FG Trade/E+ via Getty Images

After weeks of unsuccessful diplomatic operations, an unfortunate and complex sequence of geopolitical events has escalated to the point of no return. In the early morning hours of February the 24th, Russian troops have crossed the border and have begun large-scale military operations marking the beginning of the invasion of Ukraine and a new war in Europe.

In response to the invasion, the United States and the European Union have issued unprecedented and never-before-seen sanctions targeting the Russian economy. The sanctions have seen billions in Russian equities simply erased from the markets as investors flee to safe havens in fear of further sanctions.

In the middle of everything, a small and very interesting group of “Russian” companies seemed to have circumnavigated the regulators and have successfully avoided any sanctions up until this point. The largest amongst them is the steel and mining giant Evraz (OTCPK:EVRZF). The share price of the company has been decimated and is down more than 90% year to date. In this article, we will take a deeper look into what makes Evraz so special and why this high-risk high-reward investment might end up becoming an unlikely winner of the Ukraine crisis.

How did it avoid sanctions?

Referring to the history of the company as complex would be putting things mildly. The story of Evraz only makes sense if one has a deeper understanding of the history and circumstances of the downfall of the Soviet Union and how Russia transitioned from state socialism to a system of cutthroat capitalism and ended up under the rule of kleptocrats and oligarchs.

In such circumstances, the company was initially founded as a small metal-trading business in the newly reformed Russia in 1992. Back then, the company went under the name “EvrazMetall”. In the following decades, the company has developed into a very successful vertically integrated steel and mining giant.

However, as is the case with capital, it is almost always in pursuit of safer heavens. The owners have decided to move the parent company into Luxembourg, registering it as a public company under the name of Evraz Group SA in 2004.

Its journey of becoming a “British” company began all the way back in 2005 when the then Evraz Group S.A. floated some 8.3 percent of its shares in the form of global depository receipts in London. The company was priced at $14.50 per GDR implying an equity value of $5.15 billion. An additional 6% stake was placed in January 2006. This resulted in a total free-float of 14.3%. This was part of a much larger movement of GDRs becoming premium London listings.

In 2011, a decision was made to fully move the parent company across the channel to London. A small “shell” company under the name of “Project Savannah PLC” was renamed into “Evraz PLC”, which acquired and exchanged the outstanding share capital of “Evraz S.A”. This is how a small Russian import business has become one of the largest British integrated steel and mining giants and so became the company we know today.

So the simple answer to “Why did it avoid sanctions” comes down to a simple fact, it is technically not a Russian company. If one had to summarize the situation in one sentence, the best way to put things would be to call the company British-based and Russian-owned. This is unlike dozens of other Russian-listed companies that we have seen sanctioned and suspended from trading, such as was the case with the likes of Gazprom(OTCPK:OGZPY), Lukoil(OTCPK:LUKOY), Rosneft(OTCPK:RNFTF), and others. However, the “Russian-owned” part is causing multiple problems as it is reflected in the share price.

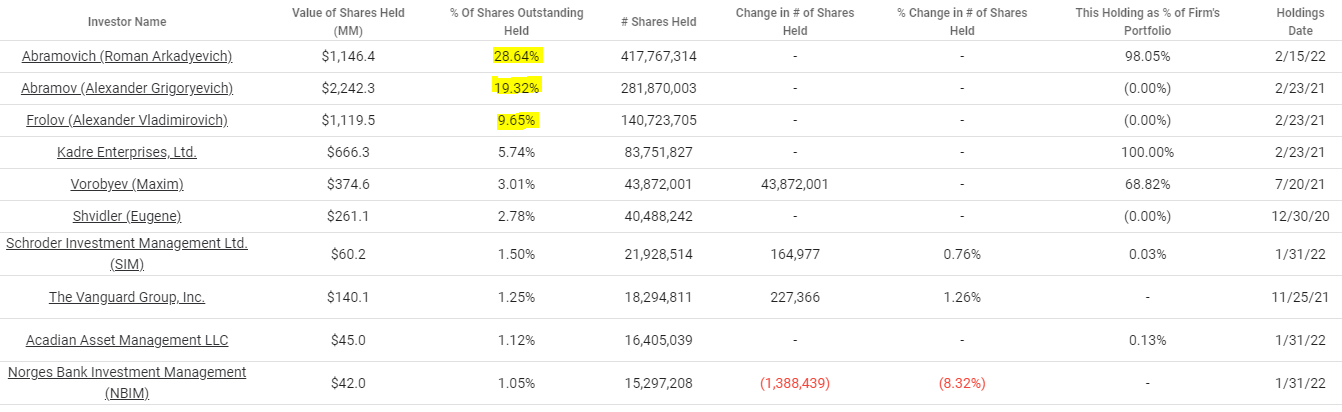

Ownership Structure (TIKR Terminal)

