Justin Sullivan/Getty Images News

A multitude of headwinds has undoubtedly been weighing on the Nvidia (NASDAQ:NVDA) stock’s performance this year. Macroeconomic challenges like the Federal Reserve’s current plan to increase rates by 5-bps increments coming June and July are risking erosion of future valuations and a potential recession to the broader economy. This has also heightened concerns on industry-specific challenges like signs of semiconductor inventory build-up following a strong, multi-year boom, which is a 180 from the ongoing industry-wide shortage. Meanwhile, Nvidia is also facing company-specific headwinds from a potential slowdown in GPU take rates due to softening gaming and crypto demand (yes, for those who have been following, I am finally addressing crypto’s impact on Nvidia).

But the company’s fiscal first quarter fundamentals have continued to trump the speculative overhang. Nvidia finished the first quarter with another solid sales and earnings beat as expected. Specifically, data center and gaming revenues continued to demonstrate robust growth, which is consistent with strong results observed across cloud service providers. However, some investors were taken back by the estimated $500 million in lost revenues stemming from the Russia-Ukraine war and COVID-related lockdowns in China, as well as management’s warning of a “challenging macroeconomic environment” in the near term.

Looking ahead, we continue to see Nvidia as the backbone and enabler of key innovative themes ahead. With the stock’s performance still paradoxical to the value it adds to innovation and its growth prospects alongside the continued development and scalability of emerging technologies like autonomous driving, robotics, cloud computing, and the Omniverse, Nvidia remains a compelling long-term investment opportunity at current levels.

Brief Update on 1Q23 Fundamentals

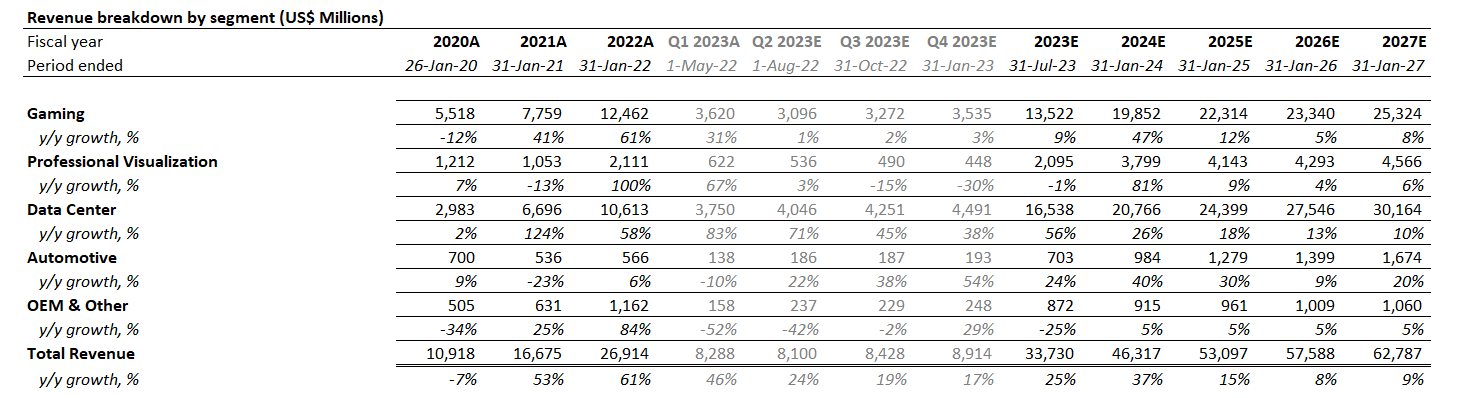

Nvidia reported first quarter revenues of $8.3 billion (+46% y/y; +8% q/q), beating consensus estimate of $8.09 billion (+43% y/y; +6% q/q) and its previous guidance of $8.1 billion (+43% y/y; +6% q/q). Gaming segment represented 44% of consolidated sales, with growth of 31% from the same period in the prior year (+6% q/q) to a record-setting $3.6 billion. Data center sales also maintained strong double-digit year-on-year growth of 83% (+15% q/q) to $3.75 billion in the fiscal first quarter, and now drive 45% of consolidated revenues. Meanwhile, automotive’s performance remained soft in comparison as expected, largely due to continued car production challenges observed across OEMs in the first quarter due to supply chain bottlenecks that have been further exacerbated by recent COVID-related lockdowns in China.

