Thesis

Hyliion Holdings Corp. (HYLN) made its debut in the up-and-coming zero-emissions transport industry via SPAC. Presently valued at $4.6B, the venture boasts more vision than numbers to back its capitalization. An over-reliance on parts suppliers, subjectivity in growth assumptions and no defensible order book suggests the company valuation regresses when actual sales & operations data become more discernible. Accordingly, I remain bearish on the short-term prospects of the company.

Introduction

When 28-year-old Thomas Healy buzzed the bell on the NYSE on Monday 5 October, proof showed that he had unquestionably come a long way. A serial entrepreneur whose logbook includes the HeadSmart Labs ALS Ice Bucket challenge and a far-reaching study into Deflate-gate, he is now the kingpin in a cutting-edge powertrain venture with desires of transforming the trucking industry with eco-friendly technology.

Source: HeadSmart Labs “DeflateGate” Study

His corporation, Hyliion Holdings Corp. – a semantic play on Hybrid Lithium Ion – is the purpose of a reverse merger with Tortoise Acquisition Corp. driven by Vincent T. Cubbage. The merger will endow the firm with $560M for upcoming development and commercialization of technologically advanced tractor units.

And who better than Mr. Cubbage to back the deal? After gauging over 200 firms 18 months into the IPO of SHLL, he landed with Hyliion, ostensibly owing to the measure of expertise he can bring to the enterprise having previously closed multiple deals in the fuels marketing, bunkering and hydrocarbon industry.

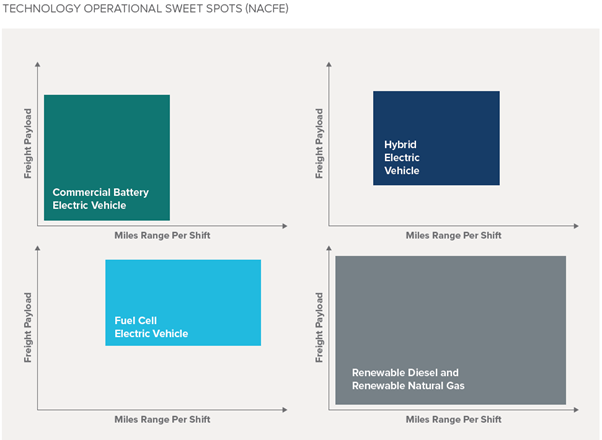

Hyliion Holdings Corp. “engineers, develops, and markets electrified drive train systems that can be installed in Class 8 trucks for most commercial vehicle original equipment manufacturers.” And the beauty of the business is very much here – a solution which is an auxiliary affording haulage companies immediate benefits from a hybrid solution with no requirement to renew its park of vehicles. But the reality is, different backdrops exist to rapidly-changing transport settings. Rick Mihelic, Director, Future Technologies, NACFE summarized it perfectly:

A future, zero emission freight world will only have electric-based vehicles but, in the meantime, we are looking at a multi-fuel reality, with many viable fuels offering opportunities

It would stand that Hyliion’s future flatbed is assured. At least, for the interim.

Source: North American Council for Freight Efficiency – Guidance Report Viable Class 7/8 Electric, Hybrid and Alternative Fuel Tractors

Currently, no one technology has triumphed – renewable diesel & natural gas power trains encompass the full spectrum of freight payloads whereas commercial battery electric vehicles, hybrid vehicles & fuel cell electric vehicles cover more specific ranges. These technological sweet spots are well documented by the North American Council for Freight Efficiency.

Source: North American Council for Freight Efficiency – Guidance Report Viable Class 7/8 Electric, Hybrid and Alternative Fuel Tractors

The technological battle for the gold standard in ecologically-friendly powertrains has yet to be played out. Each technology has dissimilar traits, benefits, and drawbacks. Presently, the “after market auxiliary” solution featured by Hyliion has the advantage of versatility, but the market itself presents risk, as the dust has not settled on adoption of a future standard by all stakeholders.

