Cost inflation biting. asbe/iStock via Getty Images

Newmont Corporation (NYSE:NEM) reported Q1 results on April 22, with the title of the associated news release alluding to solid first quarter results. The numbers told a different story, however, and the market certainly looked past the title in its initial response.

Operations

Gold production clearly fell short of expectations, and COVID-related challenges were (mostly) to blame. These challenges included staffing issues at the mine sites due to infections among workers as well as isolation requirements for close contacts, but also supply-chain issues caused by the pandemic. Here is the number the CEO put on the Q1 production shortfall during his prepared remarks during the earnings call:

As a consequence of safely managing through this surge, we expect that our production results in the first quarter of 2022 could be impacted by as much as 150,000 ounces.

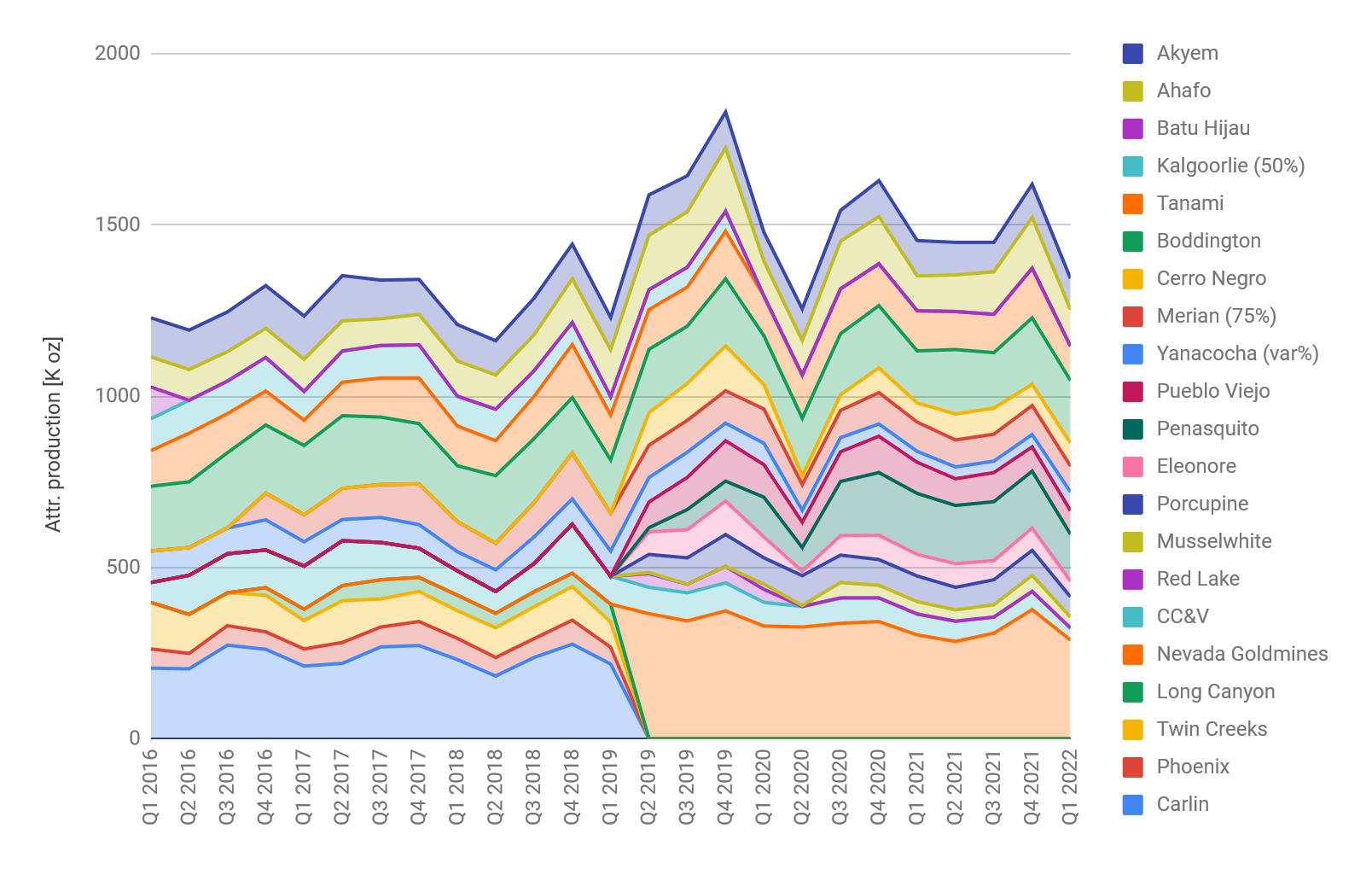

And below is the mine-by-mine production chart to go with this comment as pulled from our database. Q1 production has dropped back to levels last seen at the onset of the pandemic, and then again before the Goldcorp merger.

