bfk92/E+ via Getty Images

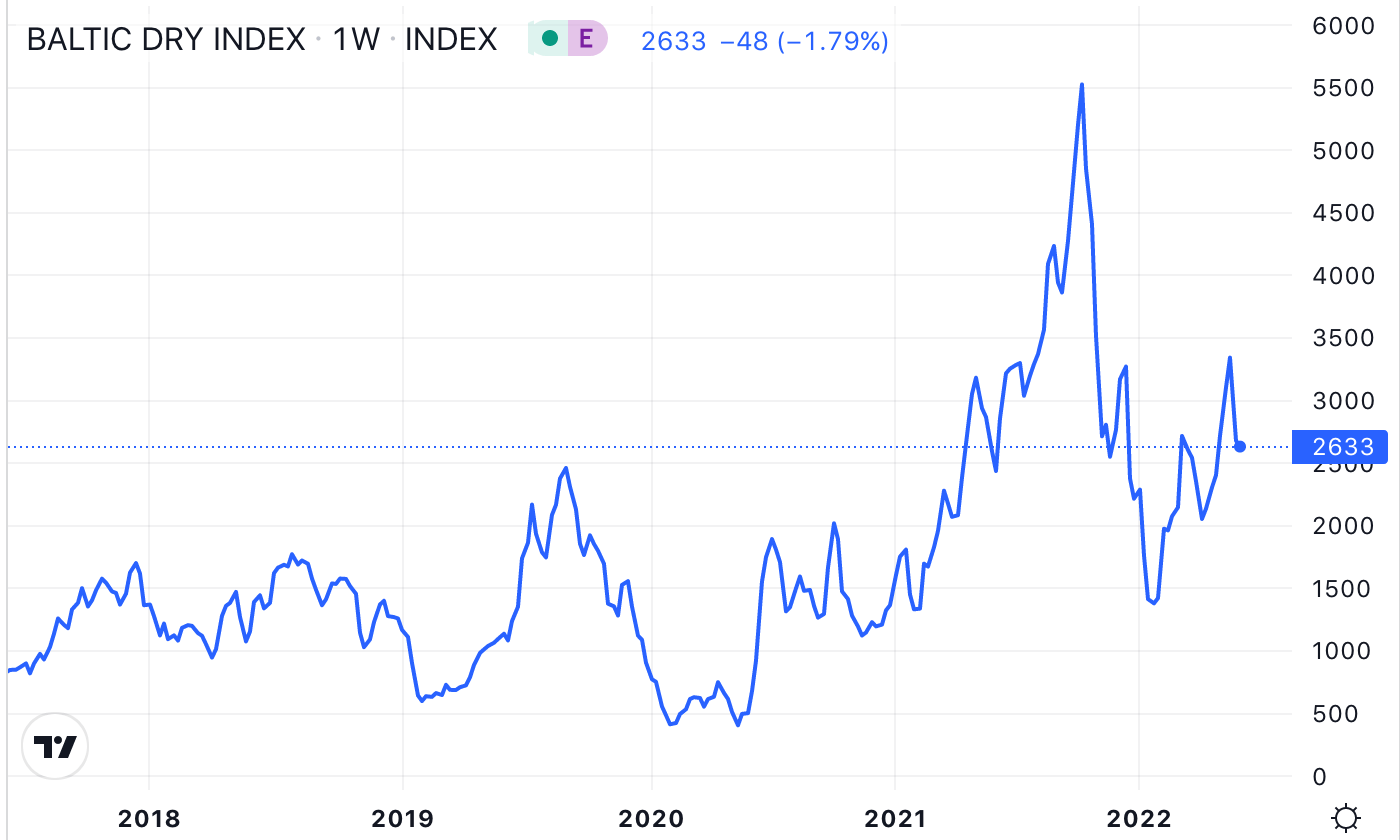

Looking to profit from the global supply chain logjam? The volatile Baltic Dry Index, which measures the relationship between the supply of large super bulk cargo ships (across 3 different sizes), and the market demand to utilize the ships and their trade routes, has been on a tear since 2021.

