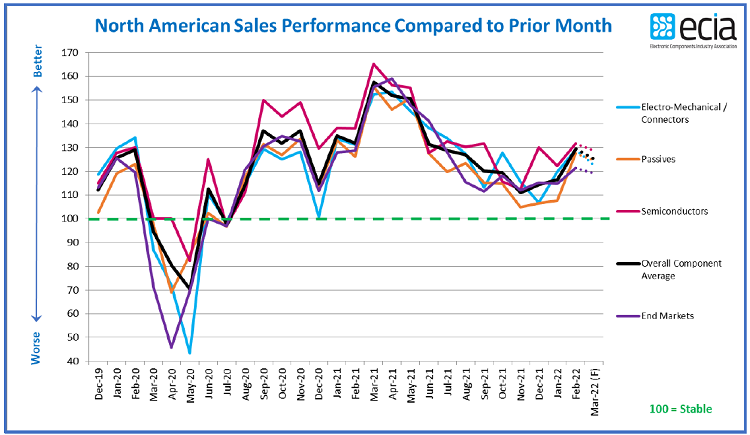

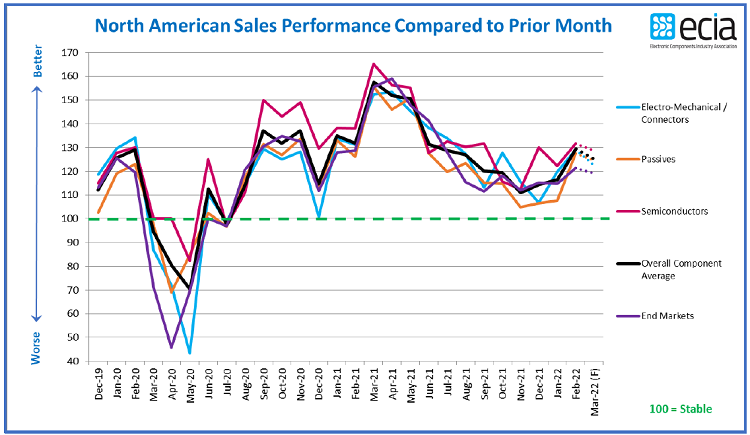

On the heels of a boost in the U.S. manufacturing sector, electronic component sales trends saw an increase between January and February, according to the ECIA. Overall sales sentiment for February registered 129.4, outperforming expectations by 16.3 points. In an indication of the strength currently seen by the supply chain, the index only dips slightly to 125.2 in the outlook for March.

Any number above 100.0 indicates positive momentum. The results for both months is a very encouraging indicator of resilience and stability in the electronics component markets, said ECIA.

Source: ECIA

In February, the U.S. PMI grew 1 percent to 58.6 — any number above 50.0 represents expansion. “The U.S. manufacturing sector remains in a demand-driven, supply chain-constrained environment,” said the Institute for Supply Management’s Tim Fiore. “The Covid-19 omicron variant remained an impact in February; however, there were signs of relief, with recovery expected in March.”

Electronics’ industry optimism is uniform across all major component categories, ECIA reported. Inductors saw a major jump in positive sentiment as they surpassed even discrete semiconductors which had been an index leader. In addition to inductors and discretes, analog/linear ICs and connectors scored notably higher than other subcategories. Every component subcategory except one achieved a score of at least 125 – resistors came in at just under 118.

The strength of the market sentiment in the first three months of 2022 shows solid momentum to start the year, said ECIA Chief Analyst Dale Ford in a statement. The end-market index continues to follow closely the general trend of the component index. In recent months the average end-market scores have come in slightly lower than the component index. February’s end-market score came in at 121.3. The difference is likely due to all market categories being weighed the same in calculating the average whereas the demand for components varies by end-market.

Overall, the U.S. computer and tech segment expanded in February, according to the ISM; employment, production and supplier deliveries all improved. Inflation eased slightly and future signals remain strong: backlog jumped to 86 percent and customer inventories remain too low. That said, one tech executive described the electronics supply chain as a “mess,” and research points to lengthening lead times, continued scarcity, logistics delays and other headwinds.

The robust component sales sentiment in the index continues a strong pattern as it has now registered above 100 for 19 straight months dating back to August 2020, ECIA reported. A comparison between the three groups surveyed – manufacturers’ reps, distributors and component makers — shows a dramatic shift in sentiment among manufacturers. Compared to their pessimistic expectations for February, their sentiment for actual February performance came in at the top of all three groups.

This time, distributors were the most conservative in their report of sentiment for February. All three groups see a slight dip in expectations for March, but all still score above 123 in the coming month.

Economic concerns

The continued strength of sentiment is impressive considering the continued supply chain challenges as well as economic concerns, said Ford. The war on Ukraine by Russia had not commenced by the end of the survey so the potential impact from that major world development is not captured in the ECIA survey. ISM does not expect domestic manufacturing will stall although logistics costs will increase along with oil prices.

ECIA’s survey presents a strong positive picture for both Q1 and Q2 2022. The overall average of the total number of respondents expecting growth in Q1 2022 is 64 percent and only dips slightly to 62 percent in Q2. However, the mix of expectations for growth in the different tiers shows a shift to lower growth expectations in Q2 compared to Q1. Bottom line: There is solid expectation for growth through the first half of 2022 with growth slowing in the later months.

Once again, semiconductors measure the highest level of optimism with at least 70 percent expecting growth in both Q1 and Q2.

As anticipated in January, mobile phones, computers, and consumer electronics registered weak sales sentiment scores of 100 or less in February, according to ECIA. However, in the outlook for March, markets see measurable improvement with scores solidly above 100. Softness in these areas early in the year reflects a typical seasonal pattern for these markets.

Automotive electronics and industrial electronics both delivered strong sales sentiment above 130. Avionics/military/space measured 125 in February. Medical electronics and telecom networks both achieved solid sentiment scores in both February and March.

Concerns related to the economy have not changed from the last report as inflationary pressures continue to increase and consumer confidence takes a strong hit, said Ford. The most recent PMI index still shows optimism for growth. But the overall economic picture still leaves room for concern. The Lehigh University “Supply Chain Risk Index” placed economic concerns at the top of the list, ahead of transportation disruption risk in Q1 2022. Cybersecurity and data risks also saw a big jump in the latest index. With no end in sight to elevated supply chain challenges, manufacturers and retailers continue to face an extremely risky and uncertain future.

Common projections for resolving the major supply chain challenges still stretch out into early to mid-2023. Lead time data reported by ECIA through January seemed to point to a peak in lead times in December and January for all semiconductor categories and many passive categories. The latest survey results saw increased lead time expectations in February. This is a reversal in trends seen over the past several months.