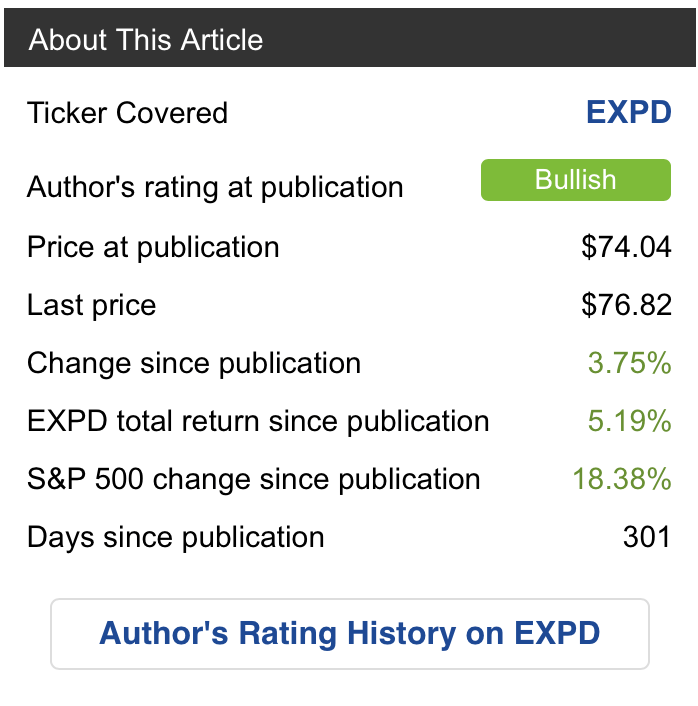

Patient Zero

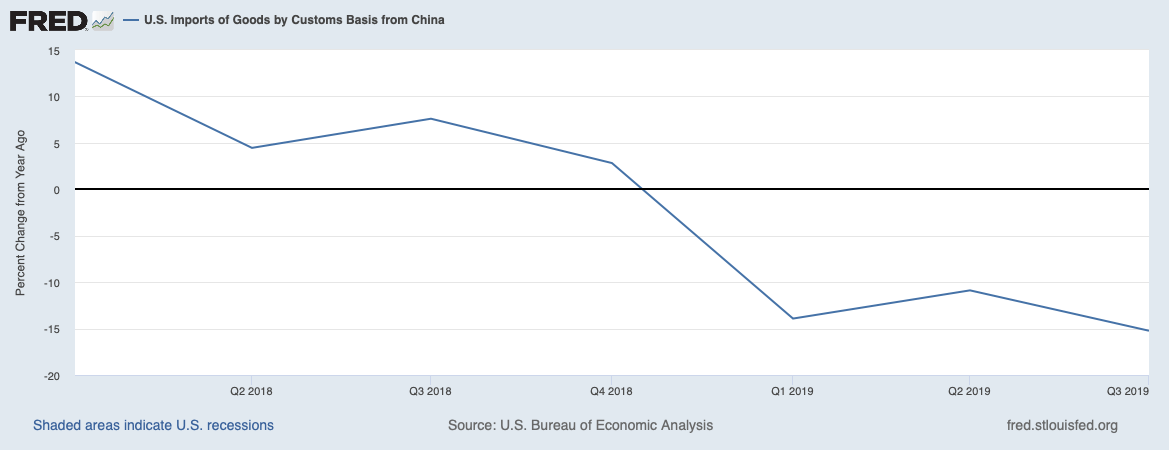

Expeditors International of Washington (EXPD) is one of my favorite companies, with great leadership and culture, and a history of navigating macro challenges quite well. But they are in the freight-consolidation and logistics business, and their biggest regional route is greater China to North America. There’s only so much great leadership can do with this:

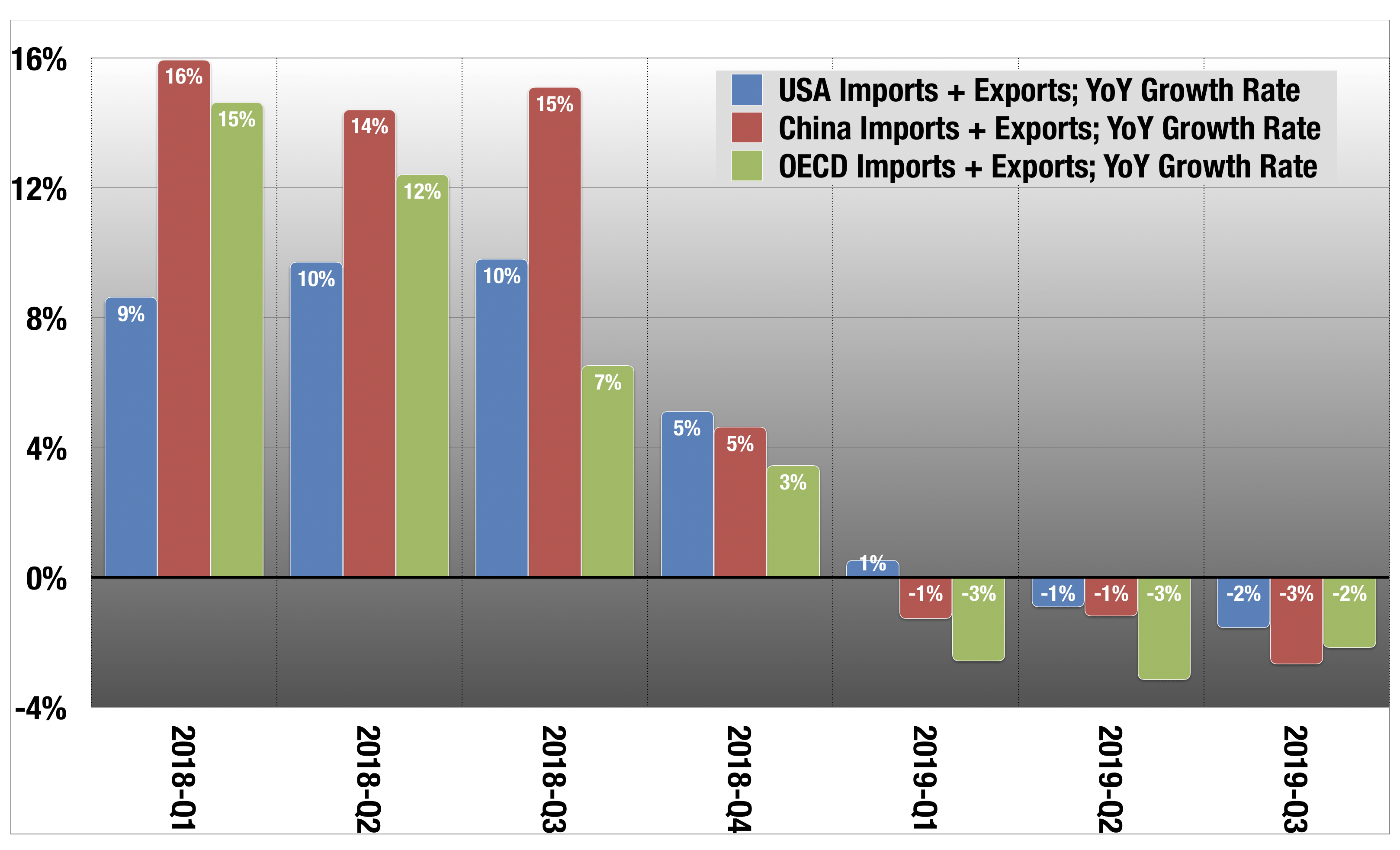

Here’s the broader picture of global trade:

Here’s the broader picture of global trade:

OECD

OECD

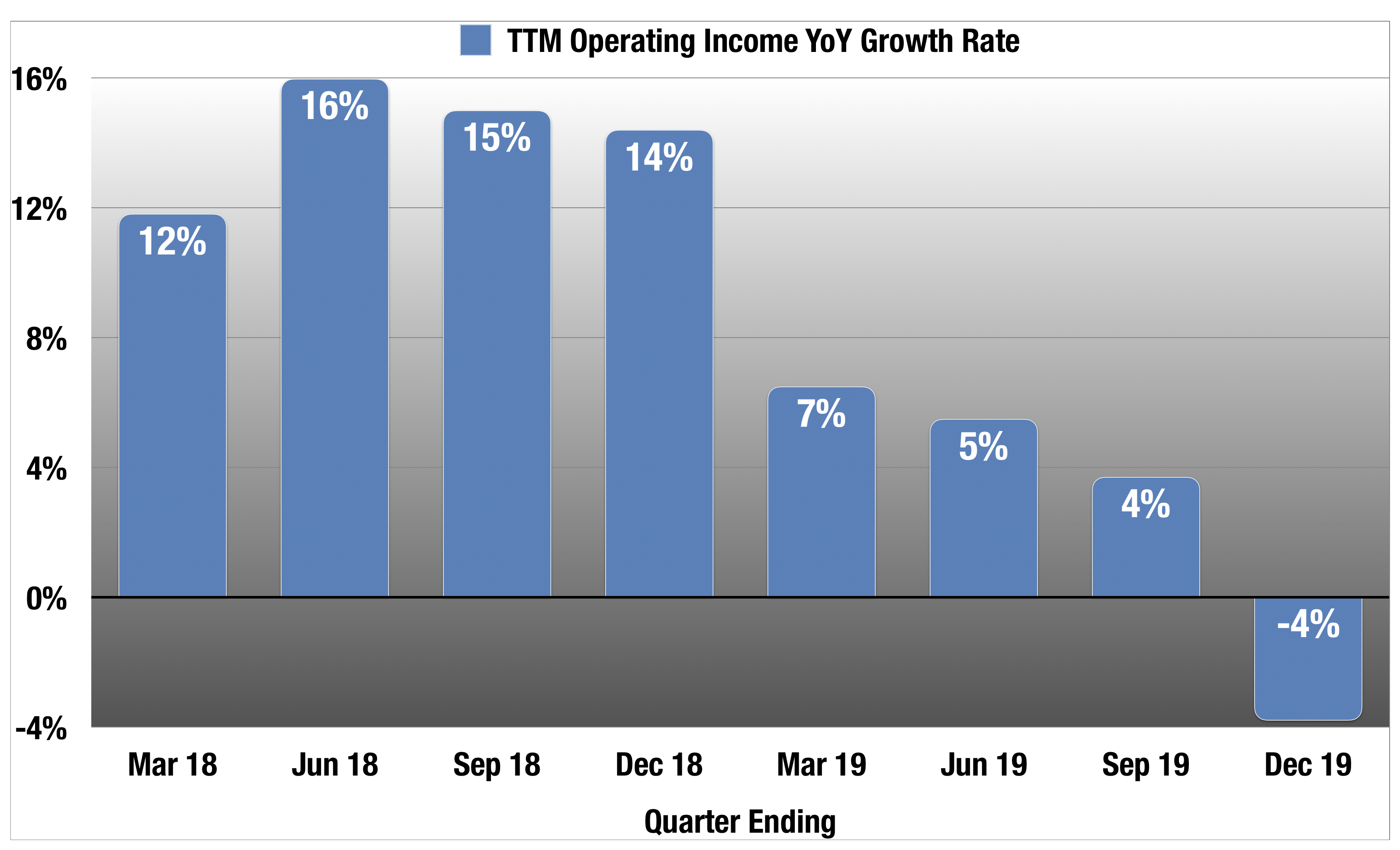

This is what happened to Expeditors’ operating income:

Company filings.

Company filings.

That last number for the December 2019 quarter comes from a recent 8-K they filed with some disappointing guidance on 2019 Q4 operating income (that growth rate is for the midpoint). This is a very quiet company that doesn’t put out many announcements and doesn’t do a quarterly earnings call. But they do follow Crisis Management 101: get all bad news out quickly and completely, with full transparency. It’s amazing how many companies can’t follow that simple rule.

The stock took a beating on the news:

Data by YCharts

Data by YChartsAs you can see, it bounced quickly off the open, but still wound up off 5.6% on the day. The company has a lot of fans and longtime shareholders, and that is typical when the stock tumbles.

As for me, I sold out last March after FedEx’ (FDX) first round of downward guidance. From my last report on Expeditors from March 2019, explaining why:

Global growth is slowing and it has begun to hit the US economy, beginning in December. Global demand is slacking, and this is not good news for the freight and customs brokerage business. The morning after the FedEx cuts, Expeditors was trading pretty close to its 52-week high, so I sold my position, and I’m looking to get back in at a lower price.

I didn’t just sell EXPD but all transports, which I was pretty heavy on at that point.

Since then:

It is one of the lowest performing members of both the Dow and S&P Transport indexes. As you can see, I haven’t gotten that lower price, but it is drastically underperforming the S&P 500. But now, with more realistic pricing and the Phase One deal coming on line, there is reason for another look.

It is one of the lowest performing members of both the Dow and S&P Transport indexes. As you can see, I haven’t gotten that lower price, but it is drastically underperforming the S&P 500. But now, with more realistic pricing and the Phase One deal coming on line, there is reason for another look.

I’m going to start off by explaining why I like them so much. Briefly:

- They have great leadership and culture.

- They navigate the variety of macro headwinds they face exceptionally well.

- They have a very sexy balance sheet that can carry them through tough times.

We’ll look at a couple of past case studies of large macro headwinds they faced, and how the company performed through it. Then we’ll look at their current situation and what the lowered tensions may mean for them.

History and Culture

Expeditors was formed in 1981 as a one-stop shop for freight and customs brokerage for small and medium-sized companies. It is a basic buy for a nickel, sell for a dime business. They purchase air and sea freight at bulk wholesale prices and sell it to customers for more. In addition, they provide services like customs brokerage and logistics, a growing portion of the business.

There were 8 founders of Expeditors, and by 1988 they had 24 locations, gone public, and named one of the founders, Pete Rose (seriously) as CEO. Like his namesake, Rose was a bit of a character and had a lot of hustle. He instituted their unique compensation and HR systems, which I will get to in a moment. Rose never did quarterly conference calls, but rather an extensive written Q&A, in which his razor wit was often on display, and we’ll get a little taste of that later.

After expanding the company to 250 locations with 14,000 employees, Rose retired in 2014, and his cheeky Q&As unfortunately went with him. He was replaced by CIO Jeff Musser, who began at Expeditors as a messenger in 1983 at 17 years old. It took him 8 years to move up from messenger to district manager, another 8 years to regional VP and from there, CIO and CEO. 31 years from messenger to CEO.

This is not uncommon at Expeditors, and all of the top executives began at low levels. How do they keep their employees for so long? Rose realized early on that Expeditors was wide open to all sorts of macro shocks that were beyond their control — recessions, tariffs, oil prices, forex, etc. So he chose to focus on what they could control: efficient corporate operations, and finding, training and retaining the best people.

The biggest part of this is their unique compensation system, where pay is tied directly to performance, and even low-level managers can make a lot of money. The company believes that this attracts and retains the best people, and keeps them motivated and challenged. It is also demanding, so slackers leave on their own. Moreover, employees need look no farther than the C-suite to see that years of hard work can pay off at this company — the top five executives all joined the company in the 1980s at entry level.

