m-gucci/iStock via Getty Images

In any economy of any real size, various types of industrial equipment will be necessary to handle the infrastructure needs such an economy would have. One company that plays in this space that investors should pay attention to is Miller Industries (NYSE:MLR). Prior to the Covid-19 pandemic, the company was exhibiting consistent growth. While the business is now recovering from a decline in sales, profits and cash flows remain challenged. But given where shares are priced today, it may not be a bad prospect to consider. Should conditions for the enterprise not improve, the stock probably is fairly-valued or slightly undervalued. But a recovery in margins would likely result in some nice upside for long-term, value-oriented investors.

An industrial equipment firm

Miller Industries manufactures a wide range of towing and recovery equipment products to sell to their customer base. It sells these products largely through independent distributors that, collectively, operate in all 50 states, as well as in Canada and Mexico. Some of its products also make their way to Europe, the Pacific Rim, the Middle East, South America, and Africa. Though the company is diverse geographically speaking, it did, in 2021, generate 87.5% of its revenue from its domestic market. According to management, of the distributors it works with, 85% or more sell their products exclusively. The company claims that this serves as a testament to brand loyalty and the quality of its own products.

One of the pieces of equipment the company sells is a brand of wreckers. These devices are used to recover and to disabled vehicles, as well as other equipment, when they are unable to move or when it is impractical to move them. Some of these that the company produces have a capacity as small as 4 tons. And others can handle up to 100 tons of equipment. The company also produces car carriers, which are specialized flatbed vehicles that have a hydraulic tilt mechanism that enables a towing operator to connect cars to them for the purpose of transporting them. The company’s transport trailers serve as multi-vehicle automotive transport units that often have both an upper and lower deck, as well as hydraulic ramps for the purpose of loading said vehicles. These generally can transport six to seven vehicles, depending on size and weight. Operationally, the company has a few key brands that it owns. These include Century, Vulcan, Challenger, Holmes, Champion, Chevron, Eagle, Titan, Jige, and Boniface.

