Investment thesis

Jumia (NYSE:JMIA) is the de-facto play on e-commerce in Africa. While e-commerce and digitization of finances constitute long-term secular tailwinds, it remains to be seen how fast this trend will be seeing broad adoption in Africa, as the continent is still confronted with logistical constraints and low internet penetration in rural areas. Jumia has competitive advantages based on the breadth of its services offerings, including broad regional coverage and established logistics networks across major African countries, including its in-house payments solutions JumiaPay, all tied together in one platform. Jumia is in the very early stages of penetrating the african e-commerce and fintech market and there are multiple monetization opportunities within those segments. The company has recently implemented business shift mix efforts that show early signs of improving unit economics and may support management’s goal of achieving long-term profitable growth.

Due to the company’s high current valuation short term stock upside may be limited, but I believe the overall secular tailwinds that support the adoption of e-commerce in the fast-growing, young African population will support strong growth in the years ahead.

In this article I will discuss the company’s prospects, most recent financial results and equity offering, Citron’s reversal on the stock, as well as competition and risks.

Company overview

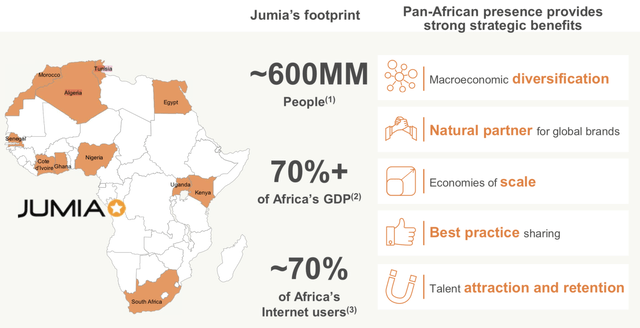

Jumia is the leading e-commerce operator with a Pan-African presence across 11 countries that together have a population of 600 million people, which accounts for >70% of Africa’s GDP of €2 trillion and almost 70% of Africa’s internet users.

Source: company presentation

Due to its broad presence across Africa, there is huge potential for diversification and economies of scale, which is an important advantage in the still fragmented e-commerce market. Jumia’s services offerings range from core e-commerce where 3rd party sellers and buyers are connected, to logistics & fulfillment, marketing, and digital payments solutions from its JumiaPay offerings.

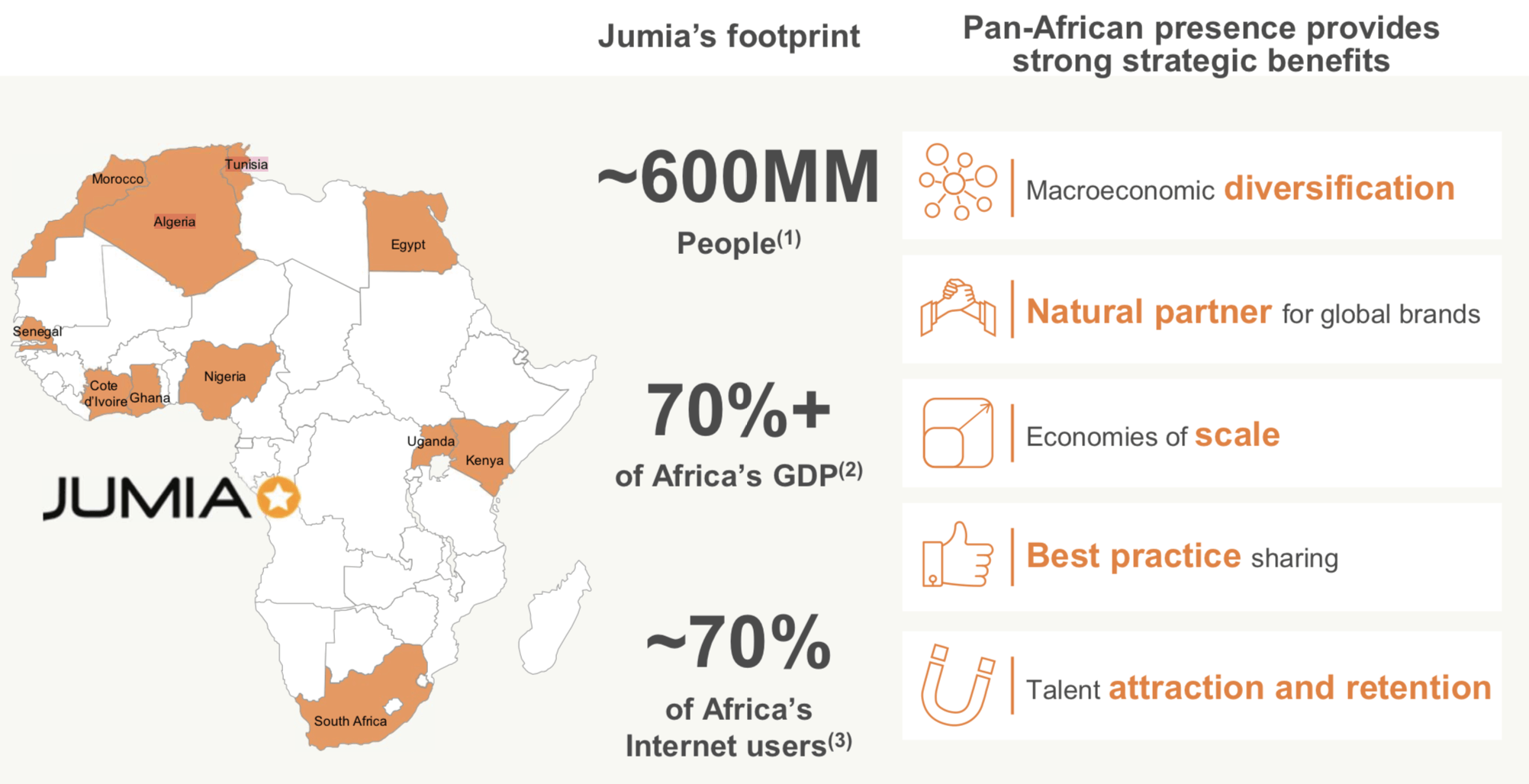

The company earns money from commissions on items sold on its e-commerce platform from 3rd party sellers, while also offering full handling of the logistics, including warehousing and fulfillment, deliveries, tracking, return handling and payments offerings. Buyers can use Jumia’s platform to buy good and services from all kinds, including everyday products like cosmetics & hygiene, fashion, electronics, and even food delivery. The most recent split of goods sold on its platform is shown below.