In every quarterly filing as far back as I can find, Expeditors has included some version of this passage:

From the inception of our company, management has believed that the elements required for a successful global service organization can only be assured through recruiting, training, and ultimately retaining superior personnel. We believe that our greatest challenge is now and always has been perpetuating a consistent global corporate culture…

We reinforce these values with a compensation system that rewards employees for profitably managing the things they can control. This compensation system has been in place since we became a publicly traded company. There is no limit to how much a key manager can be compensated for success. We believe in a “real world” environment where the employees of our operating units are held accountable for the profit implications of their decisions. If these decisions result in operating losses, management generally must make up these losses with future operating profits, in the aggregate, before any cash incentive compensation can be earned…

We believe that our unique culture is a critical component to our continued success. We strongly believe that it is nearly impossible to predict all events that, individually or in the aggregate, could have a positive or a negative impact on our future operations. As a result, management’s focus is on building and maintaining a global corporate culture and an environment where well-trained employees and managers are prepared to identify and react to changes as they develop and thereby help us adapt and thrive as major trends emerge.

Compare this to other HR systems like GE and Microsoft’s notorious “stack ranking”. Unlike that old Jack Welch system, Expeditors’ compensation system rewards performance, but also does not punish anyone for someone else’s good performance. You can’t do well by making someone else do poorly, like stack ranking encouraged. If all segments do well, everyone benefits.

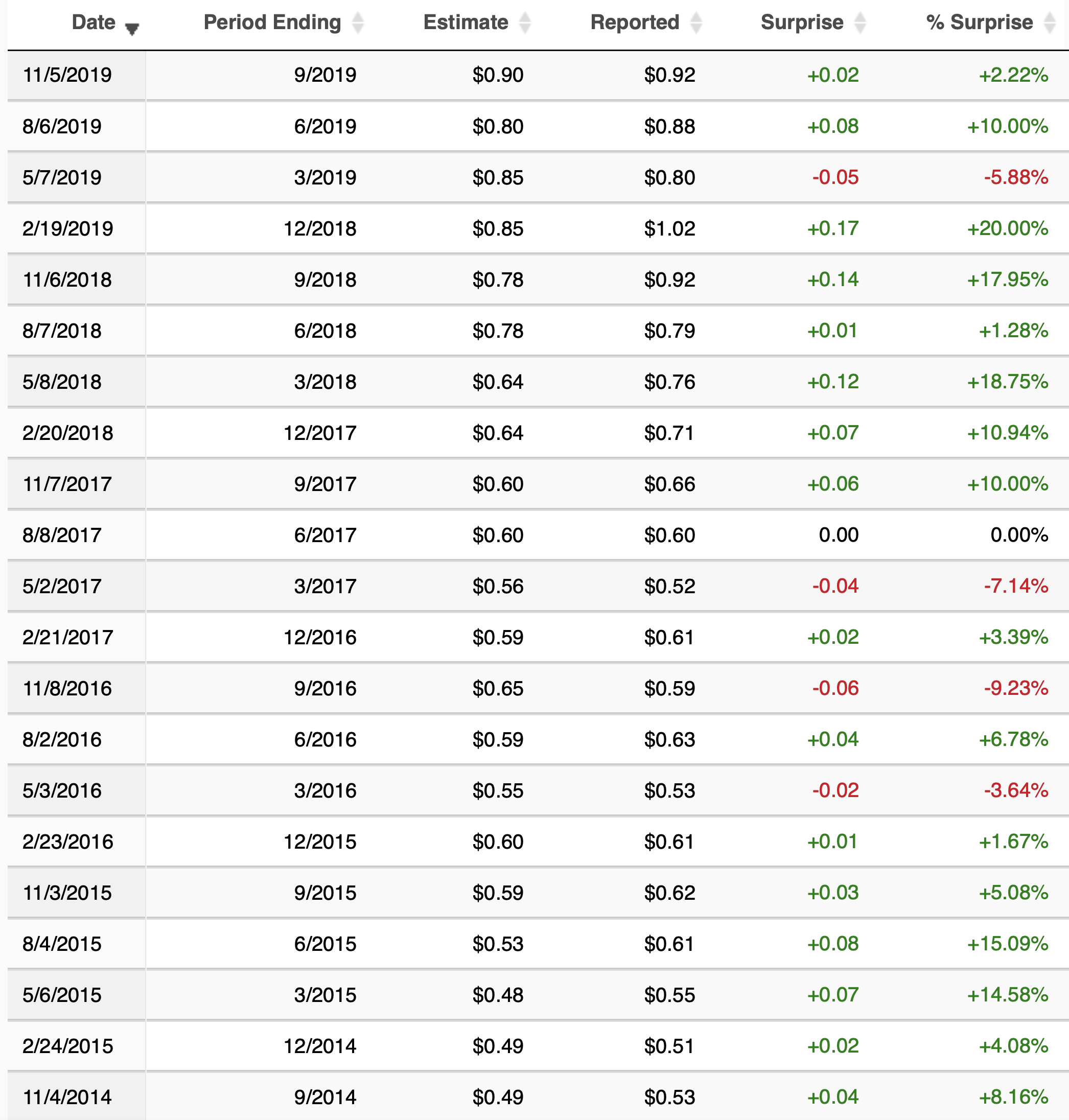

A Consistent Expectations Beater

The first thing I noticed about Expeditors was that it is a fairly consistent earnings beater. This told me they had great management, or at a bare minimum were really good at managing expectations. These are the quarters since Jeff Musser took over as CEO in 2014.

Lots of green there. That’s great and all, but it could just be Jedi mind tricks they play on analysts.

You will factor increased fuel cost pressures on sea freight into your estimate.

Let’s see what the real picture is.

The Balance Sheet: Cash Money

This type of thing always makes me happy, so let’s begin here. First off, they have zero long term debt. I love zero long-term debt. They don’t even bother having a line item for it in their filings. But beyond that, Expeditors generates a lot of cash for its size and returns much of that cash to shareholders, mostly in buybacks but also in dividends.

We’re going to look at the 10-year window here to get a sense of how they’ve done through this entire long cycle.

Data by YCharts

Data by YChartsCash flows from operations has continued to grow nicely, but their cash total took a hit as they increased their dividend and also began more aggressive buybacks in 2014. As you can see, they’ve pulled back on the buybacks due to current conditions, and cash is back up to $1.2 billion, 9.3% of their market cap, down from 16% before they got aggressive with the buybacks.

Let’s go deeper into operations, revenue and earnings.

Buy for a Nickel; Sell for a Dime

The oldest business model: buy for a nickel; sell for a dime. Expeditors has three basic revenue streams: sea freight, air freight and services. The first two have this sort of model, but services does not. Along with the usual GAAP revenue, they report “net revenue,” which in the freight categories is simply the revenue minus the consolidated cost to the company for that freight. From their last annual report:

Management believes that net revenues are a better measure than total revenues when analyzing and discussing management’s effectiveness in managing our principal services since total revenues earned by Expeditors as a freight consolidator include the carriers’ charges to us for carrying the shipment, whereas revenues earned by Expeditors in our other capacities include primarily the commissions and fees actually earned by us. Net revenue is one of our primary operational and financial measures and demonstrates our ability to manage sell rates to customers with our ability to concentrate and leverage our purchasing power through effective consolidation of shipments from multiple customers utilizing a variety of transportation carriers and optimal routings.

To be clear, this isn’t a “here’s our earnings, except for all the expenses that matter” type of non-GAAP measure; this is how they view their own top line internally. This is closer to a gross profit measure. It gives them, they feel, a more apples-to-apples view of services versus freight. The large bonuses that are attainable by employees are largely based off net revenues, so it is a very important internal number and salaries are highly correlated to net revenues. Salaries as a percentage of net revenues has remained remarkably steady at 53-55% for years now.