If we take a look at the current ownership structure of the company, we can see that Russian oligarchs own almost 60% of the shares outstanding. The first among them with a 29% stake in the company is Roman Abramovich, a Kremlin insider best known for being the owner of the Chelsea Football Club. With pressures over the sanctions rising, they seemed to have had a “change of heart” in relation to supporting the official Moscow politics. Most notable, Abramovich has decided to sell Chelsea and donate all of the proceeds to the victims of the war in Ukraine. Similarly, his daughter went on social to publically criticize the conflict in Ukraine and voiced her opposition to Vladimir Putin. The PR campaign can be seen as a sign that the oligarch believes there is a good chance for him to remain sanction free and to hold his claim on Evraz.

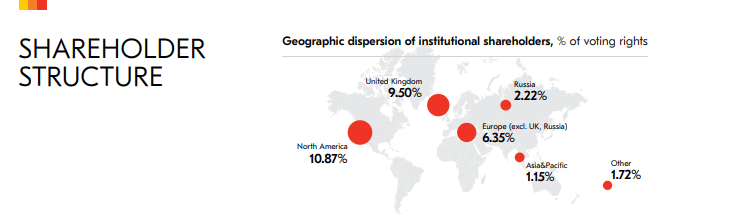

Even if sanctions end up being enacted, I see a good possibility of them personally targeting the oligarchs, either by freezing their assets or otherwise cutting their influence in the company. Further to the point, most of the free float of the company is actually owned by institutions with limited ties to Russia. According to the 2021 annual report, only 0.2% of institutional ownership of Evraz is Russian.

Institutional Shareholders (Annual Report)

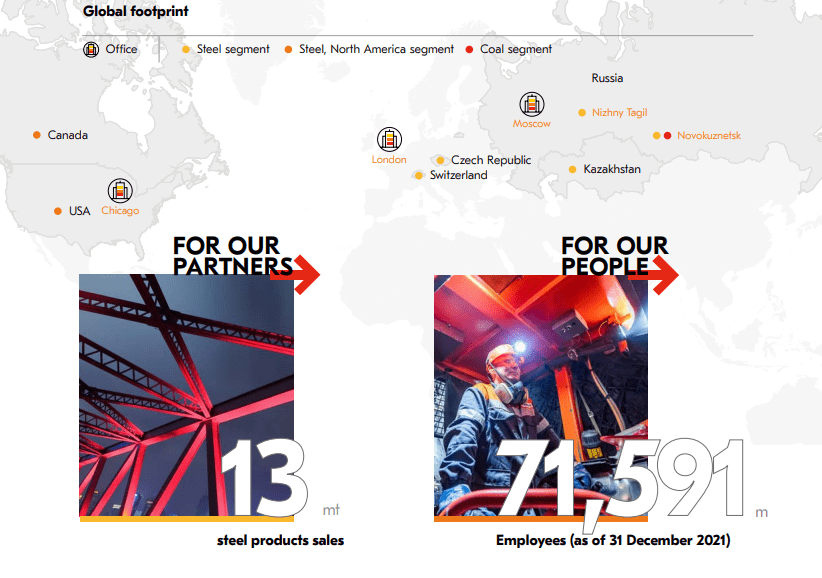

Another good reason why sanctioning Evraz might not be in the best interest of the Western authorities is that the company is a lot better geographically diversified than many would think. Evraz has operations mainly in Russia, but also in Kazakhstan, Switzerland, the Czech Republic, and most notably the United States and Canada.

Evraz operates three steelmaking facilities in North America: a 1.1-million-tons-per-year plant in Pueblo, Colorado; an 840,000-tons-per-year plant in Portland, Oregon; and a 1.2-million-tons-per-year plant in Regina, Saskatchewan. Sanctioning Evraz directly would jeopardize thousands of jobs and millions of businesses, which is obviously not in the best interest of the authorities. The North American operations themselves are home to around 4000 jobs.

