AsianDream/iStock via Getty Images

Thesis

The Stone Harbor Emerging Markets Income Fund (EDF) is a closed end fund focused on emerging market debt. The fund has a broad mandate being able to invest in sovereign and corporate EM bonds but has an aggressive credit risk profile with most of its holdings being allocated to below investment grade credits. We wrote an article assigning the fund a Sell rating back in October 2021, and the fund is down almost 20% on a price basis since the writing of our article. The current Ukraine crisis has driven a massive risk-off environment which has led to a significant credit spread widening, especially for sub-investment grade emerging market credits. EDF is a very leveraged vehicle (above 30% leverage) which has served to magnify the current risk sell-off thus contributing to the significant recent negative performance. We do not think EDF is a good long term buy-and-hold vehicle and its metrics are poor, including its very significant annual NAV give-up, but we are currently in a set-up where a short seller would be well served to close an outright short position in the fund after a very significant gain. We are moving from Sell to Hold on this fund and we would wait for a narrowing in the premium to NAV as a signal for an outright short term buy trade.

Ukraine Crisis

The current Ukraine crisis has driven a significant widening in emerging markets credit spreads:

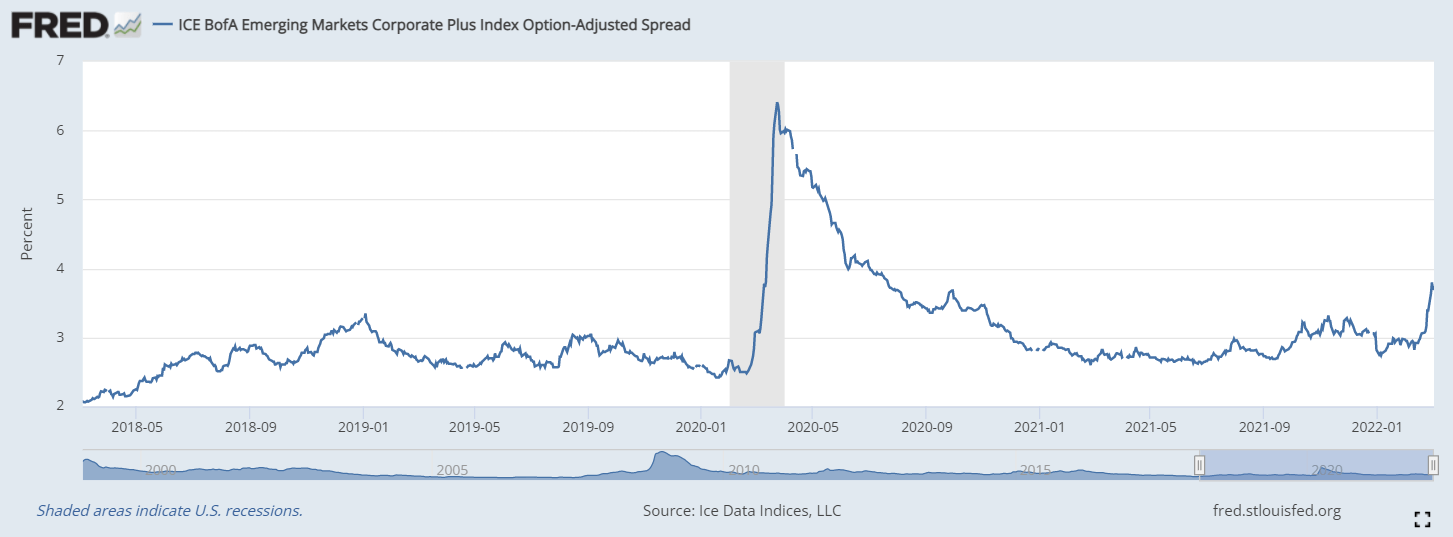

EM Credit Spreads (The Fed)

In fact we can see from our option-adjusted spread graph that EM spreads are at the widest levels since the Covid crisis. The uncertainty of political decisions in certain jurisdictions and their impact on corporate credits that otherwise are exhibiting healthy metrics has been significant. Political risk plays a large part in EM credit spreads and it is a very difficult variable to quantify and price. After banning foreign investors from selling assets Russia is currently a quandary in respect to ultimate recovery for both corporate and sovereign debt held by foreigners. With a sub 5% Russia exposure the fund has not been steamrolled by the country exposure but is pricing currently a de-minimis recovery in the jurisdiction. Given its high leverage (above 30%) the credit spread widening has been magnified for the fund, accounting for the significant negative performance. Leverage works well to increase returns in a stable or tightening spread environment, but is also very destructive when downward moves occur.