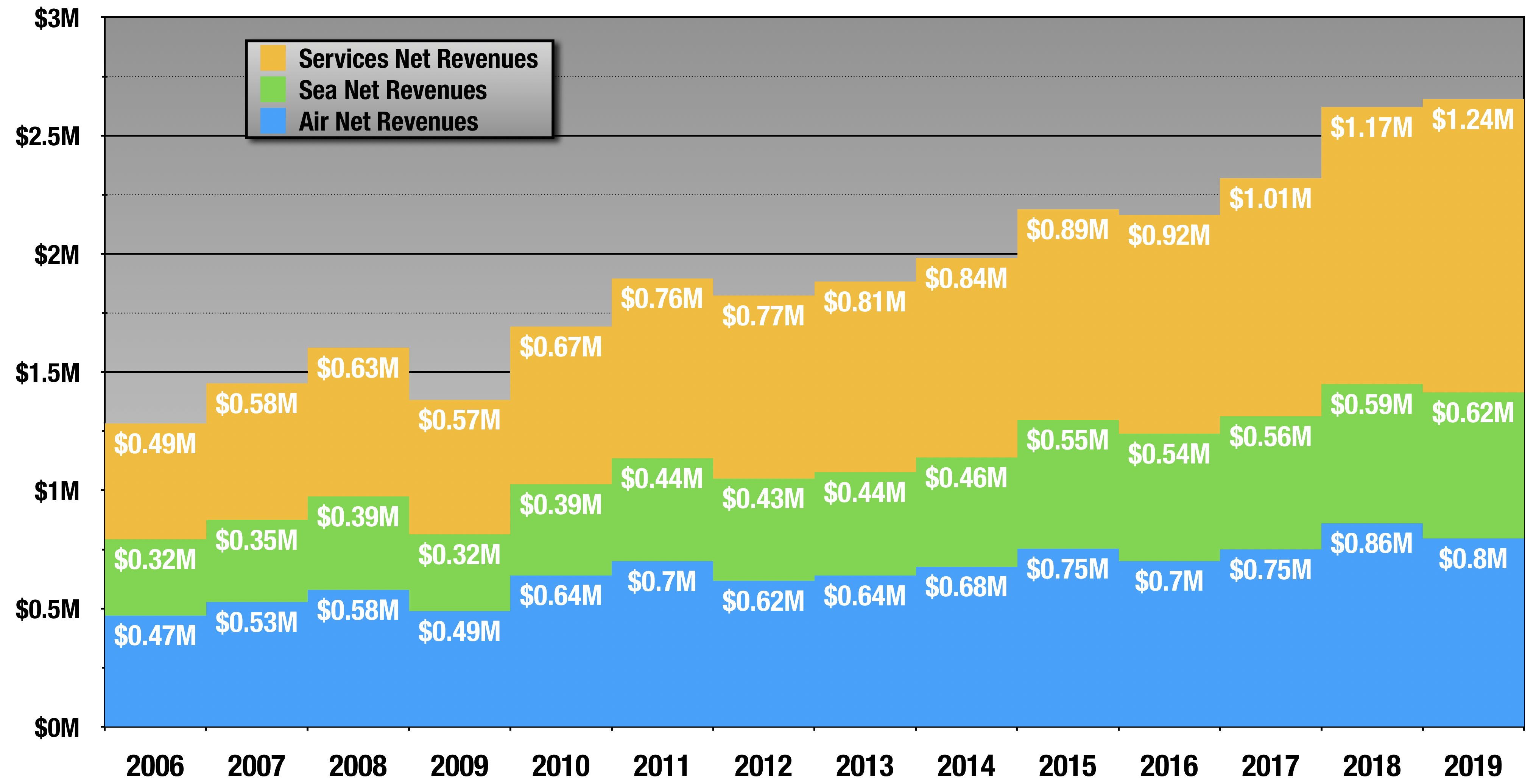

Now let’s look at some trends in the three sources of net revenue. First, we will look at the net revenues accounted for by each source over time. The 2019 number is the first three quarters of 2019 annualized, but likely those will come in smaller after Q4 is reported.

Company filings.

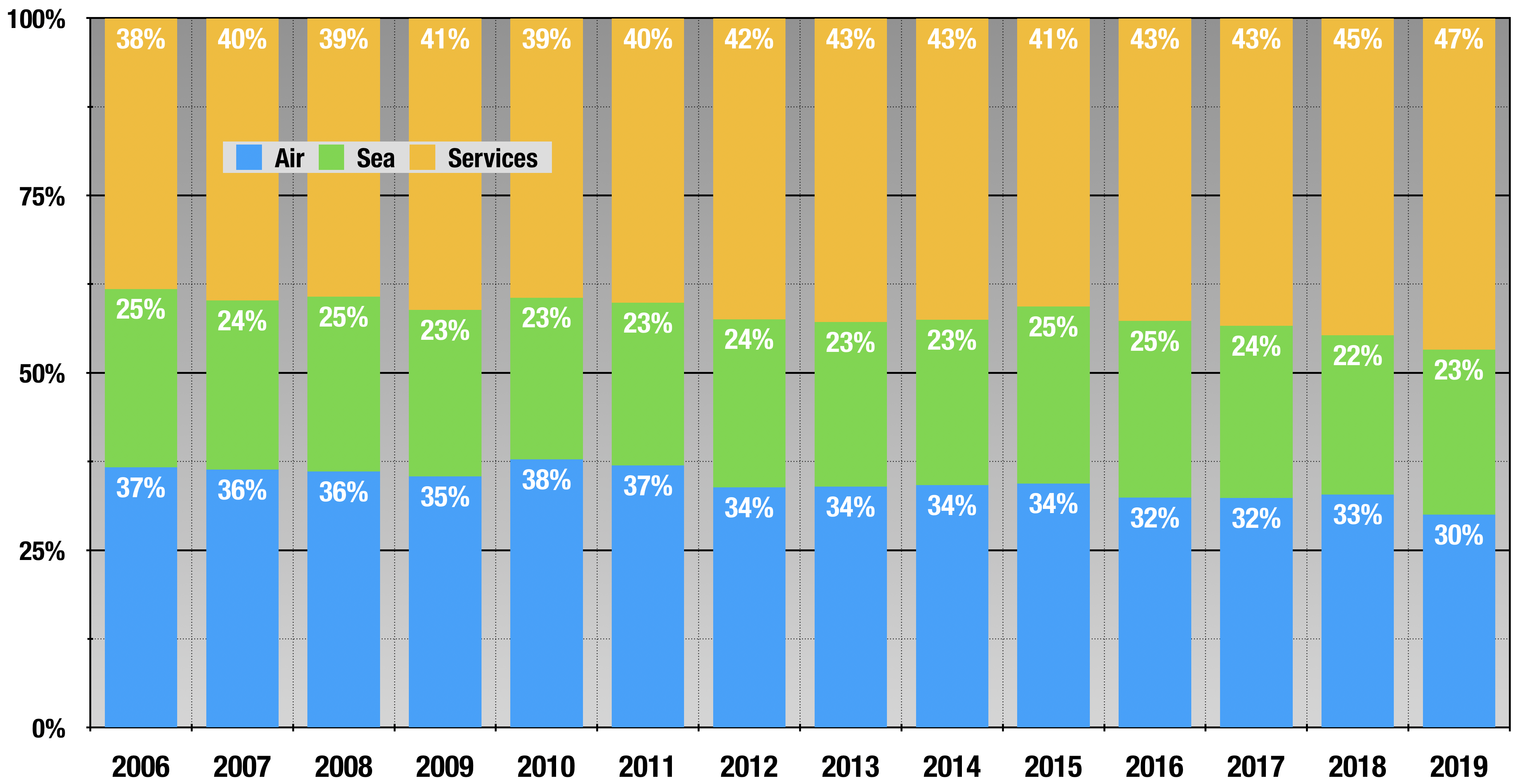

We see steady growth all around until 2019. As you can tell, Services have become more important to their top line. Percent of total net revenues:

Company filings.