Geographic Diversification (2021 Annual Report)

To summarize why I believe there is a good chance for Evraz to be able to avoid any meaningful sanctions:

- It is, in the end, technically a “British multinational company”.

- Sanctions are much more likely to target high-profile Russian oligarchs.

- Most of the free float of the company is held by institutions with no ties to Russia.

- Its underlying assets are more geographically diversified than many people would assume.

Why is Evraz so interesting?

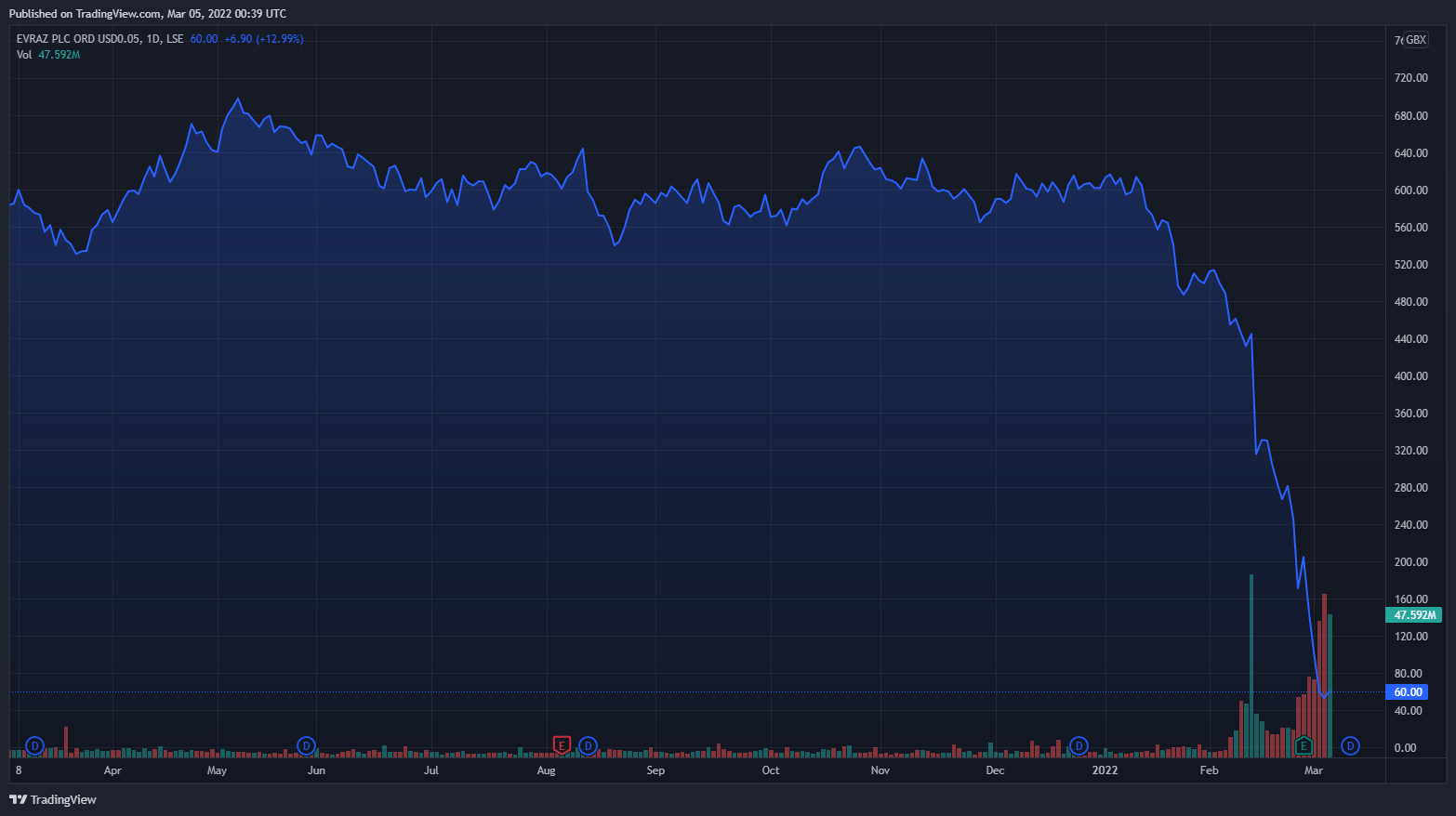

Evraz is a very successful steel and mining company that has seen its share price decimated. It has one of the worst track records of the year with the stock price being down by more than 90% year to date. However, other than the reputational impact and the direct exposure to Russia via its subsidiaries, fundamentally it is still a very successful company.

