kynny/iStock via Getty Images

Lam Research (LRCX) reported F2Q 2022 earnings, with Non-GAAP EPS of $8.53 beating by $0.02. However, revenue of $4.23 billion missed by $188 million. Although revenues for the quarter were up 22.5% YoY, what’s more important is that QoQ revenues in the recent quarter dropped 1.8%.

Equally damaging, revenue guidance was low at $4.25 billion for F3Q 2022 compared to consensus of $4.50 billion.

Supply Chain Shortage Issues

Lam CEO Tim Archer blamed the weak earnings and guidance in the company’s earnings call on the following:

- Effects of COVID-19

- Labor shortages

- Freight and logistics cost escalation and

- Supply chain constraints

OK, let’s forget the fact that these issues have been around in one form or another for about two years. Let’s also forget the fact that I discussed supply chain shortages negatively impacting ASML (ASML) in an October 24, 2021 Seeking Alpha article entitled “ASML: Too Inconsistent, Too Overbought To Recommend.” That was one quarter or three months earlier that I alerted readers of problems arising in the equipment sector.

Let’s also not forget my Semiconductor Deep Dive Marketplace newsletter article of November 23, 2021 entitled “Applied Materials: Deconstructing Its Destructive FQ4.” It was abridged as a free Seeking Alpha article of November 24, 2021 and renamed “Is Applied Materials Stock A Buy, Sell, Or Hold After Recent Earnings?”

That article was written two months ago, shortly after Applied Materials (AMAT) reported its fiscal 4Q 2021 in which CEO Dickerson noted:

“We expect supply shortages of certain silicon components to persist in the near-term, and managing these constraints in partnership with our suppliers and chipmakers is our top priority.”

Back to Lam, I noted in the above Applied Materials article that:

“Lam’s revenues grew 5.8% QoQ in its latest quarter ending just one month earlier. Lam also noted in its earnings call that it had supply constraints, but would not quantify the impact of revenue. Remember, Lam’s revenue ended one month prior to AMAT’s.”

Revisiting Lam’s previous F1Q 2021 earnings call on October 20, 2021, CEO Archer noted:

“No. I guess I’d just reiterate, we build incredibly complex machines. They do amazing things on the wafer. They require a lot of parts from a lot of different suppliers to do that, including tremendous amount of semiconductors themselves. And so when – we’ve heard so much about chip shortages. Clearly, that hit some of our machines. And it only takes a few of those critical chips to delay us being able to ship what otherwise is a very complex system. So we’re, as Doug said, just having to work down through the supply chain through lots of suppliers to find out where those pinch points are. And it’s a daily activity. But so far, we’re working through this and being able to deliver growth and also meet the most urgent needs of our customers. That’s really our key focus.”

So let’s put things in perspective:

- Lam had shortage issues in F1Q 2022 (C3Q 2021) and was working on the issue three months ago

- ASML had shortages in C3Q 2021 which I wrote about

- AMAT had shortages in its F4Q 2021 which I wrote about

- Lam reports shortage issues in F2Q 2022 (C4Q 2021), the topic of this article, as well as blaming COVID, worker shortage, and high gas prices.

What’s The Main Cause of The Shortage?

My database includes nearly all component suppliers to Lam Research, as well as those of AMAT. Many of the component suppliers to AMAT are also used by LRCX, including MKS Instruments’ (MKSI) rf power sources.

John Lee, CEO of MKS noted in the company’s recent earnings call:

“With our broad and unmatched portfolio, which we estimate serves greater than 85% of WFE, we play in every critical semiconductor manufacturing process in the world today, including deposition, etch, wet clean, lithography, metrology and inspection.”

“We estimate first quarter revenue of $750 million plus a minus $30 million. This estimate includes headwinds of industry-wide supply chain constraints, which we expect to persist through the first quarter.”

MKSI stock dropped 8% following the announcement that outlook is below consensus mark from supply chain disruptions

Applied Materials, which announces quarterly earnings next month and shares MKIS as a supplier with LRCX, will also be negatively impacted by this supplier shortage.

Lam’s Fundamentals

China’s Exposure to China – Not Affected by Shortages

I discussed in an October 14, 2021, Seeking Alpha article entitled “Lam Research Stock: Substantial Tailwinds From China And NAND Memory Exposure” that Lam’s high exposure of equipment revenues from shipments to Mainland China was a tailwind for the company.

