xavierarnau/E+ via Getty Images

GXO Logistics’ (GXO) stock has been pummeled in recent weeks, which strikes me as unjustified coming on the heels of a potential cash and stock acquisition of Clipper Logistics (OTCPK:CLPLF) worth 920p/share or $1.3bn in equity value. Strategically, Clipper should augment the already robust GXO e-commerce portfolio nicely, while a preliminary analysis also indicates a strongly accretive deal outcome. Assuming no regulatory hurdles, the odds of a deal getting finalized is also strong, in my view – GXO has irrevocable commitments from Clipper’s key management (Chairman, CEO, and CFO), which should prove binding in the event of a competing offer. Overall, the e-commerce logistics tailwind is just getting started, and with the discount widening relative to forwarder peers like DSV (OTCPK:DSDVF) amid a supportive freight backdrop, GXO offers good relative value here.

| Fwd EV/EBITDA | |

| GXO | 10.7x |

| DSV | 13.1x |

Source: MarketScreener

The Announced Deal Terms

GXO issued a press release outlining an agreement on key terms for the acquisition of Clipper Logistics, a pure-play contract logistics provider focused on the UK region. The current offer implies a £0.95bn enterprise valuation (after incorporating ~£11mn of Clipper net debt), comprising 75% cash and 25% in new GXO shares. While the equity dilution is a slight negative, the offer price of 920p represents a reasonable ~18% premium to Clipper’s pre-deal closing price on February 18. Using Clipper’s reported FY21 financials of £696m of revenue and £43m of EBITDA, the implied deal multiple comes to ~22x FY22 EV/EBITDA pre-synergies – a premium to where GXO trades (~16x EV/EBITDA pre-announcement).

The valuation seems pricey as a starting point, but synergies will be key to making this deal work. GXO’s strong track record on post-M&A integration helps – since closing the Kuehne + Nagel (K+N) acquisition in 2021 (pre-XPO Logistics (XPO) spinoff), management has successfully generated ~5% of run-rate synergies (as a % of revenue) from procurement and operational overlap (relevant quote from the Q4 2021 transcript below):

“We were able to extract $30 million of synergies, roughly 5% of its target sales in a very difficult year, and we have more benefits that will accrue in 2022.”

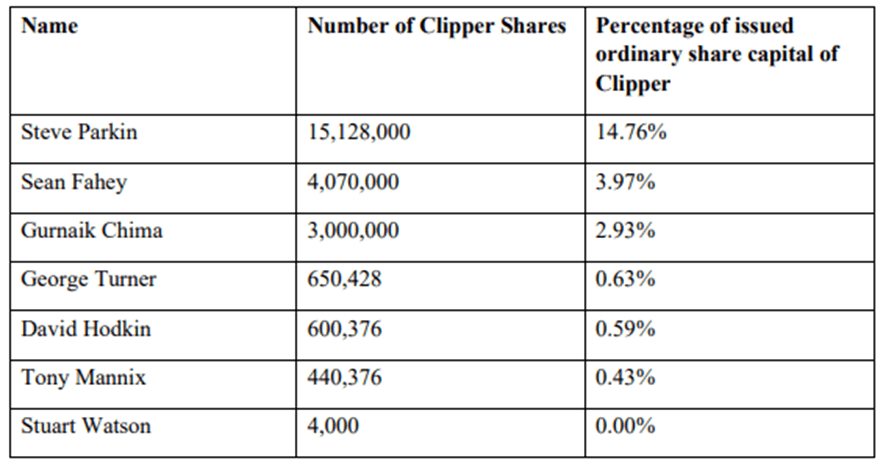

Conservatively assuming half of this for Clipper still brings the multiple down to a post-synergy 14-15x FY22 EV/EBITDA, below where GXO was trading pre-announcement. As 75% of the transaction will be funded by debt, post-deal leverage should rise closer to ~2x, but should not threaten its investment-grade rating. The timing of a deal close is undisclosed for now but given GXO has received irrevocable undertakings from key management (Chairman, CEO, CFO) representing ~23% of the shares outstanding, interests are aligned, and thus, I think investors can have reasonable certainty of a positive outcome.

GXO

Source: GXO Statement (Rule 2.7 Announcement)

Early Innings of an Expansion

The transaction fits nicely within GXO’s broader plan to augment its organic growth potential with a quality asset exposed to fast-growing end markets in the complementary UK and European geographies. A key advantage here is that Clipper derives ~93% of its revenue within UK logistics from open book or minimum volume guarantee contracts, with a focus on the e-fulfillment and returns management areas. Given the limited customer overlap with GXO’s core base, this should expand the potential opportunity for cost synergies to be unlocked. In addition to the cost side, GXO also has the option to unlock revenue synergies via a broader customer base, diversifying into the life sciences vertical, and expanding into new markets like Germany and Poland.

As the balance sheet remains strong post-deal, GXO’s previous target of completing one or two tuck-in acquisitions per year is intact. Even with the consolidation environment picking up, led by Maersk’s purchase of Visible SCM, Pilot Freight, and LF Logistics, the acquisition of Clipper demonstrates there is still room to pick up quality assets at a reasonable price. Clipper, for instance, generates strong returns on capital (~30% ROIC vs ~28% for GXO) while sustaining overall revenue growth in the high-teens % CAGR (mainly e-fulfillment with returns management growth running at >30%). As long as rates remain elevated and capacity remains constrained across freight transportation, I think GXO is well-positioned to execute on its growth-driven M&A plans.

Preliminary Numbers Signal an EPS Accretive Scenario

GXO didn’t quantify the potential cost synergies in its press release, although management did note it would be “significant.” While GXO did extract ~5% of revenue in synergies from the K+N deal, I would model a more conservative 2.5% of the target’s LTM revenue synergy scenario as a starting point in the accretion analysis. Assuming a ~2% cost on new debt (in line with GXO’s latest issuance), this gets me to 4.5% pro-forma EBITDA margins and ~7% EPS accretion (post-dilution). Given the pro-forma margin profile is below industry leader DHL’s (OTCPK:DPSGY) ~5%, I think a higher outcome is very much possible, particularly given Clipper’s higher e-commerce exposure.

|

USD ‘m |

GXO (FY22E) |

Clipper (LTM) |

Synergies @ 2.5% Rev |

Funding |

Pro-Forma |

|

Revenue |

8,905 |

909 |

9,814 |

||

|

EBIT |

380 |

39 |

23 |

442 |

|

|

EBIT Margin (%) |

4.3% |

4.3% |

4.5% |

||

|

Interest Expense @ 2% |

20 |

4 |

19 |

43 |

|

|

EPS Accretion Post-Dilution (%) |

7% |

Source: Author

Gearing Up for M&A-Driven Growth

The GXO/Clipper announcement is another positive development in a broader consolidation within logistics for the last year, coming on the back of recent discussions of a DSV/Schenker merger. I like where GXO is going with this deal – the limited customer overlap should present management with synergy opportunities, while the complementary industry verticals and operational levers should drive a favorable long-term outcome. The price discipline and accretion are also key positives, and while another bidder is possible, the irrevocable commitments from Clipper’s key management (and shareholders) signal intent. Thinking long-term, the stock looks good here – GXO stands to benefit from a secular e-commerce logistics tailwind, yet its relative discount to its EU-based forwarder peer DSV makes this a good relative value play.