Evraz Stock Price (TradingView)

Shares of the company can be purchased on the main London listing, the secondary Frankfurt listing, or as an over-the-counter stock in the US. If we use the Frankfurt listing as an example, the stock went from trading at 7.5e per share to a 52 week low of 0.65e per share on March the 2nd. This wouldn’t be all that interesting if the stock isn’t going ex-dividend on the 10th of March, paying out a dividend of 0.45e per share. If paid out, the March dividend itself would cover almost 70% of the investment.

Evraz is reported to be sitting on $1.02 billion in cash, so making the payment should not be an issue financially. However, it is highly questionable if the dividend will end up getting paid out or if it will end up being deferred in the upcoming days due to the current situation and the ongoing crisis.

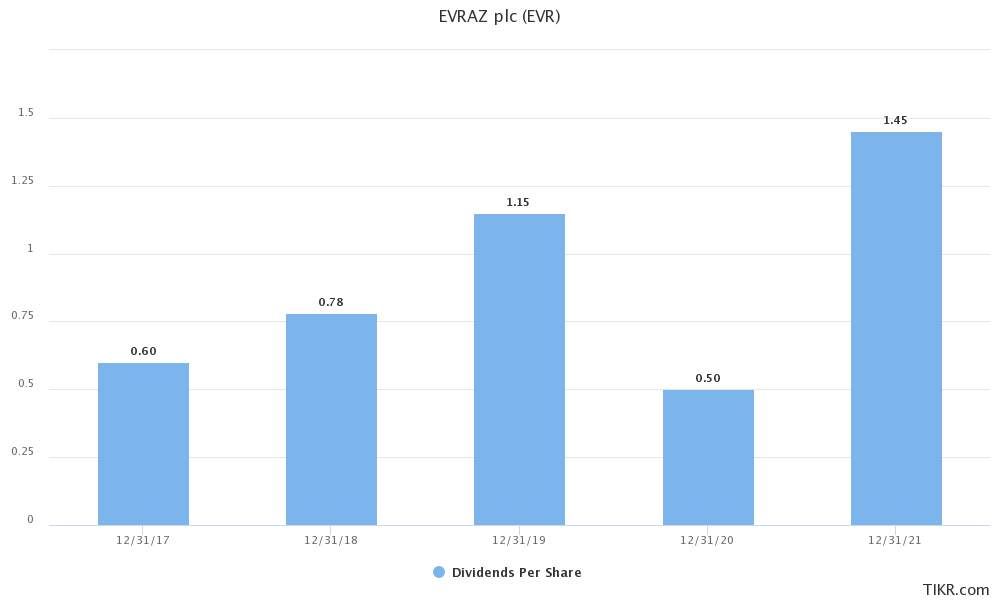

The company has long held a dividend policy of paying out a minimum of $300 million annually provided that the net leverage ratio remains below 3.0x. Evraz maintained an average dividend of $0.90 per share throughout the last five years. Given the current price, the dividend yield would be 70% if another yearly average dividend managed to get paid out. If they end up keeping in line with the policy, that would result in a dividend yield of 20%.

Dividend History (TIKR Terminal)

In this context, it would be interesting to take a look at Polymetal International PLC (OTCPK:POYYF) (OTCPK:AUCOY), another mining company that is structured in a relatively similar way to Evraz and has as well managed to avoid sanctions up until this point. The company does have a smaller direct exposure to Russia, but also the added complication of being listed on the Moscow Stock Exchange.

Polymetal had the added inconvenience of having to host their Q4 earnings call on the 2nd of March. Most of the questions have been associated one way or another with dividends or otherwise sanctions, so I would recommend giving it a read.

Now having reiterated production guidance and suspended cost guidance, I’m pleased to say that we maintain our commitment to adhere to the previously announced carbon footprint reduction trajectory, which calls for the reduction by 30% by 2030. And we continue to plan to release our long-term GHG reduction goals by the end of the year. And in terms of the outlook, last but not least, we currently plan to pay a regular annual dividend. And this will come for approval at the AGM at the end of April, to be paid by the end of May. However, citing again the aforementioned uncertainties, the management and the Board reserve the right to exercise judgment and discretion to postpone or partially postpone or cancel the dividend if the political and sanction situation changes significantly.