Newmont gold production by mine. (Company filings & author’s database)

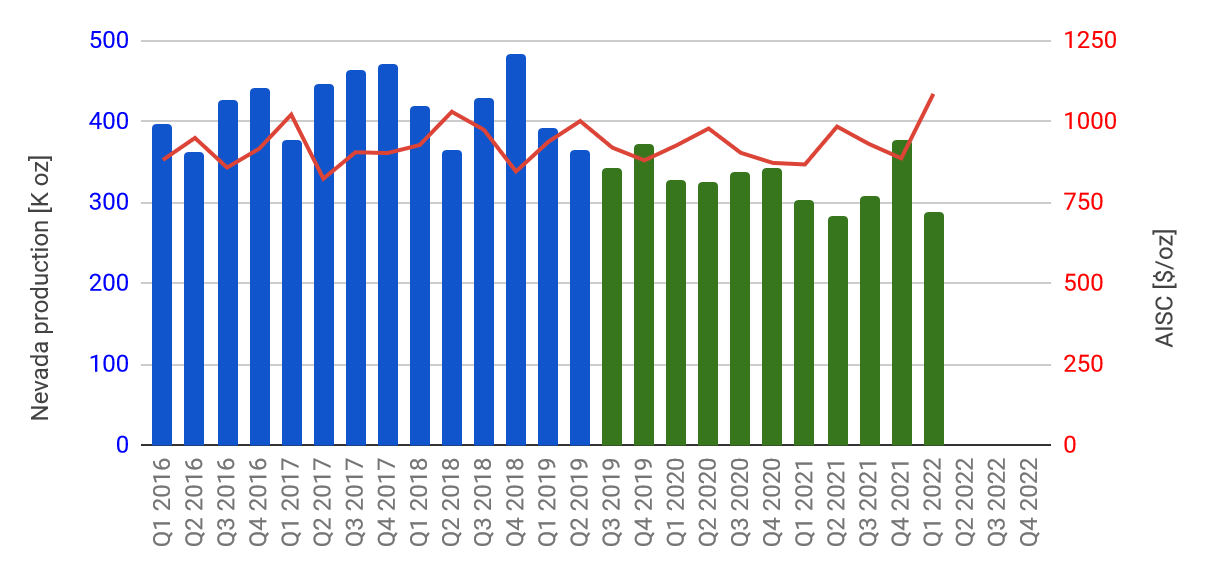

North American operations were the most affected, and the chart for the Nevada operations below may serve as just one example. Absentee rates peaked at 15-20% of the workforce at the Canadian operations, forcing the Musselwhite mine to suspend operations for seven days in February. A fire at the CC&V mill further exacerbated the production shortfall in North America.

Nevada operations (Company filings & author’s database)