Source: company presentation

As of Q3 2020, the company had 6.7 million Annual Active Consumers and >110k of active sellers on its platform. For the 12-month period ending Sep 2020, the company handled €1bn in GMV (which is the value of good sold/bought on its platform) with a total of 28 million orders being placed on its platform. Transactions via JumiaPay accounted for 34% of total orders completed for the first 9 months in 2020 (Source: company presentation).

The breadth of services offerings from Jumia’s platform provide sellers with an attractive value proposition by means of full integration of services from product placements on its e-commerce platform to logistics, and payments handling. More importantly, sellers gain access to an already large and growing consumer base, marketing tools and unique data insights on consumer behavior.

Source: company presentation

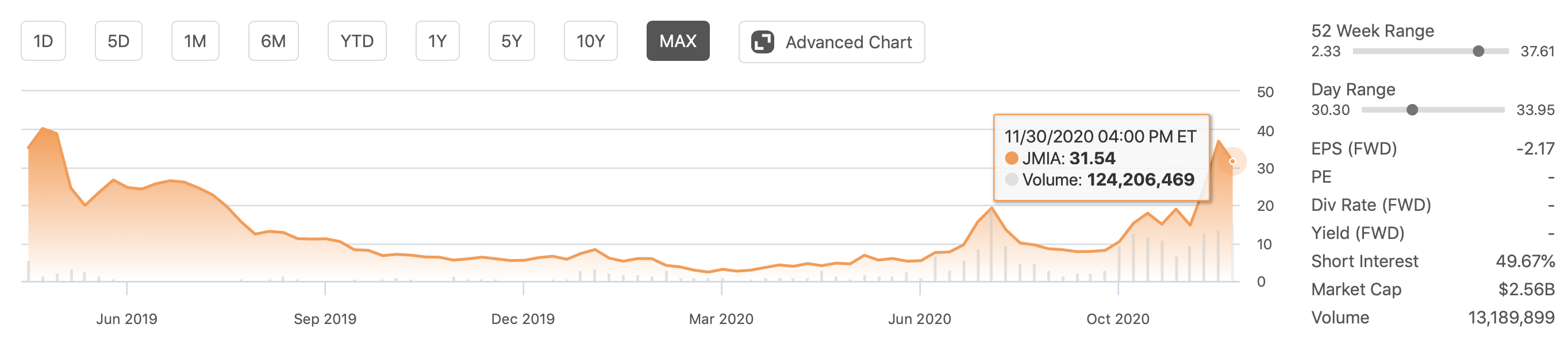

It has been a bumpy ride since the company’s IPO back in April 2019 when the IPO was priced at $14.50 and closed up 75% on its public deput, just to see its stock crash down all the way to the $2 range in the following 12 months. While there were multiple reasons for that crash, including disappointing quarterly results, discontinuations of operations in some countries, and a destructive short-seller report from Citron, Jumia’s stock price has recovered in an astonishing fashion since hitting its all-time lows at $2.33 per share during on March 16th 2020.

Source: SeekingAlpha

Source: SeekingAlpha

Since the March 2020 lows, the company continued to provide a mixed bag of financial results. Highlights were continued growth in its JumiaPay offerings, and most recently, strengthening unit economics for its core e-commerce offerings following cost efficiency measures.

Opportunity for African e-commerce & fintech is huge

There are numerous articles around the large opportunity for e-commerce and fintech adoption in Africa, so I will not go into detail here and summarize to say that Africa, with its 1.3 billion population, has one of the world’s largest under-penetrated populations with respect to e-commerce and fintech adoption. The African population is also the fastest growing of all continents with a 2.7% growth rate per year, more than twice the growth rate of South Asia (1.2%) or Latin America (0.9%). It is estimated that Africa’s population will double by 2050, making it a 2.5bn people contintent respresenting more than a quarter of the world’s population (see here). Nigeria, Jumia’s largest active market, is estimated to overtake the US as the world’s third-most-populous country by2050, reaching 400 million people (see here).

Most importantly, the age structure of the population provides opportunities for fast digitization acceptance. According to the United Nations, the number of African people aged below 35 accounts for a staggering three quarters of Africa’s total population (see here).

Africa is not only a large contintent but also shows promising signs and growing penetration of internet usage: Jumia reports that, as of June 2019, Africa had 523 million internet users. Around 17 million SMEs and merchants and $4.0tn in household and B2B spending underpin the large untapped opportunity for digitization of commerce and payments (see here). McKinsey estimates that African e-commerce could account for 10% of the continent’s overall retail sales by 2025, which would be $75 billion in annual revenue potential (see here). Irrespective of the actual market size, it is clear that Jumia has only penetrated a very small portion of that market with its marketplace revenue reaching €66.1 million for the first 9 months in 2020.

Jumia is also going all-in with its fintech offering JumiaPay. Digitization of finances could actually be the spotlight in Africa’s digitization journey as it enables a largely underbanked population to gain access to financial solutions. A McKinsey report stipulates that >60% of Africans could have access to banking services by 2025, with >90% using mobile wallets for daily transactions (see here). A look into the most recent developments around African fintech companies being backed by global payment giants and venture capital firms clearly shows that there is a strong secular trend ahead:

Investor appetite in Africa, especially in payment services, is one of the strongest in the world. If Jumia continues to scale its JumiaPay offerings in the right way, it can well become one of the leading fintech players not only in Nigeria but in Africa as a whole. However, consolidation in the space seems inevitable.