SWIFT is irrelevant for the physical ability to move funds. So switching off SWIFT — switching Russian banks off SWIFT doesn’t make transactions impossible. It just makes them much more expensive in terms of transaction costs, so money still can be moved around. While we are being very cautious about the ability to pay dividends, this is not really about our ability to move money. This is more about the risk of increasing capital controls in Russia and the potential disconnect between the global gold price and the domestic gold price or, in general, a further tightening of the sanctions, which would lead to more significant trade bans or logistical challenges. So this is, in essence, the risks and uncertainties which underpin our cautious approach to dividends. In terms of liquidity and current ability to move money, this is not an issue.

Q4 Earnings Call – Vitaly Nesis, CEO

The main issue as outlined by management is the long-term ability to pay out dividends by the Russian-based subsidiaries, considering that they are currently banned from paying dividends to offshore shareholders. The bottom line is that the company believes it is technically able to and is planning to maintain its current dividend payout plans. Furthermore, management stated they believe it is unlikely that they will come under the impact of direct sanctions, but do believe sanctions overall can have a negative impact on the business. It is possibly not unreasonable to expect that a relatively similar situation is ongoing within Evraz as well.

Back to fundamentals

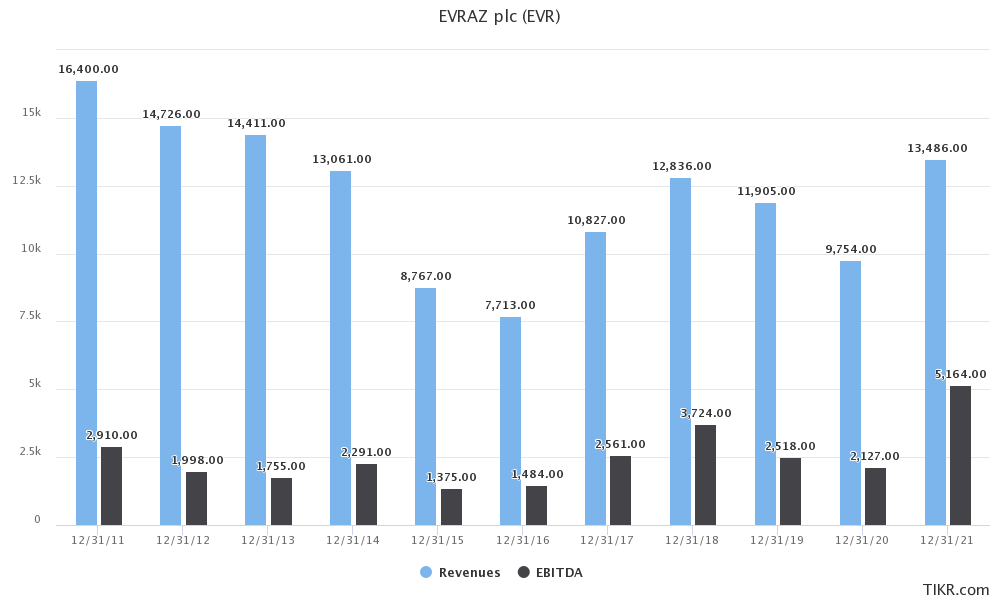

Evraz is an endurable, well-structured, low debt, free cash flow dividend-oriented machine that is only suffering from geopolitical tensions. In my view, it is fundamentally a very strong company. Primarily as a steel and iron ore producer, it is highly dependent on commodity prices. However, it has been shown over the years that it is well-positioned to benefit when steel and vanadium prices are high. Such was the case in 2021 when the group delivered its best results in seven years.

