Although gold prices have recently pulled back from a 6 year high in September, the yellow metal has put together a fairly impressive year. Up over 15% year over year, gold (GLD) has managed to outperform many major stock market indices, and when compared to its own 5 year track record is showing a sustained break to the upside.

Recent news concerning a breakthrough in US-China trade discussions has led some to claim gold’s rally is coming to an end, as global recession concerns are moderated. While this is likely premature by any measure, the indication that a global economy is over the prospects of a recession seem premature if not naïve. The issues plaguing the global economy are more structural in nature and it is difficult to see how the explosion in debt and the excessive use of monetary stimulus would not have long term repercussions, especially considering there have been no major improvements on either front. For a further explanation of the issues, a previous article discusses the topic at length can be found here.

While investors who opted for a direct play on gold are likely pleased with the returns for the year, those who took on a leveraged play through gold miners are likely ecstatic, with many gold indices returning over 30% on the year. While the lot of gold miners have ridden gold’s coat tail higher, a selective group of miners have not shared in the same success, case in point Iamgold (IAG).

Difficulties concerning the company’s costs continued with profits coming in below expectations. A shut down at the Rosebel mine left production below guidance and contributed to the issues surrounding costs. Management’s continued failure to deliver on previous guidance has left many investors unsatisfied with returns given the strong performance of gold. While still posing a strong financial position, Iamgold is showing signs of a classic value trap, with the remainder of 2019 shaping up well for the company, any further misses on guidance could create the case for investors to look elsewhere in hopes of joining a continued gold rally.

Profitability and Cash Flow

Though revenues increased through the third quarter compared to the first half of 2019, they exhibited no definitive trend on a 24 month basis.

Gross Profit (USD millions)

(Source: Iamgold Q3 Report)

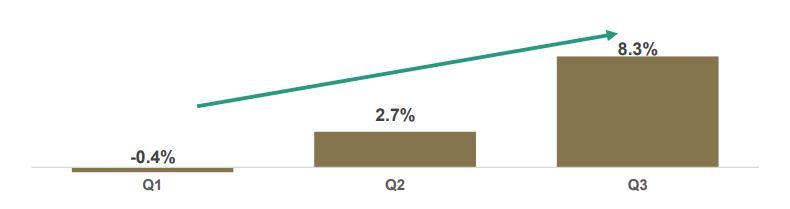

Gross profit margin for the quarter was an improvement from the first half of the year, but coming in at 8% can be considered an underperformance. Net income per share was below expectations coming in at a loss of $0.01, stringing together now what is a consist series of net losses on a quarterly basis.

Gross Profit Margin

(Source: Iamgold Q3 Presentation)

Quarterly Financial Results

(Source: Iamgold Q3 Report)

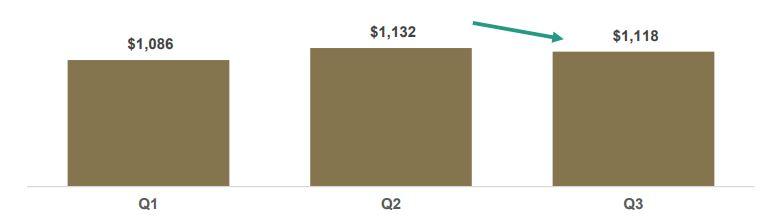

When considering the strong movement in gold prices over the same period, it leaves investors with a number of questions as to the miner’s inability to capitalize on a clearly positive business environment. Persistent issues with cost management were prevalent through the quarter as Iamgold came in above previous guidance on all major measures of cost performance. All in sustaining cost (AISC) for the quarter was $1,118/oz, while the 2019 weighted average AISC is $1,112/oz, 5.97% and 5.45% above the year end 2018 guidance of $1,055/oz respectively.

All In Sustaining Costs

(Source: Iamgold Q3 Presentation)

A major contributing factor to the underperformance in AISC came from the company’s fairly sizable miss on gold production. Since AISC is a per oz metric, a company’s inability to scale back fixed costs will typically lead to an increase in per oz cost when production levels come in below expectations. While Iamgold’s largest mine, Essakane, has come in on target for the year, Westwood and Rosebel have both underperformed, with the later being a central point of the third quarter discussion.

