Drew Angerer/Getty Images News

After contesting new 52-week lows during a steep sell-off in U.S.-listed Chinese stocks earlier this week on renewed delisting fears amongst other macroeconomic challenges, NIO (NYSE:NIO) posted a sharp rebound during the mid-week regular session. The stock plunged towards $13 on Tuesday, marking year-to-date declines of 62% (peak to trough), and wiping out 81% of its value since peaking at $66.99 earlier last year. Yet, during the following session on Wednesday, the stock opened at $17.64, 18% higher from the previous day close, and ended with intraday gains of as much as 12%. The stock’s movement in the past two days continue to underscore the theme of soaring volatility for the broader cohort of Chinese stocks as investors continue to grapple with ever-changing regulations and reporting requirements.

On one hand, NIO has been severely punished by the market since the onset of Beijing’s regulatory crackdowns last year. Although NIO and the broader Chinese electric vehicle (“EV”) has yet to experience any material changes to its operating environment nor its growth trajectory like those experienced by the internet sector as a result of Beijing’s ongoing regulatory overhaul, the stock has nonetheless experienced spillover effects. Meanwhile, on the other hand, NIO remains at the center of delisting risks stemming from the SEC’s adamant requirement for compliance with PCAOB audit inspection rules, although its recent “homecoming” listing in Hong Kong seeks to mitigate some of the related risks.

But in a shift back to NIO’s fundamental prospects, EV adoption remains strong within the automaker’s core Chinese market and supplementary European market. The upcoming addition of sedans to its line-up, which would make a new vehicle segment to its current SUV-dominant product portfolio, paired with the roll-out of a sub-brand is expected to help NIO better penetrate the fast-growing EV market. Supply chain constraints are also expected to ease in the latter half of the year, which would complement NIO’s continued efforts in ramping up its production line and boosting delivery volumes for top-line growth. Although local Chinese consumer sentiment remains damp, the last of EV subsidies this year is expected to help maintain vehicle sales growth and offset some of the near-term economic headwinds. A gradual uptrend for the NIO stock is expected to resume later in the year, despite some turbulence along the way, as China continues to resolve regulatory woes for domestic companies and work with the U.S. on abating delisting risks, while industry-wide supply chain constraints begin to ease.

What Does Beijing’s Recent Vow to Support Overseas Listings Mean for NIO?

It has been tumultuous month for the NIO stock and its U.S.-listed Chinese peers. The onset of the latest landslide for U.S.-listed Chinese stocks began last week shortly after the SEC identified five companies within the cohort – including Yum China Holdings Inc. (YUMC), Zai Lab Ltd. (ZLAB), BeiGene Ltd. (BGNE), ACM Research Inc. (ACMR) and HUTCHMED (CHINA) Ltd. (HCM) – at risk for delisting “if they fail to comply with the [Holding Foreign Companies Accountable Act’s] auditing requirements for three consecutive years”. In fact, last Thursday marked the “worst day of trading since the global financial crisis” for U.S.-listed Chinese stocks due to renewed regulatory woes.

Yet, the NIO stock, alongside its U.S.-listed Chinese peers, posted steep rebounds during Wednesday’s session after “China’s state council vowed to keep its stock market stable”. A report released by state-media Xinhua News on Wednesday reaffirmed Beijing’s efforts to “keep its stock market stable and support overseas share listing”, and cited “efforts to rectify internet platform companies should end soon”. The recent turn of events has been music to the ears of investors in U.S.-listed Chinese stocks, like NIO, which have been plagued by a broad-based regulatory overhang in the past year due to Beijing’s opaque rule book and the SEC’s tightening reporting requirements for the cohort. The stock’s rebound on Wednesday also underscores heightened market sensitivity to regulatory changes for U.S.-listed Chinese companies, amongst other macroeconomic challenges from soaring price pressures to intensifying geopolitical tensions.

As mentioned in earlier sections, the sell-off of NIO stocks over the past year is largely the result of investors’ concerns over the future of U.S.-listed Chinese stocks due to the large regulatory overhang. Although we had previously assessed related risks for NIO as low, the stock has, nonetheless, suffered from the spillover effects of soured investors’ sentiment following repeated growth-suppressing regulatory overhauls ordered by Chinese regulators on the internet sector.

