Andrii Yalanskyi/iStock via Getty Images

Introduction

On September 3, 2021, I wrote my first article covering GXO Logistics (NYSE:GXO), the spin-off from logistics giant XPO Logistics (XPO). I discussed the company’s exceptional business model in a rapidly evolving logistics/supply chain environment, its high growth rate, and its attractive valuation. Fast-forward to May 2022 and the call is 30% underwater. Was I wrong? Was I early?

I’m sure I am not wrong about the long-term ability of GXO to generate tremendous value for its shareholders and customers. The problem GXO shareholders encountered is that the market is currently selling off. Investors are selling everything to gain liquidity, which includes some of the hottest stocks in the market (easier to take profit to cover other losses) and so-called “growth” stocks. Most of the hottest 2020/2021 stocks are down more than 70% as loss-making growth stocks are getting punished by higher rates and the unwillingness of investors to buy companies that make no money.

That’s where GXO comes in. The stock is definitely a growth stock. Yet, it is profitable, generates high free cash flow, and is now trading at a “value” valuation. It’s a typical case of a situation where the market is overreacting, throwing the baby out with the bathwater.

In this article, I will update my bull case and explain why this weakness is a blessing instead of a curse.

Yet Another Selloff

The S&P 500 is currently roughly 14% below its all-time high. It’s one of the most severe sell-offs we witnessed in the past ten years. Yet, it’s far from spectacular. In general, the market tends to fall 10% every year.

While it’s hard to call a bottom, one thing is for sure, and that’s the fact that for some people this sell-off feels much worse than it actually is. The tech-heavy ETF (QQQ) is currently down more than 23%, which is technically a bear market. In other words, investors who piled into tech and growth stocks are in a much worse place than “the market” might suggest.

Hence, in “hot” industries, we’re seeing a lot of damage as investors have sold even their strongest positions to free up cash. One of these industries is Industry 4.0 logistics. If there’s one part of global supply chains that benefited from the pandemic, it’s the seamless integration of producers, buyers, sellers, and storage facilities through automated warehousing.

GXO, An Advanced Industry 4.0 Player

As I explained in my last article, Industry 4.0 is a very broad term that applies to multiple areas of global supply chains:

One of the most important things that investors will have to take into account is Industry 4.0. Basically, Industry 4.0 is a broad definition of the new wave of technological advancements that provide us with a well-connected supply chain. It technically applies to industrial practices but can be used in a broader context. This includes a wide variety of breakthrough technologies like cloud computing to handle data, artificial intelligence, big data, the internet of things, and automation. This new industrial revolution was ‘invented’ in Germany. The country, which is known for its automotive industry, has implemented it by more or less focusing on streamlining the automotive supply chain. This includes keeping inventories low by only ordering what is needed and completely relying on automated processes.

Spectral Engines (Nynomic Group)

GXO is a great way to get serious targeted exposure in this area without having to buy either very small startups or big players that do have exposure in the area but make most of their money in other areas – the 2021 spin-off from XPO made that possible.

Since the spin-off, the company is the largest pure-play contract logistics provider in the world. The company provides customers with high-value add warehousing and distribution, order fulfillment, e-commerce, reverse logistics and other supply chain services differentiated by its technology-enabled solutions.

This is how the company puts it:

Our revenue is diversified among hundreds of customers, including many multinational corporations, across numerous verticals. Our customers rely on us to move their goods with high efficiency through their supply chains — from the moment inbound goods arrive at our logistics sites, through fulfillment and distribution, and the management of returned products. Our customer base includes many blue-chip leaders in sectors that demonstrate high growth and/or durable demand, with significant growth potential through customer outsourcing of logistics services.

In other words, it’s the perfect company to support customers in an industry that demands efficient logistics to stay competitive. After all, retail competition is fierce and any automation reduces long-term costs. Outsourcing also allows customers to focus on what they are good at like producing products, marketing, and whatnot, without having to deal with advanced logistics.

Hence, headlines like the one below are now popping up at an increasing pace:

Wall Street Journal

I don’t want to focus too much on this story as this article is about GXO, but essentially, Shopify (SHOP) is working to improve its entire supply chain:

The acquisition will help Shopify “accelerate its roadmap by assembling an end-to-end logistics platform that manages inventory from port to porch and across all sales channels,” Shopify Chief Financial Officer Amy Shapero said in an investor earnings call Thursday.

