Thesis

Northern Dynasty Minerals (NAK) is a Canada-based mineral exploration and development company whose share price has seen a significant roller coaster ride during the past six months. As we move ahead in H2 2020, I expect this price volatility to continue and advise the investors to exercise caution while initiating a position in this company, at this point.

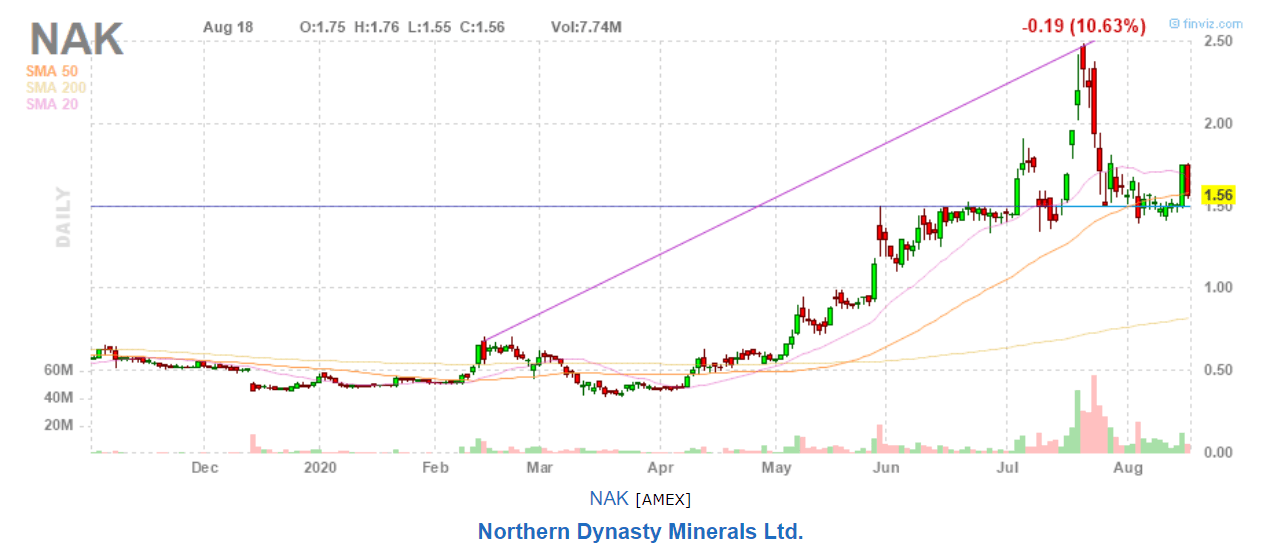

In this article, we will discuss three things. First, the long-term attractive mining outlook of NAK’s flagship asset; the Pebble Project. Next, we will consider two significant near-term catalysts that fuel the share price upside in NAK. Finally, since a recent political risk has become headline news for the stock (and could potentially hurt the stock’s performance, going forward), I expect the volatility in NAK’s share price to continue in the near term. As such, it merits to say that investors should carefully watch the project development scenario during the remainder of the year and avoid initiating a position even at the currently distressed prices (Figure-1). Let’s get into the details.

Figure-1 (Source: Finviz)

Robust fundamentals indicate a valuation gap

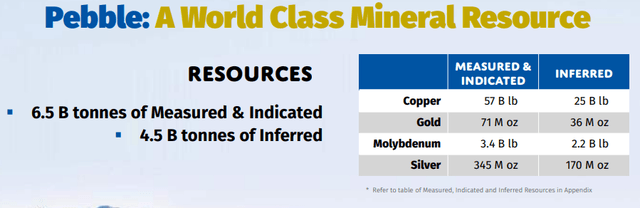

Let’s talk numbers. NAK’s ‘Pebble’ project is expected to contain a massive mining resource amounting to 6.5 BB tons in M&I (read: Measured & Indicated) Resources and 4.5 BB tonnes in Inferred Resources. So, how does this resource concentrate bifurcate into different metals? In terms of M&I resource, these numbers amount to 57 BB lb of copper, 71 Moz of gold, 3.4 BB lb of molybdenum, and 345 Moz of silver. In terms of Inferred resource, they amount to 25 BB lb of copper, 36 Moz of gold, 2.2 BB lb of molybdenum, and 170 Moz of silver (Figure-2).