However, it should not be overlooked that NIO, alongside its Chinese EV peers, are largely differentiated from big internet stocks, like Alibaba (BABA) and Tencent (OTCPK:TCEHY). While big internet stocks have experienced some of the most significant declines amidst Beijing’s ongoing regulatory crackdowns, related impacts to the Chinese EV sector have been relatively less pronounced as automakers have yet to experience any materially adverse repercussions to their growth trajectories as a result of direct regulatory changes. This is largely due to the critical role that the EV sector continues to play in China’s journey towards becoming carbon neutral by 2060. In fact, China’s EV sales have continued to accelerate at an unprecedented rate, thanks to the Chinese government’s intervention through generous consumer rebates on eligible EV purchases. The Chinese government’s support for the nation’s EV sector is also officialized through the five-year State Development Plan for the New Energy Automobile Industry, which plans to have EVs account for 20% of total vehicle sales by 2025 and become the mainstream choice by 2035 to ensure China’s continued dominance in the global EV market.

While Beijing’s vow to support market stability and overseas shares listing on Wednesday has effectively lured the return of some buyers after a relentless, yearlong sell-off of Chinese equities, concerns remain on whether the latest rally is sustainable. It will likely take a few more quarters of consistent improvement to China’s regulatory landscape and economic recovery to convince investors that the rout has in fact come to an end. But the Chinese State Council’s announcement yesterday, paired with confirmation that ongoing internet sector crackdowns are nearing an end, is definitely a boost of confidence for investors, especially for high-growth Chinese EV stocks. Wednesday’s announcement marked one of the few times that Beijing has provided clear affirmation on where its political and regulatory agenda is headed since the crackdowns began in late 2020, and may point to the beginning of a broader recovery for U.S.-listed Chinese stocks ahead. The latest development is especially favourable for NIO, whose fundamental prospects remain intact even after Beijing’s tightened regulatory grip over every sector in the past year as part of its broader efforts in restoring “common prosperity” and equitable growth.

What Does China’s Stance Regarding Compliance with SEC Reporting Requirements Mean for NIO?

Meanwhile, China has also started to directly address the SEC’s requests for compliance with its audit inspection rules. Following the SEC’s identification of five companies last week that are at risk of delisting if found non-compliant with PCAOB audit inspection requests within the timeline (i.e. three consecutive years beginning 2021) stipulated in the Holding Foreign Companies Accountable Act, China’s Securities Regulatory Commission (“CSRC”) responded by saying “it would like to work with U.S. regulators on the accounting inspections in line with international practices”. This has largely contributed to the stock’s latest rally, as the CSRC’s change of tone helps to abate some of the renewed delisting fears.

To date, mainland China and Hong Kong remain the only regions that have not complied with PCAOB audit inspection requests. Last year, registered public accounting firms in mainland China and Hong Kong have signed audit reports for 191 publicly listed companies with a combined global market cap of $1.9 trillion, yet the PCAOB has not been able to effectively access and conduct independent inspections on these audits due to “national security concerns” raised by China.

In the latest development, the CSRC is “considering allowing U.S. officials to inspect documents on firms that do not possess sensitive data”, but the agency would still like the ability to “withhold sensitive data from inspection” where applicable on the grounds of national security concerns. However, the offer still does not address the key reason for PCAOB audit inspections, which is the need to assess “unredacted” audit papers to ensure information reported in publicly disclosed financial statements are reasonable and free from material misstatements. The CSRC’s recent consideration also defies the purpose of the Holding Foreign Companies Accountable Act, which was enacted in late 2020 to ensure all issuers in the U.S. stock exchange are subject to the same rules and regulatory treatment, including compliance with PCAOB audit inspection requirements.

Nonetheless, statements issued by both the PCAOB and the CSRC last week affirming their respective interests in finding a mutually acceptable solution to the issue, paired with China’s confirmed support for overseas share listings this week are favourable developments. They also represent a significant step towards resolving yearslong scrutiny over the SEC’s leniency on Chinese non-compliant with PCAOB audit inspection requirements, which have time and again contributed to fraudulent reporting by Chinese companies like Luckin Coffee and Orient Paper. The CSRC’s latest acknowledgement of the need to work with the PCAOB in finding common ground continues to corroborate an optimistic outcome, which would benefit NIO’s valuation prospects over the longer-term.

