Editor’s note: Seeking Alpha is proud to welcome Daniel Dunaevski as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA PREMIUM. Click here to find out more »

Stock Analysis Fuchs Petrolub SE

In my opinion, Fuchs Petrolub (OTCPK:FUPEF) is a company with a sustainable business model, an important competitive advantage and a very competent and forward-looking management. Despite the current difficulties, I am convinced that FUPEF will be a successful long-term investment. But let us first have a look at the fundamentals of the company.

FUPEF is a holding company that holds shares of 58 operating companies, 53 of which are active abroad. Over the past decades, the company has expanded into new markets and upgraded existing production sites, so that production is now carried out locally in 33 different countries.

The structure of the holding company is as follows: The parent company holds 100 percent of most of the subsidiaries, which in turn transfer their profits to the shareholder in the form of dividends. The parent company consists practically only out of equity. This equity consists out of shares in the participating interests, receivables from affiliated companies and cash and cash equivalents.

FUPEF is majority family owned in the third generation. The family holds 54% of the ordinary shares. Since 2004, Stefan Fuchs has held the role of CEO. In the course of the analysis I was able to discover some interesting articles and interviews with Stefan Fuchs and gain a good first impression of him. In my opinion he is a very intelligent and forward-looking CEO who is interested in the long-term success of his company. Under his leadership, the expansion into new markets, debt reduction and specialization of the product range has been successfully continued. In my view, the influence of the long-term oriented founding family becomes clear relatively quickly when you look at the objectives and investment programs of recent years.

In addition to the family as the main shareholder, 5.2% of the ordinary shares have been held by DWS-Investment since 2003 and a further 5% since January 2019 by Mawer Invested Ltd. from Canada. However, they have not yet (publicly) attempted to actively influence the decisions of the founding family.

Source: Data from Annual Report 2018

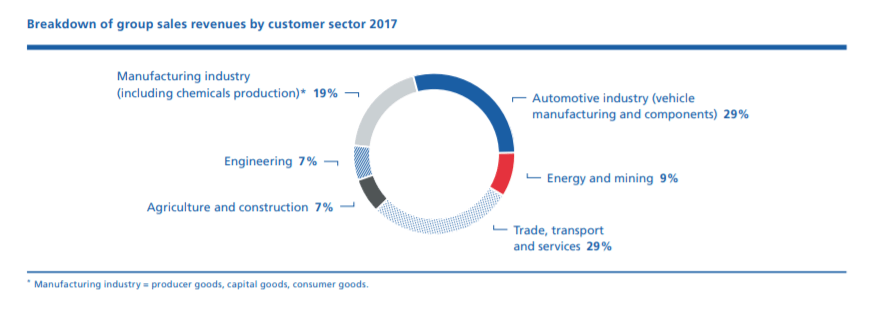

FUPEF is currently active in 45 countries and has over 100,000 individual customers worldwide. It is an advantage that the share of individual customers does not exceed the 2% mark. This means that there is little dependence on the development of individual companies and the customer’s negotiating power is also limited. The composition of the customer sectors is as follows:

Source: Data from Annual Report 2017

This illustrates the high dependence on a few cyclical sectors. This picture is reinforced if we look at the group’s sales structure by product groups.

Particularly noteworthy here is the significant share of sales accounted for by the automotive industry. Although the company is diversified among the various suppliers, it is still highly dependent on developments in this field. Thus, mainly due to the current situation in the automotive industry, EBIT for the current year is predicted to be 20% below that of the previous year. Here, however, the business model of FUPEF is advantageous, as the automotive industry often can hardly do without lubricants despite a weak phase.

Source: Created by author using data from Annual Report 2018

FUPEF is also relatively well diversified regionally and is constantly driving further expansion. This appears necessary when one looks at the development of lubricant demand in the individual regions.

Source: Created by author using data from Annual Report 2018

Source: Created by author using data from Annual Report 2018

At first glance, the above table appears sobering, but it should be noted that FUPEF is currently in the process of building up its infrastructure in Asia and aims to increase its market share there, so that growth above market level should be achievable in the medium to long term.

Source: Created by author using data from Annual Report 2018

In Europe and especially in Germany, where FUPEF already has a market share of around 15%, growth is weaker. However, FUPEF should be able to gain market share and therefore market growth should be exceeded.