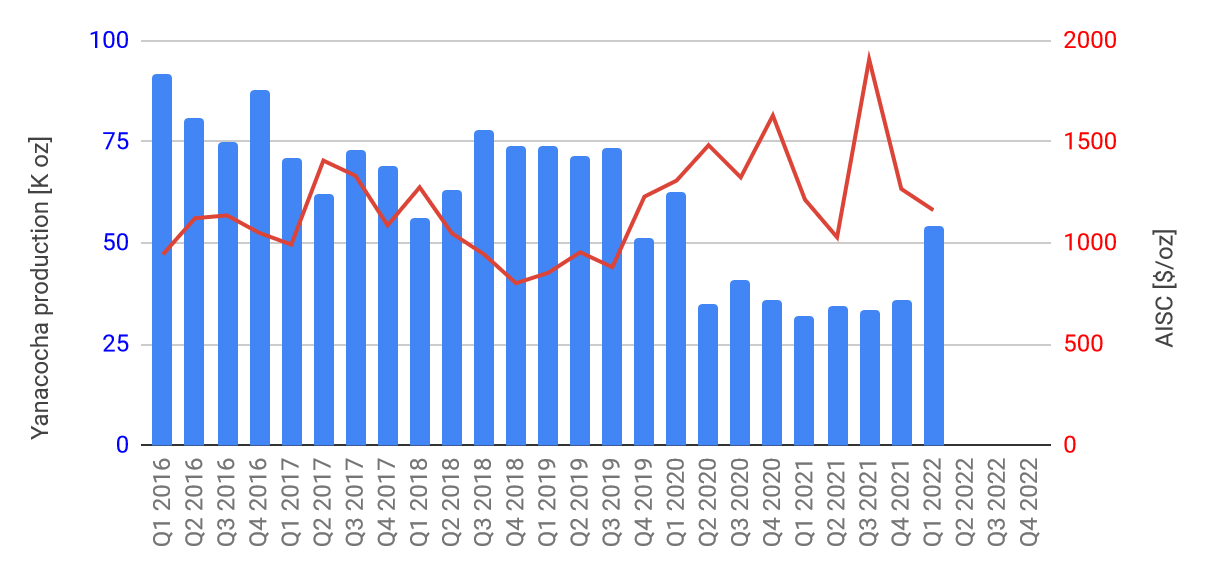

Yanacocha production numbers may look like a surprise to the upside at first sight, but upon closer inspection, the uptick in attributable production was caused by the acquisition of Buenaventura’s (BVN) 43.65% stake in the mine which closed during the quarter. In fact, record rains and a federal emergency in Peru impacted the site and actual production was down for the quarter. On a brighter note, Newmont has announced the acquisition of the final 5% stake from Sumitomo Corporation (OTCPK:SSUMF) since quarter-end and now owns the Yanacocha mine outright. This paves the way for an investment decision on the sulphides project towards the end of the year.

Yanacocha (Company filings & author’s database)

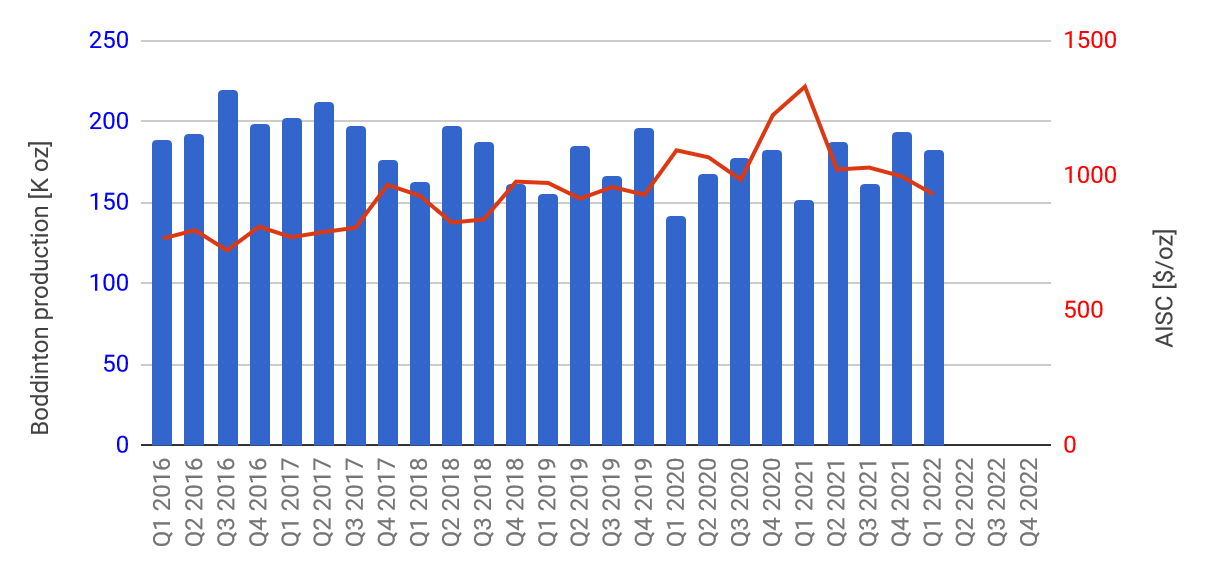

Boddington on the other hand is the one mine we would like to highlight for posting positive results, despite the challenges experienced after Western Australia finally opened its borders and let the virus in. The chart below shows steady production and falling costs for the Boddington mine, and that’s a veritable feat considering the myriad of problems reported by fellow gold miners throughout Western Australia.

Beyond the challenges caused by open borders within Australia, there is also opportunity, especially with regards to the Tanami mine extension where specialized labor will be required on-site in coming months to finish the new shaft, and that’s definitely going to be easier without the travel restrictions that have hampered proceedings during the past two years.