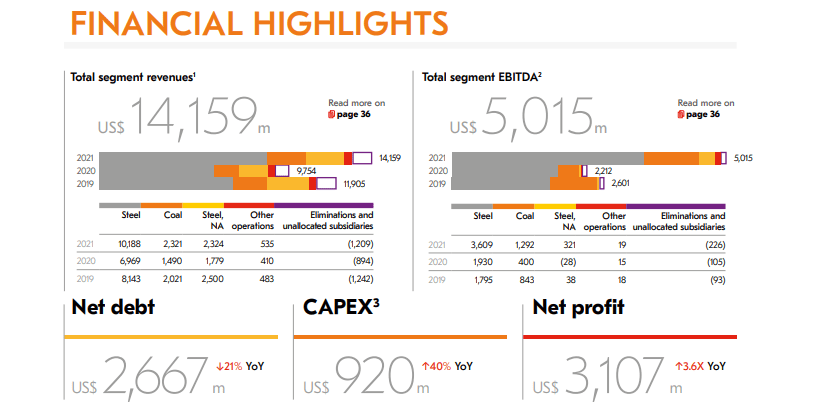

Financial Highlights (Annual Report 2021)

In 2021, Evraz’s total segment revenues climbed by 45.2% YoY to $14,15 billion, compared with $9.75 billion in 2020. The increase was caused primarily by higher sales prices for semi-finished and construction products, as well as greater volumes for vanadium products. This increase was also attributable to higher average realized prices and third-party sales for coal.

The Group’s total segment EBITDA amounted to $5,01 billion during the period, compared with $2,21 billion in 2020, boosting the EBITDA margin from 22.7% to 35.4%. The increase in EBITDA was primarily attributable to higher steel, vanadium, and coal product sales prices.

Revenues and EBITDA (TIKR Terminal)

Coal revenues made up a total of $2.32 billion in revenues for 2021, which amounts to about 16% of total revenues. This is important to note since the company has decided to divest its coal assets with this no longer being a source of income in the future. The demerger of the coal assets might be carried out by distributing the shares which Evraz directly holds in Raspadskaya, being about 90% of the total, to all Evraz shareholders in proportion to their existing shareholdings in Evraz.

Raspadskaya currently provides approximately 70% of EVRAZ metallurgical coal supply requirements needed to support its operations. In order for such supplies to continue 2 EVRAZ steel mills, Evraz and Raspadskaya had entered into two 5-year supply contracts, securing approximately 60% of EVRAZ coal supply. While EVRAZ remaining coal supply will be tendered on an arms’ length basis from a variety of suppliers.

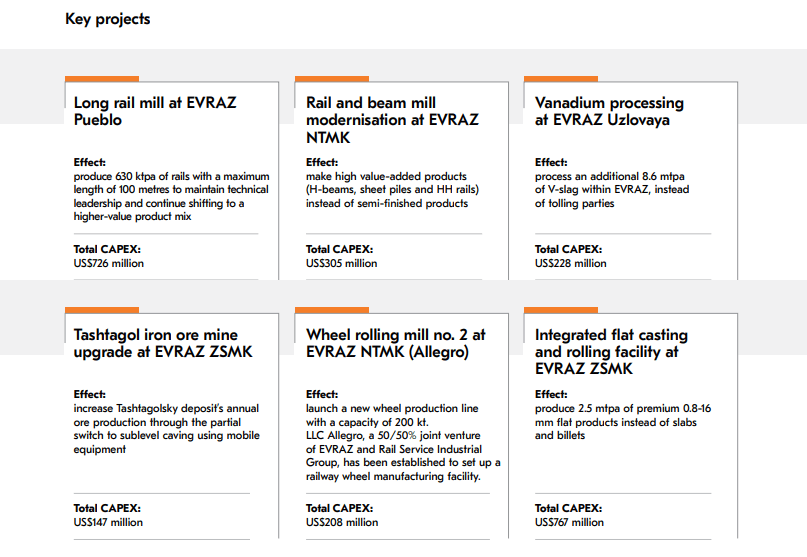

Future Projects (Annual Report)

In the last year, the company invested a total of $920 million in CAPEX, of which $517 million was spent on maintenance projects and $403 million on development projects. Development CAPEX doubled year on year, mainly as a result of an increase in spending on key projects mainly focused on iron ore and steel production. Given the current political climate, it would be wise to point out that only the Evraz Pueblo project is a North America based project, while the other major steel and vanadium projects are all in various regions of Russia.

