No sense of direction and a “sea of uncertainty” are the reasons behind the dry bulk market’s lackluster performance of late. As a result, 2019 ends with a lack of optimism on the future. In a recent weekly report, shipbroker Allied Shipbroking said that “with the Christmas mood now firmly in place, it would seem that the focus of most is as to what the expected prospects are for next year. Given this, while assuming that it is highly unlike that we will see any extreme change in market conditions for the final few weeks of the year, it seems as though there is considerable debate as to what extent 2019 was a good year for the overall dry bulk sector”.

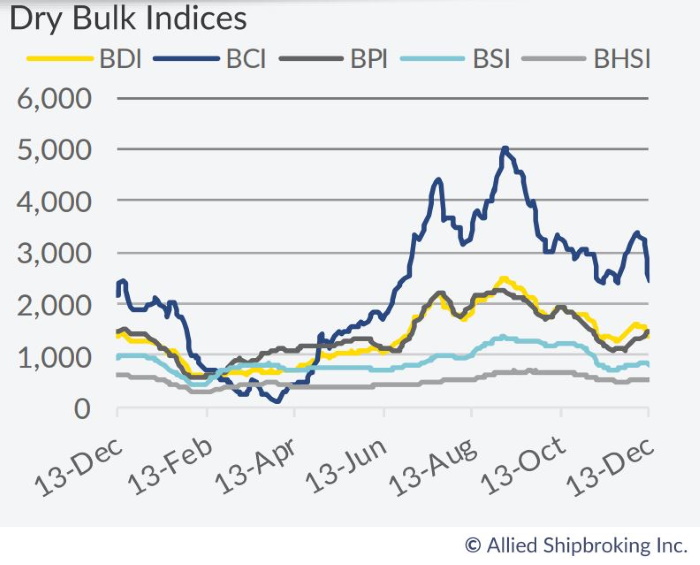

Thomas Chasapis, Research Analyst with Allied said that “I can say with certainty, that in absolute terms, a straightforward answer would be difficult to give. What most would utter is “it depends…” Seeking for a silver lining there is no better place to start than the “impressive” Capesize market. Looking at the BCI-5TC figure, if nothing dramatically changes, we will probably have its highest annual figure since at least the past five years. However, the point to stick to the most is the robust 2nd half, with the market almost (a few exceptions here and there were seen) holding above the 20,000 $US/day. Moreover, it is evident that the once considered “overpriced” FFAs back in late September, were actually “in-the-money”.

According to Mr. Chasapis, “this certainly caught many by surprise given the overall step back in iron ore’s seaborne trade for the year, while, at the same time, we experienced for two consecutive months (within the final quarter) decreasing imports of iron ore to China. On the other hand, earnings for Panamaxes and Supramaxes, despite having reached long term highs earlier in the year, the extended downward correction finally pushed their average yearly earnings below those of the year prior, putting both these submarkets into the perceived doldrums”.

He added that “with “fragile” trade conditions being seen for the near future, while the market is looking to absorb the more than 5% increase noted in the Panamax/Kasmarmax fleet, the coming period will be, to say the least, challenging. Many have pointed out volatility as the main culprit for this bizarre trajectory of the dry bulk freight market. However, the current bewildering sentiment and the lack of any direction as of late, is more so a reflection of the excessive uncertainty that has been surrounding the market for many months now. The term excessive is justified, because it is one thing to have uncertainty as a result of high volatility and a whole other thing to adopt uncertainty and volatility as the same thing. To get a good taste of this on only need to take a simple look at the derivatives market. We have mentioned many times the bearish attitude in terms of forward sentiment that has been portrayed of late in the paper market. At that time, it was considered more as an overreaction, rather than the actual forward perspectives being viewed”.

Meanwhile, “given the lack of upward potential for some time now, I feel that we have a “misprice” of the uncertainty being portrayed, something that could further drive the already volatile nature of the shipping markets (in the short-run at least). Taking a closer look at the “longerterm” FFA contracts, we see a huge step back in overall returns, especially when compared with those noted over the past 3 years or so. Beyond this mere step back, we are talking about returns that are at least “questionable” in terms of sustainability (under a risk-reward analysis scheme). We might be stating the obvious here, but if forward returns would be to hold at such “squeezed” levels for that long, one would expect that the market would react (at least on the supply side of things) in accordance to bring about healthier levels much sooner. For the time being, the market must recover much quicker in terms of sentiment, to be able to confront the dynamic pressures that are set to arise soon enough”, Chasapis concluded.

Nikos Roussanoglou, Hellenic Shipping News Worldwide