Mlenny/iStock via Getty Images

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on May 28th, 2022.

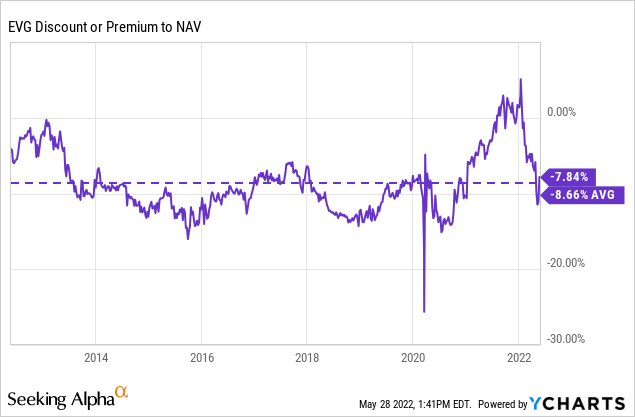

The last time we touched on Eaton Vance Short Duration Diversified Income Fund (NYSE:EVG), it traded at an unusually rich valuation. This was a rare sight for this fund since the last time the fund traded at a premium was back in 2007. Since that publication, the fund has come down quite significantly to an attractive discount. This has put the fund much closer to its longer-term average where it has traded previously. The overall fixed-income market has come down significantly, too, with higher interest rates.

A couple of factors pushed the fund to trade at a richer valuation. They had implemented a tender offer and enacted a managed 10% distribution plan. These were brought about as efforts to get shareholders to approve the merger with Morgan Stanley (MS). Since then, the tender offer has been completed, but the managed distribution plan is still in place. The higher yields generally get investors to bid up funds, whether it is earned or not.

While I don’t believe the current distribution can be earned still, the fund’s valuation makes it a much more tempting offer than where it was previously. There just has to be the realization that it is a slow liquidation of the fund with the current distribution plan. There isn’t anything wrong with that for some investors, either.

The other warning here would be that it seems that higher rates are now priced in. If rates start moving higher again and go higher than anticipated, there would be continued downside pressure for this fund.

The Basics

- 1-Year Z-score: -1.61

- Discount: 7.84%

- Distribution Yield: 11.21%

- Expense Ratio: 1.35%

- Leverage: 23.23%

- Managed Assets: $284.09 million

- Structure: Perpetual

EVG is a relatively simple fund; they “seek to provide a high level of current income.” The secondary objective is to “also seek capital appreciation to the extent consistent with its primary goal of high income.”

To do this, their investment policy is rather flexible as well. The fund “will invest at least 25% of its net assets in each of the following three investment categories: [i] senior, secured floating rate loans made to corporate and other business entities, which are typically rated below investment grade; [ii] bank deposits denominated in foreign currencies, debt obligations of foreign governmental and corporate issuers, including emerging market issuers, which are denominated in foreign currencies or U.S. dollars, and positions in foreign currencies; and [iii] mortgage-backed securities that are issued, backed or otherwise guaranteed by the U.S. Government or its agencies or instrumentalities or that are issued by private issuers.”

This essentially sets them up as a multi-sector bond fund approach where they can invest in just about any fixed-income asset. Additionally, it means they aren’t limited to just investing in U.S. positions.

A Look At The Fund’s Leverage

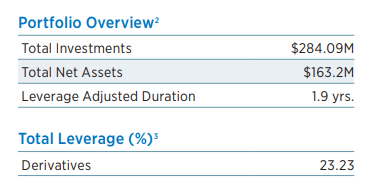

EVG is a small fund, as I’ve highlighted previously; it has only become smaller since the last time we covered it. At the end of Q1 2022, total assets are down to around $284 million and net assets at $163.2 million.

EVG Asset Stats (Eaton Vance)

Since that previous update, the fund’s leverage adjust duration has risen. On an absolute basis, it wasn’t a large leap from the 1.1 years prior. However, on a relative basis, that is quite the jump.