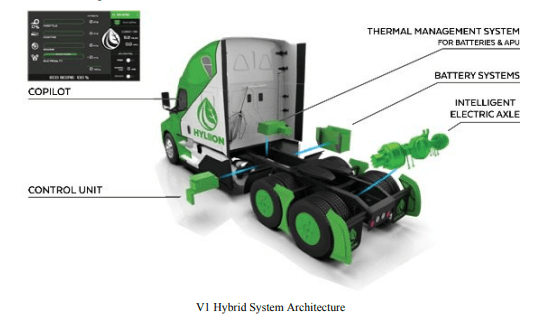

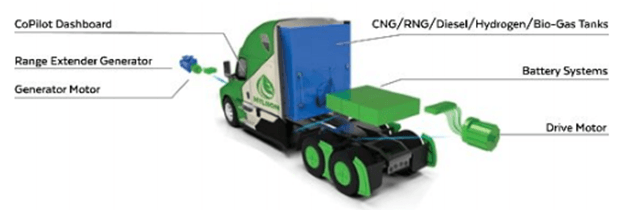

The Cedar Park, Texas-based firm exceedingly publicizes itself as a leading technology platform for the future motorization of tractors with a dual offering – an immediately available V1 Hybrid aftermarket pitch, encompassing Hyliion’s proprietary battery systems matched with a software management package, control module, data analytics, power distribution & thermal management. The data management & analytics systems whose value is incremental has been tested over 2 million miles thus far. This may seem material but merits perspective, over the past 4 years, Tesla (TSLA) has tested close to 3 billion miles with its data analytics & AI package.

The platform does have advantages nonetheless – an instant plug & play solution, an addressable market tantamount to the entire fleet of class 7/8 heavy-duty tractors and an opportunity to build adoption rates among fleet managers unwilling to commit to a technology with the full renewal of their asset bases. It may be the bridge formula to success – at least at initiation.

Source: Proxy Statement Tortoise Acquisition Corp

Source: Proxy Statement Tortoise Acquisition Corp

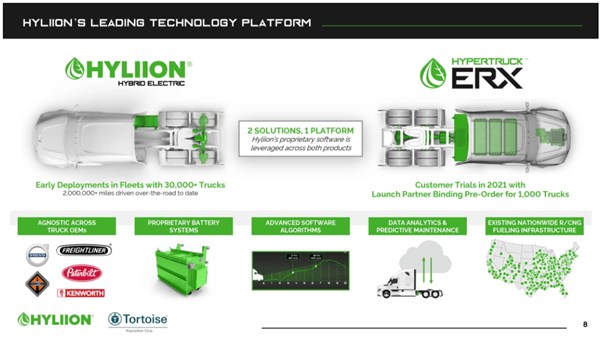

Arguably, a more troubling feature of the Hyliion value proposition relates to its Hypertruck ERX. The system differs from the hybrid aftermarket formula. Its fully electric drivetrain capitalizes on the hybrid system which, when combined with a customer’s primary source of energy, offers a net carbon-negative solution for Class 8 commercial vehicles. This bears resemblance to a middle-of-the-road approach from a firm reluctant to commit to any one given technology.

The organization intends on trialing in 2021 with a binding pre-order for 1,000 units. While providing flexibility to customers, the real long-term gains seem uncertain. If it were in fact such a competitively positioned pitch, questions arise about the competition. Why would this not already be developed by large drivetrain and powertrain parts suppliers? Did Dana (DAN), Ricardo and ThyssenKrupp (OTCPK:TYEKF) essentially miss something? Possibly…

Source: Proxy Statement Tortoise Acquisition Corp

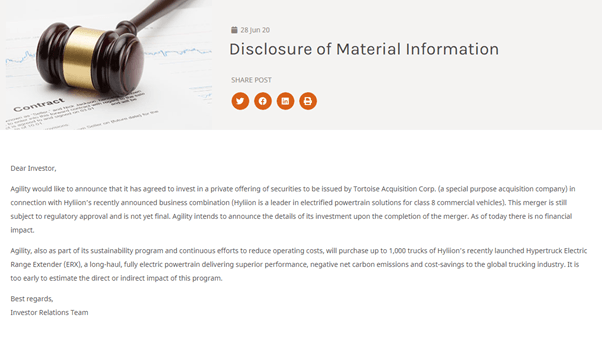

The pre-order for 1,000 units while material is ambiguous. The pioneer customer will be Agility Logistics USA – the Kuwaiti-owned global logistics firm more focused on airfreight than trucking. More importantly, Agility is an equity partner in Hyliion Holdings Corp. Therefore, the pre-order really should be regarded more as an inter-company transfer than a manifestation of Hyliion’s ability to bring the product to market. Agility’s carbon emissions for its trucking division are minimal compared to both air and sea freight divisions. So, another question must be asked as to the purpose of Agility’s investment – is it fundamentally used to change its carbon footprint or is this more about selling a narrative to the public?

Source: Agility Financial Filings – Disclosure of Material Information

Source: Hyliion Holdings Corp Investor presentation

The company has opted to outsource a noteworthy amount of its core business, including:

- Design & Engineering -> IAV Automotive Engineering & FEV

- Batteries -> Toshiba (OTCPK:TOSBF)

- E-drive components -> Dana

- Truck Modification Centres -> Fontaine Modification & SV Lonestar Electric

- OEM assembly line install of Hyliion system -> Freightliner, Kenworth, Volvo, International & Peterbilt

In essence, the venture, which disposes of a range of proprietary patents and technologies, is marketing a hybrid plug and play solution while outsourcing large chunks of its business with multiple firms throughout the value chain. This harbors reservations about barriers to entry, products of substitution or even long-term technological viability. Why wouldn’t original equipment manufacturers be designing & installing proprietary systems? The technological & operational moats seem virtually void.