The long-term regional expansion of the company becomes clear when looking at the development of sales in Germany: Whereas in 2009, 30% of sales were generated in Germany, the share was reduced to 23% in 2018 (despite growth in the domestic market). Thus, on the one hand the dependency on a regional market was reduced and on the other hand the share of faster growing markets was increased.

Growth

In 2018, FUPEF was able to grow organically in all regions. At the same time, however, FUPEF is on the lookout for interesting takeover opportunities to expand its product range in a targeted manner. It currently looks as if organic growth in 2019 continued growing in the lower single-digit range, while profits fell by around 20%, but more on this later.

To ensure the long-term growth of the company, several investment programs have been set up in recent years, of which “Program Fuchs 2025” is currently underway. In this way, annual investments of at least 100 million euros are to be made in production, IT and infrastructure. The Mannheim location, for example, has been expanded and modernized. In many cases, the plants are designed to be fully automated in the course of the modernization and thus made fit for the future.

Among other things, a further new plant in China was commissioned in 2018. This became necessary because the previous plants had reached their capacity limits. This shows that the company is pressing ahead with global expansion and building up capacity in line with demand.

Other investment priorities in the future will be the USA, Germany, China and Sweden.

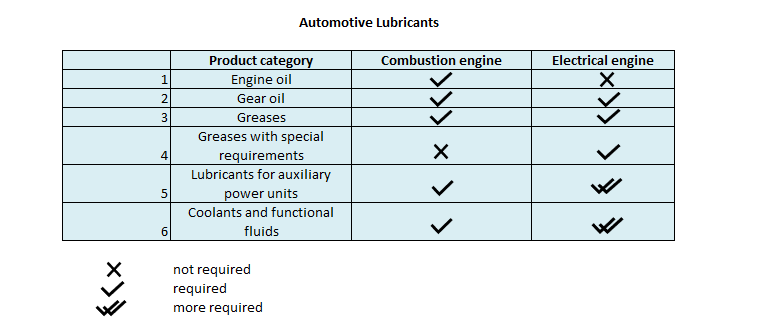

Future growth is to be generated through further expansion, targeted acquisitions and the early identification of new trends. Electromobility will play an important role here. Due to new areas of application for lubricants, this brings new challenges, but above all opportunities. In my opinion, FUPEF is very well positioned in this area, as the trend was recognized early on and the research orientation was adjusted accordingly.

For example, the annual report deals in detail with the changes in requirements for lubricants for the powertrain and transmission of electric cars. Smaller manufacturers with less research capacity are likely to be at a disadvantage here for the time being.

Although sales of engine oils are likely to decline in the course of the switch to electric mobility, other options are opening on the other side, such as for central locking systems, sensor motors or rolling bearings in electric motors.

Source: Created by author using data from Annual Report 2018

According to FUPEF, the decline in the demand for lubricants is likely to be only marginal. However, since requirements and complexity will increase at the same time, there will be opportunities for growth.

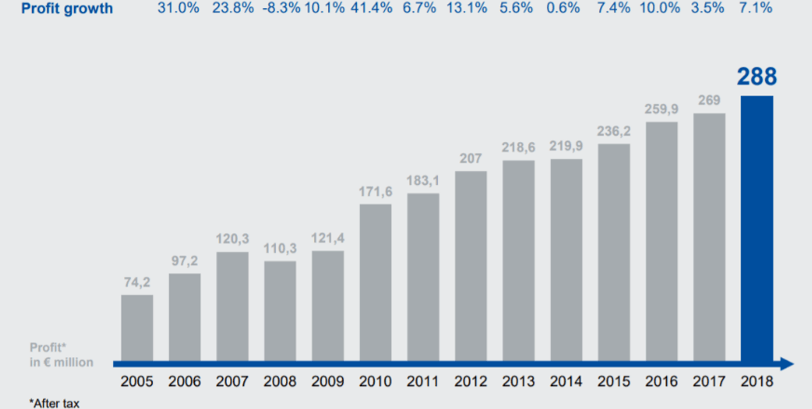

In recent years, sales and profit increases have been achieved mainly organically, although it should be noted that a major acquisition (€135 million) took place in 2015. Although share buybacks were carried out in 2013 and 2014, these were relatively small. FUPEF was therefore able to grow revenue by 9.2% and earnings by 10.7% over the last 10 years. This development was far above the market average, which was in the low single-digit range as stated in FUPEF’s annual report 2018. However, it should be noted that growth has slowed in recent years.