Boddington (Company filings & author’s database)

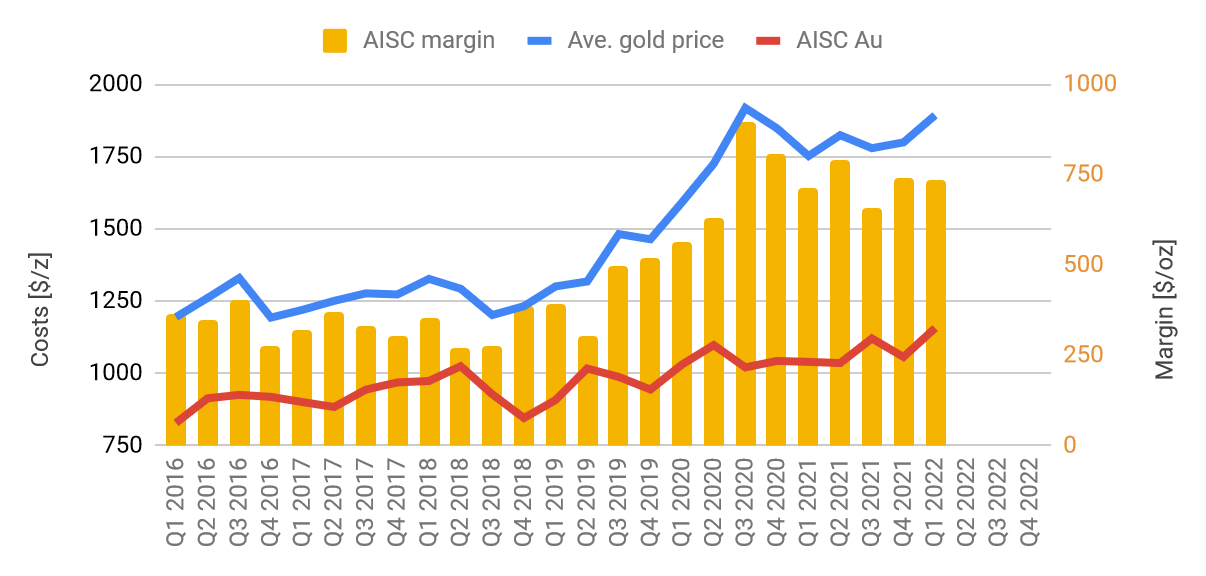

Newmont is still targeting annual 2022 production to fall within the guided range, but most likely below the 6.2M oz mid-point. Lower production commonly leads to higher costs as economies of scale cannot be captured as efficiently. This was also true for Newmont in Q1, and additionally, the company saw inflation bite – leading to the highest reported all-in sustaining costs in the history of reporting this measure. Fortunately for Newmont, margins were saved by a strong gold price environment.

Margins (Company filings & author’s database)