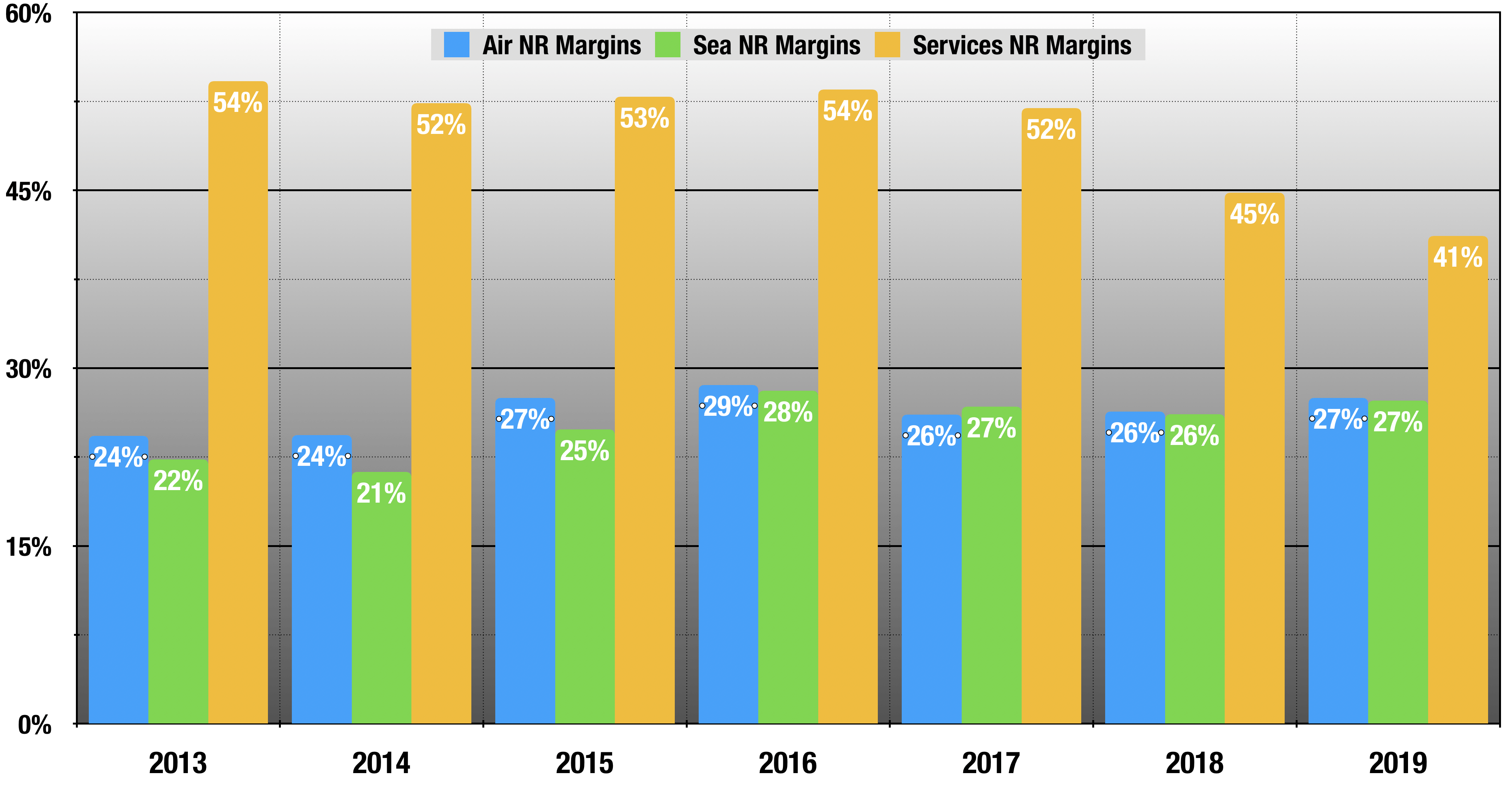

On top of that, the margins on services are much fatter, but they have been declining, and this is one big source of their poor performance:

Company filings.

I don’t have any explanation for the drop in services margins. In their 2018 Q&A, they put it on product mix alone, but have not updated on the further erosion here.

