adamkaz/E+ via Getty Images

Modes of transportation are, by necessity, complicated pieces of equipment that require many different components in order to operate accurately. One company dedicated to providing niche components to various transportation devices is Fox Factory Holding Corp (NASDAQ:FOXF). Over the past few years, the management team at the enterprise has done well to grow its top and bottom lines. Revenue has risen nicely, while cash flows look robust. Shares are not particularly cheap at this time. But if current guidance holds, the firm does look somewhat attractive on a forward basis. Due to all of this, I believe that Fox Factory Holding Corp, while not a fantastic value opportunity at this time, does offer some upside potential in the years to come.

A Diverse Play On Transportation Equipment

According to the management team at Fox Factory Holding Corp, the company engages in the production and sale of performance-defining products and systems that are used on various types of equipment. The equipment in question includes bikes, side-by-sides, on-road vehicles with and without off-road capabilities, off-road vehicles, trucks, ATVs, snowmobiles, specialty vehicles, motorcycles, and commercial trucks. To be more specific, it would be best to break the company’s operations down into two different categories.

On the powered vehicles side, the company sells vehicle suspension products to its customers that consist of major OEMs like Ford (F), Polaris (PII), Toyota Motor Corporation (TM), and others. In addition to selling directly to these companies, the business also sells to aftermarket dealers and distributors, both in the US and abroad. On the specialty sports side, the company sells bike suspension products, as well as other related components to the domestic and international bike OEMs that it works with. Like in the case of powered vehicles, the company also services the aftermarket crowd by working directly with US dealers and through international distributors.