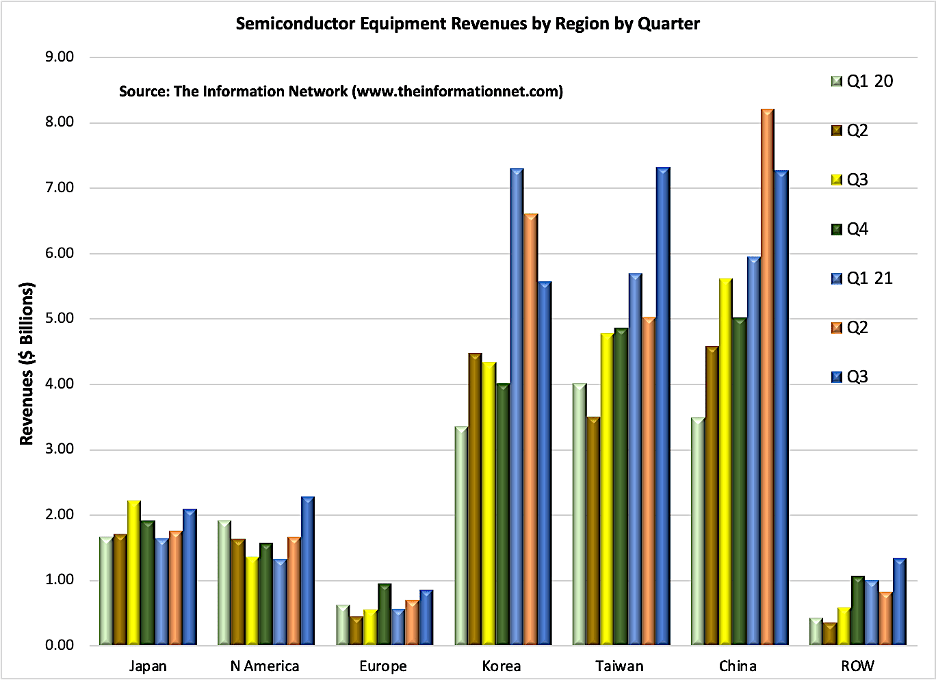

In 2020, China held the largest market for semiconductor equipment purchases, growing 39% to $18.72 billion. In the first three quarters of 2021, China was again the largest market for equipment, representing 24% of total equipment sales. Chart 1 shows QoQ growth of equipment sales to China from Q1 2020 through Q3 2021.

The Information Network

Chart 1

A large exposure of equipment sales to China is important as discussed above. In 2020, Lam’s revenues from China increased from 26% in 2019 to 35% in 2020. The percentage of revenues continues to be higher than competitors on this list, but Lam’s exposure decreased from 37% in Q3 to 26% in Q4, representing a decrease of $370 million. There are important takeaways:

- Lam’s exposure decreased significantly in Q4 2021, while ASML’s and Screen’s exposure increased, According to our report entitled “Mainland China’s Semiconductor and Equipment Markets: Analysis and Manufacturing Trends,” equipment imports by China decreased just 5% between Q2 and Q4 2021, but etch equipment, the core of Lam Research, decreased 30%.

- This means that the company’s poor performance in CY Q4 2021 was NOT due to supply chain, COVID, gas prices, or labor shortages, but to cuts in etch purchases in China. Inspection equipment sales to China, on the other hand, were up 40% – a strong signal for KLA (KLAC).

- Lam Research’s revenue in Q4 missed by $188 million as noted above. The $370 QoQ decrease in revenues could have been directly related to China equipment revenues.