Source: Annual Report 2018

While sales are expected to increase only very slightly for 2019 and 2020, profits are expected to fall, which is due to high raw material costs and weaker sales in the high-price segment.

Profitability

When considering profitability, it quickly becomes clear that FUPEF has a special market position. In recent years, the company has been able to increase the price of its products due to its specialization strategy and focus on specific customer requirements. This development is clearly illustrated by the EBIT margin, among other things.

Source: Created by author using data from Annual Report 2018

This is a very good development and at the same time it is clear that the margin has not been increased in recent years. An important factor for this are the costs of raw materials. These account for a large part of the costs of sales and are relatively volatile in contrast to other relevant cost items, such as personnel expenses and administration. However, it should not be the case that raw material costs are directly correlated with the price of crude oil, since a number of intermediate products are used in the manufacture of lubricants, and their price development does not exactly reflect that of crude oil.

The return on equity is also very high despite an equity ratio of around 76%. Over the last ten years, an average return on equity of about 25% has been achieved. Among other things, this indicates a certain market power or good positioning. Although the return on equity is currently at a very high value of around 20, it cannot match the values from 2010 to 2014. This can also be attributed to the ever increasing equity ratio and slowly rising profits.

Another indication of FUPEF’s good profitability is the high free cash flow. This has been steadily increased over a longer period with the exception of a few years. In recent years, however, the free cash flow has been reduced by investment programs. Since the investments serve to expand infrastructure and capacities, investors are likely to benefit more from this in the medium to long term than from a higher FCF and the associated higher dividend payments. All in all, I believe that FUPEF is investing its money very sophisticated and with a focus on future growth.

Overall, however, profitability is likely to decline in the future, as growth is mainly achieved in Asia and South America, where only lower margins can be achieved.

Stability

The stability and thus potential susceptibility to crises has improved greatly at FUPEF in recent years. Financial debts have been reduced slightly each year and are practically non-existent at the present time. At the same time, net liquidity (2018: €191 million) has been increased so that, on the one hand, acquisitions can be implemented without having to borrow and, on the other hand, it is possible to survive periods of economic weakness. FUPEF also has €183 million in free credit lines which can be used beyond the existing liquidity. From the current perspective, however, these are unlikely to be necessary in the short to medium term, as investment programs can easily be paid for out of operating cash flow and still leave enough free cash flow to pay dividends and even increase them.

For the sake of completeness, it should be briefly mentioned at this point that both the gearing and the dynamic debt-equity ratio of the last ten years are negative, as the liquid funds far exceed the financial liabilities.

A large part of FUPEF’s liabilities is made up of trade accounts payable. However, these liabilities do not require debt service and are of a short-term nature.

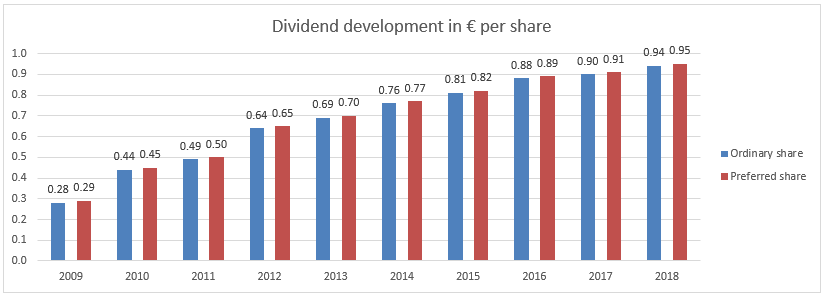

Another point is the payment of the dividend. This has been increased every year since 2001 (beginning of my observation). The crisis years were no exception. Except for two years, the dividend was paid out of free cash flow. This is likely to increase significantly following the completion of the current investment program, so there is still scope for dividend growth.