Author – SEC EDGAR Data

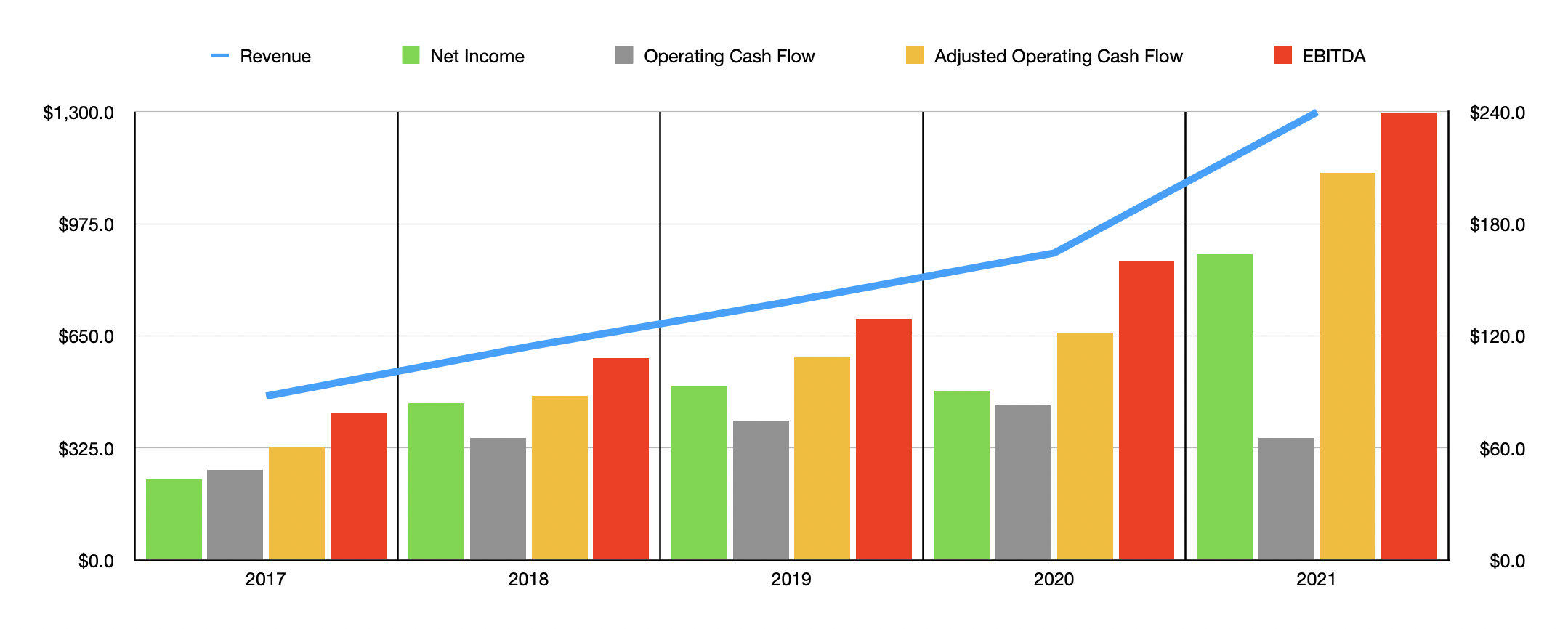

Over the past few years, the management team at Fox Factory Holding Corp has done an incredible job growing the company’s top line. Revenue in 2017, for instance, totaled just $475.6 million. This increased each year since, eventually climbing to $1.30 billion in 2021. That translates to an annualized increase of 28.6%. Growth was particularly strong from 2020 to 2021 when revenue soared by 45.9%. According to management, this increase in sales was driven largely by a 57.8% rise in specialty sports products. However, the company also experienced a 37.5% increase in revenue associated with the powered vehicle products that it sells. However, the company also attributed some of this growth to its 2021 acquisition of SCA, which required it to pay out $331.5 million in cash consideration.

On the bottom line, things have followed a similar trend. The company saw its net profit rise from $43.1 million in 2017 to $93 million in 2019. It then dipped to $90.7 million in 2020 before jumping to $163.8 million last year. Of course, we should also pay attention to other profitability metrics. More volatile has been operating cash flow. It grew from $48.2 million in 2017 to $82.7 million in 2020. But then, in 2021, it fell to $65.3 million. The good news for investors is that if you adjust for changes in working capital, the picture does change. And for the better. Using this approach, cash flow would have risen consistently year after year, climbing from $60.9 million in 2017 to $207.4 million in 2021. Meanwhile, EBITDA for the company also increased, rising from $79.1 million in 2017 to $239.5 million last year.