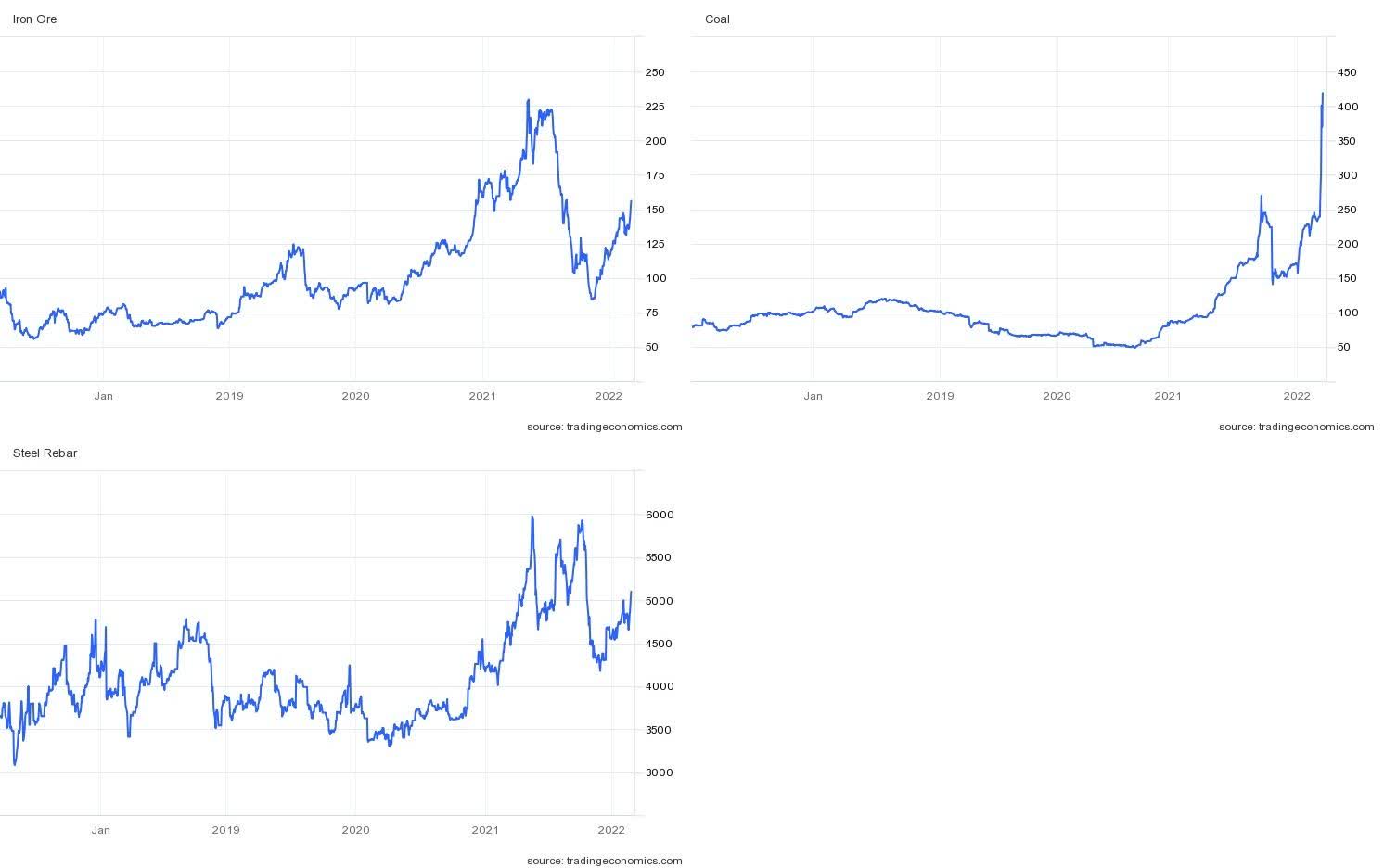

Commodity Prices (TradingEconomics)

Commodity prices have been soaring for several months already over supply chain issues and general fear caused by the crisis. Such is the case with steel and iron ore prices. In normal circumstances, Evraz would be brilliantly positioned to take advantage of this.

However, with a large portion of its operations still remaining within Russia and currently under the impact of sanctions, the financial outlook does look bleak unless the crisis can be deescalated in the following weeks or months. Furthermore, it is likely that the Russian subsidiaries’ inability to do business is in part causing the supply chain issues.

