fizkes/iStock via Getty Images

In the U.S., recent retail earnings were almost a complete disaster with historic post-earnings plunges for some of America’s best known names. So it was quite a relief to see one of Africa’s top e-commerce companies, Jumia Technologies (NYSE:JMIA) pull off a 30.9% post-earnings surge. Going into earnings, e-commerce company JMIA had lost a soul-crushing 91.6% from last year’s all-time high. This stock market no longer pays a premium for risk and promises of future success. Jumia’s Q1 2022 earnings report indicated the company received the message. Management flipped from celebrating plans for future spending to emphasizing peak losses and the path to profitability. This turn-around comes just in time for the June celebration of Jumia’s 10-year anniversary.

Jumia Technologies [JMIA] tries for another bottom following a 30.9% post-earnings surge. (TradingView.com)

While the price chart above shows the major deflation in the stock, the graph below of enterprise value to sales demonstrates how thoroughly JMIA has returned to earth. I daresay, JMIA is in value stock territory.

Jumia has returned to a rock bottom valuation based on enterprise value and revenue. (Seeking Alpha)

“Scaling the business towards profitability”

Jumia’s present message on profitability consists of four points:

- Accelerating usage growth

- Accelerating monetization

- Improving cost efficiency

- Developing JumiaPay

Jumia achieved a near 2-year high in year-over-year order and GMV (gross merchandise value) growth. The growth is of course a pandemic-related favorable comparison. However, Jumia insists that it can maintain this kind of momentum going forward. Most notably, the accelerated order growth helped boost GMV growth despite a 9% decline in average order value (AOV). This decline will continue given management’s strategy to emphasize the purchase of everyday items. The share of sales from “everyday categories” has steadily increased from 55% in Q1 2020 to 67% in the latest quarter. These sales were enabled by the addition of almost 1 million FMCG (fast-moving consumer goods) SKUs. These share gains come at the expense of the sales of phones and electronics.

These sales dynamics pressure management to keep accelerating user adoption and growth. Fortunately, Jumia has “….been driving a consistent increase in quarterly purchase frequency over the past five quarters, reaching three orders for quarterly active consumer in Q1 this year, compared to 2.7 others same quarter the year before” (from the transcript of the earnings conference call). Management did not answer an analyst question on repeat customers with specific numbers.

Revenue and gross profit have also achieved near 2-year highs in growth rates (before customer incentives). The strongest message about a pivot towards profits comes from marketing efficiency and EBIDTA. Sales and advertising as a percentage of GMV peaked at 10.1% in Q3 of 2021. Jumia worked that number back down to 7.5% in the current quarter. Management was not completely clear on whether this reduction is a reflection of the seasonal drop-off from holiday promotional spending in Q4. Further reductions will occur from GMV growth as the company flattens out absolute marketing spending. From the transcript of the earnings conference call:

We’re stabilizing the level of marketing investment and we confirm that we expect to invest between $50 million and $55 million in sales and advertising for the first half of 2022. And this compares with $55 million in H2 of 2021. So, very similar level of investment, and this is why we call this a stabilization.

EBIDTA loss hit a whopping -$70.0M in Q4 2021. Jumia claimed that mountain of red ink as the moment of peak losses. Still the -$55.3M loss in Q1 2022 is a 69.6% year-over-year increase. Jumia has a lot more work ahead to achieve its goal of EBITDA year-over-year declines starting in 2023. For example, fulfillment expense scaled a bit faster than order growth, 42% versus 40% year-over-year.