Financials

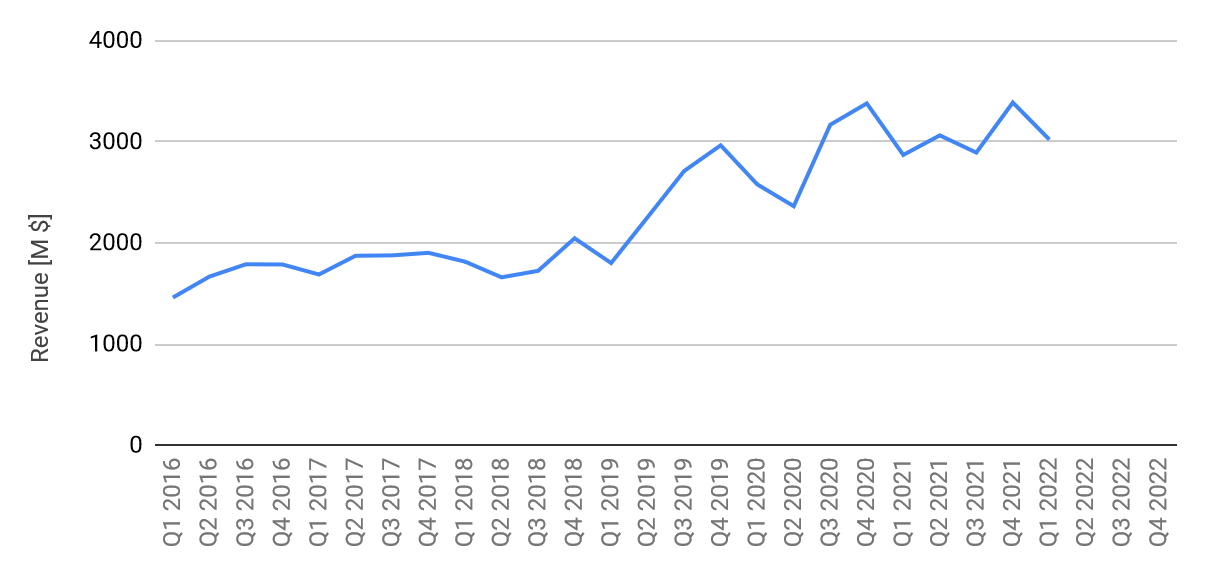

With gold prices hovering near all-time highs the strong topline came with little surprise.

Revenues (Company filings & author’s database)

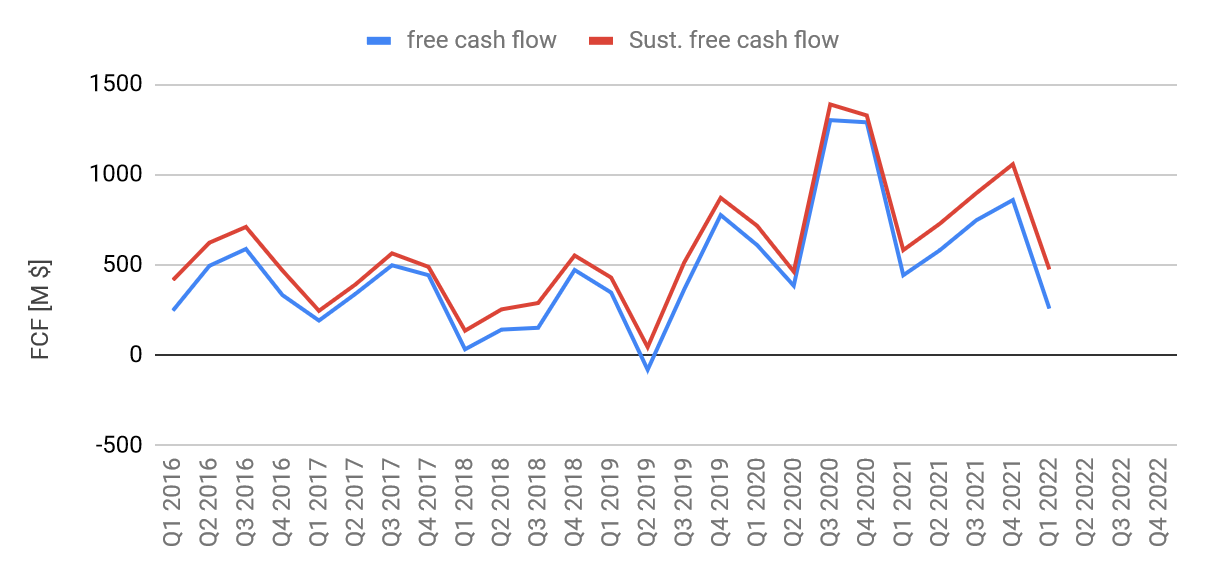

However, free cash flow took a dive nevertheless, thanks to cost increases across the portfolio (the red line in the chart below nets out growth capex and only considers sustaining capex).

Free cash flow (Company filings & author’s database)