Author – SEC EDGAR Data

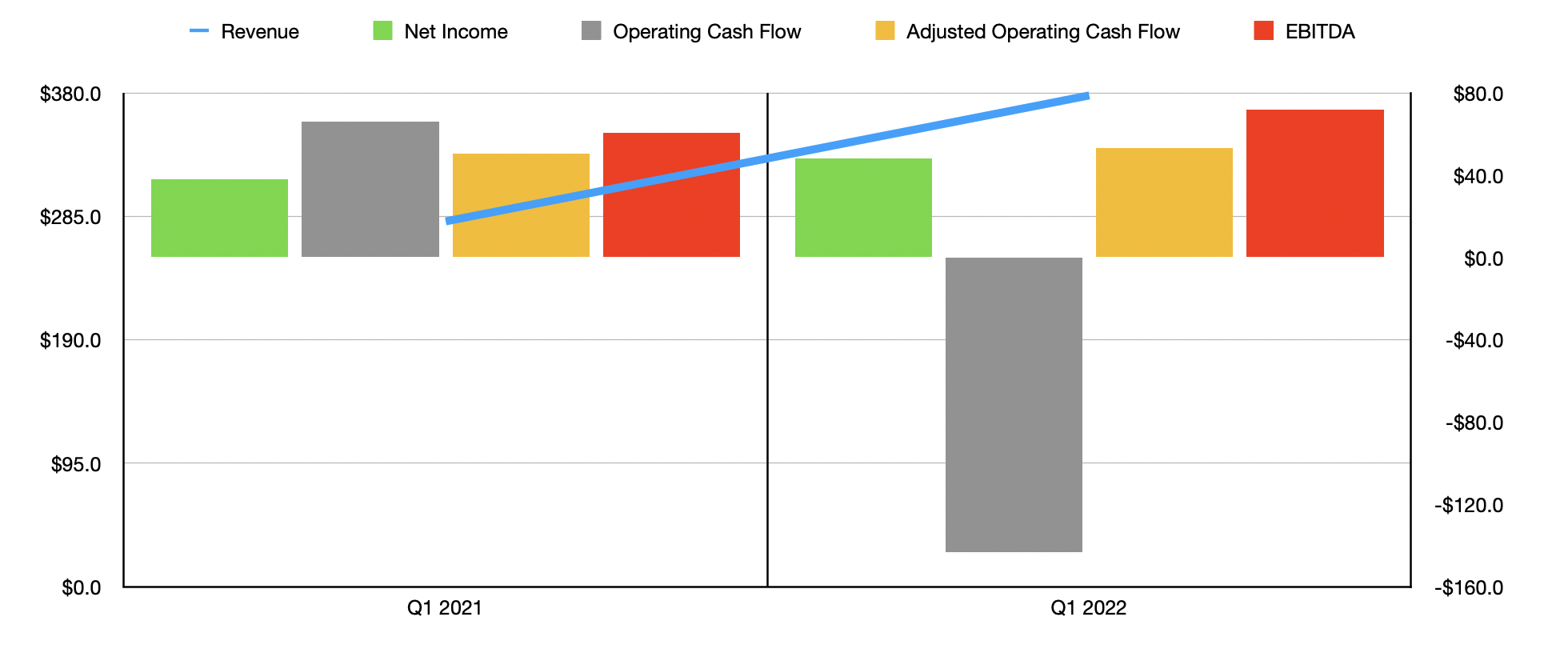

When it comes to the 2022 fiscal year, management has some rather upbeat expectations for the company. Sales should come in at between $1.50 billion and $1.53 billion. At the midpoint, this would translate to a year-over-year increase of 16.6%. The company is also forecasting earnings per share of between $5 and $5.30. Midpoint figures imply net income for the company of $216.2 million. If we assume that the growth in earnings is indicative of the kind of growth, we can expect for adjusted operating cash flow and for EBITDA, then those metrics should be $273.7 million and $316.1 million, respectively. So far, the company is off to a pretty strong start. Sales in the first quarter of 2022 totaled $378 million. That is 34.5% above the $281.1 million generated in the first quarter of 2021. Net income has risen from $38 million last year to $48.1 million this year. Operating cash flow did worsen, falling from $66 million to negative $143.1 million. But if we adjust for changes in working capital, it would have risen from $50.5 million to $53.3 million. Meanwhile, EBITDA is also up, having risen from $60.4 million to $71.8 million.