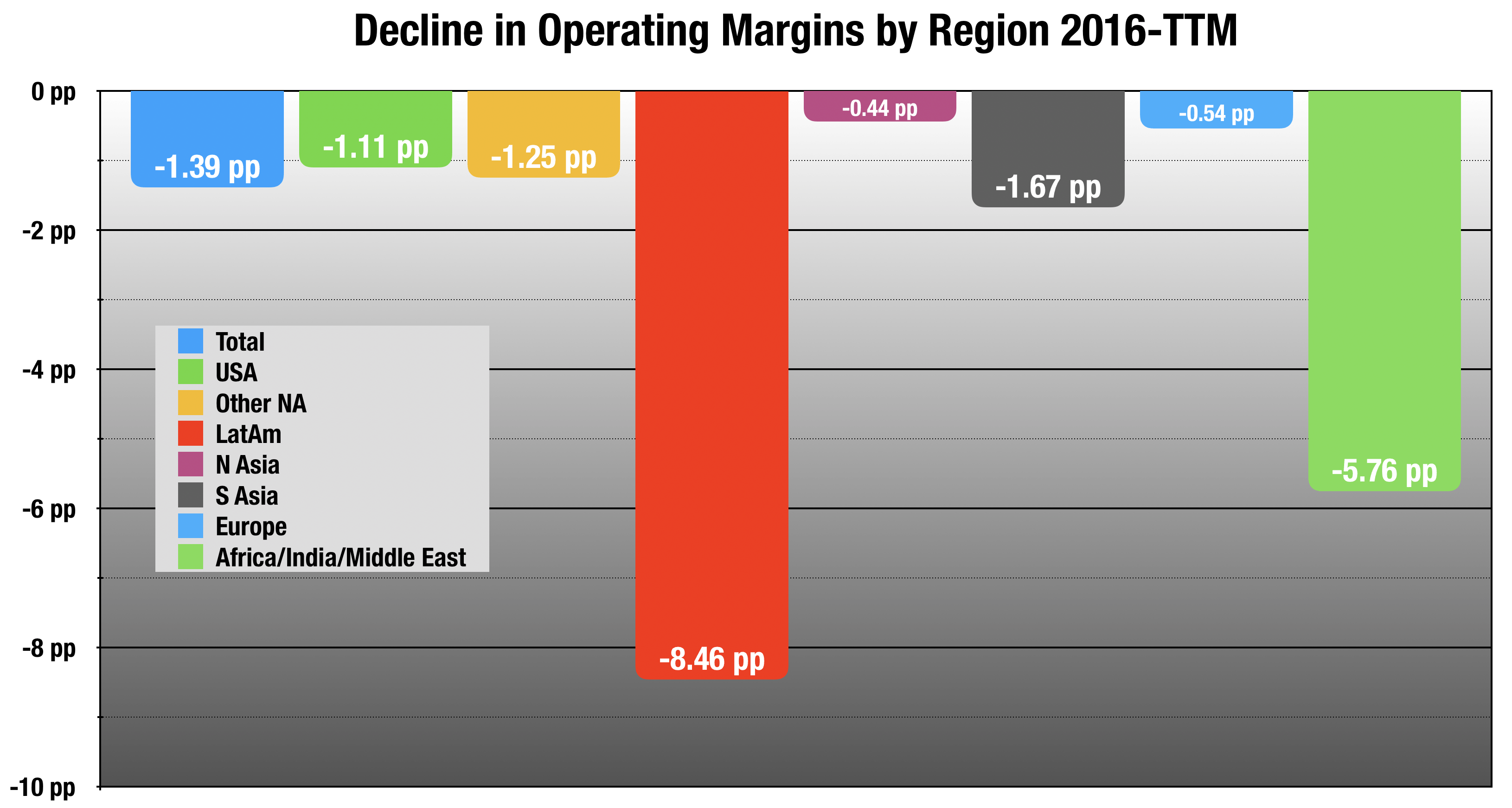

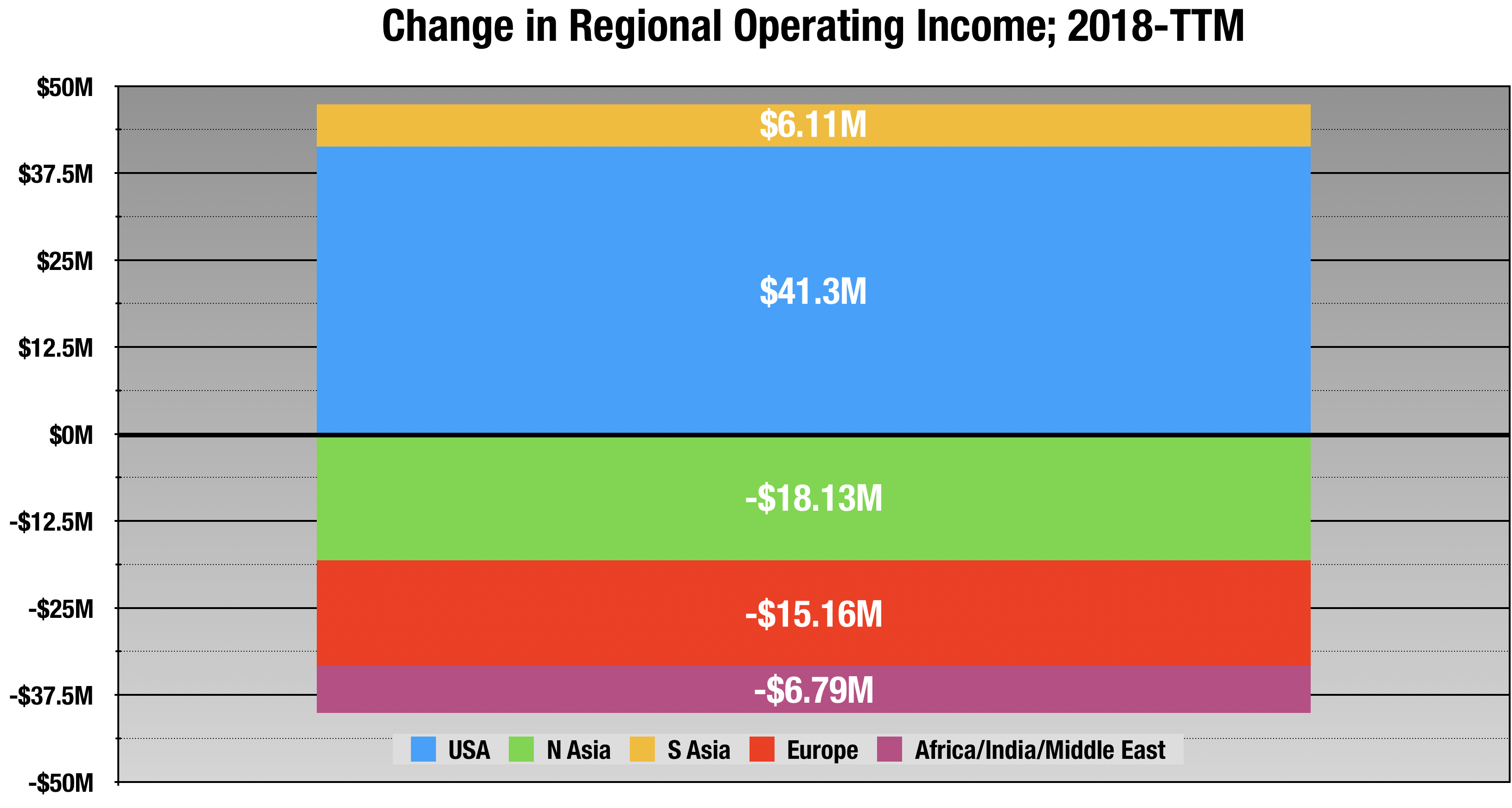

The result is declining operating margins in every region:

Company filings.

Interestingly, their smallest declines come in the two regions they are having the most problems with: North Asia (mostly China), and Europe. Another sign of hustle.

The two smallest regional contributors to the change in operating income, Other North America and Latin America, are not in chart. They basically offset each other and net to $0.5 million. Company filings.

The two smallest regional contributors to the change in operating income, Other North America and Latin America, are not in chart. They basically offset each other and net to $0.5 million. Company filings.

As you can see, some trade has shifted from China (North Asia) to South Asia. But the only thing keeping them afloat through Q3 was the US, and my guess on the new guidance is that their operating income is way down there in Q4.

So the company is in rough seas now. Let’s look at how they handled earlier downturns.

Risk Factors: Almost Everything

As I alluded to earlier, Expeditors is open to just about every macro headwind there is except for interest rates (did I mention: zero debt?). Some of the major ones:

- Forex: Most of Expeditors’ revenue comes from overseas and this has always been the case.

- Trade: Obviously.

- Global recession: Obviously.

- Oil price shocks: the consolidated prices they pay for sea and air freight can rise sharply with the price of oil. Additionally, changes to international shipping regulations on diesel fuel that take effect in 2019 will raise their costs there.

So Expeditors is a bit like a boat at sea, being blown this way and that by the changing winds. Their strategy for dealing with this has always been to rely on their mangers in far-flung places to navigate these headwinds, with corporate support for whatever course they set upon. This is where their unique HR and compensation system come into effect. Local managers are highly motivated to bring their net revenue up, or their personal earnings will suffer, not just now, but in the future. The company believes that these managers, properly motivated and attuned to local conditions, business culture and environment, are the best weapon against the unpredictable.

It sounds great in theory, but how does it work in practice? The short answer is that they can take big hits during crises, but because managers are highly motivated to make up for past losses, the recoveries are quite dramatic. Let’s look at two case studies: the 2009 collapse in global trade, and the Dollar Index rising to 113 in 2002.