In light of Industry 4.0, GXO is exactly what customers need as it has intelligence warehouse automation:

Our intelligent warehouse automation includes deployments of autonomous robots and cobots, automated sortation systems, automated guided vehicles, goods-to-person systems and wearable smart devices — these are all effective ways to deliver critical improvements in speed, accuracy and productivity. Importantly, automation also enhances safety and the overall quality of employment. Our warehouse management system creates a synchronized environment across automation platforms to control these technologies holistically, providing an integrated solution.

Moreover, and this is even more fascinating, the company allows customers to be prepared for higher (or lower) demand periods by applying predictive analytics.

Our predictive analytics add significant value for customers, particularly in e-commerce and omnichannel retail, where seasonality drives high volumes through outbound and inbound logistics processes. For example, up to 30% of consumer goods bought online are returned and this creates increased volumes at certain times of the year. We have developed analytics that predict surges in demand using a combination of historical data and customer forecasting.

As of December 31, 2021, the company has 906 properties. Most of them are in the United States (316) followed by the United Kingdom (257) and Europe (252). 538 properties are leased. 361 are customer-owned facilities. GXO owns 7 facilities.

As good as everything above sounds, it gets better as GXO is not a startup, nor is it a company that doesn’t make money. It’s a profitable corporation that brings a lot of value to the table.

There’s Significant Value In GXO

On May 4, the company released its 1Q22 earnings. The company generated $2.1 billion in revenue, which is $40 million more than analysts expected. Non-GAAP EPS came in at $0.59, which is $0.08 above consensus estimates.

It gets better, though. The company had 19% organic revenue growth, which is the fifth consecutive quarter of double-digit organic growth. The company won over $1 billion of new FY2022 revenue through the quarter. That’s equivalent to 13% year-on-year revenue growth.

Some of the company’s new customers include Zalando, Carrefour, Decathlon, iRobot, and Raytheon (RTX). Companies like Raytheon aren’t focused on customers, but even industrial firms need flawless supply chains to i.e., lower inventory costs.

The company now has a 1Q sales pipeline of $2.5 billion. That’s 20% year-on-year growth. Moreover, despite economic challenges (in general, not company-specific), management upgraded FY2022 organic revenue growth expectations from 8-12% to 11-15%, that’s a big deal.