First announced on August 1st, Iamgold issued a press release indicating there had been an incident resulting in the death of an unauthorized miner at the site. Operations at the mine were ceased entirely and a large number of workers were laid off pending further investigation. The mine remained fully closed through the month, only reopening at partial capacity with the northern pits coming back on line to end the August. The Southern pits did not come back online until late September with full operations for the entire site resuming at the start of October. This temporary close had a significant impact on the sites production as 2019 output is expected to be approximately 28% below 2018 year end guidance. (315 – 330 reduced to 240 – 250 thousands of oz)

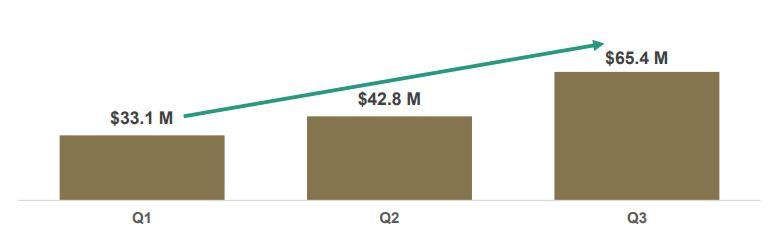

Operating Cash Flow Before Changes to Working Capital

(Source: Iamgold Q3 Presentation)

Cash flow came in stronger than previous quarters mainly attributable to the increase in prices received for gold sales. The company was able to receive an average gold price higher than that of the market, coming in at $1,481/oz vs the market average of $1,472/oz. Although the measure is a positive, the impact overall from a 0.6% increase is minor to the overall cash flow of the business.

Gold Margin

(Source: Iamgold Q3 Report)

While cash flow came in below an ideal level for the company largely driven by the reduced production, the financial position for Iamgold remained relatively strong. $100 million in money market securities had to be liquidated in order to cover the lack of cash flow from operations, but given the company’s strong working capital, the sale did not prove to greatly impact the company’s financial standing.

Iamgold had also previously entered into a forward gold sale agreement with a syndicate of banks, with a promise to sell 150,000 oz by 2022 in exchange for $170 million set to be received in December of this year. This influx of capital should be enough to fully cover any expenditures for the fourth quarter, coming as a positive for investors considering third quarter cash flow failed to meet capital expenditures.

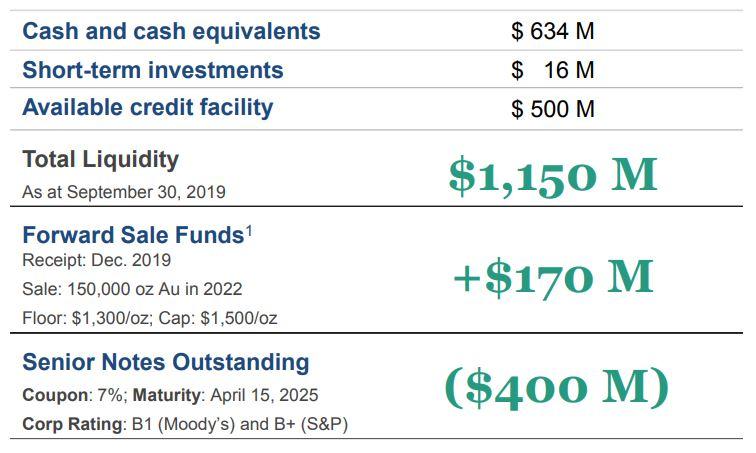

Financial Position

A main factor for investor interest in Iamgold is the company’s sound fiscal position. Although the company has strung together now a number of quarters of underperformance in terms of cash flow and profits, its balance sheet has remained largely intact. Although there has been some deterioration, to date it has not been so significant to cause much concern.

The company’s working capital proved more than adequate to alleviate some concerns of investors. Although it has dropped on a year over year basis, coming in at 4.1 the working capital ratio is still strong on an absolute basis, posing enough current assets to cover approximately 83% of the company’s entire liabilities.

Working Capital Ratio

(Source: Iamgold Q3 Report)

Add to this strong current ratio a $500 million credit facility maturing in 2023, and it is clear Iamgold has a strong liquidity position that should allow the company to capitalize on opportunities that arise.

(Source: Iamgold Q3 Presentation)

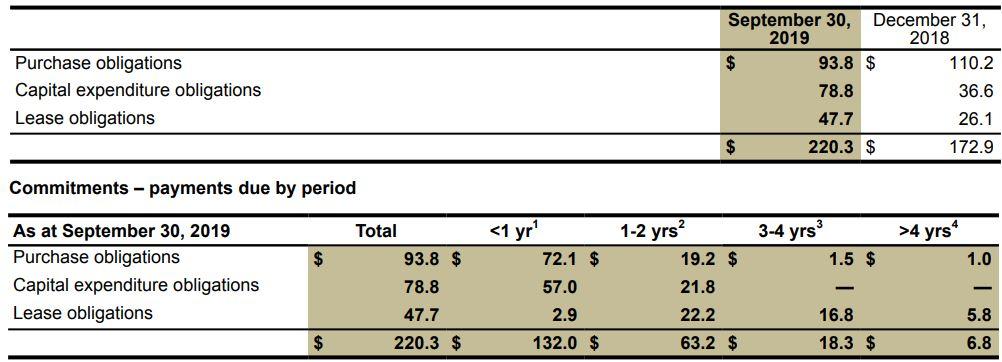

This ample access to capital should prove more than adequate for management to meet its upcoming obligations through the next few years. On a longer term basis the company has $400 million of long term debt currently on its books with a maturity of 2025, leaving no cause for concern within the near term.