Jumia’s Financials

Jumia has struggled to deliver the financial growth that many investors had hoped for when the company went public, with declining revenue growth rates over the past quarters, which were partly due to cost-cutting, exiting of countries like Cameroon, Rwanda, and Tanzania, as well as business-mix shift towards lower cost, everyday product categories, away from electronics and smartphones.

Jumia now seems to be on the right path with respect to its goal of achieving cost-efficiencies that will support healthy long-term profitable growth as shown by its most recent financial results from Q3 2020 (Source: Q3 press release):

-

Marketplace revenue increased by 18.9% to €23.4 million from which commissions revenue grew by 43% and fulfillment revenue by 13% YoY respectively;

-

Annual Active Consumers reached 6.7 million in Q3 2020, up 23% YoY;

-

Gross profit was €23.2 million (growth of 22% vs Q3 2019) and reached positive territory even after including fulfillment expense (€6.6 million in Q3 2020 vs. a loss of €1.7 million in Q3 of 2019);

-

Overall, operating expenses were cut down dramatically and operating loss decreased by 49% YoY;

- JumiaPay TPV was €48.0 million (YoY increase of 50%) while on-platform TPV penetration almost doubled to 25.6% of GMV Q3 2020;

-

On the negative side, total orders declined 5% YoY and were mostly affected by a 20% decrease in digital services transactions from JumiaPay (Jumia said that orders on the rest of the platform were stable);

-

GMV also declined by 28% to €187.3 million, as the effects of the business mix rebalancing initiative continued to impact overall GMV and revenue growth.

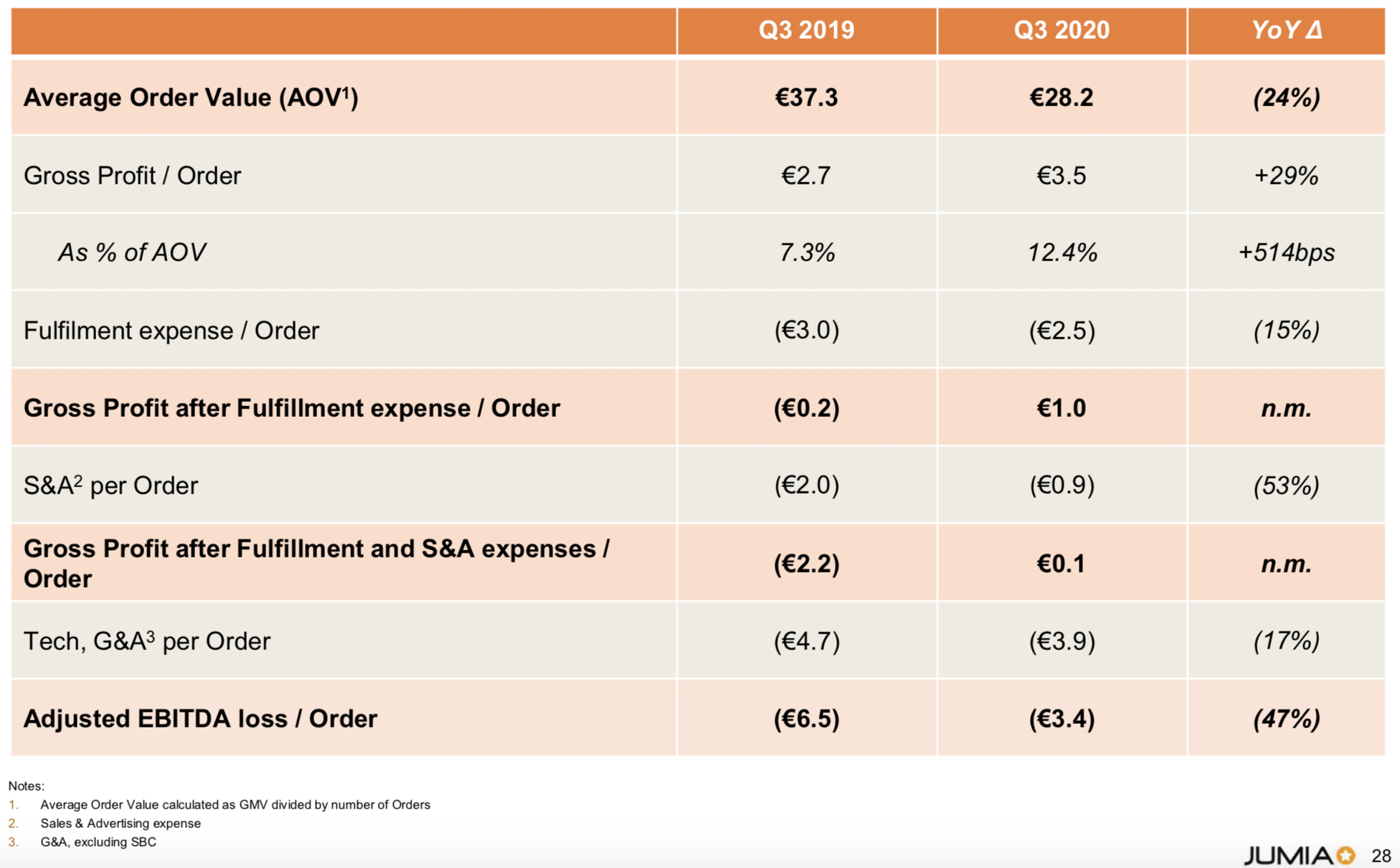

While overall GMV, revenue, and order numbers were largely disappointing, these current figures need to be interpreted with caution as they are impacted by the business mix shift towards lower cost, higher frequency purchase, everyday product categories, as well as enhanced promotional and expense discipline. Current comparisons are against higher lifetime value, more expensive goods such as phones / electronics which had a significantly larger share of the company’s GMV in the past quarters. Jumia reported a reduction in GMV share from phones & electronics down from 56% in Q3 2019 to 43% in Q3 2020 GMV. The business mix rebalancing efforts led to a 24% decrease in average order value from €37.3 in Q3 2019 to €28.2 in Q3 2020, affecting overall GMV and revenue performance. Meanwhile gross profit margin inched up by +514bps YoY (see here).