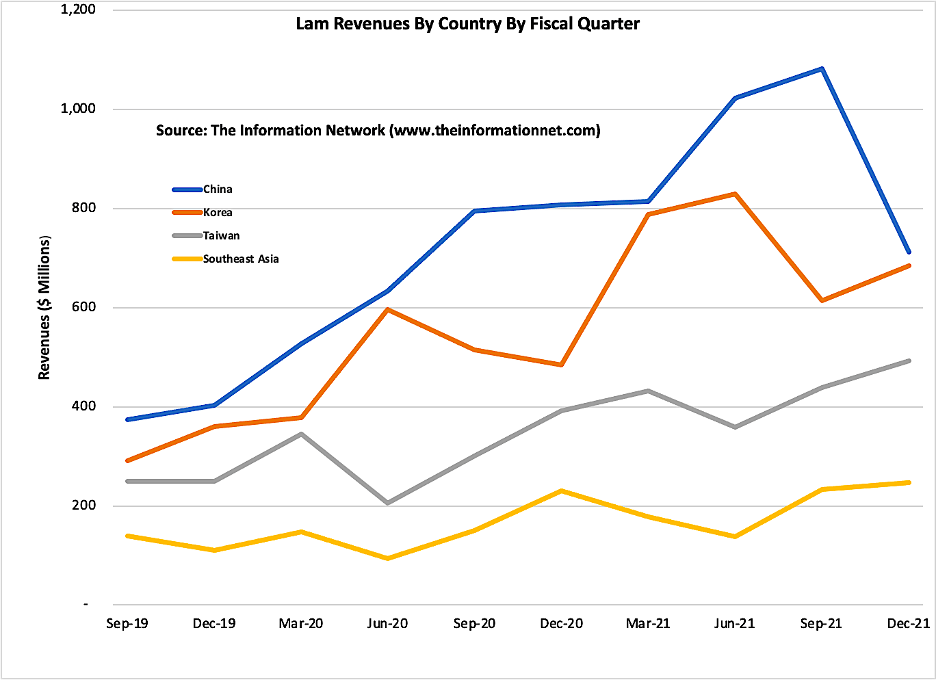

Chart 2 shows Lam’s revenue by country between September 2019 and December 2021. China represented its greatest source of revenue during this period, although the drop in Q4 2021 is significant.

The Information Network

Chart 2

Lam’s Exposure to NAND Memory – Affected by Shortages

Chart 2 above also shows that Lam’s exposure to Korea (orange line) is its second-highest source of revenue. This is significant because Lam has a high exposure to NAND memory, and the largest manufacturers Samsung Electronics (OTC:SSNLF) and SK Hynix (OTC:HXSCL) are located in Korea.

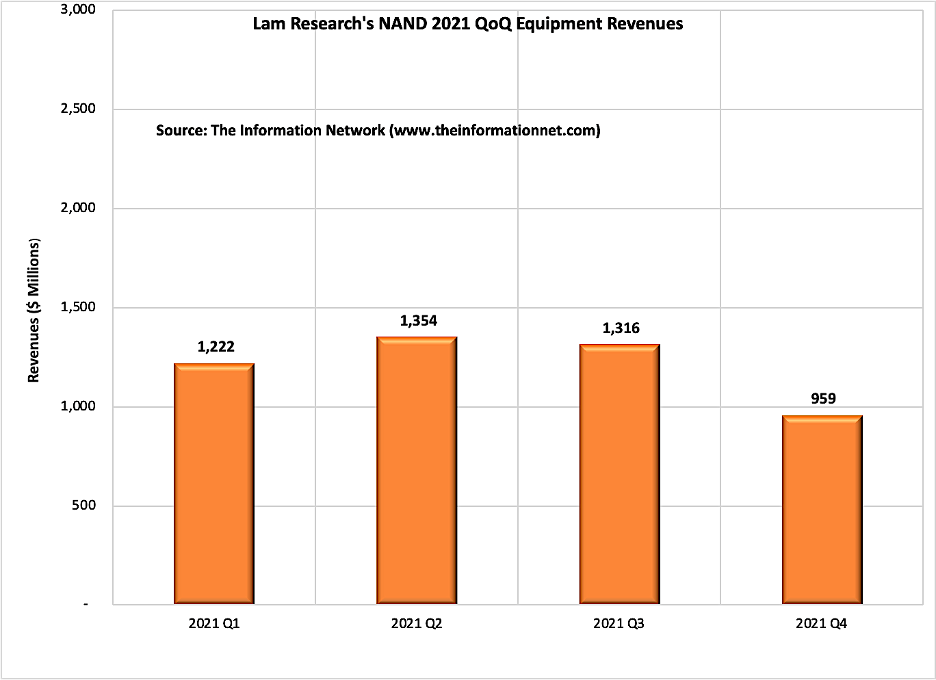

Lam’s NAND exposure was 57% in 2017 and 64% in 2018 during the time of the peak memory cycle, which crashed in 2019 because of high supply, inventory overhang, and lower average selling prices. Even during the downturn and subsequent recovery in 2020 despite the pandemic, Lam’s exposure to NAND was 41%, which increased to 44% in 2021.

However, Chart 3 shows 2021 QoQ NAND revenues and a significant drop in Q4 2021 as NAND exposure decreased to 35%.

The Information Network

Chart 3

Chart 1 above also shows equipment spend in Korea. Of interest is that equipment purchases follow a cycle of supply-demand for the memory sector (peak in Q1 2018 followed by a crash followed by a recovery). I see further growth in the NAND sector through 2022, but memory companies have developed a judicious spending approach to capex to avoid the memory crash that was due to excessive capex spend in 2017-2018.