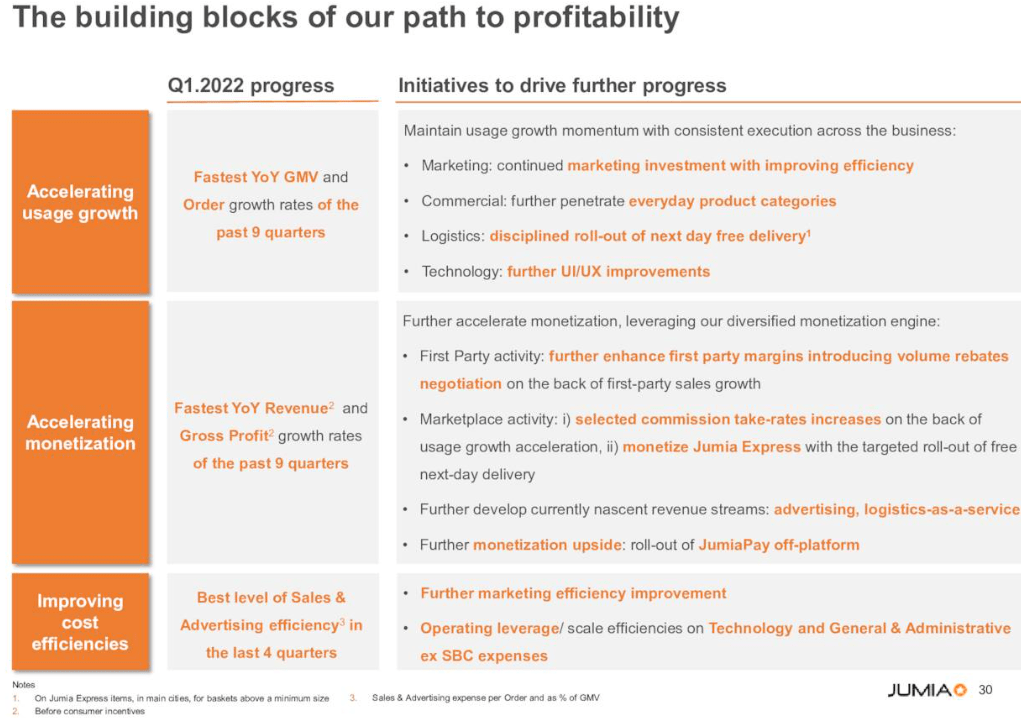

The following chart from the earnings presentation summarizes Jumia’s religion on getting to profitability:

Jumia’s path to profitability (Jumia Technologies)

Note that Jumia is plowing some of its increased monetization into consumer incentives like pricing and shipping discounts. The boost from $2.1M to $7.2M year-over-year likely helped drive the accelerated order and revenue growth.

JumiaPay

Jumia announced a breakthrough in licensing in Nigeria and Egypt for off-platform use of JumiaPay. These are exciting developments, but the payoff is far enough in the future that Jumia is not including the growth prospects in any forecast expectations: “It’s not a prerequisite for us to reach breakeven, but it will be incremental monetization upside to give us even more flexibility and optionality in our path to profitability.”

JumiaPay total payment volume was up from 37% year-over-year (45% on a constant currency basis). The percentage of GMV also increased year-over-year from 26% to 28%. However, JumiaPay did not pace with the rapid order growth. As a percent of total orders, JumiaPay transactions dropped year-over-year from 36.7% to 34.4%.

Logistics business

Jumia’s logistics business hit a company record of 3.5M packages shipped. Jumia earned $1.2M across 1,250 logistics customers.

Jumia is serious about using logistics as a competitive advantage. Jumia Express offers next-day free shipping for minimum order sizes. The $15M-$25M Jumia expects to spend in 2022 on capital expenditures will have large logistics component (specifics not provided).

Surprisingly, Jumia said nothing about its recent partnership with UPS in Africa. Analysts did not ask about it either. In coming quarters, I want to understand how this partnership supports scaling the business towards profitability.

The Trade

I added to my core holding of JMIA shares as the stock pulled back from the initial 24.7% surge following the UPS news. I have my fill of shares for now, and I am looking for the stock to stabilize. JMIA’s valuation is at rock bottom levels and reflects a lot of fear about the future. I remain as optimistic as ever about Jumia’s prospects, but I am bracing for a lot of churn ahead before any upward momentum reappears. Jumia’s management is (outwardly) unconcerned about the macro-environment (which in turn concerns me a little!). Jumia is banking on a baseline amount of non-discretionary spending to carry them through:

….at the end of the day, we are amazingly well positioned because we are offering a very wide range of assortment. And we are offering solutions and access to consumers of products, which are very relevant with our position in the everyday categories, and we have very good prices. So, at the end of the day, we are a reflection of the supply and whatever disruption is happening on the supply…the beauty of Jumia is that we bring this amazing assortment, we bring this amazing experience and we bring very good prices. So, consumers will still need to buy everyday products, they will still need to do that.

For now, financial markets clearly feel no need to buy JMIA. That attitude should change in due time and make the 10-year anniversary a trough year.

Be careful out there!