The cost of shipping a container of goods across the ocean has increased dramatically over the past couple of years due to a series of unfortunate supply chain disruptions, including but not limited to the Covid-19 pandemic, lockdowns, panic-buying, demand shifts and the war in Ukraine.

Beginning around June of 2020 and really picking up speed later that year, the Freightos Baltic Index shows that the cost to contract a container ship rose by approximately 700% between mid-2020 and highs reached in September 2021.

Naturally, container ship stocks moved up in price accordingly, though like most cyclical stocks, their stock prices could not keep up with their earnings growth, resulting in low price-earnings ratios. Then, there are the high dividends to consider as these companies returned cash to shareholders.

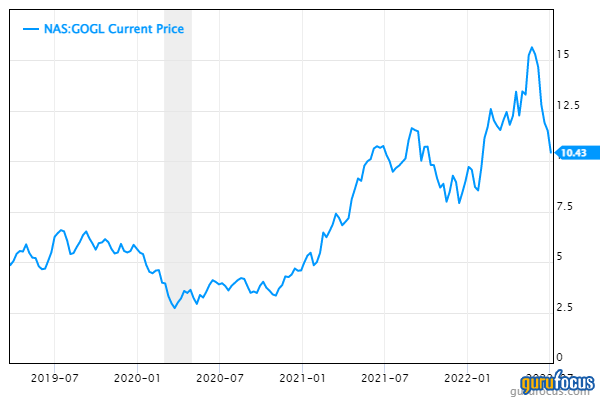

For example, Bermuda-based Golden Ocean Group Ltd. (GOGL, Financial) has seen its price rise 12% over the past year overall despite a more recent drawdown. Its price-earnings ratio is 3.89, while its dividend yield is an incredible 26.33%. JPMorgan (JMP) upgraded shares from neutral to overweight at the beginning of April, but the stock has just kept falling since then.

With all of the above going for it, how could an investor possibly go wrong with buying shares of Golden Ocean, or any number of its peers with similar numbers for that matter? Fairly easily, as it turns out. The ocean freight industry is a heavily cyclical one and rates are moving decisively down again, which could spell trouble for investors trying to hop on the hype train near the top.

Rates heading down, blanks on the rise

The Freightos Baltic Index’s Global Container Freight Index shows that after a seven-fold rise, shipping rates have come down from over $11,000 per 40-foot equivalent (FEU) in September 2021 to about $6,500 per FEU as of this writing. While that’s still a massive increase from the pre-pandemic levels of $1,400 per FEU, we are definitely seeing a downtrend.

The FBX01 Asia-West Coast assessment, which includes premium charges, is down to $7,400 per FEU from September highs of more than $25,000 per FEU. Pre-pandemic, the rate was around $1,500 per FEU.

The industry passed an important benchmark in late June, with long-term ocean freight rates between China and the U.S. falling below spot prices for the first time since April 2020.

Since May, the major shipping alliances have been utilizing “blanked” (also known as cancelled) sailings in order to prop up rates. This measure was initially meant to tide them over until the end of China’s Covid lockdowns, but continued as demand continued to drop.

Part of this has do to with congestion at California ports easing as the volume drop from China’s Covid lockdowns brought much-needed time to catch up on all of the ships stuck at port waiting to be unloaded. Part of it can also be attributed to a not-insignificant volume shift from the West Coast to the East Coast on fears of labor union negotiations for port workers’ contracts that expired on July 1.

However, the majority of the weakness is coming about as a global economic slowdown unfolds at the fundamental level: namely, the demand for transportation of goods.

A global economic slowdown is unfolding

Some analysts maintain they expect shipping prices to rise again as soon as China’s Covid lockdowns are over. After beginning to ease Covid restrictions in the beginning of June, the country began to walk back on that decision somewhat, and it is not clear when they will end for good.

What many forget, though, is that China is not the only part of this equation. Concern is growing over the impact of inflation on demand in the U.S. as consumer spending power is rapidly eroding.

While the official inflation numbers as measured by the CPI are around 8.6%, we need to keep in mind that inflation actually has a higher impact than that on most consumers’ wallets. Why? Because for non-wealthy Americans, the biggest expenses by far are housing and food, which often eat up more than half to nearly all of their paychecks. Housing prices are up more than 20% year over year in many markets, while the cost of food has risen 10%.

Thus, for many, inflation is much higher than the CPI would indicate. Add in the fact that Americans no longer have stimulus checks and savings from the initial Covid lockdowns and it is clear the factors that originally granted some defense against inflation are no longer at play.

Though the U.S. accounts for an outsized percentage of consumption, the inflation problem is worse outside of the country, especially in emerging markets. Sri Lanka and Russia have recently defaulted on their debt, and other emerging markets could soon follow as the Federal Reserve’s hiking of interest rates further strengthens the U.S. dollar, making it more difficult to service dollar-denominated debt.

This is expected to cause an entire wave of defaults as spooked investors pull money out of emerging markets. After a 20% year-to-date decline, about a quarter of nations tracked in the Bloomberg Emerging Market USD Aggregate Sovereign Index are trading in distress.

Meanwhile, in Europe, nations are seeing inflation soar due to the energy and food crises caused by Russia’s war on Ukraine.

It is not just China or the U.S. We are seeing a truly global economic slowdown, which is likely to put further downward pressure on ocean freight rates in the future.

Takeaway

It is easy to get caught up in the euphoria of a rising stock price, especially when it is accompanied by hefty dividend payouts. This is why investing in cyclical areas of the market, like ocean freight stocks, is so tough; it is impossible to predict exactly when an upturn will become a downturn.

While it is possible that the easing of China’s Covid lockdowns will result in an uptick in ocean freight rates, I do not think it is likely, and even if it does play out like that, I think it will be short-lived. Further declines in ocean freight rates means falling profits (and dividends) for ocean freight stocks, which would plunge the stocks of these companies into a cyclical downturn.