Path to profitability

Q3 2020 actually was the first quarter where the company achieved breakeven before General and administrative (G&A) expenses as gross profit after fulfilment and S&A Expenses was close to break-even at 0.4€ million vs. a loss of 15.5€ million in Q3 2019. The company added that the majority of countries have shown break-even during the most recent quarter.

Overall, there are significant improvements in unit economics in the most recent quarter as gross profit per order increased by 29% to €28.2 million in Q3 2020, while gross profit after fulfillment expense per order went into positive territory compared to a €0.2 million loss Q3 2019. Gross profit after fulfillment and S&A expenses per order were €0.1 million compared to a negative (€2.2) million in Q3 2019. Most of the improved unit economics came from cost reductions in fulfillment and S&A spending, as noted by management in the Q3 earnings release.

Source: company presentation

These efficiencies were achieved while Jumia maintained solid marketplace revenue growth of 18.9% in iQ3 2020. However, this growth is significantly lower than the 38.2% growth from the Q2 2020 financial quarter (see here). Investors should closely watch that metric over the coming quarters as it reflects the actual impact of ongoing cost-cutting and business mix rebalancing efforts, which are intended to diversify the business and support unit economics, but should not limit growth of the platform altogether.

Nevertheless, Jumia’s most recent financial performance marks a key inflection point in financial metrics. Once the transition to higher-frequency purchase, everyday product categories is complete, also the revenue growth comparisons will become more objective, and will hopefully result in better YoY comparisons. I also believe that the company can put some marketing dollars to work to enhance platform penetration and increase order frequency from new and existing customers.

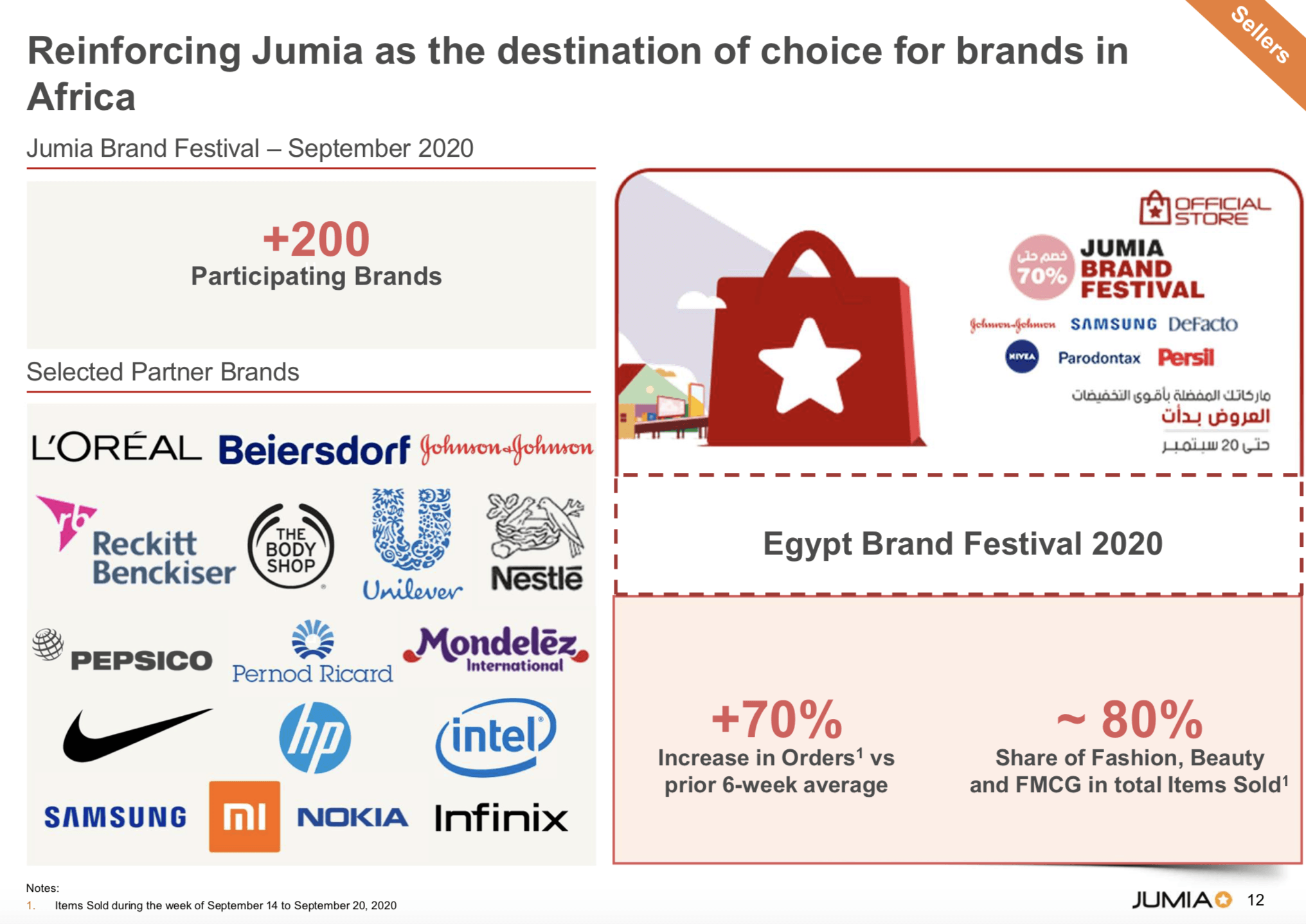

Jumia has already demonstrated that it can scale up order volumes quite easily. After launching their first ever Jumia Brand Festival the company reported a +70% increase in orders vs. the prior 6-week average. Roughly 80% of the items sold were from the targeted fashion, beauty and FMCG category that management is pivoting its business mix rebalancing efforts towards.