Speaking of changes, the fund’s leverage has also come down from the previous level, as shown above. One thing that is interesting to note here is that they only list the derivatives leverage. Derivatives, in this case, are through a plethora of instruments, including futures, options, interest rate and credit default swaps and forward foreign currency exchange contracts. Seemingly they are really going for the PIMCO approach of incorporating every type of derivative they can.

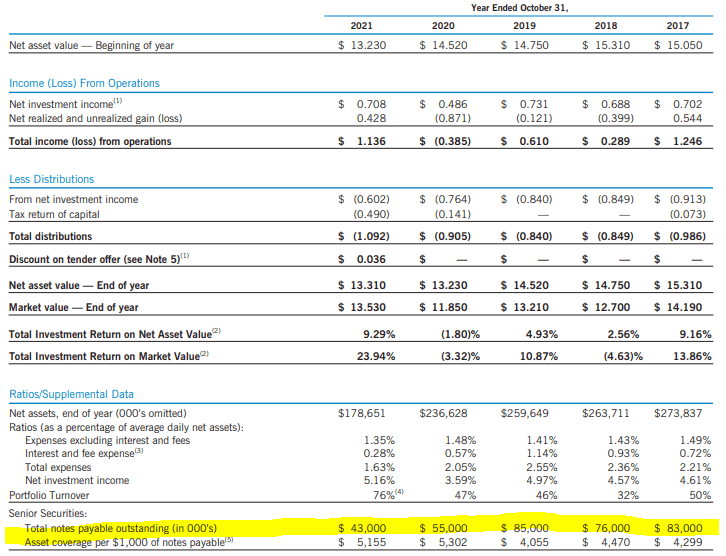

They had actual borrowings at the end of their last fiscal year, October 31st, 2021. They listed having $43 million in borrowings. This also seems to be represented when you take the fund’s total investments and subtract the total net assets; you arrive at $120.89 million. Here’s how they explain the difference between managed and net assets:

The Fund employs leverage through derivatives and borrowings. Total leverage is shown as a percentage of the Fund’s aggregate net assets plus the absolute notional value of long and short derivatives and borrowings outstanding.

In this case, I’m not sure why they aren’t showing borrowings unless they have taken this down to nothing at this time. Given that they often list borrowings in their Annual Report, it would suggest that borrowings should be listed.

EVG Annual Report (Eaton Vance (highlights from author))

In around a month, we should see a new Semi-Annual Report that can give us a better idea if they still have borrowings or if it really is just their derivatives.

One reason this is important is that their borrowings are based on floating rates, a spread above LIBOR. Their borrowing costs will also rise as rates rise, adding higher interest rate expenses. In the report above, we can see that the expense ratio came to 1.35%. When including interest expenses, it came to 1.63%.

In 2019, when rates were the highest in the last cycle, the fund’s total expense ratio was 2.55%. They had been reducing borrowings over the last few years, so it wouldn’t be completely surprising if they reduced it down to nothing for now.

Performance – Discount Opening Up

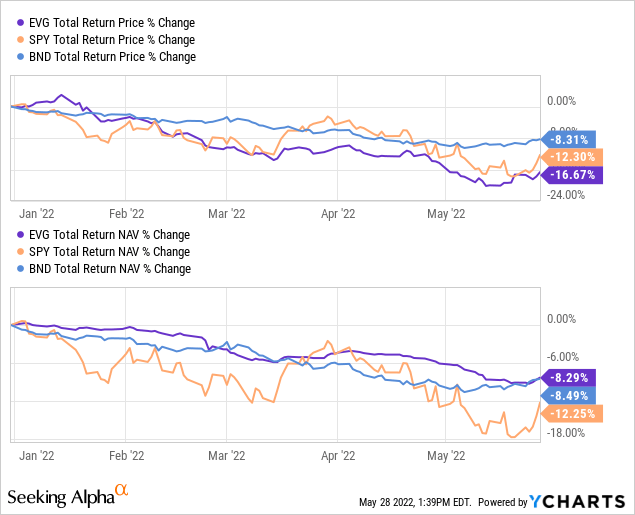

Despite the lower duration and the more complex portfolio, the fund has still fallen victim to the declines of 2022. To be fair, there haven’t been too many places to hide – besides energy and utilities. Using the SPDR S&P 500 (SPY) below simply for context.

