tum3123/iStock via Getty Images

I recently covered the Templeton Emerging Markets Income Fund (TEI) an actively-managed, emerging markets government bond CEF, with a bearish rating. Franklin Templeton has a similar, less aggressive, fund, the Western Asset Emerging Markets Debt Fund (NYSE:EMD).

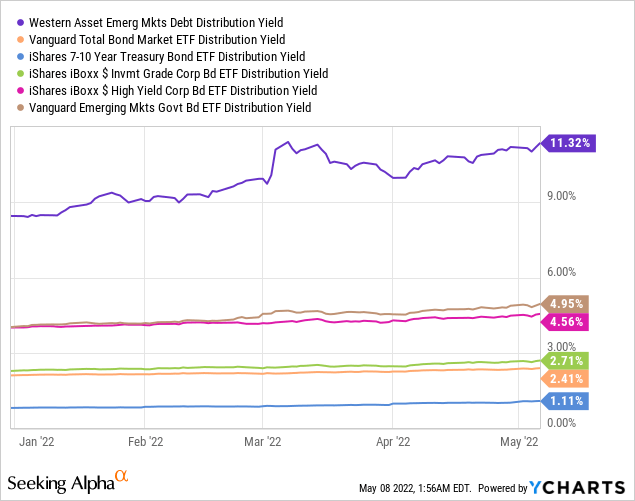

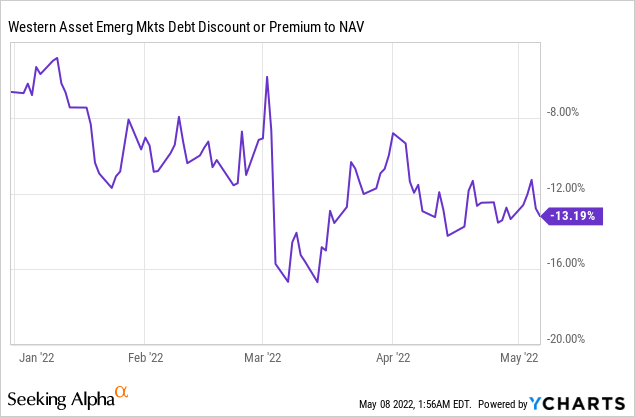

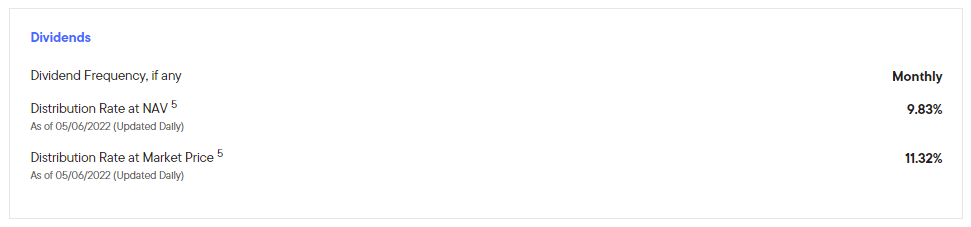

EMD offers investors a strong 11.3% distribution yield, and trades with an attractive 13.2% discount to NAV.

EMD’s distribution is not covered by underlying generation of income, which has led to consistent distribution cuts and capital losses in the past. Further cuts and losses are quite likely. EMD has also underperformed on a total return basis for most relevant time periods too. Individually, these are all relatively small issues, but the combination means EMD is a broadly negative investment. As such, I would not be investing in the fund at the present time.