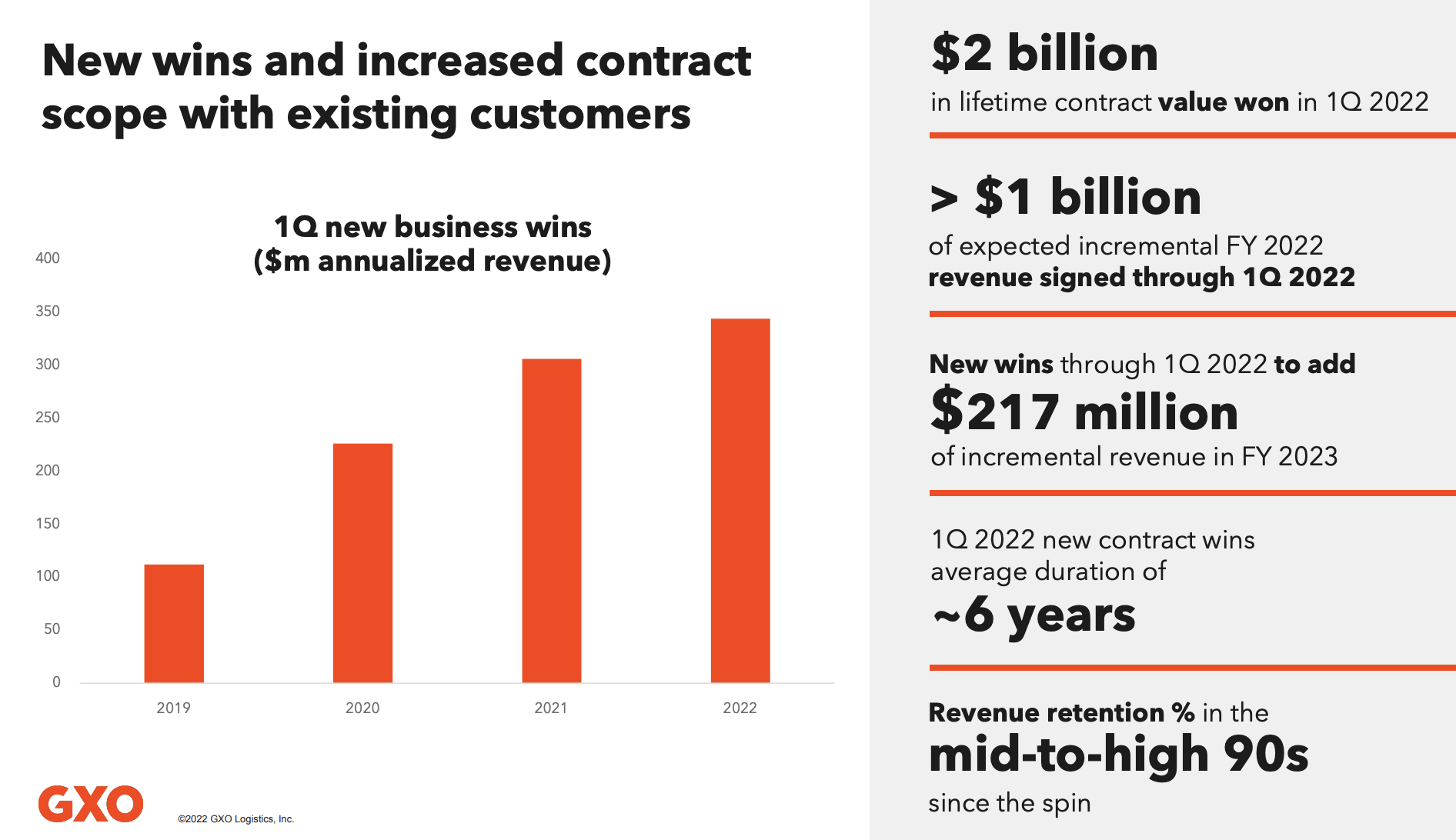

Even better, new orders are accelerating. The chart on the left side of the slide below shows new business wins in the first quarter on an annualized revenue basis. In 2019, that number was above $100 million. In 1Q22, it was close to $350 million. The average duration of these contract wins was 6% with revenue retention (%) in the mid-to-high 90s range. This matters because customers enjoy their experience with GXO as almost all of them come back – or stay with the company.

GXO Logistics, Inc

This is important because peers aren’t asleep. The company is competing with some big names in the industry:

Our competitors include local, regional, national and international companies that offer services similar to those we provide. Our competitors include Clipper Logistics, DHL, DSV Panalpina, Kuehne + Nagel, Geodis and ID Logistics.

The company sees that supply chains are becoming far more complex, which means the requirement for innovation (and scale) is becoming greater as I already mentioned. As a result, 44% of new business wins in 1Q22 were from companies that just started to outsource (first time outsourcing). 17% of wins were customers that worked with a GXO competitor in the past.