In the meantime, NIO’s latest homecoming listing by introduction (i.e. a secondary listing where no additional shares have been issued and no new capital have been raised) in Hong Kong and a planned listing by introduction in Singapore also provides partial mitigation to delisting risks, which should alleviate some of investors’ related concerns. In the unlikely event of a delisting from the NYSE, NIO shareholders from its primary U.S. listing would now have an option to convert their ADRs for Hong Kong listed shares, albeit the latter being less attractive considering the Hong Kong exchange’s “less active and liquid market” with two times less turnover on average compared to American exchanges.

Is NIO Still Investable? What You Need to Consider Ahead of Upcoming Earnings

As mentioned in the foregoing analysis and discussed in further detail in one of our previous coverages on the NIO stock, the Chinese EV maker’s fundamental growth prospects remain largely intact. The upcoming start of deliveries on the ET7 and ET5 sedans, as well as the all-new ES7 SUV will continue to complement NIO’s ongoing efforts in acquiring a greater share of China’s fast-growing EV market. The upcoming release of a sub-brand, in which NIO has touted during its Q2’21 earnings call, will also improve its appeal to the mass market and corroborate its efforts in penetrating opportunities within China’s smaller tier 3 cities.

Compared to Chinese big tech, NIO remains an investable option based on considerations that its underlying business’ growth prospects have not been materially altered as a result of Beijing’s ongoing regulatory crackdowns. While we acknowledge that a large regulatory overhang still exists, especially over concerns of potential delisting from the NYSE if the CSRC and the PCAOB cannot reach common ground before time runs out, the company is still well-poised for significant fundamental growth in coming years as global EV adoption continues to accelerate. This is expected to buoy uptrend performance for NIO’s Hong Kong shares as well and partially insulate ADR holders in the U.S. from material impairments to their investments under the worst-case scenario should a delisting from the NYSE ensue down the road.

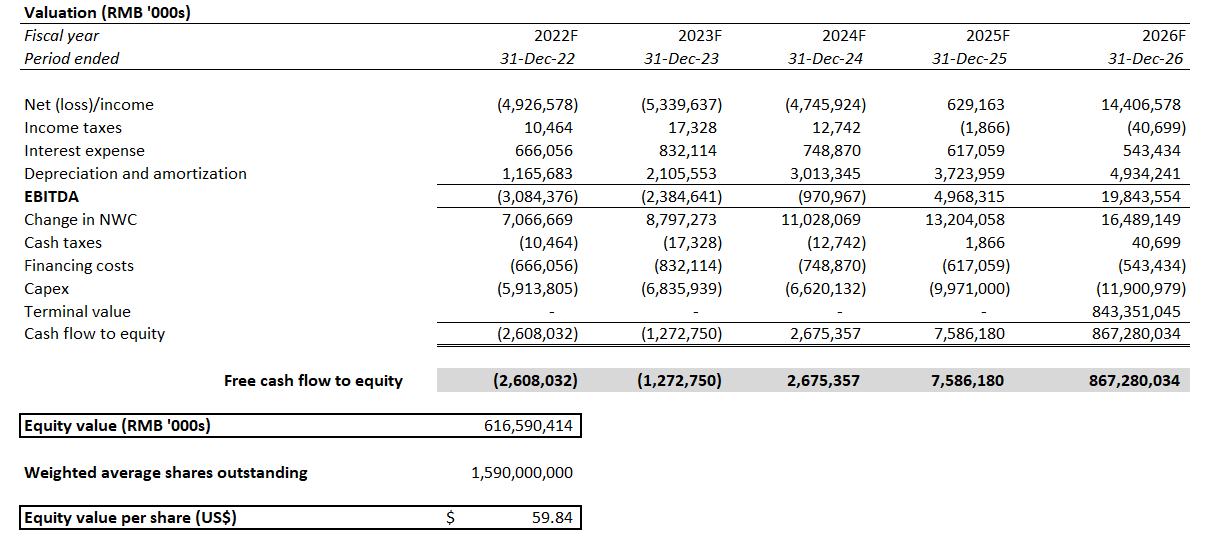

As analyzed in our previous coverage on the stock, our base case price target remains at approximately $60 based on NIO’s historical fundamental growth trends and market-share-gaining opportunities ahead. But considering recent volatility stemming from both China-specific concerns and broader macroeconomic challenges for global equities, we have performed a sensitivity analysis to determine what NIO’s current stock price implies and where it could be headed within the next 12 months.