Author – SEC EDGAR Data

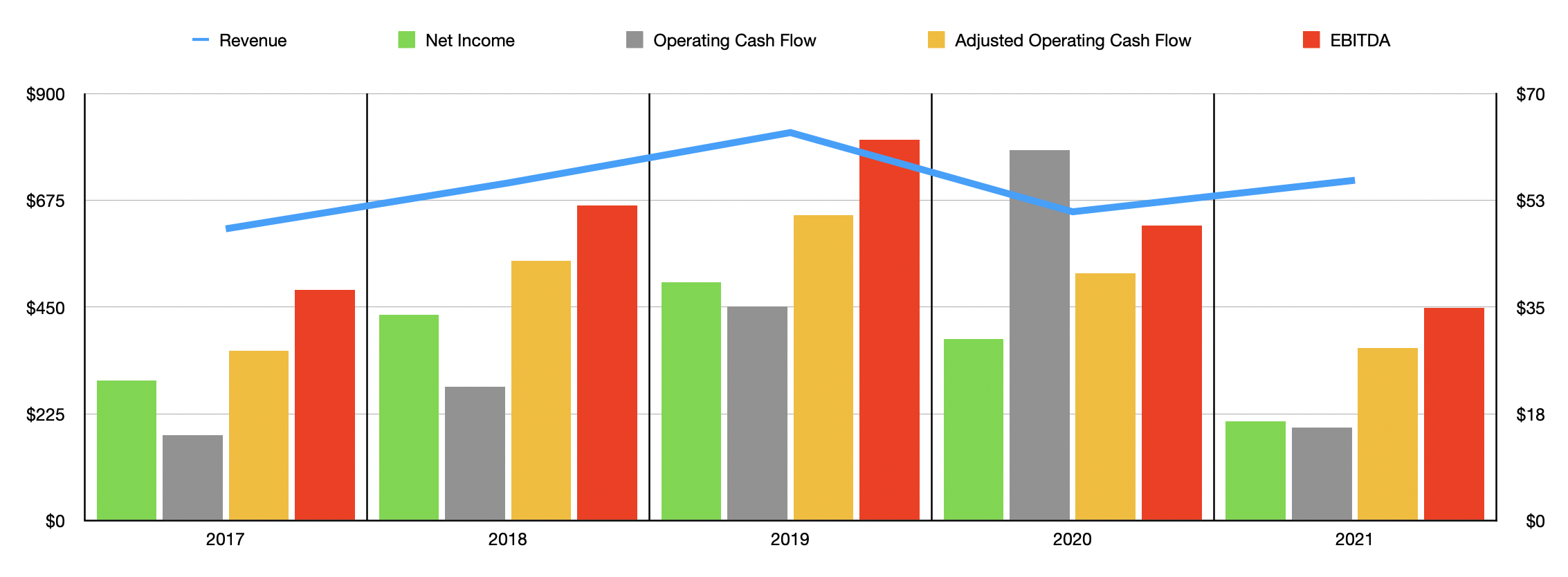

In the years leading up to the Covid-19 pandemic, management had done well to consistently grow the enterprise. Between 2017 and 2019, for instance, revenue grew from $615.1 million to $818.2 million. Then, in 2020, revenue dropped, plunging by 20.4% to $651.3 million. Fortunately for investors, the sales decline was short-lived. During the firm’s 2021 fiscal year, revenue made a partial recovery, climbing by 10.2% to $717.5 million. Although the company benefited during the year from operations opening back up, as opposed to the prior year when operations were temporarily shut down, the firm was hobbled to some degree by supply chain disruptions that caused delivery delays in both the production and sale of its products. Receiving important components necessary for the completion of orders was also a problem caused by supply chain conditions.

The trajectory of profitability largely has followed the trajectory of revenue. The one exception is that, even though sales began to recover in 2021, profits and cash flows have not. Between 2017 and 2019, net income at the company grew, rising from $23 million to $39.1 million. In 2020, net profits declined to $29.8 million before plummeting to $16.3 million in 2021. Rising inflation and supply chain disruptions and constraints caused the company’s gross margin to contract during the 2021 fiscal year. The company also saw its selling, general, and administrative costs rise as a percentage of sales by a modest amount. This related to increased salaries and other inflationary pressures the company had to contend with.

Other cash flow metrics have followed a similar path. Operating cash flow grew from $14 million in 2017 to $60.7 million in 2020. Then, in 2021, it plunged to just $15.3 million. If we adjust for changes in working capital, it would have risen from $27.9 million in 2017 to $50.1 million in 2019 before dropping to $40.6 million in 2020 and then to $28.3 million last year. Another metric that followed suit here was EBITDA, ultimately peaking at $62.4 million in 2019 before dropping to $34.9 million last year.