Performance

Since our article the fund is down almost -20% on a price basis:

Fund Performance (Seeking Alpha)

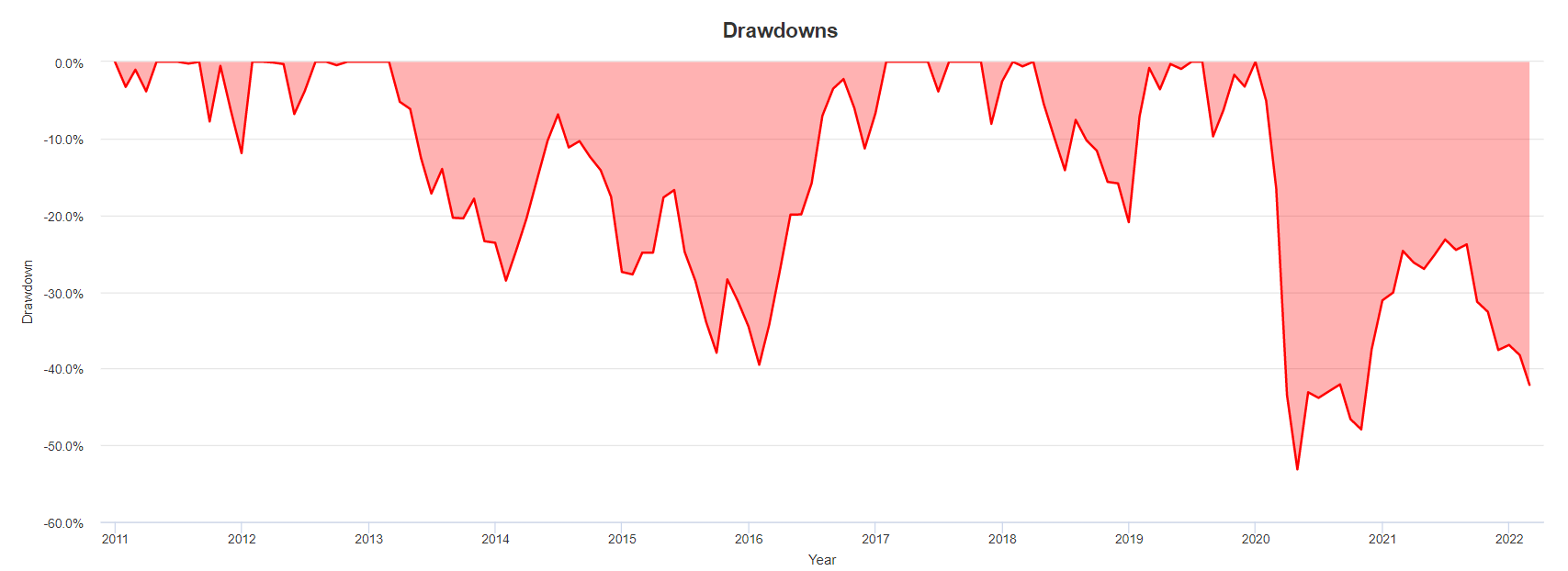

The past few months have not been kind to EDF given its aggressive portfolio set-up and the ongoing Ukraine crisis. The fund is actually experiencing its second largest drawdown in the past decade after the Covid related sell-off:

Drawdowns – 10 Year History (Portfolio Visualizer)