Figure-2 (Source: Presentation – August 2020, pg.4)

I know it makes little sense to compare a future miner with a fully-operating mining company, but I’m doing that to make a point here. For reference, let’s only consider NAK’s total gold resources (and ignore the copper-silver-molybdenum resource for a while). The total resource in both ‘M&I’ and ‘Inferred’ categories amounts to 107 Moz of gold. Regardless of the future cost of mining those gold ounces (which are purely gold ounces and if converted into gold-equivalent ounces by adding the underlying copper-silver-molybdenum resources, the total gold-equivalent resource would be considerably higher), and even if we assume NAK to contain only 107 Moz of gold, this resource massively exceeds the reserves and resource estimates (check columns B, C, & F in Table-1 here) of many established gold miners operating in Tier-1 to Tier-3 jurisdictions, by approximately 2-3 times. However, the price tag of NAK compared with those companies indicates a significant valuation gap provided the Pebble project can make it through the regulatory permitting process. Check the table below.

|

Company and Ticker |

Last Price (as on August 17) |

Nature of business |

|

Northern Dynasty (NAK) |

$1.75 |

Primarily copper-and-gold ‘future’ miner |

|

Alamos Gold (NYSE:AGI) |

$10.74 |

Primarily gold miner |

|

B2Gold (NYSEMKT:BTG) |

$7.18 |

Primarily gold miner |

|

Harmony Gold (NYSE:HMY) |

$6.25 |

Primarily gold miner |

|

Kinross Gold (NYSE:KGC) |

$9.30 |

Primarily gold miner |

|

Yamana Gold (NYSE:AUY) |

$6.31 |

Primarily gold miner |

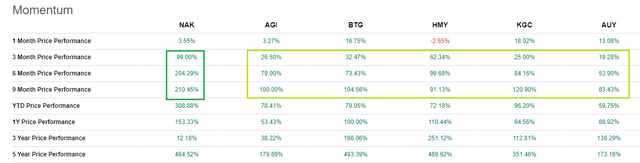

What it does confirm is that NAK is a stronger momentum play as its price performance during multiple comparable periods outruns the performance of other established gold miners (Figure-3).

Figure-3 (Source: Seeking Alpha Premium)

A valid concern could be what led to the triple-digit growth in NAK’s share price performance despite it being a future multiple-metal miner, while other established gold miners couldn’t match such gains despite the recent sustained bullish run in gold prices? In my view, the answer lies in evaluating the progress of development of NAK’s Pebble project.

The issue with NAK

The Pebble project is owned by NAK’s 100% subsidiary; Pebble Limited Partnership (or PLP). The main issue with NAK is that Pebble permitting and subsequent development had been haunted in the past through challenges posted by regulatory and environmental authorities, time and again.

[Author’s Note: This archived document contains a comprehensive list of permitting and development hurdles involving Pebble project’s development during the window from 2004 to 2014 (read from pg.5 to pg.9 for a historical overview), and is being shared with readers for reference.]

In my view, a one-liner statement for NAK’s main problem would be that despite the fundamental attraction of the Pebble project, the concerns of environmentalists and politicians regarding the ecosystem of the sockeye salmon in the BB (read: Bristol Bay) area of Alaska (that also happens to be the location of NAK’s Pebble project) have historically weighed heavily on NAK’s share price performance despite management’s re-assurances that the project would not hurt the salmon sanctuaries.

In the case of Pebble mine development, there appears to be an intense conflict (or so it is purported) between two opposing economic interests. On one hand is the fact that the BB fishery is home to the world’s largest sanctuary of sockeye salmon. Given the health benefits of this fish breed together with the fact that economic livelihood of locals has historically been attached with salmon fishing and the ‘fishing-sport’ opportunities provided by this natural habitat (check my previous article on NAK for more details), the opponents of this project make a strong case for resisting mine development. On the other hand, the mine’s proponents (a majority of whom happen to be the company’s top management) argue that the mine would not hurt the salmon sanctuary. It’s also worth noting that if Pebble project is constructed, it could become one of the largest mining projects in entire North America. Add to that the additional employment that would be created through the mine’s operations and you can figure out why the management is keen to have this project up and running. Nevertheless, Pebble project has been in the media lately and the project’s permitting and timely development (if at all) is the most factor impacting the share price.

In the news

FY 2020 has been quite an interesting year for NAK, even if we remove the potential impact of COVID-19. The Final EIS (read: Environmental Impact Statement) that’s issued by the USACE (read: US Army Corps of Engineers), and the RoD (read: Record of Decision) that’s to be issued by the EPA (read: Environmental Protection Agency) were considered the two major regulatory milestones for this year. The draft EIS was issued in February this year and indicated that the Pebble project could co-exist with the fisheries and water resources at Bristol Bay.