Despite rising input costs, Nvidia also posted a fiscal first quarter earnings beat at $1.36 per share, compared with consensus estimate of $1.29 per share. Net income totalled $1.6 billion (-15% y/y; -46% q/q), thanks to robust gross margins of close to 66% (+140 bps y/y; +10 bps q/q) and free cash flow margins of 16%.

For the fiscal second quarter, Nvidia is guiding revenues of $8.1 billion (+24% y/y; -2% q/q), which is slightly down from consensus estimates of $8.5 billion (+31% y/y; +3% q/q) due to an estimated $500 million negative impact from the ongoing Russia-Ukraine war and protracted COVID-related lockdowns in China. Specifically, data center revenues will continue to benefit from strong cloud computing uptake while gaming revenues will see some normalization to previously tight inventory levels, with sequential revenue declines estimated “in the teens”. Gross margins will also see some slight decline to 65.1%, as management continues to press forward with cost-cutting measures that include a “slowdown to its hiring pace” to counter near-term macroeconomic headwinds.

Pioneering Innovation with Innovation

Despite looming macroeconomic challenges, Nvidia’s unwavering commitment to bettering the performance of its existing hardware and software offerings continues to bolster its longer-term growth prospects ahead. This also pairs especially well with the long-view bullish demand environment buoyed by ongoing technological innovations spanning self-driving vehicles and next-generation robotics to virtual worlds.

Data Center PCIe Liquid-Cooled GPU Debut

Nvidia has recently introduced its first data center GPU equipped with liquid cooling technology, pushing the boundary in next-generation computing beyond performance. The newly unveiled A100 PCIe GPUs will be the first of the PCIe series of data center graphics processors to be equipped with liquid cooling technology. With shipments beginning in the third quarter, the A100 PCIe GPUs will “deliver the same performance (as regular A100 GPUs) for less energy, enabling enterprises with options to deploy green data centers”.

The newest development will address issues like climate change from its source, in addition to enabling next-generation AI technologies and high-performance computing (“HPC”) deployed in solving similar complex problems. It also complements how Nvidia’s GPUs already “deliver up to 20x better energy efficiency on AI inference and HPC jobs than CPUs”. Running data center servers on “GPU-accelerated systems” already reduces the industry’s annual energy consumption levels by 11 trillion watt-hours per year – to put into perspective, that is equivalent to annual energy consumption at more than 1.5 million homes. The addition of liquid cooling capabilities will further reduce data center energy consumption by 30%, which effectively catapults Nvidia’s efforts in pioneering computing performance measured by carbon impact going forward.

The increasing urgency to reduce global carbon emission levels and tame climate change has accelerated the incorporation of ESG considerations across the enterprise sector worldwide. This is further corroborated by the rapid expansion of the green bonds market in recent years, which grew by $500 billion in 2021 alone (+50% y/y). Over the next three decades, capital spending aimed at driving net emissions down to zero is expected to reach $275 trillion, or approximately $9.2 trillion per year. Meanwhile, global demand for AI hardware (e.g., data center processors) is expected to accelerate at a compounded annual growth rate (“CAGR”) of 43% towards $1.7 trillion by the end of the decade. The statistics, along with the increasing demand for data center hardware, underscore the additional growth opportunities unlocked by the high-performance, yet low-energy-consuming, processors that Nvidia has to offer.

Accelerating AI Development

Nvidia’s leading expertise in AI development is being proven again through its role in the gradual transformation of modern data centers into “AI factories”. With the upcoming deployment of the “Grace CPU Superchip“, new GPUs based on the “Hopper Architecture” like the “NVIDIA H100“, as well as the “NVIDIA BlueField DPUs“, Nvidia seeks to address some of the next-generation AI workload processing needs at both the hardware and software level.