Source: company presentation

In my view the following aspects will be the key drivers for Jumia towards profitable growth in the not too-distant future:

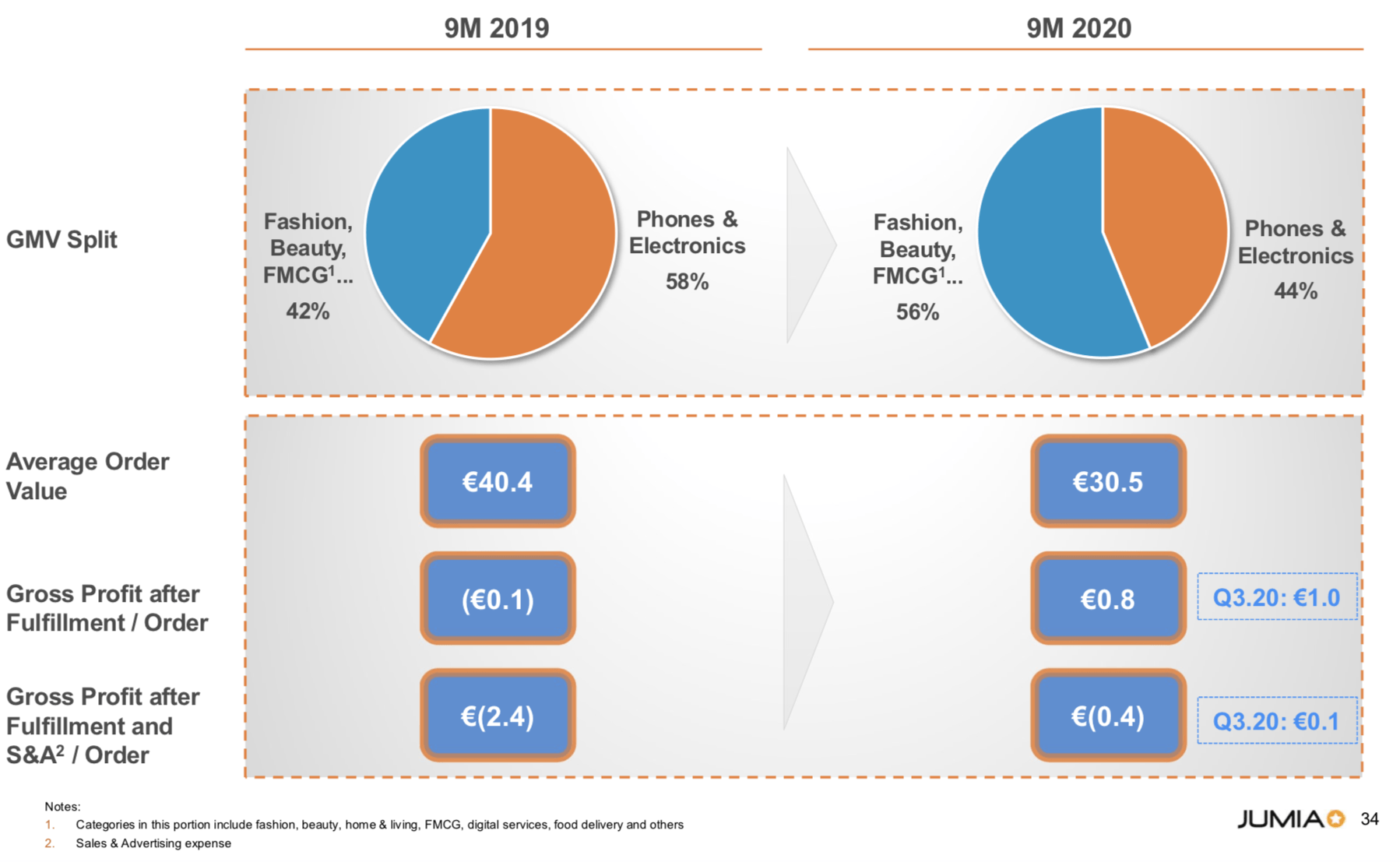

1) Continued shift to everyday products with more frequent purchase behavior and better margin profiles that will result in improved unit economics as shown in the financial data from the first 9 months of 2020;

Source: company presentation

2) Continued efforts to cut operating costs by leveraging economies of scale and its asset-light Jumia logistics & fulfillment offerings;

