from the three major credit rating firms before the acquisition and its net interest expense was consuming only 5% of its operating income back then. Extremely few companies can boast of such a strong financial position right now.

Moreover, after the merger, in the most recent quarter, net interest expense consumed 45% of operating income. On the one hand, this steep increase confirms that the balance sheet has greatly weakened after the costly acquisition. On the other hand, Occidental can still cover its interest expense with a meaningful margin of safety. Even better, the company has repeatedly stated that it will sell some assets of Anadarko and will also use the excess free cash flows to reduce its debt load. As the company generates positive free cash flows at oil prices above $40 and the price of oil is likely to remain above that level for the foreseeable future, Occidental is likely to reduce significantly its debt load in the upcoming years.

Hedging

The main reason behind the extreme punishment of the stock by the market is the increased risk of the stock. Due to its leveraged balance sheet, Occidental has become much more vulnerable to low oil prices than it was before the acquisition. As oil prices experience dramatic swings from time to time, the risk of Occidental has undoubtedly increased after its acquisition.

However, Occidental decide to hedge its production in order to reduce its risk. According to a source, Occidental will sell 110 million barrels of oil at a minimum price of $55 this year if the actual price of oil remains above $45. The company also hedged a portion of its production in 2021. This strategic decision protects the company to a great extent from the gyrations of the oil prices and thus renders its free cash flows much more reliable.

On the other hand, investors should keep in mind that there is no free lunch in this market. Due to its hedging positions, Occidental has essentially capped its profits for the next two years and hence it will hardly benefit from a strong rally of the oil price above $74. While such a scenario seems unlikely right now, oil prices often experience surprising moves and hence the cap on potential profits is a negative for an oil producer. Nevertheless, given the extreme sensitivity of the company to the prevailing oil prices, the hedging decision seems warranted right now.

Growth

In its last earnings report, Occidental announced that it will reduce its capital expenses by 40% in 2020, from a proforma amount of $9.0 billion to $5.4 billion. As a result, the oil producer now expects to grow its production by only 2% this year, much less than the 5% growth rate it expected previously. Consequently, the stock plunged 5% on the day of its earnings release.

On the one hand, the announcement confirmed the market’s fears that the excessive debt will negatively affect the growth trajectory of Occidental. On the other hand, the company still expects to grow its production by 5% next year, as it intends to boost its capital expenses to $6.6 billion next year. Moreover, Occidental will be assisted by the great synergies from the acquisition of Anadarko, whose acreage is located in the middle of the core development area of Occidental and hence it is ideally positioned to benefit from the supply chain of the latter. Overall, Occidental expects to achieve $2.5 billion of annual synergies by the end of this year and $3.5 billion of annual synergies in 2021.

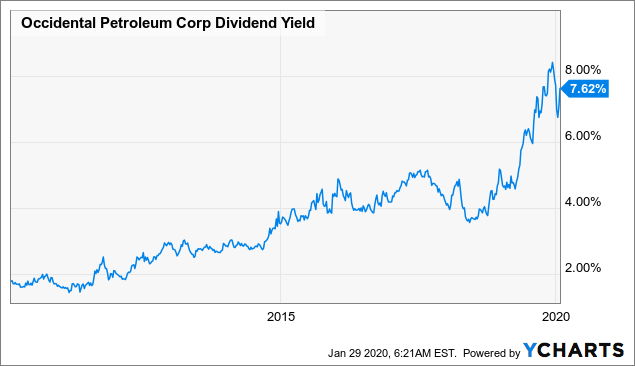

Dividend

Occidental has an enviable dividend growth record, as it has raised its dividend for 17 consecutive years. This is an exceptional dividend growth streak in the energy sector, which is infamous for its high cyclicality. Moreover, thanks to its depressed stock price, Occidental is currently offering a nearly all-time high dividend yield of 7.7%.

Data by YCharts

Data by YCharts

Unfortunately, due to the temporary plunge of the earnings of the company in the aftermath of its gigantic acquisition, we will have to wait for a few quarters in order to evaluate the safety of the dividend based on the payout ratio. Just before the acquisition, the payout ratio was 57%, an undoubtedly healthy level. Due to the increased interest expense, the payout ratio will spike in the upcoming quarters but it is likely to return to healthy levels as the deleveraging process progresses.

Moreover, management has repeatedly stated, even after the acquisition of Anadarko, that the company fully covers its dividend at oil prices above $40. As the price of oil is not likely to plunge to this threshold for an extended period anytime soon, the dividend seems safe for the foreseeable future.

Final thoughts

The acquisition of Anadarko greatly increased the sensitivity of Occidental to the underlying oil prices. As the market hates uncertainty, it is only natural that it punished Occidental harshly for its high leverage. However, as usual in similar instances, the market seems to have punished the stock to the extreme. Occidental will reduce its debt load in the upcoming years thanks to asset sales and its excess free cash flows. As a result, it will reduce its inherent risk while it will also enhance its earnings per share thanks to lower interest expense. Given also its 7.7% dividend, the stock is likely to highly reward those who purchase the stock despite the current negative market sentiment.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.