As mentioned in the earlier section, Nvidia’s GPUs have made significant contributions to improving both the performance and energy efficiencies of data center operations in recent years. The newest H100 GPUs based on its latest Hopper Architecture are capable of training massive AI models at up to 9x faster speeds, and a just handful of them can “sustain the equivalent of the entire world’s internet traffic”. Nvidia’s technology has also accordingly driven down the costs of AI development significantly over the years. Think about it this way – massive and complex models such as Mixture of Experts with 395 billion parameters which previously might have taken a week to train using the predecessor A100 GPUs can now be done in a little under 19 hours using the H100. And by next year, with Nvidia’s liquid cooling technology coming to the H100, all of this improved performance can be achieved for even less energy consumption, enabling both cost and time efficiencies to enable further scalability of AI development.

Accompanying the H100 GPUs is the “NVIDIA DGX” system. The DGX system offers a family of hardware that leverages Nvidia’s existing expertise in GPUs used in training, storing, and managing complex AI and HPC workloads with high, scalable performance. The latest DGX H100 is the “world’s first AI platform to be built with the new NVIDIA H100 GPUs”, enabling faster performance in training massive AI workloads like “language models, recommender systems, healthcare research, and climate science”. Equipped with eight H100 GPUs, the DGX H100 system is capable of delivering up to 6x more performance than previous systems built with the A100 GPUs, which as mentioned previously, will make significant contributions to the continued scalability of new AI developments.

The newest DGX H100 system also includes two “NVIDIA BlueField-3” data processing units (“DPU”). Dubbed the “third-generation data center infrastructure-on-a-chip”, BlueField-3 is capable of delivering some of the most powerful performance capabilities across “software-defined networking, storage and cybersecurity acceleration”. The DGX H100 system enables a significant leap in the performance of Nvidia’s next-generation AI infrastructure platforms, which include “NVIDIA DGX POD” and “NVIDIA DGX SuperPOD“.

Nvidia’s next-generation hardware and software developments around AI technology continue to satisfy the performance requirements for training “massive models in industries such as automotive, healthcare, manufacturing, communications, retail, and more”. This accordingly drives Nvidia to benefit from the creation of new addressable markets and grow alongside the vast opportunities stemming from continued innovation. These include increasing demand for performance across “partners in data centers, HPC, in digital twins, and cloud-based gaming”, which management alludes to as a “half-trillion market opportunity“.

Capitalizing on the Age of Robotics

The recent supply chain bottlenecks and labour constraints have highlighted the increasingly critical role that automated robotics play in enabling “manufacturers’ flexibility and responsiveness to demand spikes”. Market data shows that the implementation of robotics in industrials has accelerated over the past 10 years, with take rate expanding at close to a 20% CAGR over the same period.

This development is consistent with one of the first interactions with industrial robotics we have had about six years ago, where automated packing and logistics robots (autonomous mobile robots, or “AMRs”) roamed around a client’s distribution warehouse on designated tracks carved into the floor to fulfil tasks from the receiving bay all the way to the shipping dock. At the time, the client was already preparing for the deployment of a new distribution warehouse, which featured automated logistics that did not even require carved-out tracks on the floor at all. Since then, automation driven by developments in robotics has only further improved to enable new services like Amazon’s (AMZN) one-day delivery, driving additional value to society without adding to demand for labour.

The burgeoning demand for industrial robotics is favourable to Nvidia’s continued software developments in the Omniverse, as well as hardware developments in robotics. The latest launch of “NVIDIA Jetson AGX Orin” curated for AI use-cases in autonomous machines is expected to further accelerate the implementation of robotics across production lines, driving increased operational and cost efficiencies while enabling new growth opportunities ahead for Nvidia.