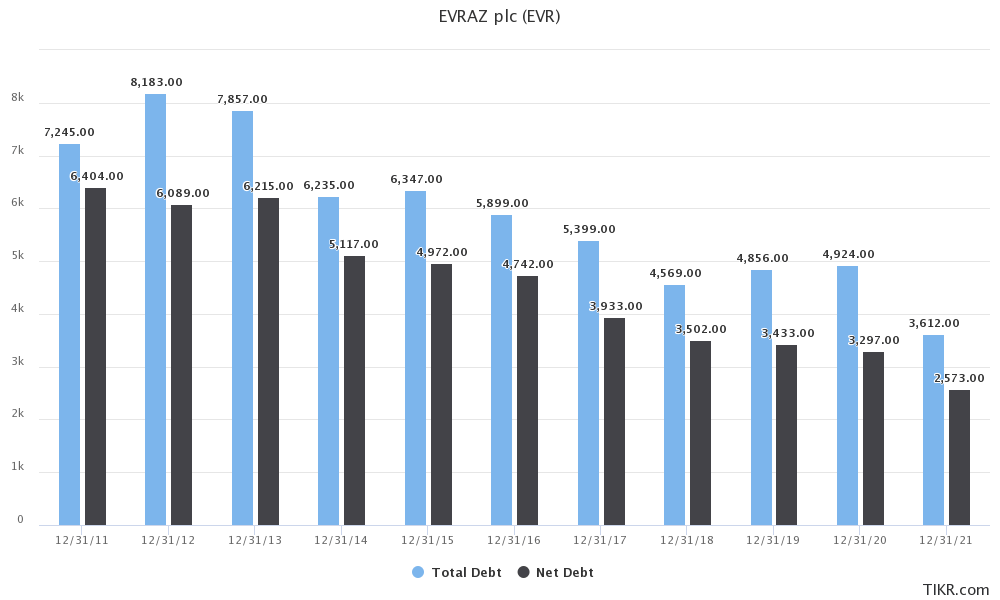

Total Debt and Net Debt (TIKR Terminal)

Currently, Evraz has $3.61 billion in total debt and $2.57 billion in net debt as they are sitting on some $1.02 billion in cash. We can see that the last decade has been marked with plenty of success in terms of deleveraging and that the company is finding itself in a very attractive financial position.

In 2021, the company has generated a solid free cash flow of $2,257 million. Coupled with the net debt/EBITDA ratio below 2.0x, which enabled EVRAZ to return $1,54 billion to its shareholders in the form of dividends for a dividend yield of 13%. Long term, the group is attempting to target a net debt level below $4.00 billion and a Net Debt/EBITDA ratio below 2.0x.

A very good case for Evraz could have been made even before the crisis has emerged when it traded north of 7e per share. Today, trading at as little as 0.65e per share, discussing fundamentals does seem a bit pointless, especially given that the crisis is changing things from the ground up.

Why this remains highly speculative

If the investment idea is something you are interested in, there are several different risks and major downsides associated with it that you need to understand before deciding to invest. In the end, this remains a highly speculative investment and should be treated as such.

- The majority of its operations are still based in Russia. The country is currently targeted by economic sanctions while being at war. If prolonged, the combination of the two is most definitely going to have a negative effect on the Evraz business.

- The scale of the sanctions remains unprecedented and it is unlikely that they will be able to endure for long. Unless de-escalation can be achieved, it is likely the Russian economy is going into a long period of isolation and depression.

- Evraz managed to circumnavigate all sanctions up until this point, but there are no guarantees that the company will not come under scrutiny in the upcoming weeks. Nobody knows the full extent and boundaries of the possible sanctions. Anything and including the company getting delisted from the exchanges remains a possibility.

- Russia’s response to the western imposed sanction still hasn’t been announced. It is possible that Evraz’s Russian-based subsidiaries will end up getting targeted by them.

- The stock price might come under heavy pressure as institutional investors liquidate their positions since the company is no longer meeting certain eligibility factors.

Final Thoughts and Conclusions

I find it very difficult to fundamentally analyze a company that has seen its share price decimated and is trading at one-tenth of the price from a point at which it was already considered a good value play. Evraz is an endurable, well-structured, low debt, free cash flow dividend-oriented machine that is only suffering from geopolitical tensions. However, the events over the last couple of weeks have shown that strong fundamentals mean nothing in the face of geopolitical risks and that emerging markets always carry a high level of political risk associated with them.

It all comes down to how long will the hostilities last and will the company get specifically targeted by British authorities. I am speculating that we will see an end to the hostilities over the course of the following weeks and the subsequent de-escalation of tensions. At the same time, I don’t find it likely that the authorities will end up targeting Evraz specifically. For the following reasons, I have found Evraz attractive enough to invest considering that I view the risk as asymmetrical.