Financial Obligations

(Source: Iamgold Q3 Report)

Iamgold’s financial position puts the company in place to take advantage of potential growth opportunities and to manage a less than ideal economic environment. It is a positive for investors to know the company is on a sound financial footing, but management’s ability to leverage a healthy balance sheet and create outsized returns for investors is another story. Herein lays the difficulty for potential investors, ensuring to properly weigh the benefit gained from a strong balance sheet at an attractive price, and taking the necessary steps to avoid underperforming companies and the prospects of a value trap.

Although relatively simple concepts, a value trap can prove far more difficult to identify in practice. Iamgold’s string of quarterly underperformance can definitely leave investors frustrated. The option of being patient and hoping management can begin to unlock the value in this company leaves the potential opportunity cost of missing out on better gains with other gold miners. There is likely nothing worse for an investor than correctly predicting an industry trend yet missing out on the profits due to poor company selection.

The patience of Iamgold shareholders may be running thin, but there is still a logical case to be made for maintaining an investment within the company. The fourth quarter will prove important to see if management can take advantage of a strong business environment that the gold industry hasn’t seen in over 5 years. With a relatively strong pipeline to complement its balance sheet, there is definitely value in this company, whether management can bring this value to shareholders is the real question.

Development Projects and Merger Discussions

With a strong balance sheet in place and an expectation to return to full capacity, Iamgold should be able to put together a strong end to 2019. If gold prices can remain at current levels, or possibly increase, the company should be able to produce a sufficient gold margin generating stronger returns for investors. Higher production levels for mines to have modest ore grade should also allow the company to push down it’s per oz cost, improving key metrics such as AISC.

One positive development discussed on the third quarter earnings call was the first ore delivery from the Saramacca open pit at the Rosebel Gold Mine. The delivery was made possible by the use of an alternate road, as the construction of the main haul road is expected to be completed within the first quarter of 2020.

Although the announcement will not likely have a material impact on the 2019 production, it does pose a positive sign for Iamgold to increase the output for its Rosebel mine and begin producing a better return on the invested capital within the site. With elevated gold prices the ability to get sites producing bodes well for the company and creates some excitement to start 2020.

The more interesting revelation, and the topic investors are likely looking a little closer at, was in regards to the company’s Côté Gold Mine Project. Management has previously exhibited excitement and hope surrounding the project, and for good reason. With an estimated proven and probable reserve of 7.3 million oz, the project could provide strong cash flow for investors. With the site being in Ontario, Canada, it would also help diversify some political risk for the company as the majority of its production currently takes place in countries of higher risk. As some commentary on this thought; with environment concerns being front in center in Canadian politics, it is possible the mining industry in Canada could face pressure from policymakers, driving up costs. Calling into question the exact value of mining land within the country.

Although the project may be of interest, Côté has been largely put on hold for the time being. Management indicated that while they have interest in pursuing the project, key investors have issued concerns with projects that may run up capital expenditures to greatly. For the time being then, the company will continue attempting to de-risk the site with 42% of the detailed project engineering completed to date. Management indicated on the call that decisions to develop further will be made at a later date. They also suggested the possibility of selling a portion or the entire site, although this did not come across as the main objective.

This last line brings up another topic often discussed with Iamgold, the prospects of a buyout. With decent assets and a strong pipeline, sound financial standing, and prospects of greater profitability through improved cost measures; Iamgold does seem to check the boxes for an acquisition target. As we have discussed before and will reiterate here, mergers and acquisitions is a difficult business which requires a great degree of insider know-how. Although one may figure rational thought drives purchases, M&A transactions can often hinge on key relationships between financiers and executives, making it very hard for the average investor to get ahead of potential purchases. We then suggest the majority of individuals leave this out of their analysis and instead welcome it as a nice surprise if it were to come.

With the potential for positive developments moving forward, shareholders of Iamgold do have key objectives that they can measure management’s success against. If production levels continue to come in significantly below capacity it could prove an indication of possible failure to bring future development projects on line. For the analyst, the company’s poor 2019 would suggest applying a discount to a hypothetical fair value in order to accommodate for potential missteps in the future.