It topped out at ~5650 in October 2021, and was at 2633 as of 6/2/22:

tradinggeconomics

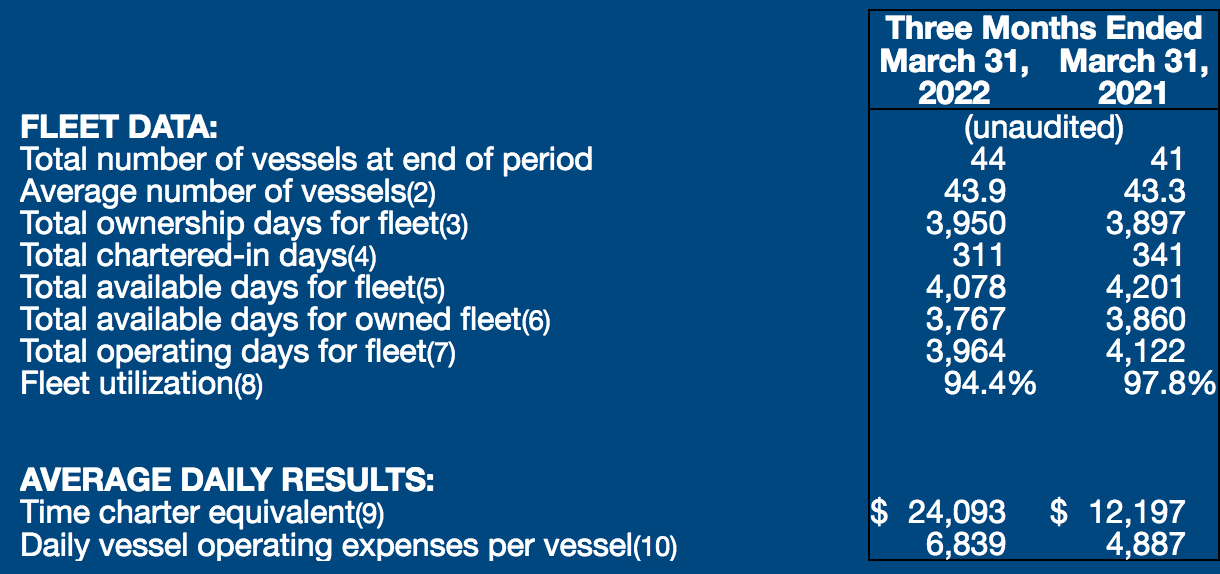

Those higher index values have greatly benefited bulk cargo shipping companies, such as Genco Shipping (NYSE:GNK), which has seen its Time Charter Equivalent, TCE, rates ramp up considerably since early 2021.

