The Income Factory® has gained a lot more acceptance from the mainstream investment community since I first developed and shared the strategy and ideas behind it here on Seeking Alpha over the past decade. But judging by comments and questions, many readers and followers still find it to be a novel and unfamiliar concept. So here is a quick “Cliffs Notes”-style introduction, with links to back-up materials and articles for those who want a more in-depth and detailed understanding. (Anyone who wants the whole enchilada in a single publication may wish to check out the book.)

Here are the basic principles of the Income Factory philosophy and strategy

It was inspired by the work of Charley Ellis, famed investor and author, who wrote an article that later became a classic book called Winning the Loser’s Game. In it Ellis compares investing to amateur tennis, where he says most points are lost by players making bad shots, rather than being won by players making good shots. Ellis shows how this is true in golf and even in war, where avoiding doing the wrong thing is the key to success much more than doing the right thing. Anyone who’s read War and Peace knows that Tolstoy would probably agree with him. In investing, doing the “wrong thing” often involves trying to beat the averages (i.e. hit “winning shots” that turn out not to be winners), or, even more typically, losing one’s nerve and selling out at what turns out to be a low point or even the bottom of a market slump. Such mistakes are often compounded by then “being on the platform and missing the train” when market prices turn up again, as history has shown us they eventually do.

The Income Factory is a strategy that helps many investors feel more secure about “staying on the train” when markets are behaving like roller coasters. It does it by creating a portfolio that depends mostly on cash distributions as the primary source of total return, with growth being a secondary and less important element. It relies on the fact that while “market growth” is the more exciting element in the total return calculation, and the one that gets most of the media attention, cash distributions are equally valid sources of return. That’s because the total return calculation is indifferent to whether the source of the return is cash or market growth. This is not a radical position, even though it cuts against the current trend which is to obsess about market movements and price growth (especially in the media). Historically, income generation was regarded as the true measure of wealth, rather than the market value of one’s assets. (For background, see this article, which some readers may recognize as Chapter 2 of The Income Factory.)

The Income Factory investor thinks of their investment portfolio the way Ford Motor regards its automobile plants. Once a plant is built, Ford doesn’t worry about its resale value. It focuses on how many cars and trucks it produces, and how to continually grow that output. Our Income Factory produces output – a “river of cash” – that we can use to create our own growth through reinvesting and compounding it.

It is hard for many investors to sit through market slumps or bear markets and only collect the 2, 3 or 4% current yields that typical “growth” portfolios pay, while watching market prices fall. An Income Factory strategy, by employing investments and asset classes that pack a full equity return level of 8% to 10% into their cash distribution, makes it psychologically easier for investors to “keep the faith” and NOT feel the urge to get trigger happy and bail out or take defensive actions that might seem like a good idea – at first – but be costly over the long term.

Nobody claims that the Income Factory is a better way to earn an equity return than Dividend Growth Investing, indexing, or traditional growth stocks. Numerous studies show that buying quality stocks and holding them through thick and thin over many decades is the most effective way to achieve investing success. But history also shows many investors do not have the will forces and “nerves of steel” required to buy and hold through market downturns. Those who do, have no need of an Income Factory, since they will do just fine with traditional investing strategies. But for others, an Income Factory may suit their psychological and emotional needs, as well as meet their long-term financial objectives. The most important thing is that investors pick a strategy, and stick with it.

Other Attractive Features of the Income Factory

My other favorite feature of the Income Factory is that it allows, even encourages, what I call “non-heroic” investing. Think about the traditional “dividend growth” stock that pays cash dividends of 3-4% (or less) and has to then grow at 5 or 6% each year to make up the difference for an overall 8-10% growth rate. Since our entire economy is lucky to grow at about 3% per year (even in a non-Covid period), we know most companies can’t be growing at almost twice that rate, unless they are like the children of Prairie Home Companion’s mythical Lake Wobegon, who were all reported to be “above average.”

That means a typical growth investor is expecting all their stocks to have “above average” growth compared to the rest of the economy. Otherwise, why would their stock prices grow any faster than the economy at large? That to me is “heroic” investing, where you are expecting the securities you buy to substantially outperform their competitors and the economy generally. For that to happen, they have to be great companies and you have to be a great stock-picker.

Securities in our Income Factory don’t have to outperform. Most of them are fixed income or “quasi fixed income” in that they represent credit instruments and other securities (high yield bonds, senior secured loans, high yielding utility stocks, REITs, BDCs, MLPs, CLOs, etc.) that are not expected to grow much or at all, and provide most or all of their return in the form of interest or other largely fixed payments. In other words, all they have to do is keep on making the interest and dividend payments they already make. I consider that “non-heroic” investing. If it were a horse race, the heroic investments that expect above-average growth over time are the equivalent of betting on horses to win the race, or at least place or show, meaning they have to excel by doing much better than the average horse in the field. Our Income Factory “horses” only have to stay alive, make it around the track, and finish the race, i.e. stay in business and make the interest and dividend payments they currently do. Which is the safer bet? Betting on specific horses to win, place or show, or betting on the entire field of horses to just finish the race? (See this article for a more detailed discussion.)