More recently, the USACE issued a positive final EIS (a ~2000 pager document) that shed more light on the environmental impact of this development project. It should be noted that the EIS was issued after thorough consultation and assessment through eight federal cooperating agencies (including EPA), three state cooperating agencies (including Alaska Department of Natural Resources, and Alaska Department of Environmental Conservation), the LPB (read: Lake and Peninsula Borough) and some local tribes. The essence of this fact is that the favorable final EIS is not the verdict of one regulatory authority, rather multiple authorities/agencies. Having said that, let’s take a quick look at the key takeaways from the ES (read: Executive Summary) of the final EIS:

- “Overall, impacts to fish and wildlife would not be expected to impact harvest levels. Resources would continue to be available because no population level decrease in resources would be anticipated.”

- “There would be no measurable change in the number of returning salmon.”

- “The increase in job opportunities, year-round or seasonal employment, steady income, and lower cost of living described above would have beneficial impacts on the EIS analysis area, especially for communities in the LPB, during construction and operations of the project.”

- “The project could reduce or eliminate the current local population decline because of the increase in employment opportunities and indirect effects on education and infrastructure; it could also lead some prior residents to return to communities.”

Meanwhile, the opposition to this project has remained intense but I personally feel that the Honorable Courts have favored the viewpoint of the regulators and have set aside the concerns raised by anti-Pebble activists. On that note, it’s pertinent to mention that the litigation filed by anti-Pebble activists to challenge EPA’s decision taken last year to withdraw its previous regulatory action that sought to preemptively veto the Pebble project before obtaining permits had been rejected by the Federal Court. The market had seen this as a very positive move and consequently, a subsequent equity offering was oversubscribed. I view this as an indication that if the project’s regulatory permitting process runs smoothly (and based on detailed scientific assessment of the project’s environmental impact), the claims of opponents could be refuted by the permitting authorities. Going forward, the EPA’s RoD (that’s expected to be granted within the next 3 months) would finally set the tone for NAK’s share price trajectory and is a key near-term catalyst. Given the positive EIS, it’s more likely that the RoD will be issued in favor of the project.