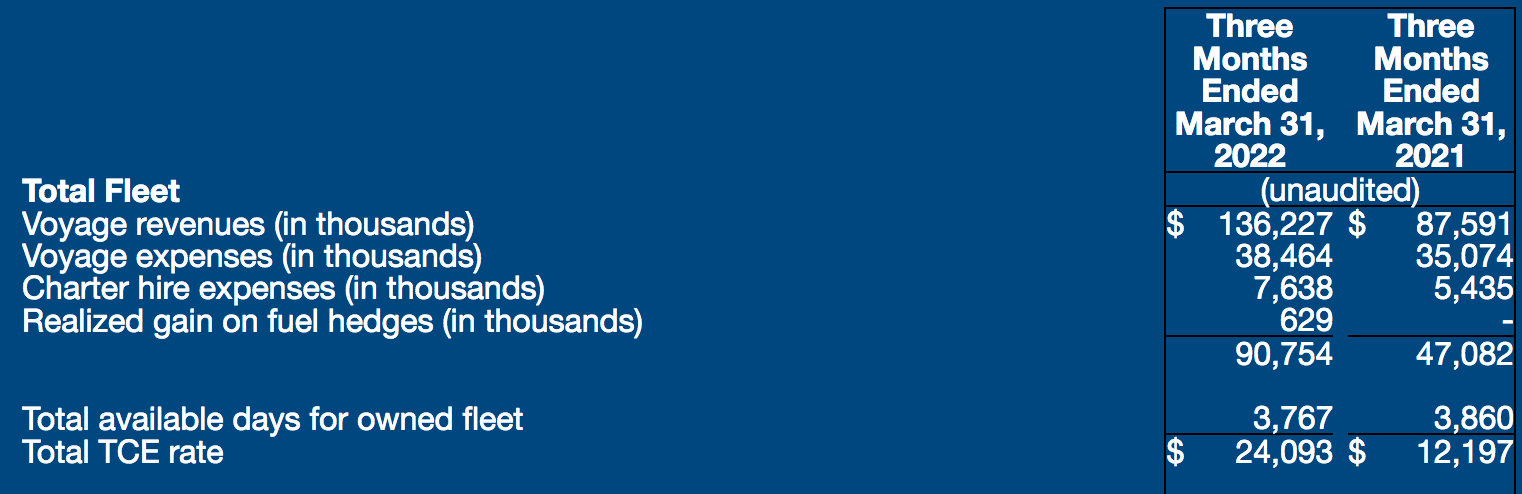

GNK’s average daily fleet-wide time charter equivalent, or TCE, for Q1 2022 was $24,093, 98% higher YOY and its highest first quarter TCE since 2010.

Those high rates didn’t slow down for GNK in April ’22 either, staying in the same high area. Management “estimates our TCE to date for Q2 2022 to be $27,596 for 68% of our owned fleet available days, based on both period and current spot fixtures.”

GNK site

Profile:

Genco Shipping & Trading Limited is an international ship owning company. We transport iron ore, coal, grain, steel products and other dry bulk cargoes along worldwide shipping routes. Our wholly owned modern fleet of dry cargo vessels consists of Capesize, Ultramax and Supramax vessels that provide an essential link in international trade.

GNK’s fleet consisted of 44 vessels, as of 3/31/22, with the delivery of the Genco Mary and the Genco Laddey, two high quality, fuel-efficient Ultramax vessels built in 2022 at Dalian Cosco KHI Ship Engineering.

Fleet utilization was 94.4% in Q1 ’22, indicating the ongoing high demand for these vessels. Russia’s invasion of Ukraine has led to higher commodity prices and a re-directing of cargo flows, especially for grains and energy, which has ramped up ton-mile demand. Additionally, higher fuel prices have led to a slowdown in the fleet, thereby reducing available capacity; while a lower newbuild rate for the global fleet has also supported chartering prices.

fleet

Dividends:

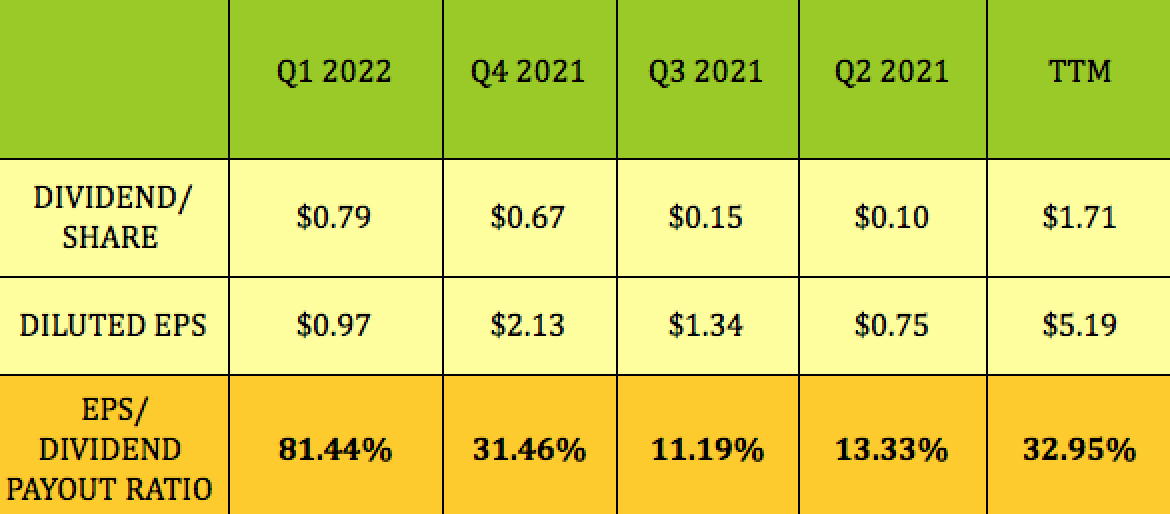

High rates led to much higher earnings, and also led to management rejiggering its dividend calculation, resulting in a much higher dividend over the past 2 quarters. The Q4 ’21 dividend rose from $.15 to $.67, and rose again in Q1 ’22, to $.79.

Using a traditional EPS metric shows GNK’s Q1 ’22 dividend payout ratio at 81.4%, with a very low trailing payout ratio of ~33%:

Hidden Dividend Stocks Plus

GNK’s new dividend policy deducts Debt Repayments, Maintenance Capex, and a reserve from Operating Cash Flow to calculate Distributable Cash Flow for dividends. That figure is then divided by the number of shares that are due dividends, in order to calculate each quarter’s dividend/share, which was $.79 for Q1 ’22.

This 2022 cash flow chart shows that Q2′ 2022 will have much higher Capex: dry docking/BWTS/ESD expenses of $24.71M, up ~$22M vs. Q1 ’22.

If GNK’s Net Revenue stays flat in Q2 ’22, the Operating Cash Flow would be ~$58.14M. With the additional $22M in Capex, the Distributable Cash Flow would equal ~$13.93M, and the Q2 dividend would be ~$0.33/share, down $.46 vs. $.79 in Q1 ’22. It depends upon the Net Revenue.

However, management sees much lower Capex costs in Q3 of just $3.95M, and $3.50M in Q4 ’22, so if TCE rates stay high in Q3-4 2022, GNK would be able to return to a paying out a bigger quarterly dividend in the 2nd half of 2022.

Another plus from this chart is that, according to the steady 42.5M share count, management doesn’t plan on issuing more shares in the balance of 2022.

GNK site

GNK site

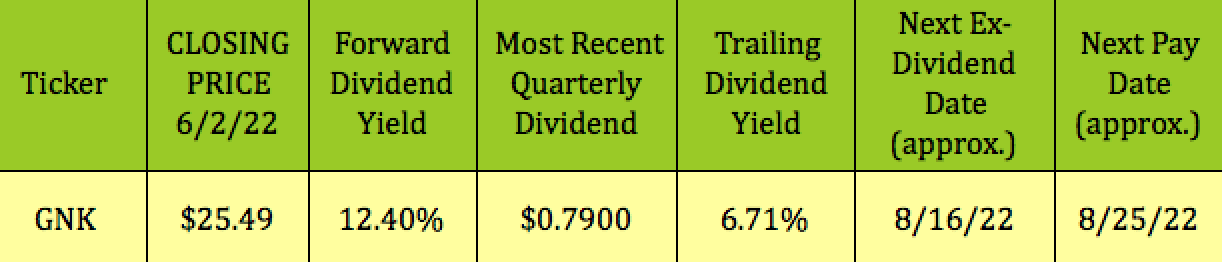

GNK’s trailing dividend yield is 6.71%, while its forward dividend yield is 12.4%. Most likely the yield will end up somewhere between the two in 2022. It should go ex-dividend next on ~8/16/22, with an ~8/25/22 pay date.