Source: Created by author using data from Annual Report 2018

Finally, it should be noted that in the 35 years since going public, FUPEF has succeeded in closing each year with a profit and even after major crises (2009) it has been able to quickly increase its profits compared to the pre-crisis period.

Cycle

FUPEF has a non-cyclical business model, but this is only partly true due to the current customer structure. Basically, lubricants are needed for existing plants, even if the economy is weak. However, it should be noted that customers from the automotive industry are subject to fluctuations which have an impact on the sales of lubricants. For example, production shutdowns can lead to a reduction in the demand for lubricants. Thus, mainly due to the weak phase in the automotive industry, EBIT has been forecast to fall by about 20% for the current year.

In addition, inventories in 2018 are 12% higher than in the previous year. In part, this can be attributed to delays in deliveries because some lubricants had to be shipped from Germany to China due to capacity bottlenecks. Another reason is due to a lower order backlog. Here, FUPEF uses the NOWC key figure to calculate the capital tied up in inventories (see Annual Report 2018, p. 39). The NOWC is currently 42% and the capital tie-up is 85 days, which makes the company inflexible in the face of short-term market downturns.

Unique selling point

The market for lubricants is highly competitive and highly fragmented worldwide. According to FUPEF, the competition consists of about 600 companies, most of which are relatively small. Fuchs has managed to avoid the competition from the large mineral oil companies by occupying a niche. Lubricants are often not developed for the mass market, but in cooperation with the customer to meet his specific requirements. As a result, FUPEF’s 10,000 different products are individually adapted to the customer’s needs and form a moat against the competition. At the same time, the customer’s dependency is also greatly increased, as changing the lubricant should not be unproblematic for existing plants. As a result, FUPEF has a pricing power. Although the company often competes locally with many smaller competitors, these are often unable to respond to individual customer wishes due to limited research capacities and hardly represent competition for lubricants with special requirements.

By expanding the infrastructure and creating new production sites, FUPEF can guarantee the customer high quality and rapid availability of lubricants on site. In recent years, both the average delivery time and the transport accounts have been reduced.

In addition, digitalization has been pushed forward in recent years, which could be used to occupy other stages of the value chain in order to bind customers even closer to them. In 2018, the company Fluid Vision Technology LLC was acquired, which has expertise in wireless sensor technology for industrial fluids. This enables FUPEF to inform the customer at an early stage when a further order of the lubricant will be necessary in order to guarantee the optimal operation of the machines. This creates an additional dependency and a high added value compared to pure lubricant suppliers.

Evaluation

I have valued FUPEF in two different ways: based on multiples and with the help of a forecast based on the ROE. In doing so, I found that, in my opinion, the weak phase of the next few years was not yet sufficiently priced into the share price. For example, the P/E ratio for 2019 would be around 24, which is far above the average of the last 20 years (14.9) and 10 years (19.6).

Source: Created by author using data from Annual Report 2018

Source: Created by author using data from Annual Report 2018

Nor do the other multipliers indicate that the market is assuming that the company is in a weak phase, as predicted by the management board.

My result of the forecasting method using return on equity is similar. Here I have tried to depict a best-case and worst-case scenario and to transfer the effects on profit development and the share price for the next five years. I concluded that in a best-case scenario a share price of €60.30 could be reached in five years. In the worst-case scenario, the share price would be €29.50 in five years. At the current price of €40.0, this would result in an annual return of between 8.5% and -5.8%. In my opinion, this would not be a satisfying return, so that I consider the share to be overvalued at present.

Conclusion

I believe that FUPEF is a very solid company with great prospects. What I like most is that it is a family business and management does not seem to attach any importance to short-term goals or share prices. The focus is on long-term growth and prospects.

FUPEF has a great unique selling point and a solid moat. In addition, the financial situation is excellent and provides plenty of scope for future development. Growth has slowed down compared to recent years, but it is necessary to wait and see how the automotive and manufacturing industries develop. At present, the company’s profitability is very good. However, it should be observed whether it can be maintained at the current level in the coming years as the company expands.

Finally, I believe that the current valuation is too high and that either the share price or the fundamentals will adjust in the future.

Even if the analysis has been somewhat critical of the company in some cases, I am nevertheless convinced that FUPEF is capable of growing in the future and generating a decent return for its investors.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.