Closed-End Funds make great Income Factories

In many ways, closed-end funds may have been designed for an Income Factory strategy. They are great vehicles for holding the sort of less liquid and more complex securities that require an investor to do more work to understand them, and thus generate higher yields. They are “closed end” to begin with, which means, with very rare exceptions, you don’t have the “run on the fund” risk you do with normal mutual funds of market sentiment forcing managers to dispose of healthy assets that may be unpopular at a given time in the market. Beyond that, there are the specific advantages of (1) being able to buy assets at a discount, so you have more assets working for you (earning you income) than you actually paid for; and (2) cheap institutional leverage that allows the fund to partially leverage itself (up to 1/3rd of total assets) at rates or in ways not available to the average investor. The combination of these two factors (discounts and leverage) means that a fund whose assets might normally generate say, 6 or 7% distributions if held directly or in an open-end fund, in a closed-end fund could conceivably generate 8 or 9%, or even higher. This is how holding fixed income securities inside the closed-end fund vehicle can produce long-term “equity returns without equity risks.”

“High Yield” need not mean “High Risk”

One objection sometimes raised concerns the fears that are often attached to the term “high yield.” In the corporate stock world, where normal dividend yields may range from 2% to about 5%, any time a stock’s dividend is yielding above that it is often considered a risky sign. It may mean (1) the market expects the dividend to be cut and has priced the stock in anticipation of that, (2) that the stock is considered to have very little growth prospects and therefore has to make up for it by paying an overly large dividend, or (3) it may reflect an unusual time in the stock markets (like the present, perhaps) where certain stocks or entire segments may be underpriced and/or under-appreciated, and therefore sporting higher than normal yields.

Some investors, aware of these concerns in the corporate stock market, transfer them directly to the credit and fixed income markets, without thinking through the differences. “Fixed income” securities are called that for a reason, namely that all or nearly all of the return their investors get is intended to come from their interest or distribution payments. So it is not at all uncommon for many higher yielding securities, including the common stock in certain industries, to pay distribution yields that would seem high, and be reasons for possible concern, if they were paid out as normal corporate stock dividends.

Mid-caps, small-caps and other “junk”

Another issue worth mentioning because it always comes up, is that many conventional equity investors insist they would never buy “high yield” bonds or other similarly labeled securities because they are supposedly so risky. High yield bonds (also sometimes referred to as “junk” bonds) are merely debt issued by non-investment grade companies, which means the companies are rated BB+ and below. That includes more than half of all companies, so almost all of the companies whose stocks are labeled “mid-cap” and “small cap” are, in fact, non-investment grade companies.

A great many of the same investors who insist so vehemently they would never buy “junk” bonds have portfolios chock full of stock from the same cohort of companies, in their mid-cap and small-cap equity portfolios. Of course the equity of those companies is far riskier than the bonds because it is further down the capital structure and thus junior to the very junk bonds that they insist they would never own. The stock would be worthless if the companies don’t pay off their bonds. (For more info on this topic, check out this article.)

Some possible “machines” for your Income Factory

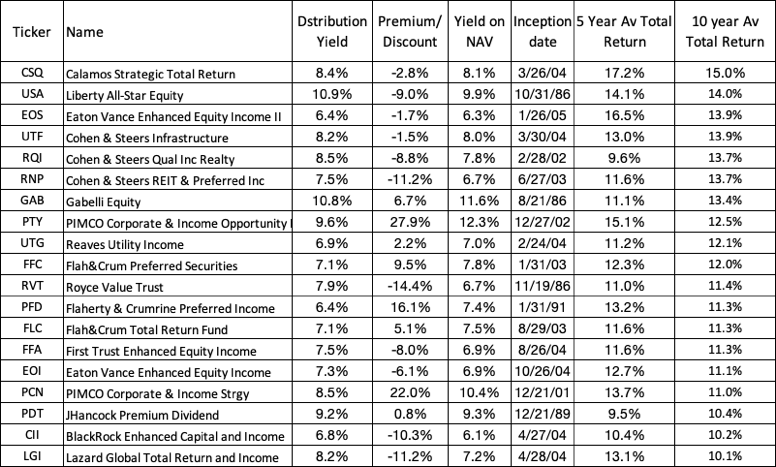

Many investors have the idea that closed-end funds are riskier or lack the “staying power” needed for long-term investing. Closed-end funds, just like stocks, require due diligence, and an Income Factory strategy can go off the rails if it picks the wrong CEFs or other securities just as much as a growth strategy can screw up if it picks the wrong stocks. But there are lots of solid closed-end funds that have provided “equity returns” over many years. Here is a list of candidates that readers may wish to check out as potential productive “machines” for an Income Factory, sorted by 10 year return:

Look forward to your questions and comments.

If you would like a more frequent look “Inside the Income Factory, including:

- Real-time alerts to model portfolios, changes to existing ones, and actionable investment ideas

- Immediate access to all new articles and our library of articles going back ten years

- Direct dialogue and informal feedback

Then please check out Inside the Income Factory. A boutique subscription service whose members get to share ideas and participate in the dialogue and decision-making that goes into our model portfolios and our search for new investment opportunities. If you want to take your Income Factory investing up a notch, please click here to learn more.

Thanks,

Steve Bavaria

Disclosure: I am/we are long UTG, CSQ, USA, UTF, RQI, RNP, FLC, PDT. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.