Recent developments like the Jetson AGX Orin also bode well for “NVIDIA Isaac“, the company’s robotics platform that provides related end-to-end solutions from “development to simulation to deployment”. On the development front, Nvidia has recently introduced “Isaac NOVA Orin“, which will be made available later in the year. The Isaac NOVA Orin is a purpose-built sensor platform for AMRs, which is similar to the “DRIVE Orin” and “DRIVE Hyperion 8” sensor suite built for autonomous driving systems in passenger vehicles discussed in our previous coverage. Leveraging Jetson AGX Orin’s “next-generation deep learning and vision accelerators” features, Isaac NOVA Orin is capable of “simultaneous camera capture synchronization and global timestamping across sensors”.

On the simulation front, the NVIDIA Isaac family of products includes “Isaac Sim“, a synthetic data generator powered by “Omniverse Replicator“. Isaac Sim leverages training data obtained from Replicator-generated digital twins to “build and deploy AI-enabled robots” under a safe and controlled environment.

And on the deployment front, NVIDIA Isaac also includes a new AMR platform, the “Isaac AMR“. The Isaac AMR incorporates “mapping, site analytics, and fleet and route optimization capabilities” powered by Nvidia’s AI technologies, including Metropolis, ReOpt, DeepMap, and other Omniverse platforms such as Isaac Sim. The optimization capabilities enabled by Isaac AMR are expected to generate billions of dollars in annual savings for the logistics industry by streamlining the deployment process. Nvidia has also introduced “NVIDIA Fleet Command“, a complementary purpose-built software for AMR fleet management. The end-to-end solutions enabled by Nvidia’s family of both hardware and software offerings make it an attractive solution ahead of growing AMR deployment opportunities across warehousing sites driven by increased e-commerce demand and labour digitization trends in coming years.

Nvidia’s Role in Crypto and Blockchain Technology

Addressing some of our readers’ queries on how the recent fallout in cryptocurrency performance is going to impact Nvidia’s outlook, the biggest headwind remains on the “reduced pace of increase in Ethereum network hash rate”, which has weighed on mining activity on GPUs. While gaming segment revenues attributable to Nvidia’s “CMP GPU” dedicated for cryptocurrency mining are likely immaterial, the company has recently disclosed a year-on-year decline of 52% in related sales. This is consistent with both the recent slump in the price performance of crypto assets, as well as the upcoming transition from proof-of-work to proof-of-stake on the Ethereum blockchain following the Merge.

The transition will eliminate the need for mining Ether altogether, which will significantly reduce the requirement for crypto mining GPUs. While proof-of-work has historically required the contribution of high computing power to solve unique cryptographic algorithms for each transaction on the Ethereum blockchain in exchange for an Ether reward, the transition to proof-of-stake will instead require Ether holders to “stake” their Ether as a validation mechanism for transactions in exchange for an Ether reward.

The transition from proof-of-work to proof-of-stake largely addresses the increasing concern of environmental impacts stemming from cryptocurrency mining. Historically, proof-of-work requires computing power to solve complex algorithms on the blockchain. And over time, with a larger transaction trail on the blockchain, the amount of computing power needed to solve the unique problems that come with each additional transaction increases, meaning higher energy consumption and higher impact on the environment.

Although the transition to proof-of-stake is going to impact some of Nvidia’s GPU sales in the near term, as observed in the latest quarter’s 52% year-on-year decline related to its crypto mining CMP GPU sales, the company always has a way in benefiting from value creation through innovation. As mentioned in earlier sections, we view Nvidia has the backbone and enabler of key innovations ahead. For now, proof-of-stake is not without its challenges. There have already been rising concerns over the long validation queues (i.e., time to validate Ethers staked) on the Ethereum blockchain, which could go for as long as years. The Ethereum blockchain currently plays a fundamental role in decentralized finance and is foundational to many Web3 transactions, such as NFT issuances. And as demand for transactions on the Ethereum blockchain continues to rise, it will only be a matter of time that innovation finds a solution to this bottleneck – just like how proof-of-stake was developed as one of the solutions addressing the environmental impact of proof-of-work. And again, semiconductor technology – like those offered by Nvidia – will continue to play a critical role in realizing this solution, underscoring its growth prospects alongside the continued development of blockchain technology over the coming years.