Hidden Dividend Stocks Plus

Performance:

With rates and dividends rocketing so much higher, GNK has charmed Mr. Market, and has outperformed the Marine Shipping industry and the S&P 500 by very wide margins over the past month, quarter, year, and so far in 2022:

Hidden Dividend Stocks Plus

Earnings:

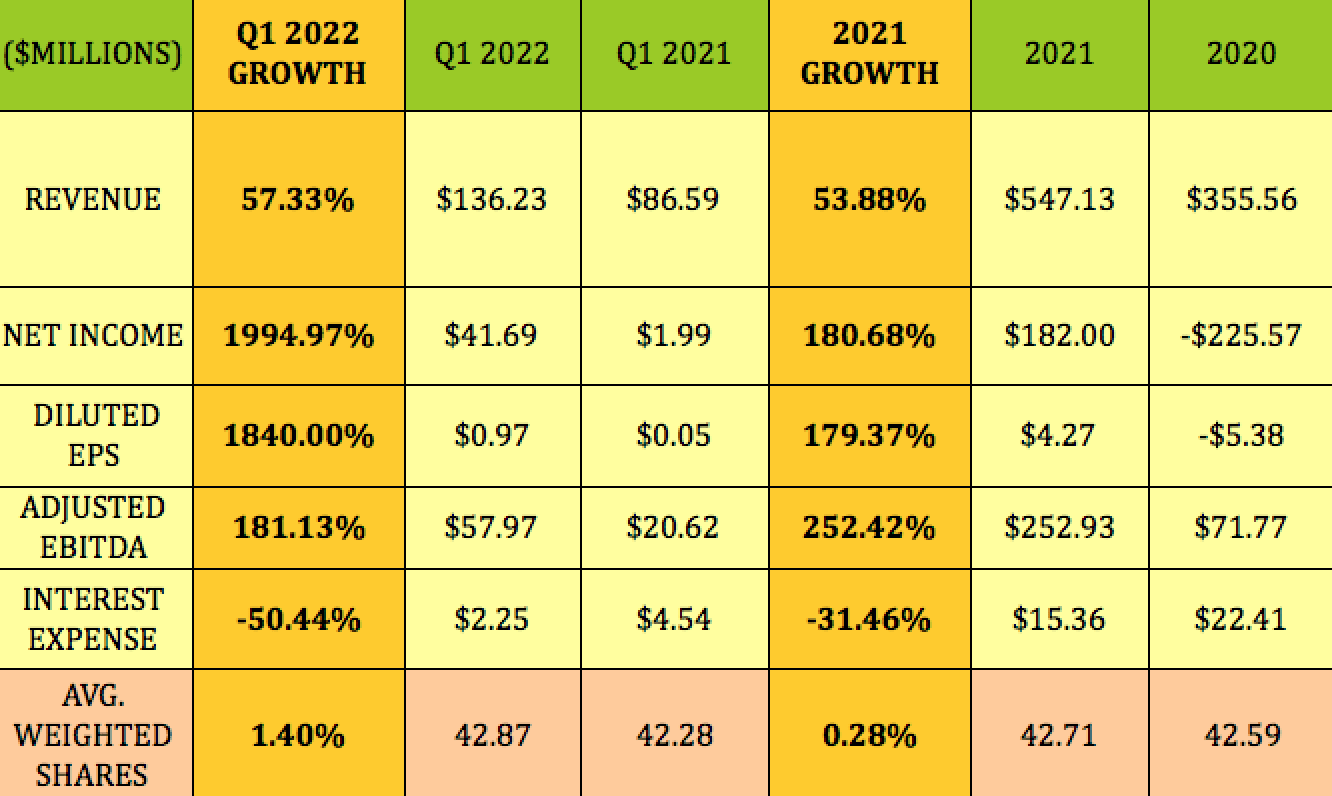

GNK’s gaudy Q1 2022 earnings growth numbers show you far bulk cargo rates have risen since Q1 ’21. 4-digit growth rates aren’t seen around these parts too often. And these numbers happened in spite of China being in lockdown mode for part of Q1 2022, due to its Covid outbreaks. That bodes well for the 2nd half of 2022, when China should fully reopen.