EMD – Basics

- Investment Manager: Franklin Templeton

- Expense Ratio: 1.59%

- Distribution Yield: 11.32%

- Discount to NAV: 13.2%

- Total Returns NAV 10Y: 1.51%

- Leverage Ratio: 1.41x

EMD – Overview

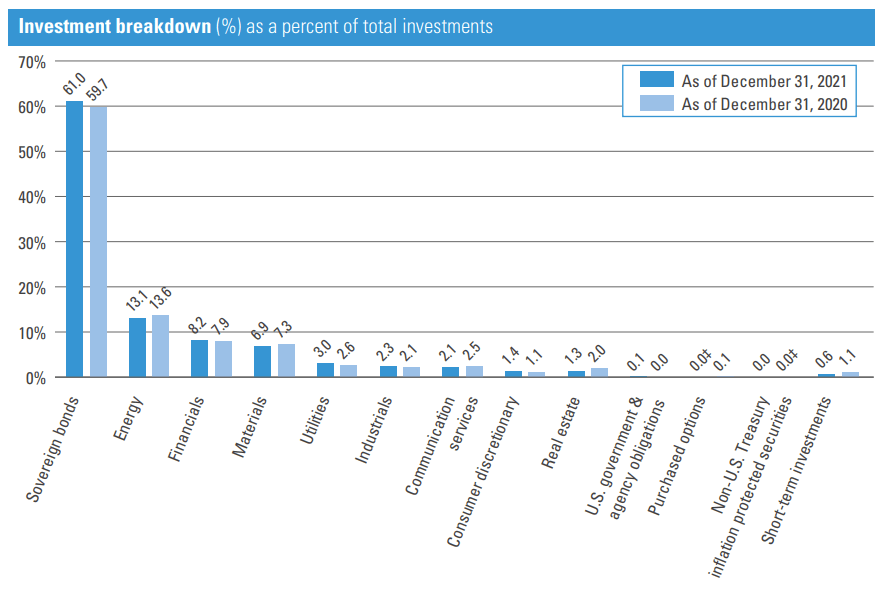

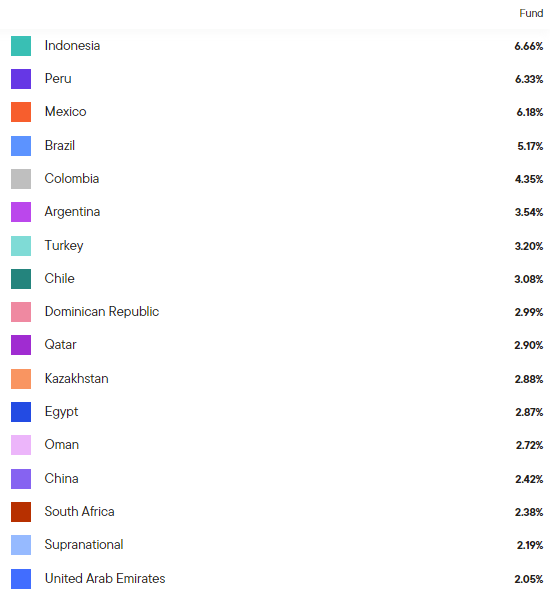

EMD is a leveraged emerging markets bond CEF. The fund’s holdings are reasonably well-diversified within their niche, with investments in 244 different securities from dozens of countries and issuers. The fund invests in both sovereign and corporate debt, being slightly overweight the latter. Sector and country exposures are as follows.

EMD Corporate Website EMD Corporate Website

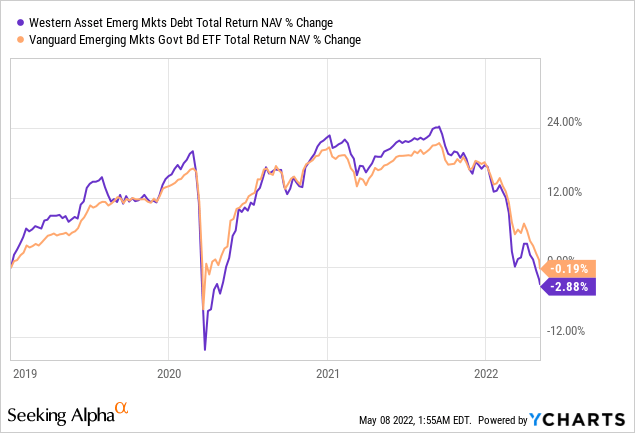

EMD’s allocation to Russian securities is currently about average for an emerging markets bond fund, with a 0.70% allocation to said country. EMD’s Russian investments were much greater earlier in the year, in the high single-digits. Said overweight position significantly underperformed earlier in the year, leading the fund to moderately underperform YTD. You can even see how the gap between the fund and the index widened in late February, when the Ukraine war started in earnest.

EMD recently reduced its allocation to Russian securities, so these issues will have no material impact on the fund or its performance moving forward.

Besides the above, EMD seems to broadly track the emerging markets debt universe, with the fund generally performing in-line with the index. Periods of significant outperformance or underperformance are both relatively uncommon.