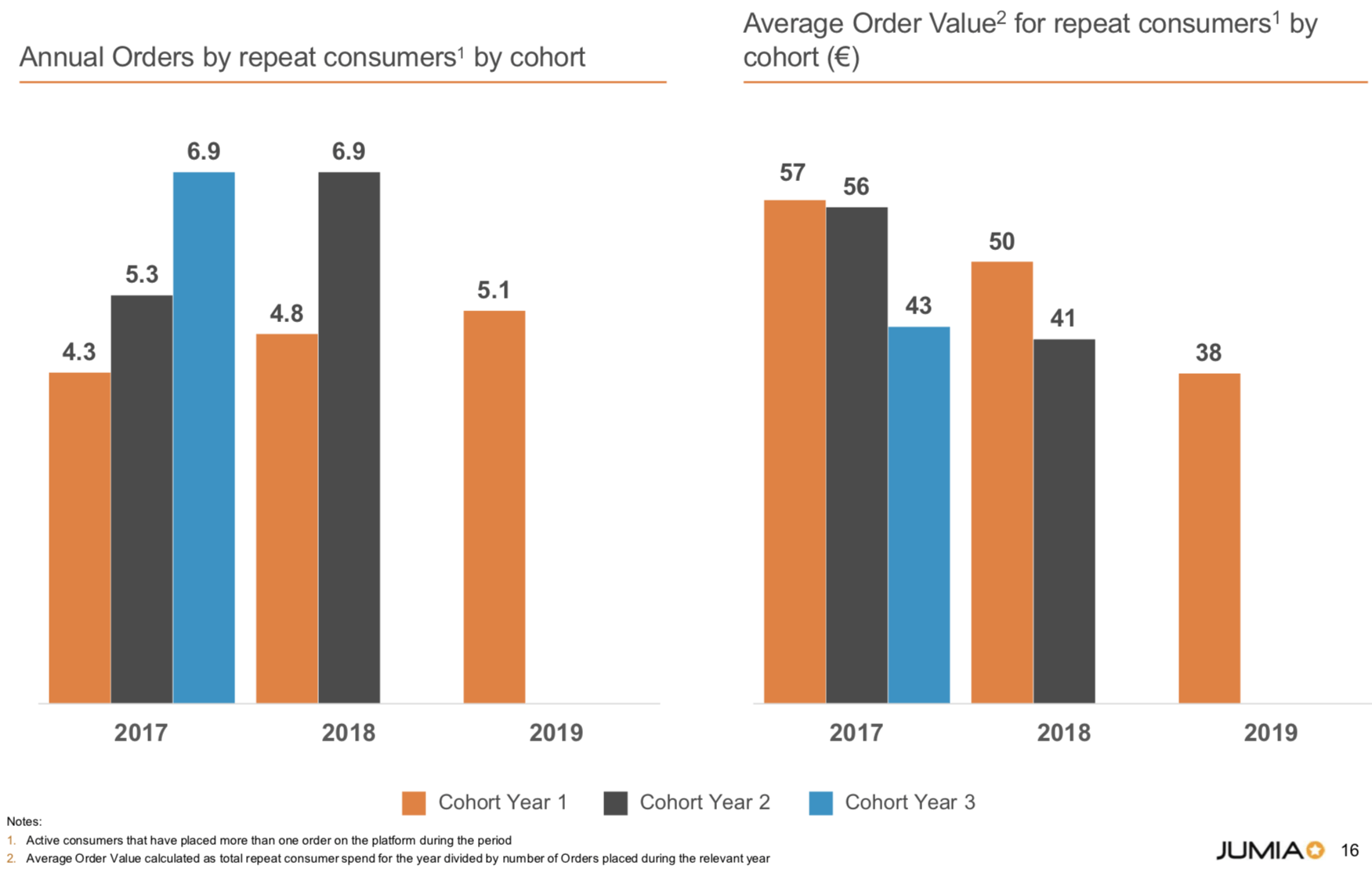

3) Continued efforts to maintain repeat purchase momentum across cohorts with a clear goal to start accelerating growth in the number of orders per consumer, fueled by initiatives like the Jumia Brand Festival;

Source: company presentation

4) Continued penetration of JumiaPay as a % of GMV on its e-commerce platform and start of additional 3rd party monetization potential.

JumiaPay may become a leading African fintech player

While it is apparent that online payments will at some point reach Africa in a similar way as they did in other parts of the world, the major question is just how fast this evolution will take place. Most research points to the large untapped opportunity in Africa by means of the high proportion of underbanked people. E-commerce certainly is the strongest driver of online payments adoption, and Jumia’s core offerings from both e-commerce and online payments may give the company an edge to benefit from both secular tailwinds.

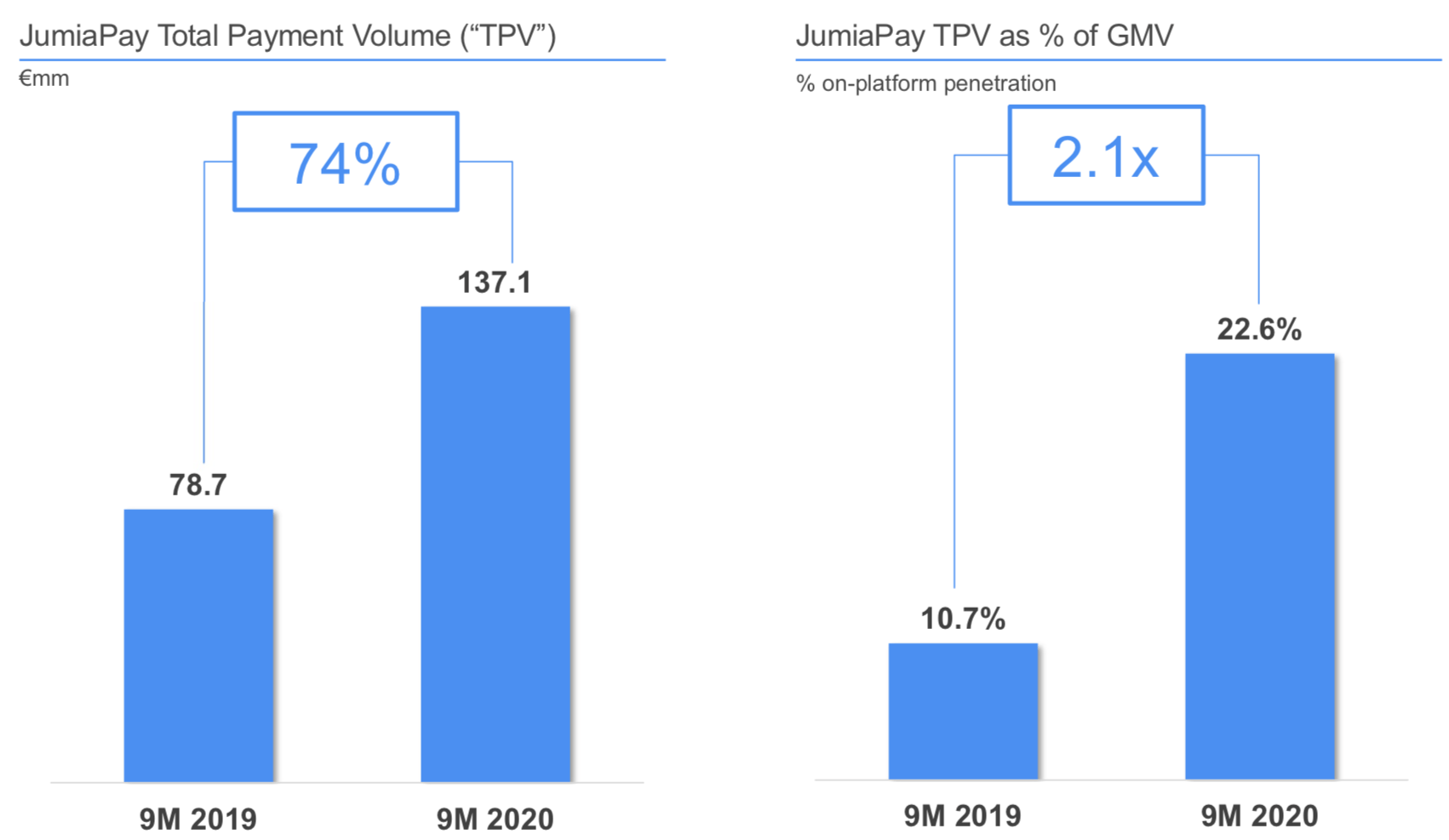

JumiaPay already has a large existing customer base and growth of JumiaPay has been one of the highlights during the past quarters: during the 9 months of 2020 JumiaPay TPV grew by 74% to €137 million and JumiaPay TPV as a % of GMV reached 22.6% (more than twice the number compared to the first 9 months of 2019).