This trend is different than that of China shown above in Chart 1, which shows no cyclicality in the period. However, of concern and a headwind for LRCX is the impact of U.S. sanctions and blacklisting of equipment into China for sub-10nm nodes.

Revenue Pull-ins in Previous Quarter

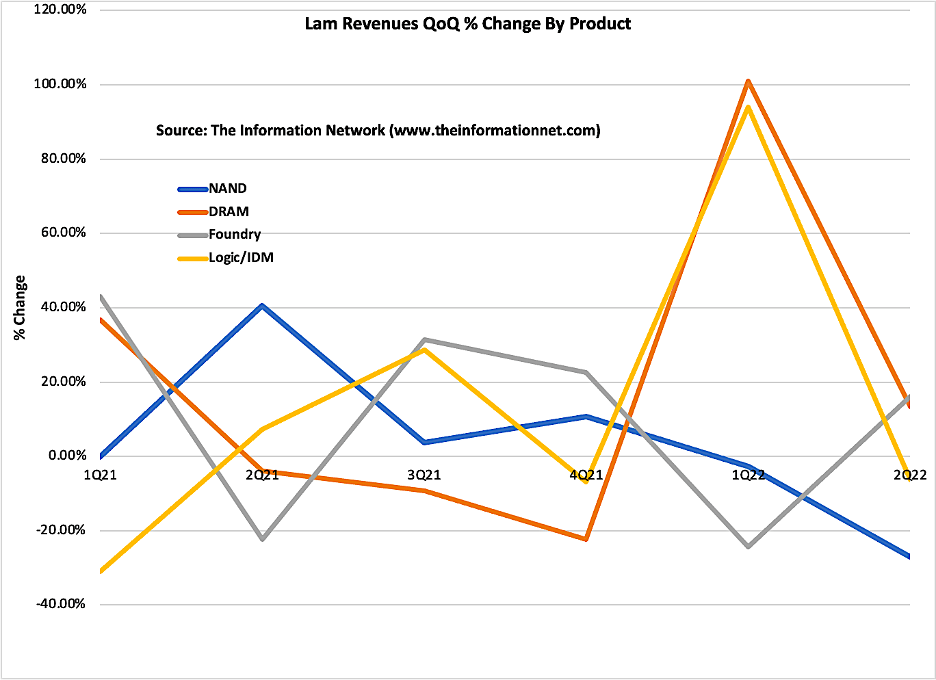

While Lam’s CEO expounded on excuses for the poor quarter, which missed by $188 million, he neglected to point out that revenues for the quarter were coming off an abnormally strong quarter due to unsustainable pull-ins of equipment by DRAM and Logic/IDM customers, as shown in Chart 4.

The Information Network

Chart 4

During Lam’s previous earnings call in October 2021, CEO Archer noted:

“Driven by strong demand and solid execution, Lam delivered its sixth consecutive quarter of record revenue and earnings per share.”

Despite the strong growth in revenue of $4.3 billion, the company missed consensus by $20 million, and the stock dropped 2.6% after hours but recovered the next day.

Investor Takeaway

Lam Research is a dominant semiconductor equipment supplier with a strong position in plasma etch, deposition, and cleaning technologies. Its customer base is worldwide, but two catalysts for growth have been sales to China semiconductor companies and sales to NAND memory companies.

The poor performance in this past quarter was a result of a drop in sales to China (Chart 2) and slower growth to NAND companies (Chart 3). Pull-ins of equipment purchases in the previous quarter resulting in a spike in DRAM and Logic/IDM sales from equipment that was earmarked for installation in the current quarter were instead pulled into the previous quarter.

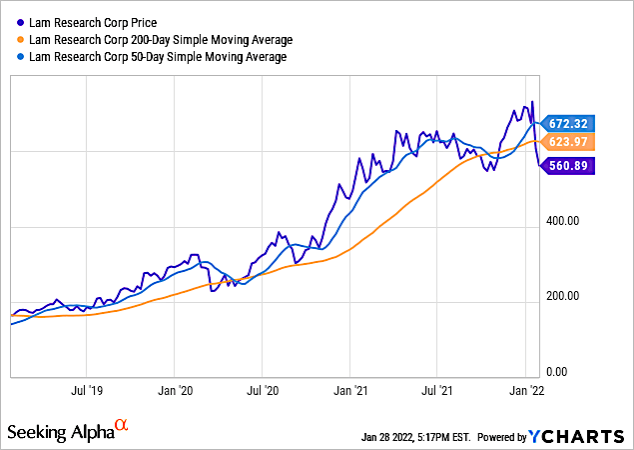

Chart 5 shows LRCX stock price for the three-year period, showing that it dropped below its 50-day and 200-day moving average. The stock last peaked on January 14, 2022, before its earnings call on January 26 after the market closed. The stock dropped below its 50-day on January 18 and its 200-day on January 19.