I’ve also included the Vanguard Total Bond Market ETF (BND). EVG has only slightly outperformed that fund on a total NAV return basis despite BND’s 6.7-year duration. This seems to be where the leveraged approach of EVG is working against the fund.

YCharts

Where the more attractive part of EVG comes is that the fund’s total price return has fallen dramatically further. Of course, that opens up the opportunity that we often highlight with closed-end funds. Looking back at the last decade’s average, we are still trading above that level.

However, it is down considerably from last year’s peak. Given the entire fixed-income space is also lower, I still believe it is quite attractive to start an initial position.

YCharts

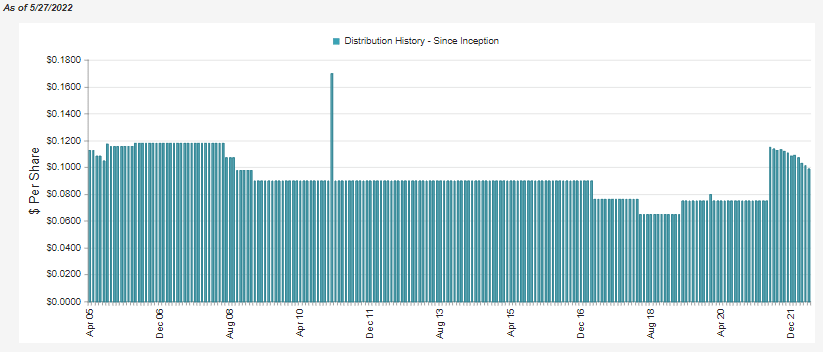

Distribution – 10% Managed Distribution Adjusted Monthly

As EVG’s NAV rises, the fund’s distribution should rise too. The distribution is adjusted monthly, so we can see this happen from month to month. Since the NAV generally hasn’t happened – and likely won’t happen – that means most months, we see declines.

EVG Distribution History (CEFConnect)

This is happening because no safe, reliable fixed-income investment can return 10% at this time, given the current interest rate environment. Of course, this could be offset if the underlying portfolio was appreciating. During an environment where interest rates are rising, that will put pressure on the price of the underlying portfolio. So that just isn’t going to be happening for now.

The fund’s portfolio is tilted with the heaviest weighting in senior loans. That should see it benefit from higher interest rates down the road; they should be some of the first to benefit. However, these are generally issued by below-investment-grade companies making them riskier.

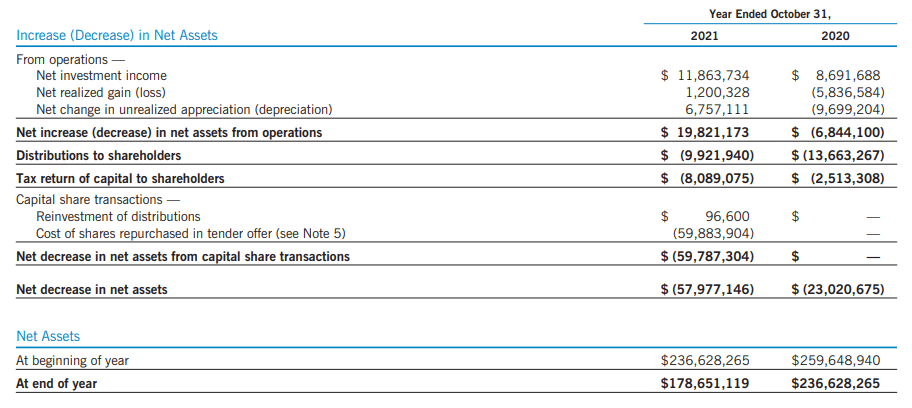

The fund’s net investment income was around $11.863 million in the last fiscal year.

EVG Annual Report (Eaton Vance)

Last month’s distribution was $0.0988 – with 13,417,575 shares outstanding, which would translate into needing over $15.9 million to maintain the current level. At some point, if rates rose high enough, this could happen. However, under the current market conditions, that just isn’t going to happen for now. That’s why it is a slow liquidation of the fund over time.

