Introduction

The biggest topic currently surrounding Energy Transfer (ET) is arguably whether their distributions will survive this downturn. My previous article on this topic discussed how their units are already priced for their distributions to be halved and thus investors should not necessarily fear this potential outcome. After publishing that article a new idea came to mind for an easy way for unitholders to essentially hedge and even potentially profit in the short to medium-term if they ultimately reduce their distributions. The beauty of this strategy is that it only utilizes their preferred units and investors have little downside risk regardless of the outcome.

Preferred Equity

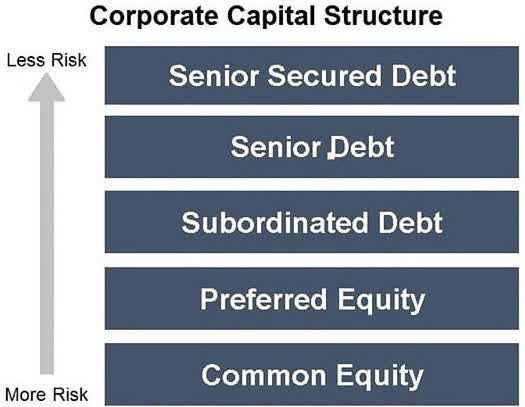

Since this strategy centers on their preferred units a simple overview of preferred equity for any new investors will be provided before going any further into the analysis. When reviewing any capital structure, the preferred equity always sits between their common equity and their various levels of debt, as the diagram included below displays.

Image Source: Value Walk.

{kind=link}

Preferred equity is quite similar to common equity on the surface in the sense that both can be bought and sold through normal retail brokerage accounts and normally make quarterly payments to their investors. The similarities end at this point since there are a number of differences that make preferred equity somewhat similar to debt, however, still just different enough to technically remain classified as equity.

The first primary difference to common equity is that preferred equity makes consistent payments that are not open to the discretion of management and are either fixed or floating with a spread above a benchmark rate such as LIBOR. On top of this difference, if they defer their preferred equity payments then nothing can be paid to the holders of the common equity until such time as all accumulative unpaid preferred equity payments have been fully paid, normally with additional interest.

The second primary difference is central to the following strategy, being that most preferred equity is issued with a par value of $25 per unit or share. This should be returned to investors by the issuing organization either on or after the call date, however, unlike debt they can elect to defer this repayment forever whilst still making the routine payments.

When these two considerations are combined it means that their preferred equity yield can only increase or decrease if their shares or units are trading above or below their par value. A simple rule of thumb to remember is that preferred equity is safer than common equity and will continue paying distributions unless the partnership is circling the drain on the brink of bankruptcy.

The Strategy

Thankfully this strategy is surprisingly simple and for the purpose of this analysis their Series C preferred units (ETP.PC) have been selected, however, this same strategy should translate broadly the same to their Series D and E preferred units (ETP.PD) (ETP.PE). The core idea stems from the fact that in theory, there should always be a direct relationship between risk and returns, whereby a higher yield stems from higher risk and vice-a-versa. Whilst this relationship could breakdown in the very short-term from time to time depending on how efficiently the market is pricing assets, the basic relationship should still hold true on average.

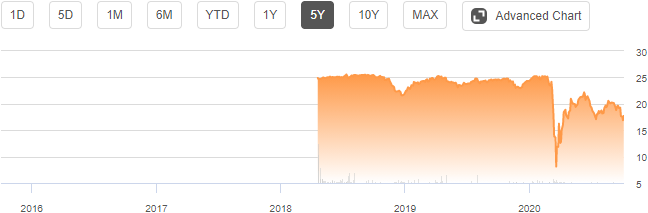

Historically their Series C preferred units were trading around their par value of $25 until earlier in 2020 when this latest Covid-19 economic downturn rocked the markets, as the graph included below displays. This has sent their original distribution yield of 7.375% soaring to its current 10.05%, which clearly reflects the higher risks attached to their preferred units in light of this hard-hitting economic downturn.

Image Source: Seeking Alpha.

So when looking forwards into the future, what would de-risk their preferred units? Simple, the same way as their bonds through lowering their leverage and thus reducing risks. This is incidentally exactly what would happen if their common distributions are reduced and thus in theory, their preferred units should rally back towards their par value if this eventuates. Whilst their preferred units may briefly drop in price following the news simply due to headline risk, I am not in the business of trying to guess very short-term daily price changes.

If the potential reduction to their common distributions eventuates, then their Series C preferred units should increase from their current price of $18.34 per unit back to par value of $25 per unit within the next year as risks decrease. This would result in a very desirable return of 36.31% even before counting any distribution and thus help to mitigate the loss of income from the common distributions. To provide a basic example, if an investor were to purchase an equal quantity of both their common units and Series C preferred units at their current unit prices they would receive distribution yields of 22.10% and 10.05% respectively, assuming no distribution reductions eventuate. If their common distributions were halved, likely the worst-case scenario, then they would lose 11% per annum of income, which the gains from their preferred units should cover three times over.

The extent that this either provides a hedge or creates profits for an investor will depend upon their position in their common units, obviously more common units equals less overall profits and vice-a-versa. If they do not reduce their common distributions then investors can still sit back and get collect a 10% distribution yield from their newly acquired preferred units, which is hardly a negative outcome.

Conclusion

Even though a distribution reduction for their common units may not ever eventuate despite the skepticism in the market, at least unitholders such as myself have a way to hedge and possibly even profit if it does eventuate. This appears to be a highly desirable win-win scenario and thus I backed up my analysis by putting my money where my mouth is and purchased their Series C preferred units last Friday. Since nothing material has changed, I will be maintaining my very bullish rating for their common units whilst also initiating a bullish rating for their preferred units.

Disclosure: I am/we are long ET, ETP.PC. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.