Author – SEC EDGAR Data

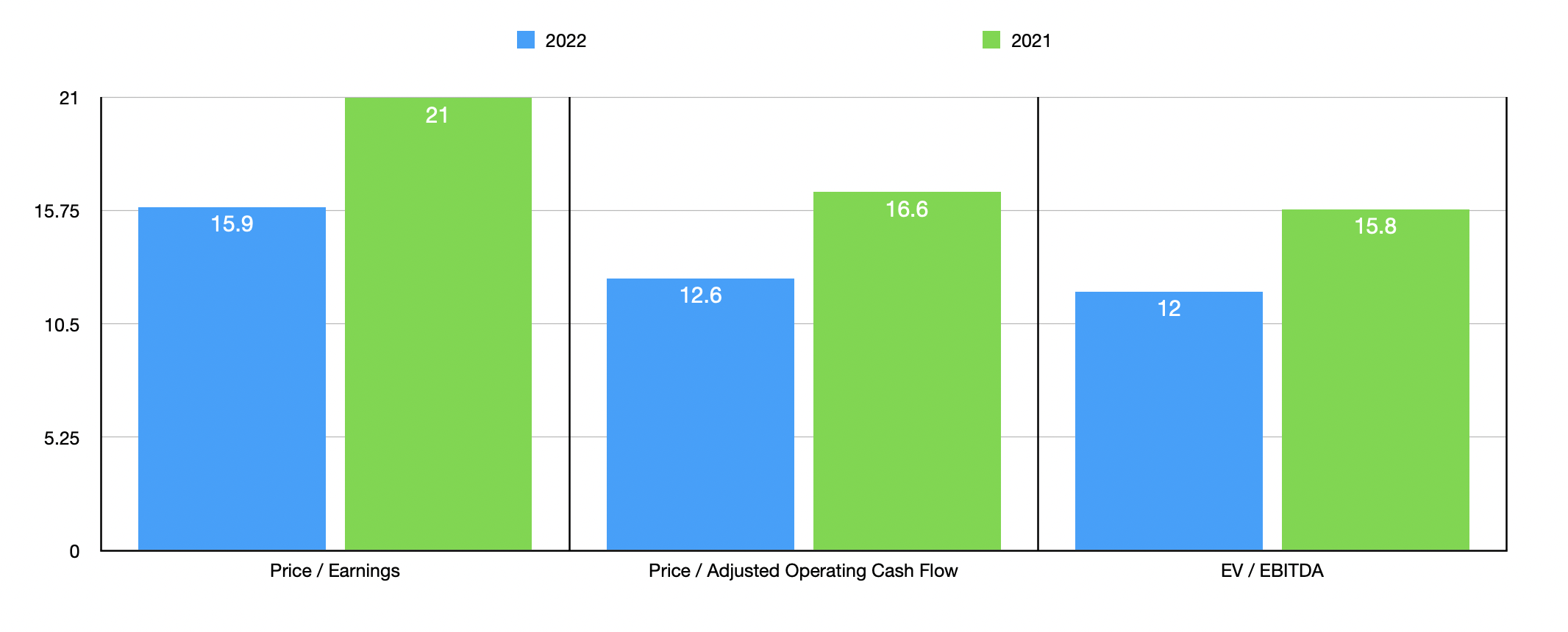

To value the company, I decided to look at it through the lens of both the 2021 fiscal year and the 2022 fiscal year. Using our 2021 results, we can see that the business is trading at a price to earnings multiple of 21. This drops to 15.9 if management’s own forecast for 2022 is accurate. Meanwhile, the price to operating cash flow multiple of the company should be 16.6. This declines to 12.6 if my estimates are accurate. And for the EV to EBITDA approach, the multiple would be 15.8, a number that would drop to just 12 if my 2022 forecast is accurate. To put this in perspective, I decided to compare the company to five different firms. Four of the five had positive financial results.

Of those four, the range for the price to earnings multiple was from 4.1 to 64.9. In this case, two of the four companies were cheaper than our prospect. This assumes that we use the 2021 results instead of the forward results for 2022. Using the 2022 data, the order of ranking here is unchanged. Using the price to operating cash flow approach, the range was from 22.9 to 158.2. Our prospect was the cheapest of the group, irrespective of whether we used the 2021 figures or the 2022 estimates. Meanwhile, using the EV to EBITDA approach, the range was from 3.3 to 15.8. With the 2021 results, Fox Factory Holding Corp was tied as being the most expensive of the group. But if we use the 2022 estimates, two of the four companies are cheaper.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Fox Factory Holding Corp | 21.0 | 16.6 | 15.8 |

| Luminar Technologies (LAZR) | N/A | N/A | N/A |

| Dorman Products (DORM) | 23.5 | 30.7 | 15.8 |

| LCI Industries (LCII) | 7.1 | 158.2 | 6.3 |

| Adient (ADNT) | 4.1 | 22.9 | 3.3 |

| Visteon Corporation (VC) | 64.9 | 116.9 | 15.7 |

Takeaway

Based on the data provided, Fox Factory Holding Corp seems to be a solid prospect at this point in time. Though shares are not exactly cheap when using the 2021 results, they do start to look quite cheap on a forward basis. Management continues to grow the enterprise at a rapid pace, and financial performance does not seem to be impacted much by inflation at this time. All of this combined leads me to rate the enterprise a ‘buy’ prospect at this time.