Case Study: 2009 Global Trade Collapse

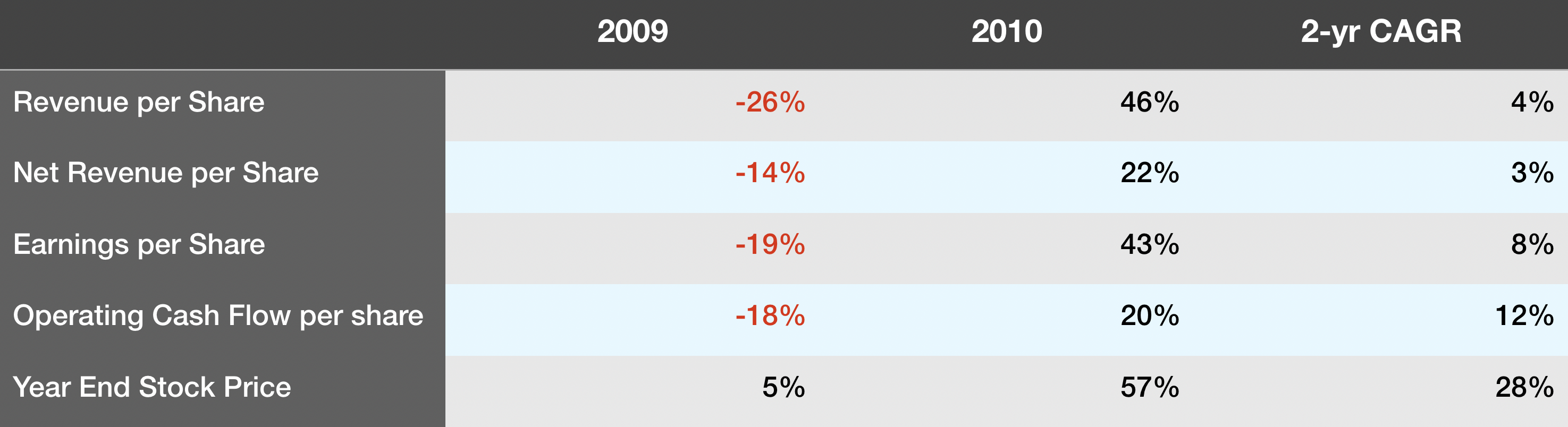

According to the WTO, in 2009, global trade was down 20% from 2008, then back up 19% the following year. How did Expeditors handle that mess, with a global financial meltdown thrown in to the mix? They took it on the chin in 2009, but their recovery in 2010 is even more eye-popping.

Company filings.

The worst recession in our lifetime, and the stock price has a 28% CAGR.

For some more color on 2009, let’s turn to the Annual Report. From Pete Rose:

David Frost had a program in the 1960s called “TWTWTW” “That WasTheWeekThatWas.” We have the longer version now, which is TWTYTW. Never in all my years had I witnessed a business disaster until now. Fortunately we saw what lay ahead in the latter part of 2008 and made some critical decisions. We instituted a hiring freeze, cut expenses, and implemented a policy of no layoffs. This should stand us in good stead when things turn around. On the positive side we have lots of cash, no long-term debt and we’re profitable. Yes, revenues are down, but whose aren’t? Just to get through the year unscathed was a modest victory…

What about 2010? It certainly couldn’t get worse, or could it? Unemployment (in the United States) is at record levels, the dollar (in the United States) is weak, and the national debt (in the United States) is in the trillions (remember when a million was a lot?). Taxes (in the United States) will be higher, health care (in the United States) is up in the air, and the economy (in the United States) drags along. Fortunately for us, we’re not just in the United States. We’re a global network, with 70% of our operational capabilities residing outside the United States. As the global economy starts to recover, we’re positioned to benefit from that recovery when and where it occurs. That isn’t to say we’re downplaying our U.S. presence. Historically, betting against the U.S. economy and its people has not been a winning proposition. We’re not economists, nor are we gamblers, but we are betting that there still remains a lot of strength and stability in the U.S. markets. While there may be some short-term trauma, in the long run the U.S. economy will be fine. We’re merely pointing out that the U.S. is just one of many nodes in our global network and that some of those nodes are recovering faster than others. We believe our long-term future well-being will have as much to do with how other countries recover from the turbulence of the last 18 months than what will happen solely in the United States.

He couldn’t have been more right.