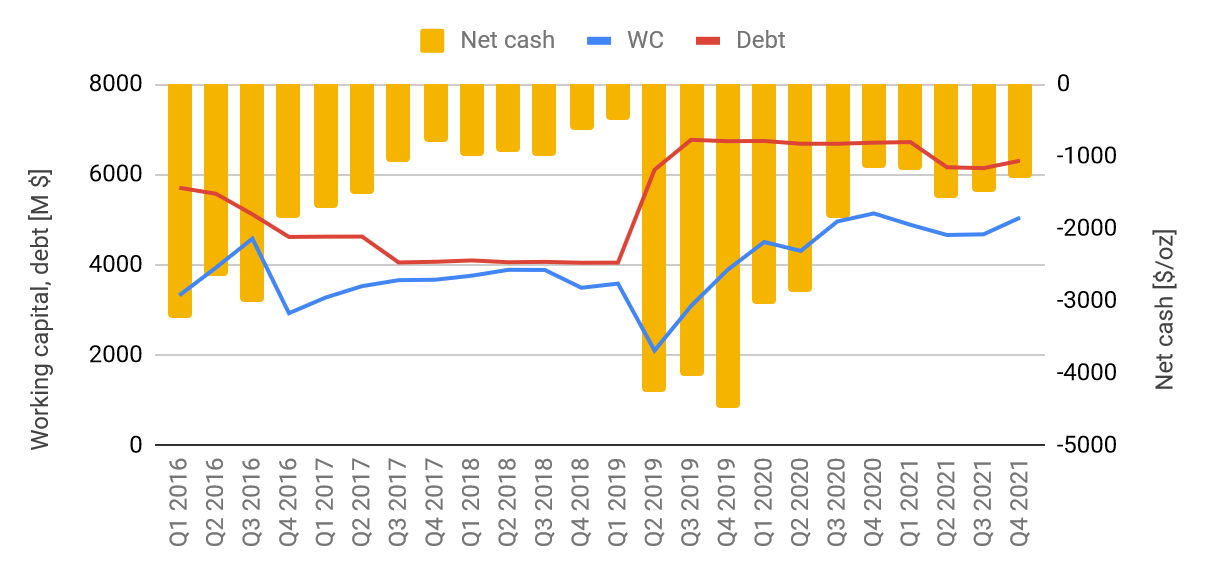

And when the dust settled, there was little if any cash available to remain on the balance sheet after Q1, despite the strong gold price environment.

Balance sheet (Company filings & author’s database)

Not to be misunderstood, Newmont’s balance sheet leaves little to be desired, but when the gold price sits near all-time highs it wouldn’t be asking too much for some increase in shareholder equity. And since rising costs clearly got in the way of that happening, the discussion with analysts on the earnings call quickly turned to this topic.

Cost Inflation

The CEO was asked for color on the inflationary pressures during the Q&A of the earnings call. Mr. Palmer pointed to labor costs as the main driver accounting for roughly 50% of Newmont’s unit costs; and proceeded to highlight cost increases for consumables, especially ammonia. Energy costs also featured in his comments, but interestingly with a lower importance (except that rising ammonia prices are of course a function of the rising natural gas price). So far cost inflation remained within the guided range, but Mr. Palmer seemed to expect costs to settle towards the upper end of the range at this point. The company promised a more detailed cost guidance update for the Q2 earnings call in July and hasn’t explicitly ruled out modifications to the cost guidance given the additional supply chain difficulties caused by Russia’s aggression.

Development projects appear on track at this point, but supply difficulties were also causing headaches, especially at the Ahafo North project in Ghana where sourcing drill rigs seems to be an ongoing problem. Cost inflation is also a topic for the capital projects currently underway. Tanami and Ahafo North are nearing their respective tail ends in terms of procurement so the worst was apparently avoided with these two expansion projects. However, the Yanacocha sulfide project will have greater exposure to rising costs, with details to be reported in Q4 along with the final funding decision.

Looking out beyond 2022 we note a pronounced drop in all-in sustaining costs in the long-term outlook for 2023, and again in 2024. In fact, the mid-range was projected to drop from $1,050/oz in 2022 to $970/oz in 2024 when this outlook was issued last October.

Company NR (Newmont Corporation)

Inflation around 2-3% was built into these projections according to Mr. Palmer, but given the current level of cost pressures, we see a strong probability of these numbers having to be adjusted upwards, keeping in mind that many affected cost factors are typically sticky.

Summary & Investment Thesis

Newmont and arguably also its closest peer Barrick Gold (GOLD) have set the scene for the gold miners as the Q1 earnings season has kicked off. Cost management was front and center during the Newmont earnings call, and we suspect, will be the governing theme for peers when they report their Q1 results.

Newmont has the luxury of a global supply chain, and we suspect the company will prove more resilient to cost inflation than many of its smaller mid-tier peers. However, Newmont’s Q1 results have shown in no uncertain terms that even this sector leader is not immune to the effects of the ongoing (yes, ongoing) pandemic. Cost inflation will most likely continue thanks to the war in Ukraine, even as we are nearing the other side of the Omicron surge. The gold mining majors have started to attract investments from generalist investors, at least that’s our explanation for Newmont (and Barrick) outperforming peers over the past six months. Controlling costs will be crucial when it comes to retaining generalists’ capital, and since this will be an upward battle for the foreseeable future, we see some additional downside risk for the two-sector leaders in the short term.

We are staying on the sidelines for this reason with regards to Newmont Corporation and will be keeping an eye out for smaller (and potentially nimbler) gold miners who demonstrate cost control and garner the benefits of the strong gold price environment more efficiently.