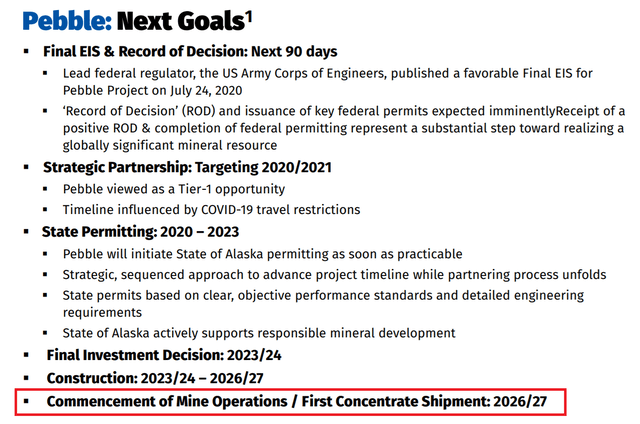

Project Development Timeline and Investor Takeaway

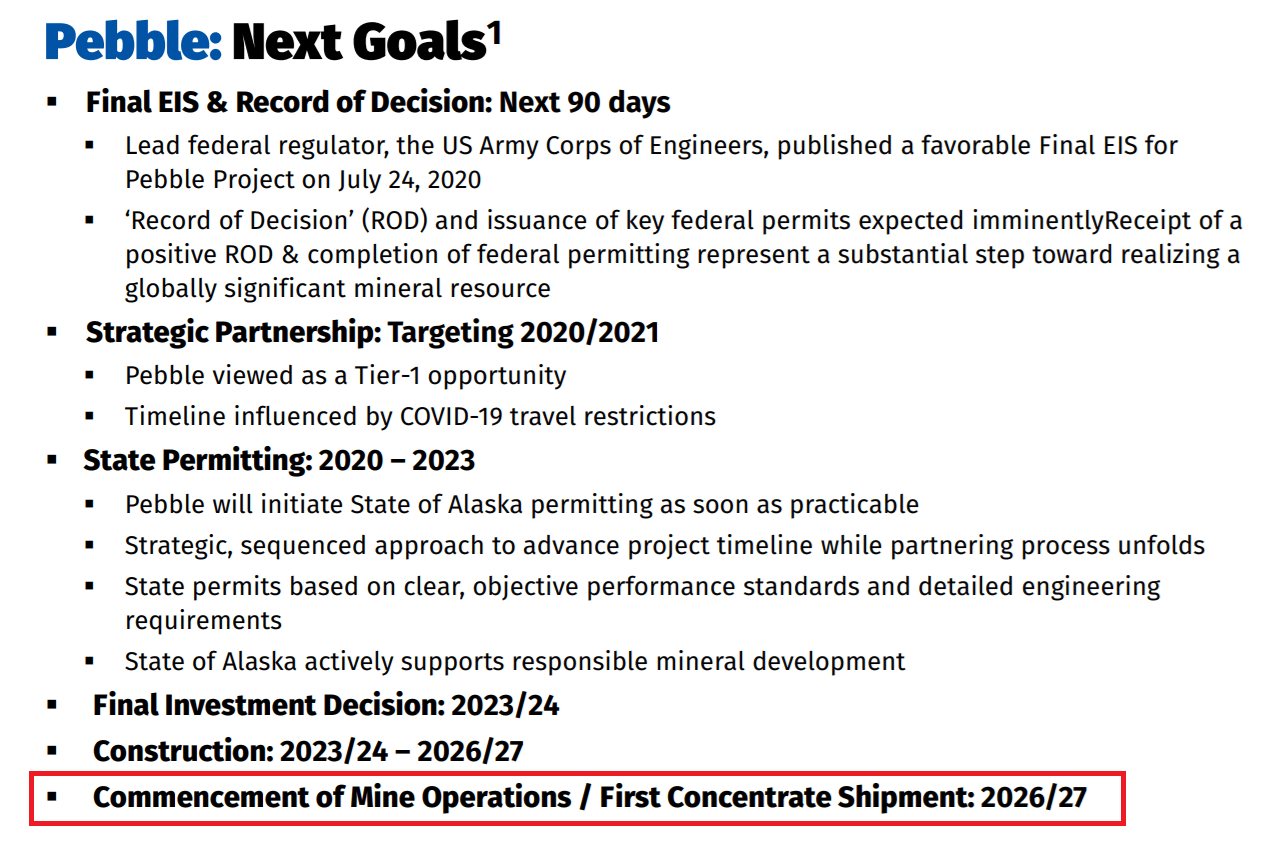

Timeline: It’s also pertinent to note that despite the strong momentum-based performance in NAK’s share price (refer to Figure-3) an investment case in NAK should be a ‘long’ one and shouldn’t be seen as a near-term profit taking opportunity. NAK’s estimated project timeline (Figure-4) assumes that the project would have been constructed by 2026-2027 (after completion of all intervening events).

Figure-4 (Source: Presentation-August 2020, pg.14)

Investor Takeaway: Despite the favorable regulatory progress, I believe a lot could happen during ‘the intervening period’ (that is, the period from present day till project construction). Considering the pressure coming from anti-Pebble activists, and more recently from a few politicians, I consider it best to wait for the remainder of the year to see how Pebble advances towards permitting. Remember, this is a ‘no-rush’ stock whose price performance is largely independent of copper and gold prices despite the massive underlying resource of both of these metals. As such, the prevailing political sentiment and the stance of the pressure groups has, and will continue to have a significant impact on the share prices, highlighting that there’s still a lot of uncertainty with this stock.

Considering the above situation, fresh investors interested in the company are advised to consider initiating a position towards the end of the year due to two reasons:

- The US presidential elections are scheduled to be held in November, and the presidential candidate Mr. Joe Biden has indicated his disapproval of the Pebble mine. The stock price tumbled by ~3.5% following the news and forced the company’s CEO, Mr. Tim Collier to come up with a couple of re-assuring arguments to counter the impact of this news. I see it as an indicator of how sharply the market reacts to any negative news on the permitting front. This also implies that NAK is rather a speculative play at present.

- Moreover, towards the end of 2020, we will have more clarity regarding the RoD to be issued by the EPA. So far, it seems that the regulatory permitting process is going in favor of NAK and the company can conveniently move ahead with the project. However, I believe it’d be better and less risky to time that investment towards the year-end.

Note that the project’s fundamental attraction is strong enough to make it a screaming buy once the regulatory permitting risks are significantly removed. Hence, the train won’t leave the station for quite some time here.

[Author’s Disclaimer: I tend to avoid political discussion in my analysis. However, given the recent interest of politicians in the company, and its impact on NAK’s share price, it was inevitable to include a bare minimum presentation of the headline news. I refrain from giving any political views in the above analysis. Investors should do their own due diligence before investing in any stock mentioned in the above analysis.]

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.