2021 full year growth was also robust, with 3-digit growth across the board. In addition to much higher shipping rates, Interest Expense also declined by 31% in 2021, and fell over 50% in Q1 ’22, thanks to management’s focus on paying down debt, and lower interest rates.

Hidden Dividend Stocks Plus

While Q1 2022 revenue jumped by 57%, expenses only rose by ~14%:

GNK site

Profitability & Leverage:

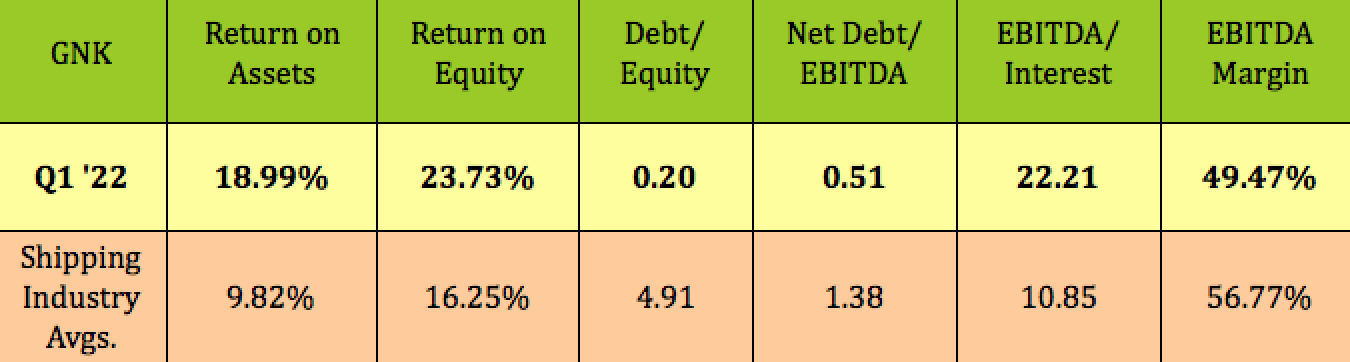

Normally when you look at the shipping industry, you expect high levels of debt leverage, but not with GNK, which has the lowest debt leverage we’ve seen in this industry for a long time. Since 1/1/2021, management has paid down $252M, or 56% of GNK’s debt.

GNK’s trailing ROA and ROE are much higher than shipping industry averages.

Hidden Dividend Stocks Plus

Debt & Liquidity:

GNK has no debt amortization payments until 2026, when its credit facility matures. It had $49.1M in cash, plus $222M in availability on its credit revolver, as of 3/31/22.

Valuations:

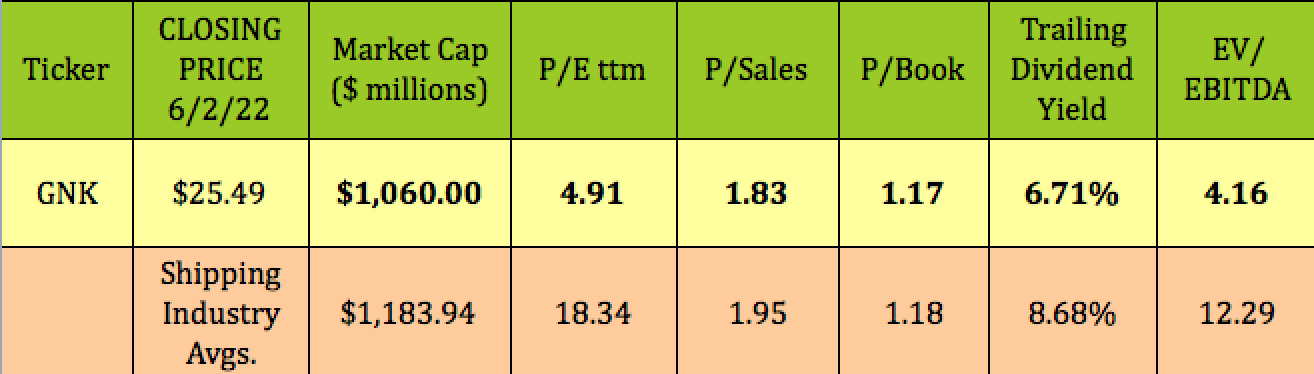

The 2 compelling under valuations for GNK are its trailing P/E of just 4.91X, vs. the 18.34X marine shipping industry average; and its very low EV/EBITDA of 4.16X, vs. the 12.29X industry average. With low debt, but strong EBITDA, all that’s left for GNK’s Enterprise Value ratio to rise is its market cap, which should do so, in light of its prospects for continued profitability in 2022.

Hidden Dividend Stocks Plus

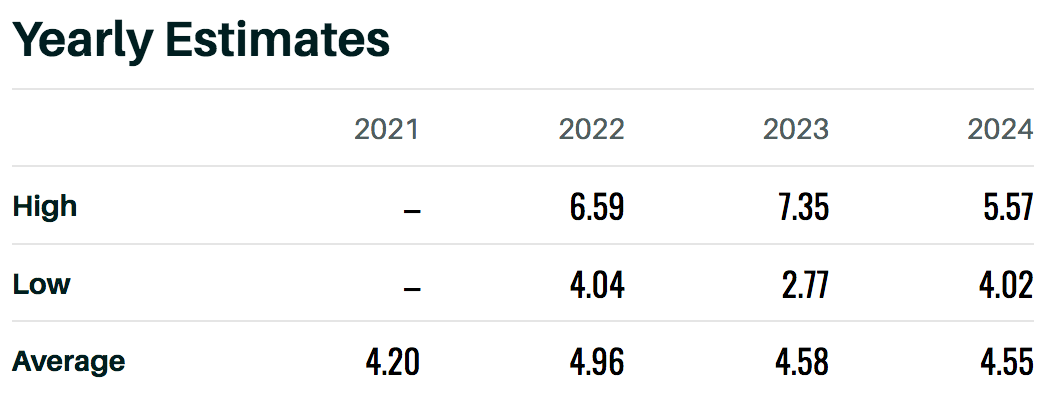

Analysts’ Estimates & Price Targets:

Looking forward, we see that GNK has a forward 2022 P/E of 5.14, still much lower than industry averages, and a 2023 P/E of 5.57.

Barrons

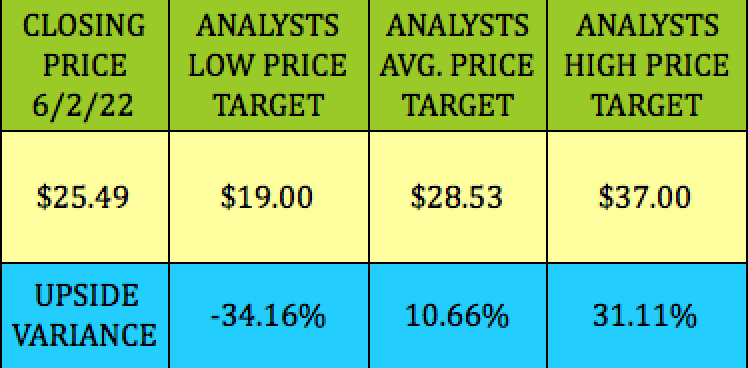

GNK received a recent BUY rating from Jefferies on 4/27/22, who resumed coverage, with a $27.00 price target. At $25.49, GNK is 10.7% below the $28.53 average price target, and 31% below its $37.00 highest price target.

Hidden Dividend Stocks Plus

Parting Thoughts:

With few orders for new ships, and China reopening, shipping rates should continue to find support in 2022, which will, in turn, support GNK’s new dividend policy.

We rate GNK a BUY, based upon its improved debt leverage, dividend policy, and shipping industry tailwinds.

If you’re interested in other high yield vehicles, we cover them every weekend in our articles. All tables by Hidden Dividend Stocks Plus, except where otherwise noted.