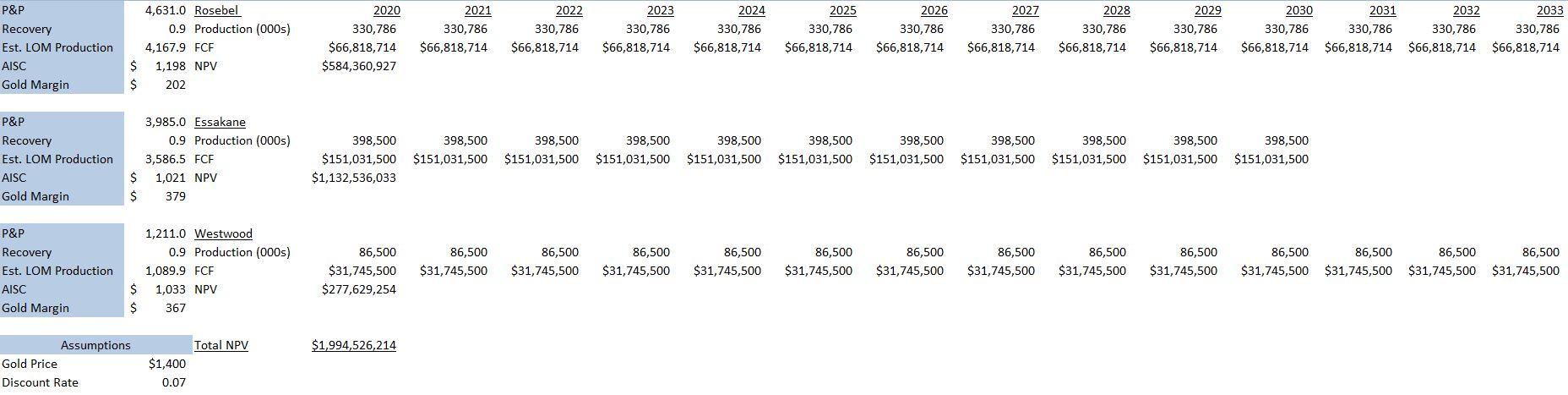

Valuation

Valuing gold miners can be a difficult practice. There are any numbers of issues that can emerge when attempting to bring the mined product to market. Not to mention the highly volatile nature of gold prices over the previous 10 years. Instead of attempting to identify a distinct figure as a fair value, this analysis attempted to determine the lowest probable valuation that one could reasonably attach to Iamgold.

Conducting a Net Present Value (NPV) analysis of the company’s currently operating mines, and taking no development projects into consideration, should provide a value to work with. The calculation assumes the company can retrieve 90% of the proven and probable reserves from Iamgold’s three operating mines: Westwood, Essakane, and Rosebel (including the Saramacca pit). Free cash flow has been calculated by multiplying the hypothetical annual gold production [(reserves * 0.9)/ Life of mine] by an estimate for gold prices and subtracting the 2019 AISC for that site. The net present value calculation assumes a 7% discount rate, which is currently the interest rate on the company’s outstanding notes, and falls within the typical range used of 5% – 10%.

Net Present Value

(Input Data Source: Iamgold Q3 Report)

The calculation produces a hypothetical NPV for Iamgold’s three producing mines of approximately $1.33 billion when gold prices are $1,300/oz, and $2.0 billion when gold prices are $1,400/oz. This calculation is not ideal for determining a true fair value for Iamgold, instead its purpose is to highlight how trading at its current valuation of $1.57 billion is fairly cheap when compared to a hypothetical minimum acceptable value.

Since the calculation does not incorporate any additional reserves, those which are indicated or inferred, and also makes no attempt to factor in any growth for the company’s mine production, it may be safe to conclude Iamgold should trade at a more pronounced premium to this level. Using a basic EV/EBITDA multiple in line with the industry’s 8x would give Iamgold a hypothetical share value of $4.24, or an increase of over 25% from the price at the time of this writing.

Conclusion

Iamgold proves to be a difficult stock to value. While the company has some promising assets, management’s failure to follow through on previous guidance leaves investors skeptical of the firms ability to create value for shareholders moving forward. Assessing the company mainly on a current cash flow basis may not necessarily be the best method. When using a net present value calculation it becomes clear the company could prove profitable for investors if management can produce.

With the fourth quarter shaping up to be promising, investors can use this as a measuring stick to determine whether to remain patient with the company. Many gold mining executives in the past have implicated a lack of capital and underperforming gold prices as reasons for poor stock. But with gold prices posting sustained moves higher and sentiment turning for the industry, now is time for companies to produce.

Iamgold’s shares at current level appear to be undervalued. A good balance sheet with strong pipeline hold hopes of outsized returns to come. A pronounced streak of underperformance by management dimes what could be a bright future for the company. If the company can regain control over its cost and bring them in line with industry competitors the valuation for Iamgold could go higher than the figures previous discussed. It creates a dilemma for investors, as is often the case with stocks possessing traits of a value trap. A wait-and-see approach may be the best strategy for the time being, although time is likely running out.

Author’s Note: If you find this article intriguing and/or useful, please like and leave a comment below. For more articles, be sure to follow my page and subscribe for email alerts.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in IAG over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.