EVG’s Portfolio

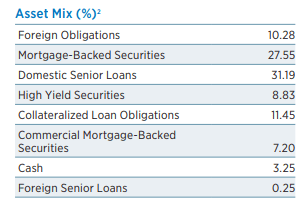

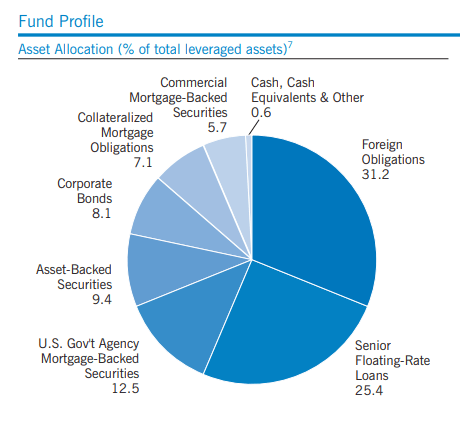

As mentioned, the fund’s heaviest weighting is in senior loans. This is then followed by mortgage-backed securities. After these two heavier weightings, it is fairly split between foreign obligations, high yield, and collateralized loan obligations.

EVG Asset Allocation (Eaton Vance)

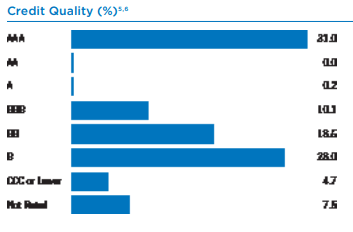

Taking a look at the portfolio’s credit quality, we can see that the largest allocation is to junk-rated debt. That is consistent with what we would expect from senior loans, high yield, and CLO investments. However, there is also a sizeable allocation to the AAA category. That’s occurring because the MBS they hold is coming from Agency MBS.

(Unfortunately, the below image quality is extremely poor. This is directly from their latest Fact Sheet.)

EVG Credit Quality (Eaton Vance)

It should be noted that the fund’s turnover is fairly high. Last year they reported a 76% turnover. That was the highest in the last five-year period. Given the fact that the allocation had gone up for floating-rate loans suggests they were trying to adjust their portfolio for the current environment. What is interesting is that with these changes, the duration still rose. I believe this is a function of the higher Agency MBS they have now shifted to as well.

Agency MBS has a lower duration relative to Treasuries and investment-grade corporate bonds, according to DoubleLine. However, relative to floating rate securities, it will be more interest-rate sensitive. DoubleLine noted that the duration for the Bloomberg US MBS Index was 5.18 years.

This turnover has actually resulted in sizeable shifts in the portfolio allocations. The above asset mix is as of March 31st, 2022. However, just going back six months prior – to the October 31st, 2021 Annual Report – gives us a fairly meaningful different breakdown.

EVG 10/31/2021 Asset Allocation (Eaton Vance)

The shorter duration of the fund should keep it less interest-rate sensitive. The duration had increased since our last update on the fund but is still rather low. The headwind that still exists for the fund going forward is if rates go higher than originally anticipated. We know the Fed is combating inflation, which has shown some signs of easing. That could bode well that the bulk of the damage is in for fixed-income. If they have to raise more aggressively, that will continue to pressure the fund.

Additionally, the fund’s heavier allocation to junk-rated holdings means that it is more sensitive to economic downturns. That is another real threat as some analysts believe the Fed won’t be able to raise without causing a recession.

Conclusion

EVG is certainly a more interesting investment than it was previously when it was more expensive. The fund’s discount has opened up, coming down from its premium previously. That alone makes it much more attractive. Then we can combine this with the overall declines, and I think it can make a compelling argument for an investment at today’s prices.

However, investors would have to be content with the fact that under the current environment, it is essentially owning a slow, self-liquidating fund. Until the portfolio can reliably start paying 10% yields (plus earning its expense ratio) from its underlying portfolio, the fund should expect lower and lower distribution over time due to eroding the fund.