Source: company presentation

In its most recent quarter JumiaPay TPV was €48.0 million (YoY increase of 50%), more than doubling on-platform TPV penetration vs. Q3 2019 to 25.6%. As mentioned earlier in this article, the most recent venture capital / investments rounds in African fintech confirm the large opportunity. JumiaPay platform and 3rd party monetization will be a key aspect to look at when Jumia reports financial results in the upcoming quarters.

Recent equity offering de-risks from further dilution

On Nov 30th Jumia announced an “at-the-market” equity offering which was completed on 3rd Dec and brought in proceeds of $231.4 million (see here). It was clear that at some point management would take advantage of the sharp stock price acceleration Jumia has experienced over the past few months. The company now has sufficient cash available to fund its activities well into 2022 and beyond. While in the short term Jumia’s stock may face some downward pressure due to the equity dilution, I believe the move de-risks the company moving into 2021 as further share price dilution becomes less likely.

Former Jumia bear Citron turns bullish and sees a $100 price target

Probably one of the most impactful short-attacks from the last few years hit Jumia just after it went public when Citron research published a destructive report in which it highlighted major discrepancies in the company’s financial statements. More importantly, Citron identified fraudulent behaviours in the way orders on Jumia’s platform were accounted for. Just after that Jumia’s management acknowledged that some improper sales practices were identified and actions taken. Not all of Citrons claims were supported by robust-enough evidence in the end. However, the short report from Citron was sufficient to disclose some problems in Jumia’s corporate culture, and sent Jumia stock price into a multi-month price deceleration.

Just recently, the picture turned and Citron went bullish on Jumia stock calling it the Generational Buy while claiming that

EITHER THESE YOUNG NIGERIANS WILL BE THE FIRST PEOPLE ON EARTH TO NOT ACCEPT E-COMMERCE OR THE STOCK IS GOING TO $100.

For those interested to read the bullish note from Citron, you can find it here.

While I can support many of the bullish claims that Citron makes, I want to provide an objective view on the company’s prospects also taking into account recent financial performance and structural barriers, as well as general risks to the company.