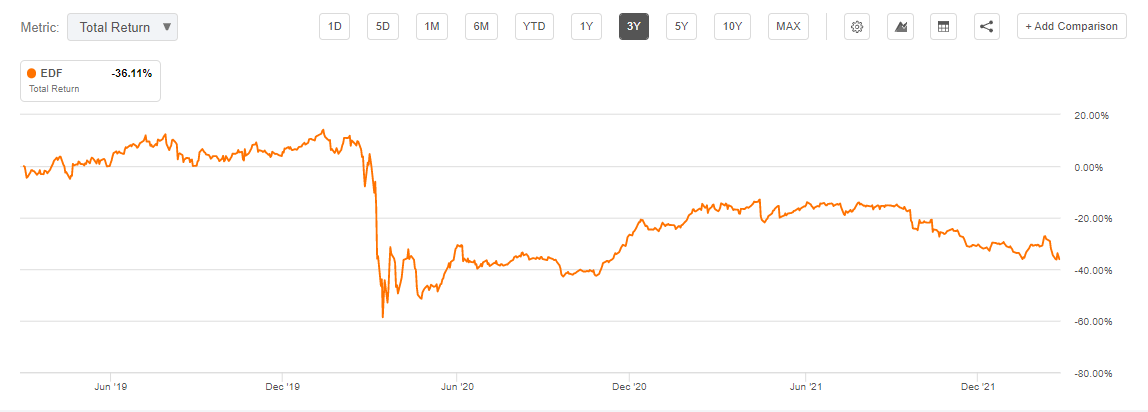

On a 3-year basis the fund is close to re-tracing its Covid move:

3-Year Total Return (Seeking Alpha)

Holdings

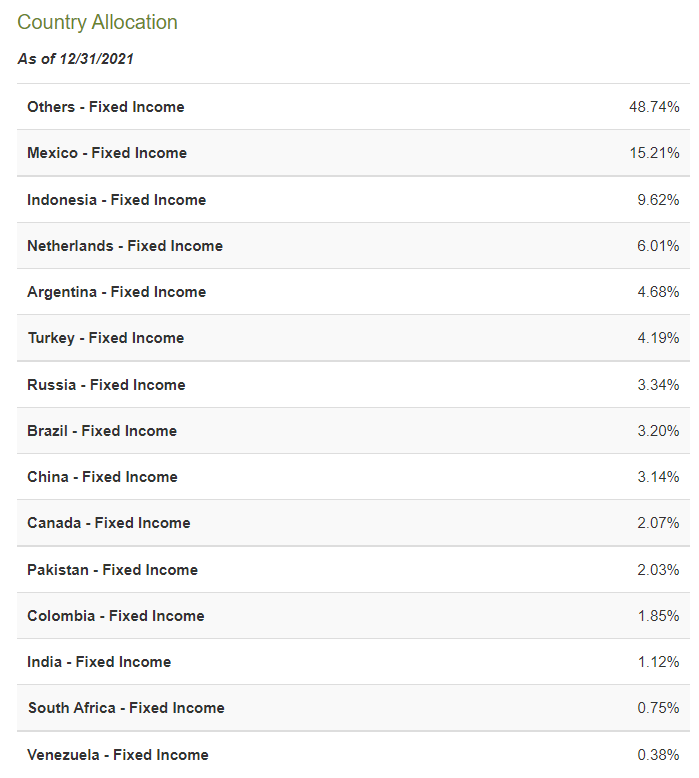

The fund has a sub 5% country allocation to Russia:

Country Allocation (CefConnect)

While not large, the Russian country allocation now trades heavily discounted and there is currently very little visibility in terms of ultimate recovery for the jurisdiction’s credits.

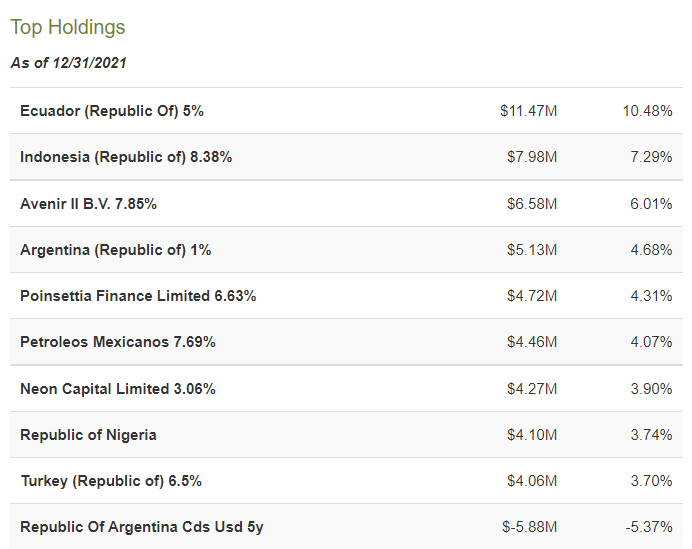

The largest exposures of the fund now sit with Ecuador and Indonesia:

Top Holdings (CefConnect)

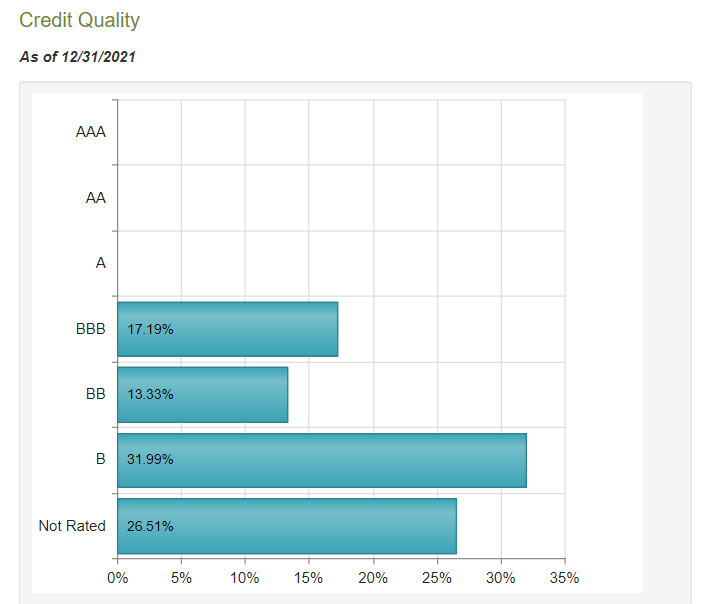

However please note that this vehicle likes to play at the bottom of the credit spectrum as discussed before with large very low rated buckets:

Holdings Ratings (CefConnect)

We can see from the above bucketing that almost 70% of the fund sits in below investment grade and not rated buckets. A portfolio heavily tilted to sub-investment grade credits tends to have a higher sensitivity to credit spreads, thus downward moves when a risk-off environment materializes are more violent than their IG peers.

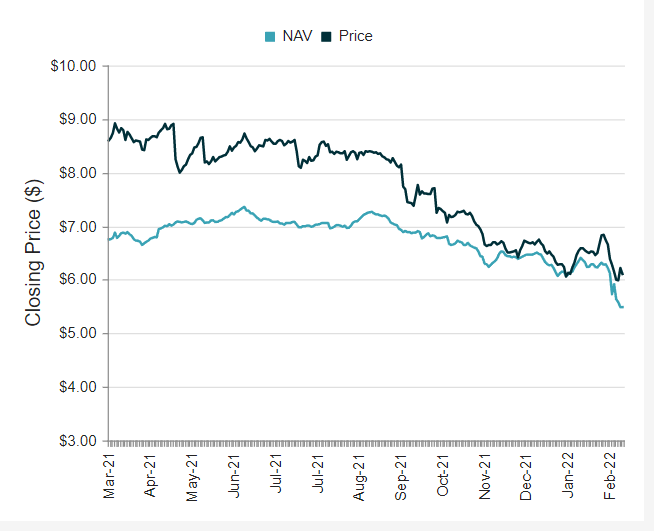

Premium to NAV

We are a bit surprised by the performance of the premium to NAV:

Premium to NAV (CefConnect)

While the premium to NAV narrowed to a flat level in the beginning of January, it is now back to above 10%. This sort of move is surprising because historically funds with large premiums to NAVs tend to see them narrow significantly when the market experiences risk-off events. What makes this fund interesting is that it has experienced a tremendous NAV sell-off on the back of fundamental factors, but the laying bricks of the CEF structure have not given in all the way. In the current set-up a nice buy signaling tool would be represented by the narrowing of the premium to NAV to a fully flat level.

Conclusion

EDF is a fixed income EM debt CEF from Stone Harbor. The vehicle has experienced a significant price decrease in the past four months (~ -20% move) on the back of the Ukraine crisis and rising Usd interest rates. The current risk-off environment and Ukraine crisis have resulted in a significant spread widening for emerging market credits and we feel that it currently represents an opportune time to close an outright short position after realizing a significant gain in the past four months. The dynamics of the premium to NAV for this fund are very interesting, with a nice buy signal potentially coming into play if the premium to NAV narrows to a flat level in the upcoming months. Overall we are moving from Sell to Hold for this name.