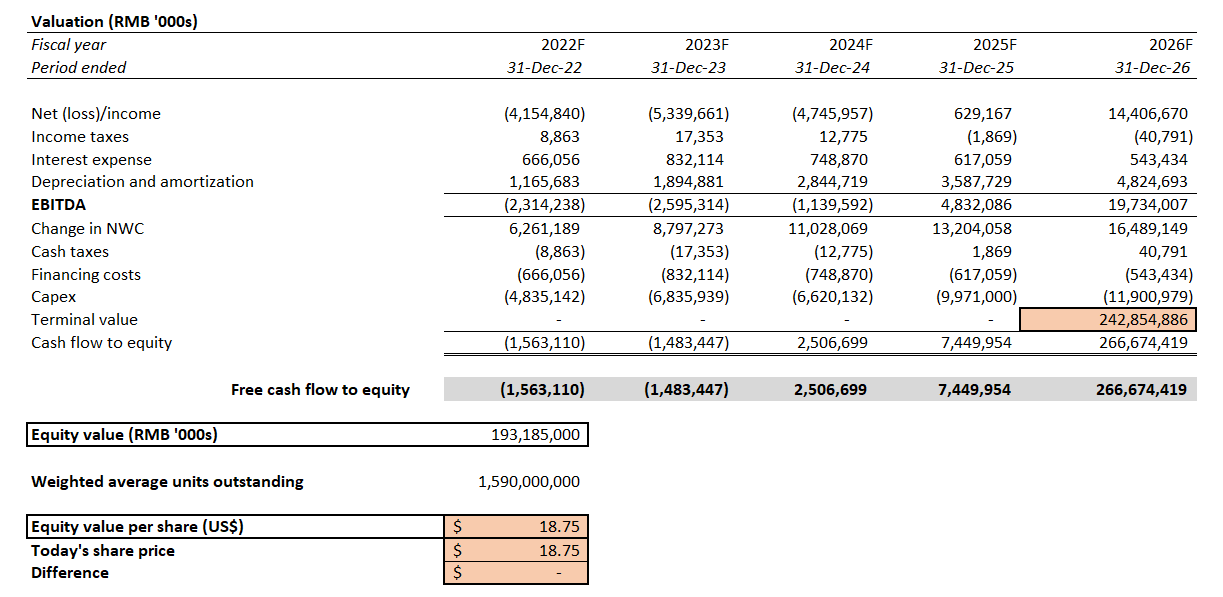

Drawing on our base case fundamental forecast analyzed here, NIO’s current share price of $18.75 (March 16th close) implies a perpetual terminal growth rate of -1%. In other words, the market is currently pricing NIO as if it is in a declining business, when it is in fact still sitting on massive growth opportunities in coming decades. While the global transition to EVs is imminent, continued adoption of the emerging mode of transportation is still in its infancy, meaning significant additional growth headroom remains on the horizon for NIO. The BNEF considers EV adoption to be at an inflection point when they account for 8% to 10% of a region’s total annual new car sales – so far, only China and parts of the EU like Norway, in which NIO has established operations in, have recently achieved such statistics, and continues to grow towards being the mainstream consumer choice.

i. Base Case Valuation Analysis:

NIO Base Case Valuation Analysis (Author)

ii. Implied Perpetual Terminal Growth Rate @ $18.75 Per Share:

NIO’s Current Implied Perpetual Terminal Growth Rate (Author) NIO’s Current Implied Perpetual Terminal Growth Rate (Author)