Risks & Competition

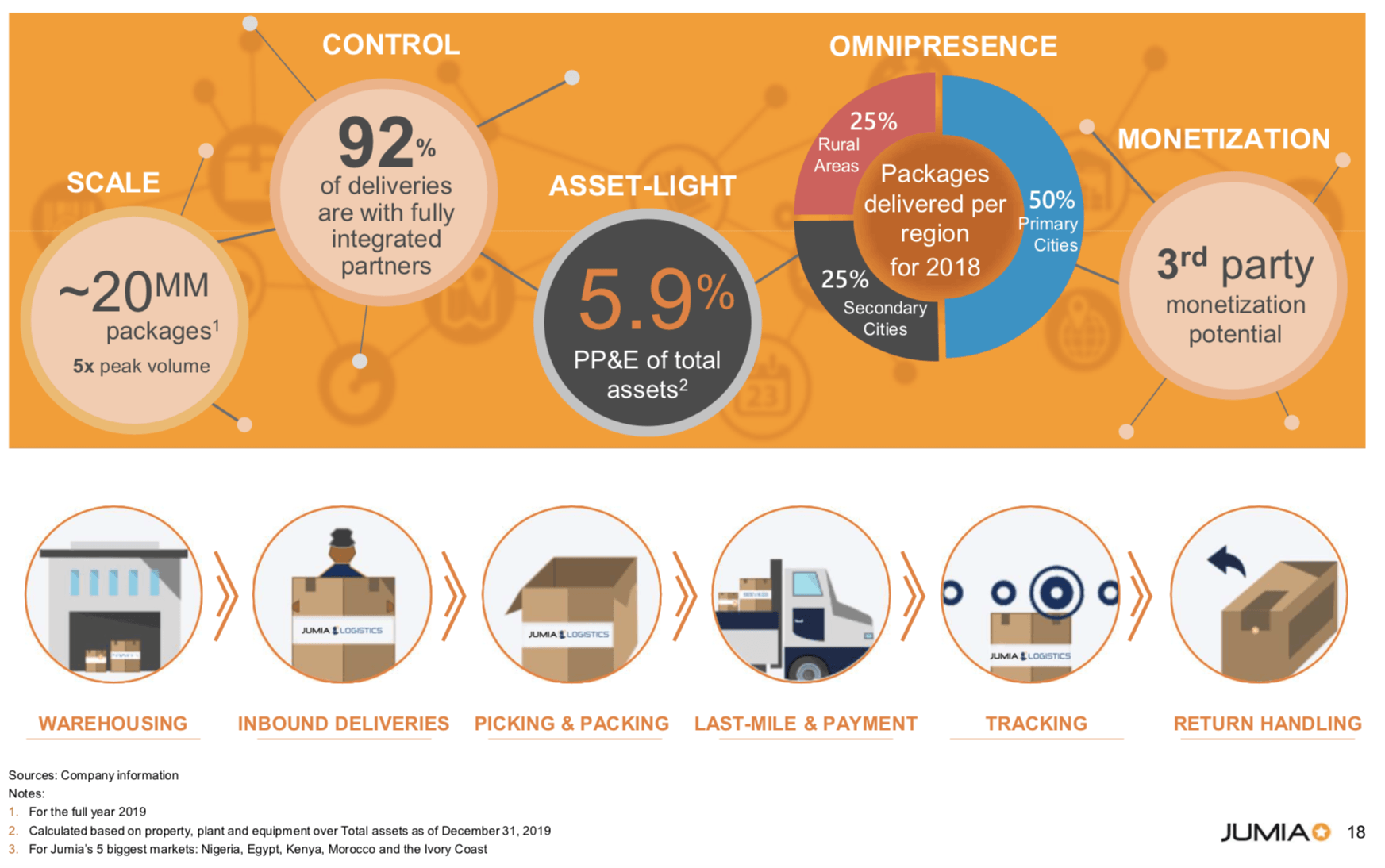

Jumia is the only fully integrated operator of e-commerce in Africa. While there at multiple players in different parts of commerce (e.g. Zando in South Africa) or fintech (Flutterwave, Paystack, Interswitch, O-Pay a.o.) there is no company that operates as a fully integrated services offerings platform across multiple countries. I see infrastructure as a major barrier to broad e-commerce adoption. I believe that Jumia’s logistics offerings will be a key differentiator and barrier to entry for competitors as it is hard to replicate that from scratch. Jumia’s logistics & fulfillment offerings are already well established and active in all major operating areas with an extensive network of fully integrated partners across the continent. Jumia already handled ~20MM packages for FY 2019 and 92% of deliveries are with fully integrated partners. Management says that Jumia logistics is asset-light and only accounted for 5.9% of property, plant and equipment of total assets as of Dec 31, 2019. During Q3 2020, Gross profit after Fulfillment expense reached positive €6.6 million, demonstrating continued unit economics improvements driven by its asset-light logistics offerings.

Source: company presentation

Another concern I have is the current level of online spending on consumer goods per person in Africa, which is still only a fraction (i.e. roughly 1/5) compared to other regions around the world (see here).

However, similar to Citron, I can only hardly imagine that the African population would not want to enjoy the same benefits from e-commerce offerings that many Western, Latin American, and Asian countries have experienced over the past years. Hence, it is probably rather a question of ‘when’ and not ‘if’ that investors need to take into consideration when looking at Jumia. E-commerce adoption is one of the strongest secular trends that we have experienced in all major economies in the world. I am not saying that Jumia must become the next Amazon (NASDAQ:AMZN) or MercadoLibre (NASDAQ:MELI), but by at least capturing a share of the potential $75 billion e-commerce market that McKinsey forecasts by 2025, Jumia may be well-positioned to become the leading pan-African player.

While competition is always a risk, I believe that Africa has very specific barriers to entry, especially with respect to infrastructure and last-mile delivery, especially in rural areas. Only a company with deep local expertise, which Jumia has built over the past years, can thrive and overcome those challenges. Therefore I do not believe that any large e-commerce operator, like Amazon would try to compete with Jumia by entering Africa on their own. I rather see a strategic investment from one of the big players as a potential scenario along the way.

The fact that barriers to entry may be higher in Africa does not mean that there won’t be setbacks for Jumia. The company already had to discontinue operations in many markets like Cameroon, Rwanda, and Tanzania. It may well be the case that more countries could follow if the economics or local competition don’t support the continuation of businesses in these countries.

I also see substantial competition in the African fintech sector, as demonstrated by the high level of venture capital investments into African fintech startups from big payment giants like Visa, Mastercard, and Chinese investors like Sequoia and Softbank. I see consolidation in the fintech space, especially in Nigeria, as being inevitable. Jumia needs to keep investing in its own platform and services offerings to make JumiaPay one of the leaders in the space. This stands in contrast to the ongoing cost-cutting measures that Jumia’s management is implementing.

Another risk I see is the high short interest in Jumia’s stock, with roughly 18% of all outstanding shares being sold short (see here). Following the significant stock price increase in the most recent weeks, a pullback of a significant magnitude would not surprise me at all, and it could be further accelerated by short-sellers adding to their positions.

Conclusion

In my view, Jumia is the most promising long-term play on the adoption of e-commerce and fintech in Africa. While Jumia’s most recent business metrics trend in the right direction, the company needs to prove it can re-accelerate revenue growth while it continues to pursue the business-mix shift towards higher-frequency, everyday order items with better unit economics.

For those that follow the company for a potential investment, I would urge to proceed with caution. While I have enjoyed the most recent stock price appreciation with my own investment around the March/April lows, I have also seen the other side of the stock price momentum after investing just around the IPO, when the company was alleged with fraud allegations and posted disappointing financial results. I continue to believe in the long-term prospects of Jumia to become the leading pan-African e-commerce play, and I also believe that JumiaPay will be one of the fintech solutions to survive the inevitable consolidation in the African fintech space.

While I am invested in the stock, I am currently taking a neutral positioning due to the most recent share price appreciation, and I would not recommend buying any shares at current levels. The trailing 12-month EV/sales ratio currently sits at a lofty ~14-15 times for Jumia. In comparison, Amazon has a TTM EV/sales ratio of ~4.5 and is growing at double the rate of Jumia and is by far the “safer”, more diversified investment with almost guaranteed long-term revenue growth.

While the Amazon comparison is not the fairest, Jumia itself has long claimed to be the “Amazon of Africa”, and I think it is just fair to hold management accountable for that. Before considering sizing up on my position in Jumia, I need to see further positive momentum in unit economics improvements and cost efficiencies. However, I need management to take caution to not jeopardize growth at all cost by scaling back investments into the business altogether. The recent equity offering should give management some leverage for investments into growth initiatives. Also, I need to see my thesis of improving YoY marketplace revenue growth comparisons translating into accelerating revenue growth as early as Mid next year. Lastly, JumiaPay needs to continue to be successfully integrated into the ecosystem. I hope to see strong JumiaPay adoption as a percentage of overall transactions to continue. I will be carefully watching venture capital flooding the African fintech space to see what competition does.

Overall, I expect volatility in the stock to continue and believe that there will be investment opportunities in the name at much lower stock price levels, unless the company surprises with significantly improved business metrics in the short-term.

Disclosure: I am/we are long JMIA, PYPL. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The author is long JMIA, PYPL,

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.