Dana provides drivetrain, axle, and electrified propulsion components for Hyliion Holdings Corp. It has received $10M worth of Hyliion Convertible notes in exchange for sharing of engineering expertise & technologies. Hyliion has an obligation to purchase from Dana powertrain components – echoing the deal between General Motors (GM) and Nikola (NKLA). Dana has an ownership stake, exclusively selling its products to the company in exchange for its expertise, and possibly allowing the drive train stalwart to test the water for product success in a very cost-effective manner.

Source: Proxy Statement Tortoise Acquisition Corp.

Source: Hyliion Holdings Corp. Investor presentation

Source: Hyliion Holdings Corp. Investor presentation

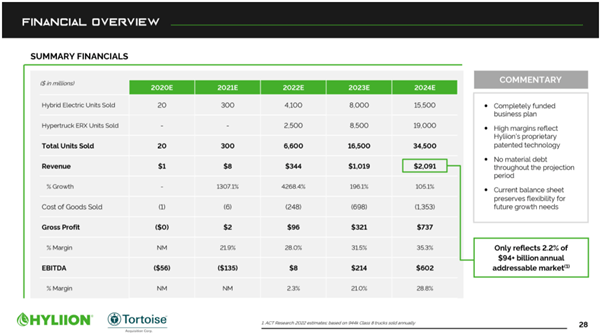

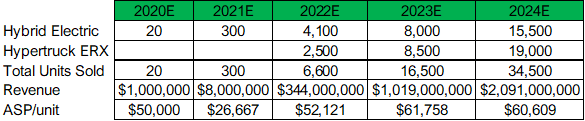

Hyliion Hybrid MSRP is published at $29,000 per unit (page 20 investor presentation) contributing $580,000 in total revenues. It does not throw light on the additional $420,000 of revenues generated to meet summary financials in 2020E. Granted this is a ballpark figure but would require a doubling of the retail price to hit guidance.

Source: created by author with information provided in Hyliion Holdings Corp. Investor presentation

Estimated average selling price per unit remains consistent and would signal the enterprise can perpetuate prices in an environment which will assuredly run into increasing attention from competition. This combined with a strategy which outsources substantial amounts of inputs seems inconsistent. Tesla has previously argued for the intangible merits of big data as being a key part of valuation – this too has earmarks of pre-maturity for an organization like Hyliion which solely proclaims 2 million tested miles.

The alternative fuels market will unequivocally have positive bearing for trade. Covid-19 has induced changes in consumer preferences towards home delivery, a market segment which is promising for organizations like Hyliion. These changes will mutate the logistics industry and present an irrefutable growth opportunity.

But the figures, the fine points brandished to investors and the middle-of-the-road blueprint may lack ambition.

Conclusion

- Hyliion’s pivotal customer has an equity interest in the firm. Thus far, this gives no real verdict of the product line commercial viability.

- Hyliion’s supply chain game plan relies on a myriad of technological partnerships, commercial agreements, and reliance on third parties; it makes barriers to entry quasi unsubstantial in a market which will solicit interest from several players.

- Hyliion’s product narrative – while providing prompt advantages such as retrofit options to fleets may not be daring enough – a wait-and-see strategy to find out which technology ultimately has an upper hand may force Hyliion to primarily follow rather than pioneer.

- Hyliion’s numbers seem to raise questions – are growth rates broadcast realistic? Are pricing mechanics sustainable? Can exponential growth be managed with a supply chain strategy which contracts out a large part of the activity for equity stakes or other fringe benefits.

The complexity in a pioneer market is being able to bet on the right horse, er… truck. In the absence of real tangible data, in the presence of ambiguity on which technology to commit to, and facing dependence on a growing supply chain, I remain bearish on the venture.

A company valued at $4.6B with no real sales, which has “neither engaged in any significant operations nor generated any operating revenues to date” a playbook which heavily relies on established original equipment manufacturers and touts growth numbers which are hard to fully justify makes for a risky investment. It also leaves me wondering how the company would have fared had they chosen to pitch these numbers to institutional investors and follow the traditional IPO route. Only time will tell.

One thing which we can factually take away is – with 34,972,856 shares presently valued at $1,039,743,009 Hyliion to date has been a success for its founder Thomas Healy. Let us hope with his vision, experience, and leadership drive, that he can turn it into a success for investors in the future.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.