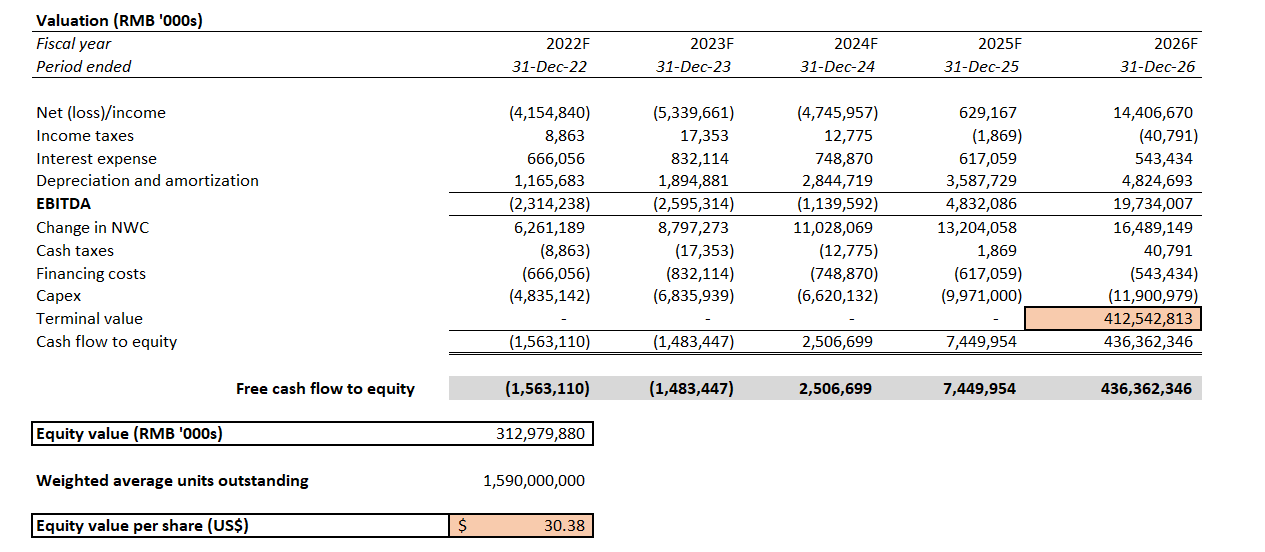

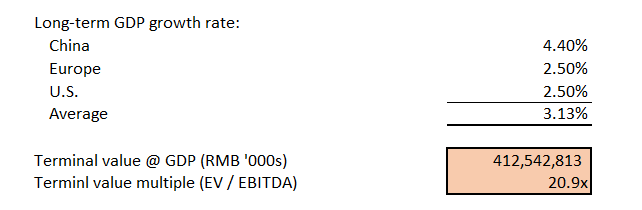

Let’s say, under the most conservative case, that NIO is valued based on the assumption of implied perpetual growth in alignment with the economic prospects of its core markets in the long-run (i.e. China, Europe, U.S.), the stock would be valued at about $30. And this is likely the fair scenario for the NIO stock in 2022 considering ongoing market uncertainties, in addition to industry-specific headwinds like protracted supply chain issues and China-specific regulatory woes. Based on the stock’s last traded share price of $18.75 on March 16th, a $30.38 12-month price target would still imply upside potential of more than 60%.

iii. Projected Valuation with Implied Perpetual Terminal Growth at GDP:

NIO’s Valuation Prospects with Growth at GDP (Author) NIO’s Valuation Prospects with Growth at GDP (Author)

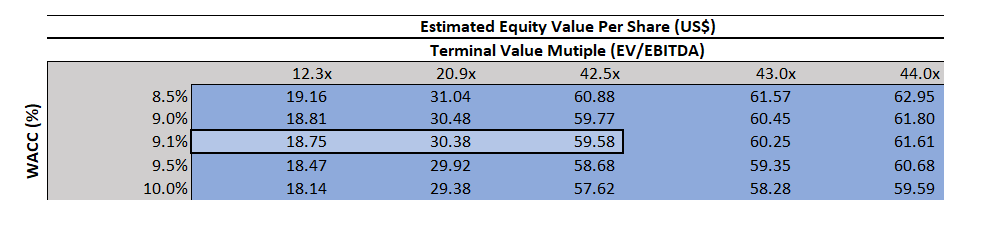

iv. Sensitivity Analysis:

NIO Sensitivity Analysis (Author)

Key near-term catalysts for jumpstarting the stock’s uptrend towards $30 over the next 12 months would include on-schedule customer deliveries for new vehicle models (i.e. ET7, ET5 and ES7), continued overseas expansion, accelerating growth in orders, easing supply chain constraints, and continued support from China on overseas listings, which we expect management to provide colour on at NIO’s upcoming earnings call:

- On-schedule customer deliveries for new vehicle models: The ET7 full-size sedan has already started rolling off NIO’s production lines and is expected to begin initial customer deliveries later this month. Meanwhile, the ET5 mid-sized sedan, unveiled in December during NIO Day 2021, will begin customer deliveries in the fall, with the ES7 SUV to start deliveries after. With NIO’s Q4’21 reporting being late in the quarter (March 24th), we are expecting management to provide updates regarding progress on the start of productions and customer deliveries for the new models, as well as their reservation volumes and/or customer take rates. We are optimistic that management is progressing on schedule for the new vehicle roll-outs, as the ET7 is already out for test drives at the Hefei NIO House in line with management’s earlier expectations for deliveries to begin in early 2022. Addition information on NIO’s progress in the development of its sub-brand will also be welcomed by investors at its upcoming earnings call, as related details remain limited to those briefly mentioned during the Q2’21 earnings call. Positive progress would imply that NIO is progressing as planned regarding efforts in capturing mass market share ahead of rapid EV adoption and increasing competition within the sector, which would bolster investors’ confidence in the stock’s long-term growth outlook.