Fundamental Forecast Update

Adjusting our latest Nvidia financial forecast for its actual fiscal first quarter financial results, and growth outlook based on recent technological developments discussed in the foregoing analysis, the company remains on a positive track towards strong double-digit revenue growth in the current year. Total revenues are expected to grow 25% to $33.7 billion by the end of fiscal 2023, with further expansion at a 13% CAGR through fiscal 2027.

Much of Nvidia’s success will continue to dwell on its higher-margin data center sales growth, driven by continued strength in cloud-computing spending. This is also corroborated by the segment’s strong topline performance in the fiscal first quarter, with its revenues surpassing those of Nvidia’s gaming segment for the first time. As mentioned in some of our previous coverages, cloud computing has become a tool of survival for the enterprise sector. More than half of the corporate scene has expressed that they would rather “tighten the belt” in other parts of the business than to miss out on digital transformation, which is considered a strategic investment in differentiating themselves from competitors while also enabling cost efficiencies. And Nvidia’s corporate strategy in combining both hardware and software offerings is expected to help it maximize penetration into related opportunities over the coming years.

Nvidia Revenue Forecast (Author)

Nvidia_-_Forecasted_Financial_Information.pdf

Valuation Update

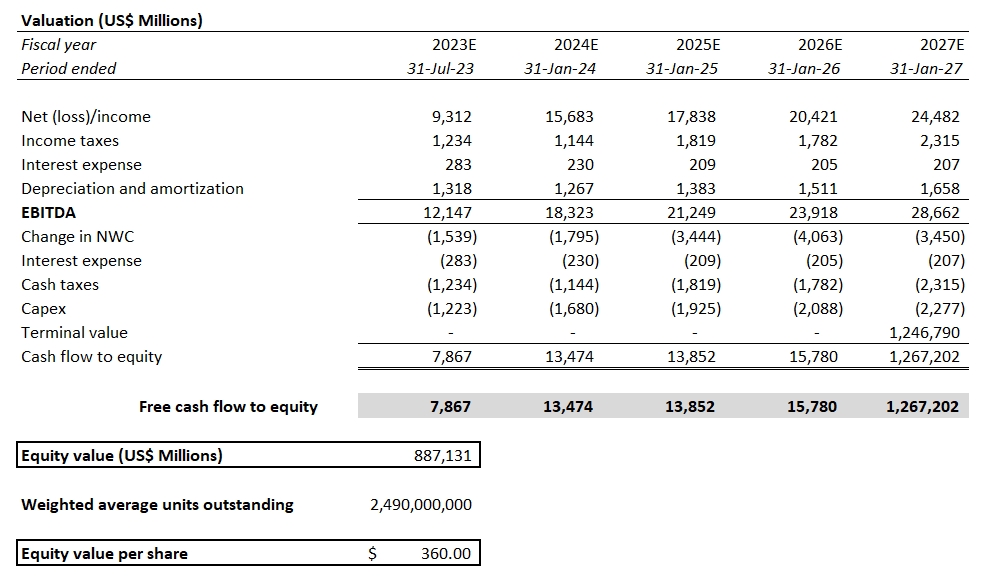

Nvidia Valuation Analysis (Author)