EMD – Positives

Strong Distribution Yield

EMD focuses on emerging market debt, an asset class with above-average yields. EMD itself sports a 11.3% distribution yield, quite strong on an absolute basis, and significantly higher than that of most bond indexes.

EMD’s strong yield is mostly due to the fund focusing on low-quality, high-yield emerging market debt securities. EMD’s yield is further boosted by the fund’s use of leverage, discount to NAV, and a return of capital component.

Compelling Price and Discount

EMD currently trades with a 13.2% discount to NAV. It is a large discount on an absolute basis, and somewhat higher than average relative to historical discounts.

EMD’s discount to NAV benefits investors in two key ways.

First, discounts can always narrow, leading to capital gains. EMD tends to trade with a relatively large discount, so significant capital gains seem unlikely. Smaller capital gains seem much more possible. I could easily see the fund’s discount narrowing to the high-single digits, levels last seen in February. These would imply capital gains in the mid-single digits for EMD’s shareholders, which are reasonably good.

Second, discounts to NAV are analogous to lower share prices, and lower share prices mean higher distribution yields. As per the fund’s management team, EMD sports a 9.8% distribution yield on NAV. EMD’s discounts mean share prices are lower than NAV, and so shareholders actually receive a 11.3% on their investment. EMD’s current discount boosts the fund’s distribution by 1.5%, benefitting investors.

EMD Corporate Website

EMD’s distribution yield and discount to NAV are both quite attractive, but overshadowed by the fund’s many negatives. Let’s have a look.

EMD – Negatives

Above-Average Risk, Volatility, and Losses during Downturn

EMD is a relatively risky fund, for three key reasons.

First, is the fact that the fund focuses on emerging market bonds. Emerging markets are significantly riskier than U.S. markets, as their economies, corporations, and governance standards are weaker. Recessions and downturns are more common in emerging market, as are defaults. Importantly, investors are well aware of these facts, and so tend to sell emerging market securities, including bonds, when times are tough, leading to lower prices and capital losses.

Second is the fact that the fund’s overall credit quality is somewhat below-average. EMD invests in both investment grade and non-investment grade bonds in equal measure, with an average credit rating of BBB. Although EMD’s overall credit quality is not terrible, most broad-based bond indexes focus on investment grade bonds, with comparatively low exposure to riskier bonds. EMD’s credit quality is lower than average, which boosts risks and losses during downturn.

Third is the fact that EMD is a leveraged fund, with a 1.41x leverage ratio. Leverage means more assets, which means more income, capital gains, and losses. Leverage is particularly harmful during severe downturns, as leveraged funds are sometimes forced to sell assets at low prices during these.

The above combine to create a relatively risky fund, and one which should underperform relative to most bond indexes during most downturns. As an example, EMD significantly underperformed relative to most bond indexes during 1Q2020, the onset of the coronavirus pandemic, and the most recent recession.

EMD will likely underperform during future downturns and recessions, a negative for the fund and its shareholders.

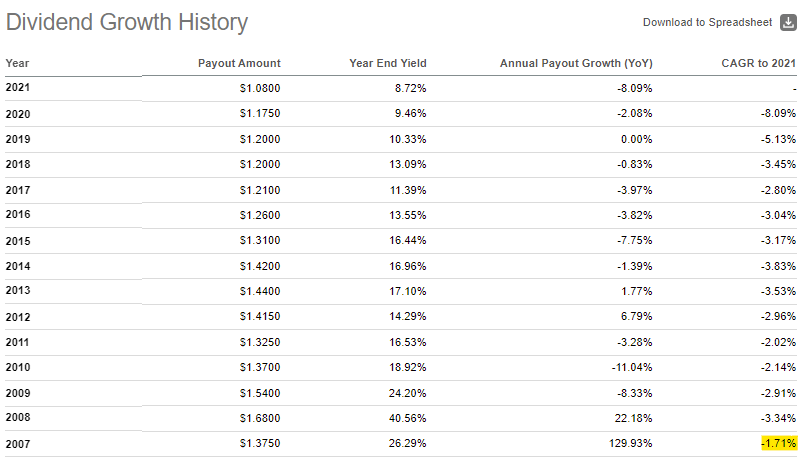

Unsustainable Distribution

EMD’s distribution yield is quite strong, but it is not covered by underlying generation of income, or even capital gains. EMD’s distribution is partly financed by selling assets, even if these have not appreciated in price. As per management data, the fund’s distribution is about 40% return of capital, although exact percentages vary. Significant return of capital distributions are, almost by definition, long-term unsustainable. Distribution cuts are likely, as have been the case since inception, and for most relevant time periods too.