Author – SEC EDGAR Data

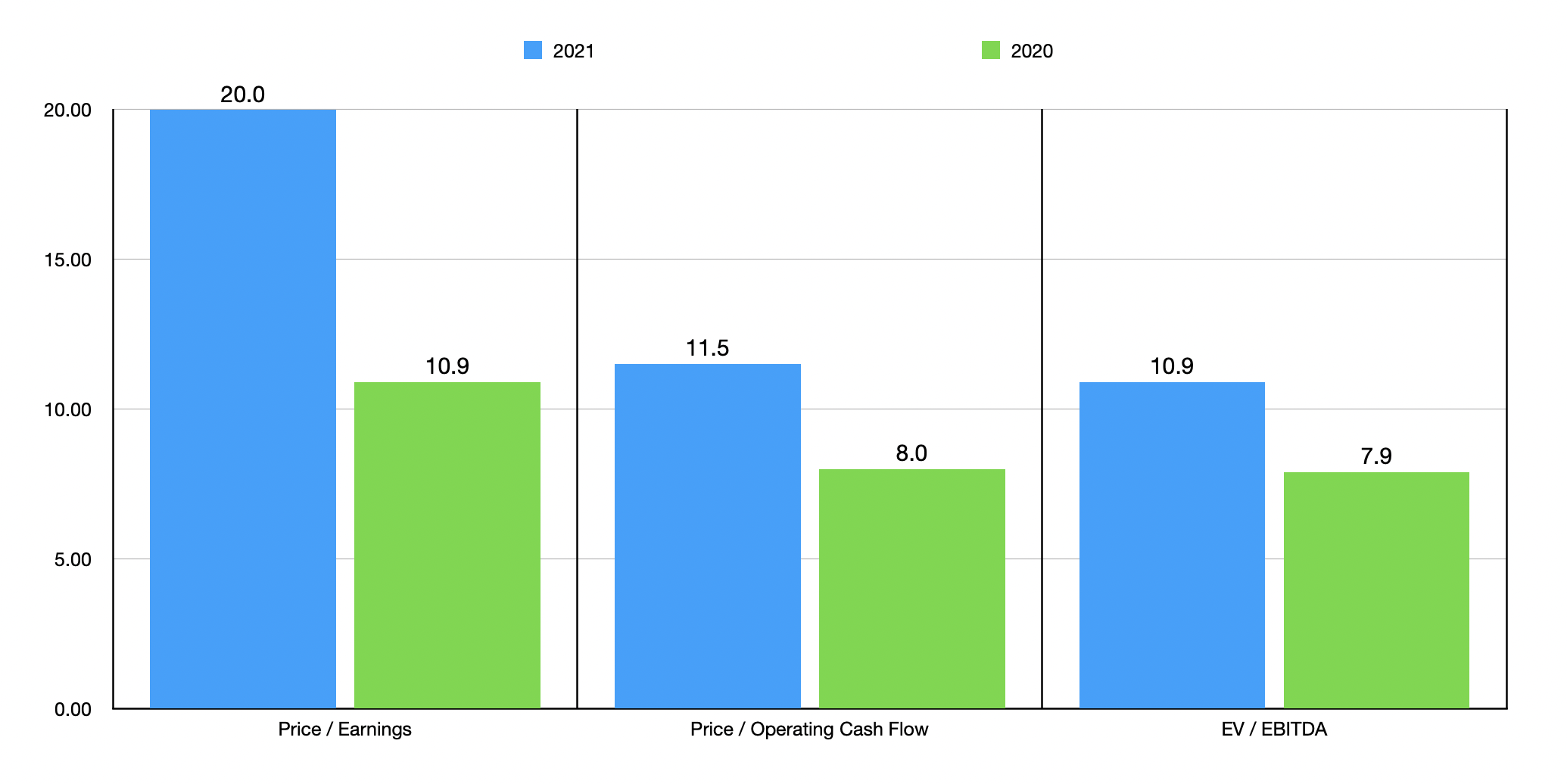

This decline in profitability caused by inflationary and supply chain issues makes valuing the company a bit tricky. The good news is that, even if these conditions remain, the business does not look to be terribly priced. Using the 2021 figures for the firm, shares are trading at a price to earnings multiple of 20. The price to adjusted operating cash flow multiple is 11.5. And the EV to EBITDA multiple of the company is 10.9. Now if we see performance improve back to at least the levels experienced in 2020, shares could see a respectable amount of upside. For instance, using data from that year, the company’s multiples would be 10.9, 8, and 7.9, respectively.

To put the pricing of the company into perspective, I decided to compare it to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 11.5 to a high of 84.6. Two of the five firms were cheaper than our prospect. Using the price to operating cash flow approach, the range was from 7.6 to 36.9. One of the five companies did not have a positive multiple. But of the four that did, two were cheaper than Miller Industries. And finally, we arrive at the EV to EBITDA approach. The five companies ranged from a low of 7.1 to a high of 57.8. In this case, three of the five firms were cheaper than our prospect. All of this assumes the 2021 figures of the company hold in perpetuity.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Miller Industries | 20.0 | 11.5 | 10.9 |

| Westport Fuel Systems (WPRT) | 19.1 | N/A | 9.7 |

| Commercial Vehicle Group (CVGI) | 11.5 | 36.9 | 7.1 |

| Manitex International (MNTX) | 84.6 | 21.1 | 57.8 |

| Manitowoc (MTW) | 55.1 | 7.6 | 9.8 |

| Blue Bird Corp (BLBD) | 40.2 | 8.4 | 42.7 |

Takeaway

Given the data that we have today, I must say that I was initially unimpressed by the recent financial performance achieved by Miller Industries. However, a deeper dive into the company and the issues affecting it led me to believe that the transitory problems associated with inflation would likely ease up eventually. Even if this does not come to pass, shares don’t look any worse than being fairly valued. So what this seems to create is a favorable risk to reward opportunity whereby the downside doesn’t look all that painful, while the upside could be quite appealing.