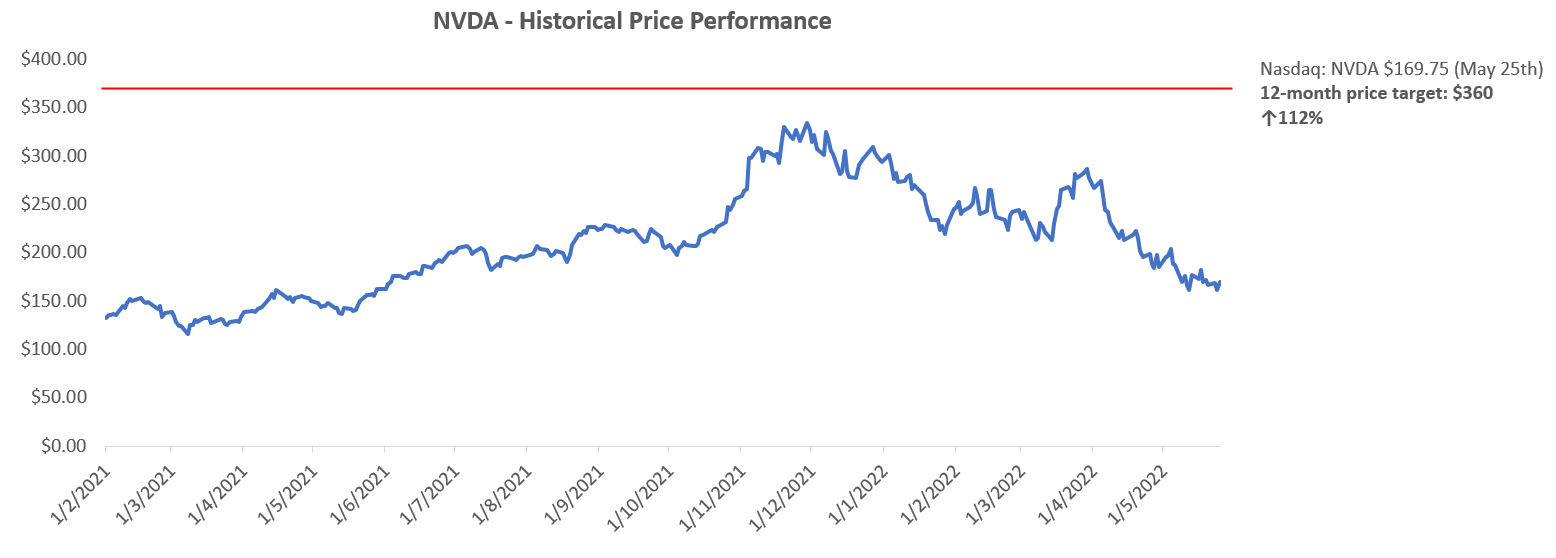

Our near-term price target for the stock remains at the $360-level, considering its fundamental growth thesis has not materially altered from our most recent coverage on the stock, offset by continued valuation multiple compression across the peer group due to the recent market climate. This represents an upside potential of 124% based on the stock’s per share price of $161 in pre-market trading May 26th.

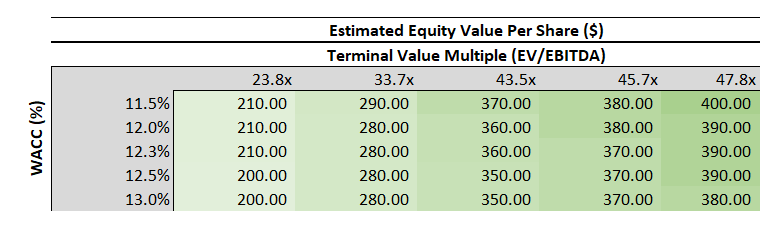

Nvidia Valuation Analysis (Author) Nvidia Sensitivity Analysis (Author)

Conclusion

Nvidia remains the powerhouse behind a slew of emerging technologies that are gradually entering mass-market adoption. In addition to continued data center strength buoyed by the importance of cloud computing and other AI developments over coming years, Nvidia is also poised to benefit from market share gains from both a hardware and software perspective across fast-growing industries like autonomous mobility, robotics, virtual reality. Continued improvements to semiconductor hardware and AI software offered by Nvidia, as well as developments to emerging technologies will remain mutually reinforcing forces, enabling scalability and cost declines to drive greater value and growth for the stock over the longer term.

Author’s Note: Thank you for reading my analysis. Please note that we will be launching a Livy Investment Research Marketplace service on June 1. The service will allow you to follow my coverage portfolio, interact with me directly, and participate in chat rooms with other subscribers. Stay tuned for more details as we ramp up to launch.