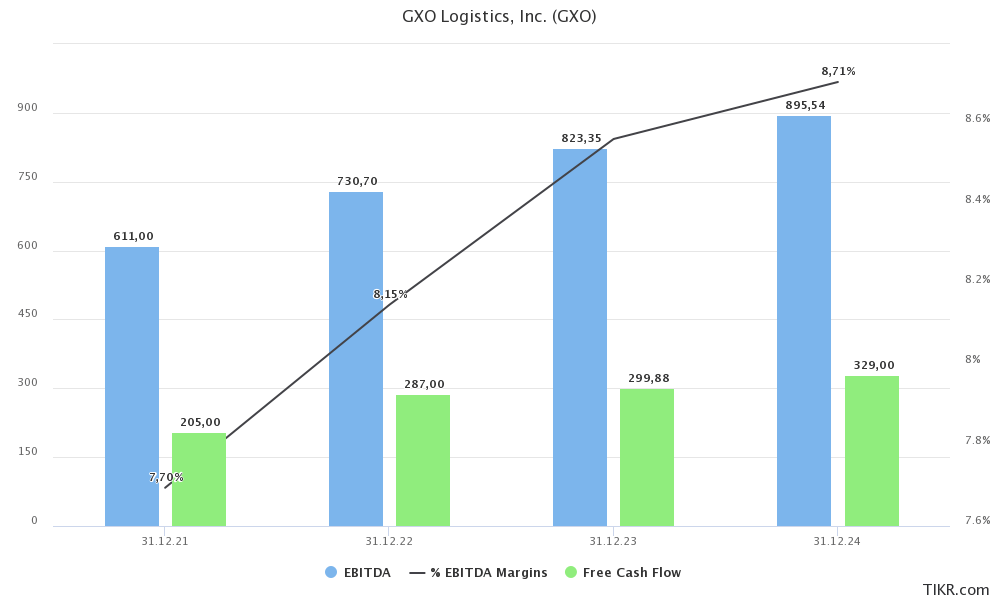

With that said, the company’s long-term expectations are phenomenal. As I already mentioned, GXO isn’t a start-up but a company that generates a lot of value. This year, we’re looking at $730 million in expected EBITDA with an expected surge to $823 million in 2023. In other words, EBITDA growth is expected to remain close to 10% with EBITDA margins working their way up to the 9% range in the years ahead.

TIKR.com

On top of that, the business is generating high free cash flow. Free cash flow is operating cash flow minus capital expenditures. It’s cash a company can spend on dividends, buybacks, or boost the cash position (reduce debt). Next year, the company could breach the $300 million FCF mark, which translates to an implied free cash flow yield of 4.4% using its $6.8 billion market cap.

As the company does not pay a dividend or repurchase shares, it is boosting its balance sheet. Next year, the company is expected to lower its net financial debt to $1.3 billion. Net debt is gross debt minus cash. In the year after, net debt is expected to soar due to higher investments (to $1.5 billion). Even then, the net leverage ratio is below 1.8x EBITDA, which is very healthy.

Last year, the company bought the majority of Kuehne + Nagel’s contract logistics operations in the UK, which generated $604 million in additional value. I have little doubt that this stellar balance sheet will be used to generate strong acquired growth in a rapidly developing market.

Valuation

The valuation is way too cheap. Using the company’s $6.8 billion market cap and $1.5 billion in expected 2024 net debt (to account for higher expected net debt) gives us an enterprise value of $8.3 billion. This includes an almost neglectable minority interest of $34 million.

This enterprise value is roughly 10x expected 2023 EBITDA.

It’s a bit useless to use the company’s short valuation history, but either way, paying 10x 2023 EBITDA is not a valuation that makes sense, as it’s too cheap. Even if economic growth deteriorates further, I don’t see a scenario where things get so bad that investments in supply chains are canceled. Delayed maybe, but not canceled. Also, as I already said, an implied free cash flow yield of 4.4% is a great deal. It’s similar to the free cash flow of some of the dividend growth stocks that I own. It once again underlines that GXO offers both growth and value.

Based on this valuation, the stock should trade at least at its all-time high. In the introduction, I made the case that it’s a case of “throwing the baby out with the bathwater”. This happens during almost all market downturns. Investors de-risk their portfolios, selling their most successful investments to free up cash. The good thing is that some companies generate value (i.e., free cash flow), which makes it easier to assess the situation. GXO is trading like a value stock with slow mid-single-digit annual EBITDA growth. That’s not the case as secular growth is way too high in the industry. And, as I said, even if investments by customers are delayed due to uncertainty, the valuation makes sense. It comes with a rather high margin of safety.

Takeaway

GXO is down almost 34% year-to-date. That’s a terrible return and it doesn’t make my 2021 bull thesis look good. However, I’m even less worried about the company’s risks now than I was last year. The company is showing how well its business model works by winning big contracts and proving that competition isn’t a problem. While the market is selling off due to economic growth worries fueled by a hawkish Fed, GXO raised full-year sales growth guidance. The company is one of the biggest beneficiaries of the Industry 4.0 trend in logistics and it offers a great mix of growth and value. Not only is EBITDA expected to grow by double digits, but investors are also paying close to 10x 2023 EBITDA and benefiting from a 4.4% implied free cash flow yield.

FINVIZ

Going forward, I expect the company to keep winning big contracts. Higher free cash flow will be used to acquire growth.

While I cannot say that the stock won’t fall any lower, I am not worried. The stock will bounce back eventually. On March 2. Stifel gave the stock a $94 price target. I believe that’s conservative. The stock has much more room to rise. The problem is getting there. I have zero doubt that when confidence returns to the market, buyers will rush for stocks like GXO. Even if you don’t buy now, having GXO on your watchlist can come with huge benefits.

(Dis)agree? Let me know in the comments!