- Continued overseas expansion: NIO is slated to continue its expansion in Norway, alongside additional store openings in Germany, the Netherlands, Denmark and Sweden later this year as part of its overseas expansion efforts. With Europe currently being the world’s second-largest EV market, on-schedule progress with penetration into the region will be critical for NIO’s longer-term business outlook, as well as improved valuation prospects as a global EV maker.

- Accelerating growth: Another key catalyst on the lookout includes NIO’s fourth quarter growth trends and current year/period growth guidance for both deliveries and orders/reservations. An accelerating order book will underscore NIO’s continued strength in capturing opportunities ahead of surging EV demand, while continued revenue growth will imply robust improvements to NIO’s production ramp up. Positive growth trends will also bolster NIO’s track record in swiftly navigating through unprecedented supply chain constraints and production challenges that have upended the automotive industry over the past 12 months. Any update on NIO’s ongoing expansion of production facility at NEO Park will also provide further visibility on NIO’s revenue outlook ahead.

- Easing supply chain constraints: As discussed in our previous coverage, NIO has demonstrated continued strength in navigating through ongoing supply chain woes. However, while many automakers have cited earlier that the worst of ongoing chip supply shortages are behind them, the recent outbreak of war between Russia and Ukraine might add uncertainties to that outlook in the near-term. Still, the supply chain bottlenecks are expected to see further easing in the latter half of the year, which would further benefit NIO’s continued strength in outperforming some automotive peers with regards to managing related challenges. Meanwhile, on the pandemic front, recent COVID outbreaks across China have forced many automotive manufacturers like Toyota (TM) and Tesla (TSLA) to temporarily suspend productions. Although there has not been any news of plant closures for NIO, we are expecting some degree of COVID-related supply chain and labour disruptions, but related impacts are not expected to be material considering production has not been subjected to extended periods of suspension.

- Continued support from China on overseas listings: Based on recent trends observed across U.S.-listed Chinese stocks, continued support from China for overseas listings and commitment between the CSRC and SEC in finding common ground over reporting requirements remain the most significant sentiment boosters. While NIO is not expected to touch on the subject directly, aside from potential allusion to its recent Hong Kong listing, any progress on a regulatory resolution would be a key catalyst in restoring uptrend momentum for the NIO stock over the longer-term.

Conclusion

Based on the foregoing analysis, NIO’s fundamental growth prospects remain intact despite Beijing’s changing regulatory agenda. This means the stock is not deserving of its currently depressed price performance, which reflects the prospects of a declining business based on our sensitivity analysis in earlier sections. The EV maker continues to benefit from strong global adoption and continues to show strength in navigating through unprecedented supply chain challenges. Although China, NIO’s core market, is seeing some setback in consumer sentiment this year, the EV subsidy program that is slated to end in 2023 is expected to provide partial compensation by pulling forward purchase decisions. And NIO’s upcoming roll-out of new vehicle models this year is expected to further complement this trend and support continued sales growth amidst a challenging macroeconomic backdrop.

We would recommend the NIO stock as a buy at current price levels, considering the low likelihood of it being a direct target of ongoing regulatory changes, which means its underlying business growth prospects as discussed above remain intact. The stock’s latest homecoming listing in Hong Kong also mitigates some of the delisting risks, with its valuations expected to maintain sustainable growth buoyed by fundamental opportunities ahead. Yet, the investment pick is not for everyone and investors will still need acknowledge potential spillover impacts from Beijing’s regulatory woes and be able to stomach delisting risks from American exchanges, which could further dampen NIO’s valuation outlook.

Author’s Note: Thank you for reading my analysis. Please note that I am in the process of planning a subscription service with Seeking Alpha’s Marketplace. The service will allow you to follow my model portfolio, interact with me directly, and participate in chat rooms with other subscribers. I’ll be launching in the near future with a legacy discount for early subscribers and I’ll be sharing more details as we ramp up to launch in the coming months.