SeekingAlpha

Distribution cuts are a negative, and particularly important insofar as they undercut one of the fund’s key benefits: its yield. EMD’s distribution yield is quite strong, but consistent distribution cuts erode the actual income received by investors through time. As an example, the fund sports a 5Y yield on cost of 6.9%, and a 10Y yield on cost of 5.3%. Consistent distribution cuts are a negative for the fund, and particularly harmful for long-term investors.

SeekingAlpha

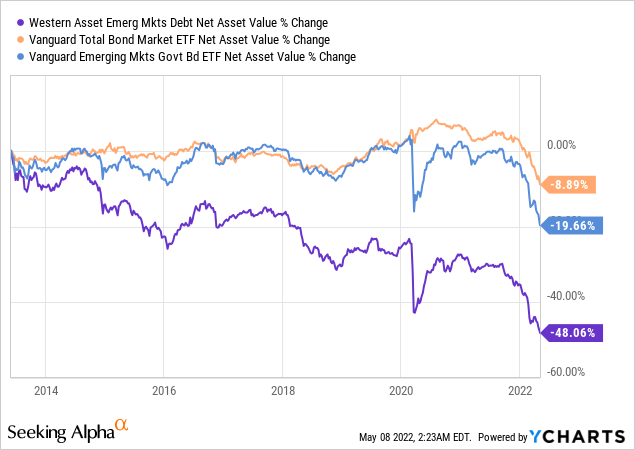

Consistent Capital Losses

EMD has seen consistent capital losses since inception, partly due to weakness and lackluster results in emerging markets, and partly due to destructive return on capital distributions. EMD’s NAV has plummeted more than 48% in the past decade, significantly higher than average losses.

Consistent capital losses are a negative for the fund and its shareholders. Capital preservation is paramount, and EMD does quite badly in this regard.

Consistent Underperformance

Finally, EMD’s performance track-record is below average, with the fund consistently underperforming relevant bond indexes. Underperformance relative to emerging market debt indexes has been quite small, however.

SeekingAlpha – Chart by Author

EMD’s consistent underperformance is a negative for the fund and its shareholders.

As a final point, I don’t believe that any of EMD’s negatives is all that significant, but the combination makes a bullish rating impossible. Distribution cuts undercut the fund’s income, consistent capital losses mean no capital gains, and consistent underperformance means total returns are subpar, at best. With a negative assessment of the fund’s income, capital gains, and total returns, there is simply no viable investment thesis here.

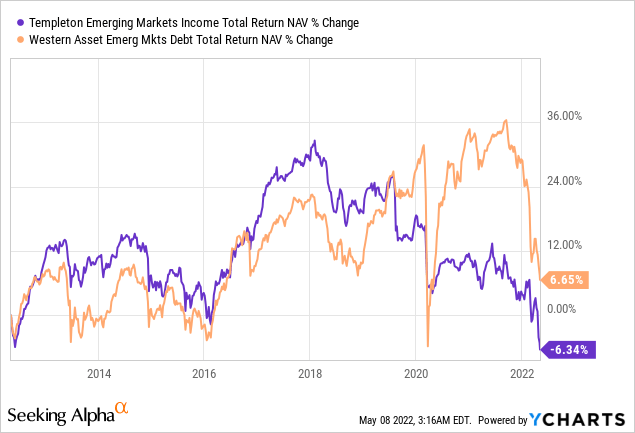

TEI Comparison

Finally, a quick comparison between EMD and TEI, the fund’s sister fund.

Both funds have similar holdings and overall strategy. TEI is, however, more aggressive in its trading and positioning, with the fund more consistently deviating from the index. Said aggressiveness has been a net negative for most relevant time periods, with TEI underperforming relative to EMD.

On the other hand, TEI’s strategy has been a success YTD, with the fund significantly outperforming during the same.

In my opinion, TEI’s long-term underperformance make it a worse investment compared to EMD, notwithstanding recent outperformance.

Conclusion

EMD’s distribution is unsustainable, the fund has suffered consistent capital losses and underperformance since inception. As such, I would not be investing in the fund at the present time.