Data by YCharts

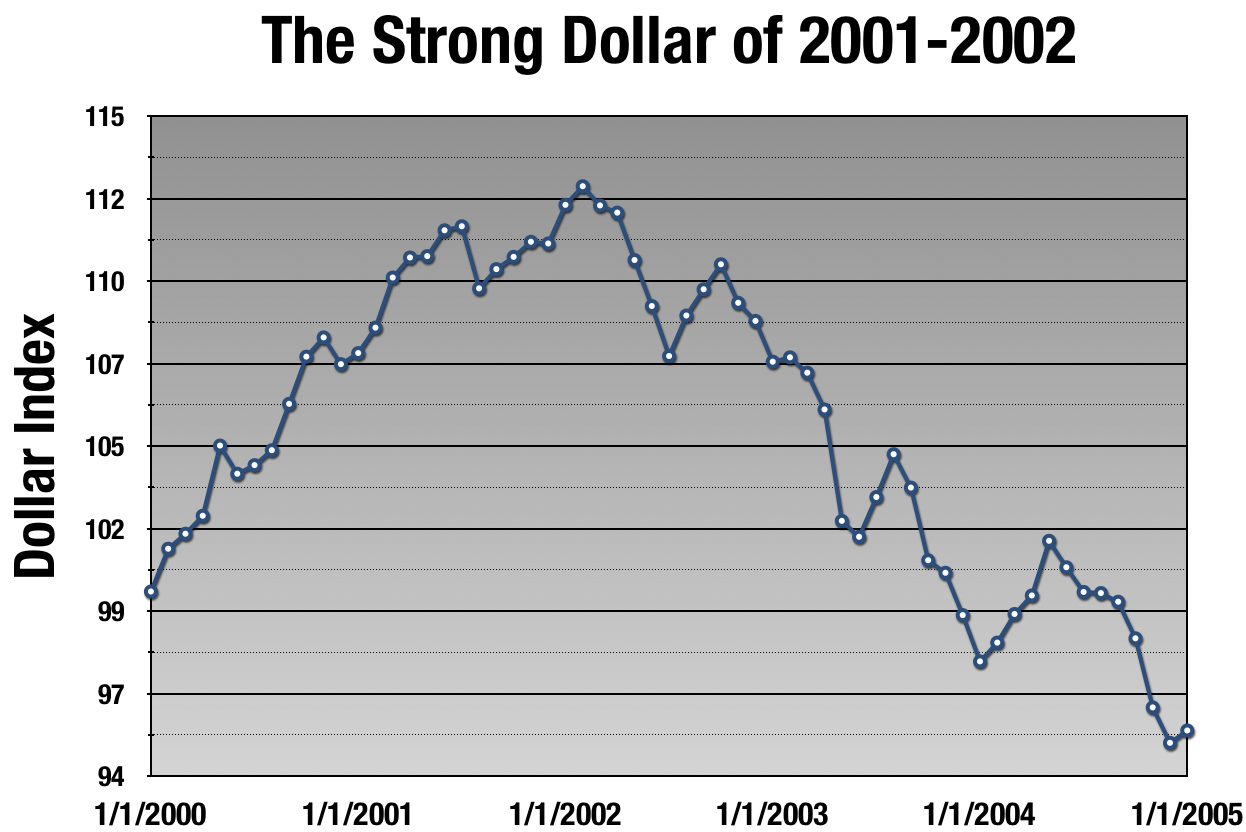

Data by YChartsCase Study: The Strong Dollar of 2001-2002

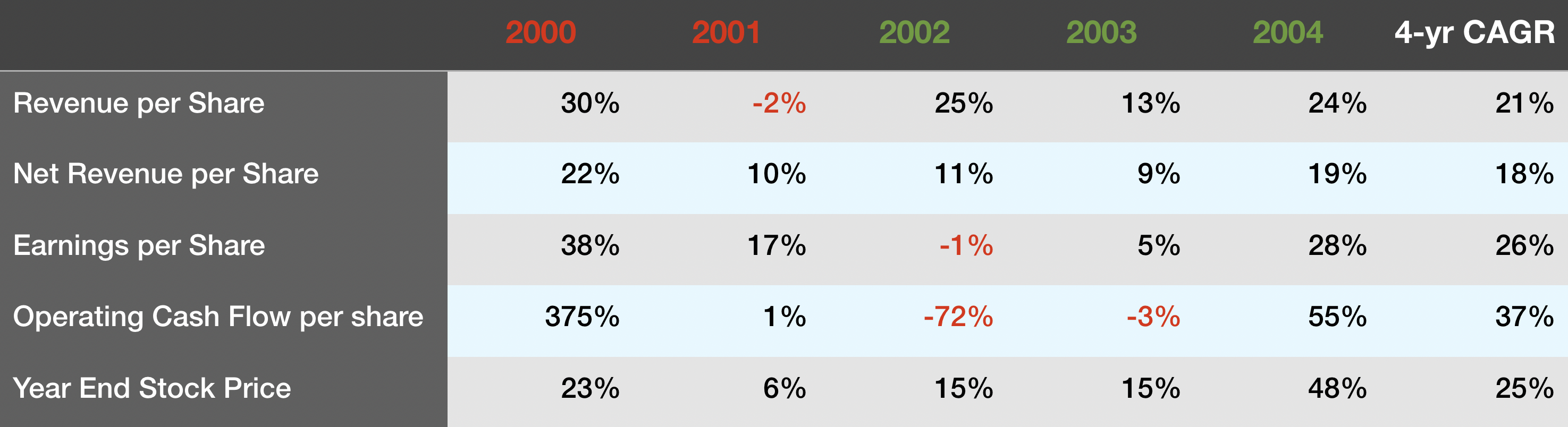

This was more of a slow-moving problem for Expeditors than our first case study, and like that one, it also coincided with a deep recession. In total, it took 5 years for this one to work itself out, roughly from January 2000 to December 2004.

Fortunately for our analysis, the Dollar Index peak happened in early February, 2002, so it coincides nicely with fiscal years.

Red Years = Rising Dollar; Green Years = Falling Dollar. Company filings.

Red Years = Rising Dollar; Green Years = Falling Dollar. Company filings.

We can see a similar, but lengthened pattern as the first case study. Overall, it was less of a problem than the 2009 collapse, and recovery was slower as macro conditions took a couple of years to correct. But 2 years after the peak in the dollar, Expeditors was certainly back in fine form. Importantly, neither net revenue nor the stock had a down year in this 5-year period, and there are small dividends added to that as well.

So, what to conclude from our case studies? That Expeditors takes their lumps, and comes back even stronger as macro headwinds clear. I believe the fact that managers cannot earn new bonuses until they’ve made up for previous losses is a huge factor here. They are doubly incentivized to maximize performance as the macro picture gets better. Their answer to every challenge is to lean into their people and culture. Some more color from Pete Rose:

Q: Wall Street has recently called your business model into question, given the uncertainty in the global economy and changes in airfreight capacity. How do you refute the claims that Expeditors’ business model, though previously highly successful, is now running an uphill battle?

A: If Wall Street did actually speak with a single voice, and if anyone were actually gifted enough to hear it, it seems odd that the voices would bother to question our business model. Our model has been marked by sticking to what we know and has been based upon sound business decisions, growth and profitability.

If you know Expeditors, you know that we are not about to alter what we do or how we do it merely to please Wall Street. To imply that we need to issue some kind of formal refutation of this questioning implies that we somehow have given credence to it.

We tire of trying to explain over and over again the soundness of our model. Frankly, we think we know more about our business than Wall Street does and if anyone doubts this fact, they should sell now and run from this stock. We acknowledge that “only time will tell” if the skeptics are correct and we are misplaced in our confidence. However, we offer the following observations in support of our position:

- International trade is not going away.

- The asset based carriers, be they ocean or air, do not have the resources or the wherewithal to handle the arrangements for all shipper and shipments moving in international trade. Even if they had the desire, they are not in a position to add the personnel required to create a global network and make it happen. Most are struggling in their own right to maintain profitability.

- It takes properly deployed intellectual capital, supported by technology and communication expertise, to efficiently match assets in transit with assets available to transport and we have these resources.

Non-asset based logistics companies are the common denominator for the transportation industry. When flexibility is an issue, a logistics company is generally required.

It is a fact that at the present time the market has our stock at a 30% discount to the all time high reached less than six months ago. This is no doubt the sound that you are hearing. What you elect to make of it is up to you. In the meantime, we plan to be right here trying our best to make money rather than addressing the queries on behalf of those who hear voices.

Seriously, all his answers were like this.

Data by YCharts

Data by YChartsPhase One: Or Why Bilateralism Failed

I have mostly avoided talking about the Phase One trade agreement until I saw a text, but even now I have more questions than answers. Mostly, they have to do with how this deal is enforced, and what Chinese incentives are.

In the 1980s, multilateral trade agreements began becoming the norm, rather than the exception. There were good reasons why:

- It raised the costs of defecting from the agreement.

- Third-party dispute resolution.

- It lowered tariffs in more places at once, allowing capital to move to its most productive home.

The problem with multilateralism is that it is very difficult to get everyone on board with these agreements, and that takes years of hard work.

Those first two bullets are especially key for practical purposes. Bilateral agreements with no third-party dispute resolution are ultimately doomed to failure. Eventually, a dispute becomes large enough that no amount of bilateral discussion will solve it, and the plaintiff needs to seek remedy elsewhere. Defendants, who are almost always losers at the WTO, have generally applied the WTO remedy, or lived with the consequences. Most importantly, the whole deal does not fall apart over a single issue. For example, one of the Chinese “concessions” was to abide by a WTO ruling on tariff-rare quotas, something they had already acceded to in 2019 after the ruling.

I need some more time with it, and some discussion with trade law experts, which I most certainly am not. But my initial reading is that there are a lot of promises that are entirely undergirded by Chinese willingness to cooperate; the downside of defection seems weak.

The enforcement mechanism is long on detail, but short on substance. I can sum it up pretty quickly. For the hard stuff, the US Trade Representative and the Chinese Vice Premiere talk. There’s no hard time limit to how long these talks will go on for, nor what happens to the rest of the deal if one side decides to call fruitless talks off and take unilateral retaliation.

It’s a text that seems ripe for cheating and bogus claims that drag on for many months. With regimes that are proven liars like the Chinese and Iranians, I always ask myself: if I wanted to look like I wanted to abide by this agreement, but not really, how would I do that? With the Iranian Nuclear Deal, it was difficult to come up with much — multilateralism at work again. With this deal, there are holes big enough to drive a truck through. For example, Article 6.2.5:

The Parties acknowledge that purchases will be made at market prices based on commercial considerations and that market conditions, particularly in the case of agricultural goods, may dictate the timing of purchases within any given year.

That indicates to me that the Chinese can keep saying “Brazil is cheaper” until the end of the year before dispute resolution even kicks in. Trump may have lost an election by then.

This type of thing is all over the place. My best guess is that the Chinese need some energy and agricultural products, especially pork bellies. Quite conveniently, there is a glut of pork bellies, and they are cheap right now.

They will buy what they need, enough to give Trump a short-term “win” and reassess what their needs are come summer/fall. But that gives them, and the rest of us, a respite from the trajectory we were on, at least through Election Day.

Finally, but by no means unimportant, the deal does nothing to address the metals tariffs, which are having the largest effects on US manufacturers.

I Come to Praise Expeditors, Not to Bury It

If you can’t tell, I like this company a lot, and it would have remained a core part of my portfolio had not all this happened. But it did.

But Phase One is still good news for Expeditors. At a bare minimum, it looks like further escalation is off the table through Election Day. If the Chinese live up to even some of their commitments, it could be a real boon to the US operation. I remain skeptical, but always hopeful I am wrong.

Moreover, as we’ve seen, Expeditors has a history of overperforming during periods of macro challenge, and then bouncing back strong once they clear. But clouds haven’t cleared yet.

So I’m going to remain cautious here and wait for the Q4 report for a little more detail on where the problems were. If it is, as I fear, a large downswing in the US operation, that will likely turn me off. We should see something the first week of February, and I will update then.

I am going to keep my Bullish call on this one, because long term, I am always bullish on Expeditors.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.