YCharts

Chart 5

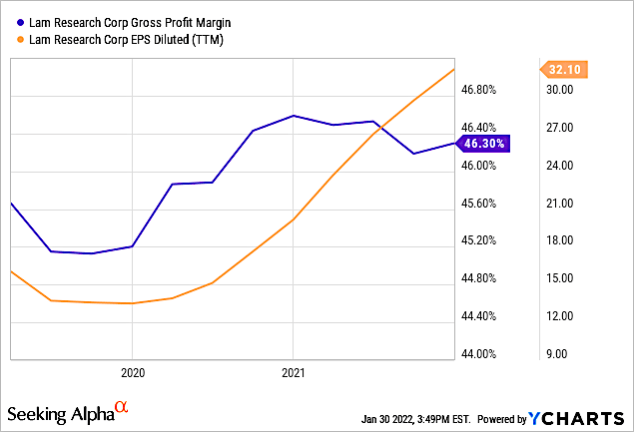

Chart 6 shows that Lam’s Gross Profit Margin decreasing slightly while EPS has grown strongly in the past six quarters following the COVID scare to financials in early 2020 that wasn’t sustained.

YCharts

Chart 6

Why have LRCX and most tech stocks fallen? After a long stretch of technology stock outperformance, stretched valuations, rising interest rates, and inflation rates have been three factors responsible for the sell-off.

Many technology stocks have been hit hard as the catalysts that had helped propel stocks higher last year have switched direction and are now headwinds to further growth. A wave of consumer demand fueled by the reopening of economies pumped up corporate profits more than expected in 2021. The Federal Reserve and other central banks also helped prop up the market by keeping interest rates extremely low, after underestimating the effect of the $1.9 trillion fiscal stimulus on the economy.

That’s now changing. It isn’t surprising that Treasury yields are climbing on the quickest pace of inflation in four decades. But the selloff in bonds isn’t because of inflation fears. Instead, investors are betting the Federal Reserve will control prices with tighter policy.

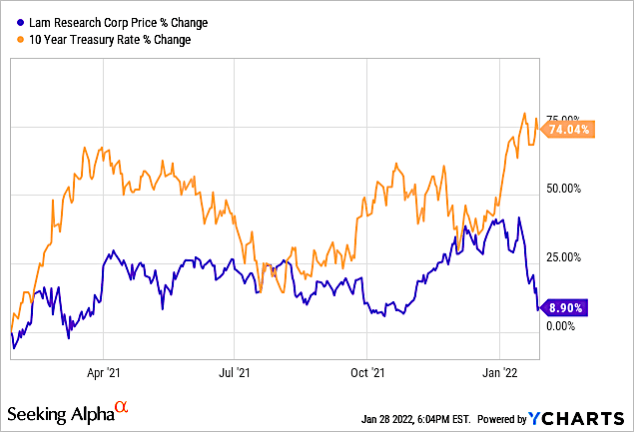

Chart 7 shows the stock price of LRCX superimposed over the 10-year Treasury Note, showing that has been inversely proportional to the 10-year Treasury Rate since October 2021.

This inverse relation has been valid for just three months. Prior to that it was directly proportional. It may move back to a more normal direct relationship. Timing is critical but unknown.

YCharts

Chart 7

LRCX has a Seeking Alpha Quant Ranking of just 20 out of 33, with a rating of 2.96. It’s rated a hold.

Near term, the plethora of excuses given by LRCX management in its earnings call is only part of the financial story for the company. The company’s poor performance in CY Q4 2021 was not due only to supply chain, COVID, gas prices, or labor shortages. It was due to a reduction in plasma etch purchases by China, which dropped 30% to all suppliers between Q2 and Q4, representing a decrease of $370 million.

The drop in equipment purchases for NAND for Q4, however may be due to the excuses presented. NAND revenues by Lam decreased 30% in Q4, while Korea increased plasma etch purchases to all vendors by 5% in 4Q.

But the bottom line is that LRCX was aware of these shortages in the previous quarter, and supply-chain management and above are to blame as investors have suffered. Yet the tone of the earnings call was not to blame executives, but “it’s the economy, stupid.”