Dollar Tree (NASDAQ:DLTR) recently reported financial results for the fourth quarter of fiscal 2019.

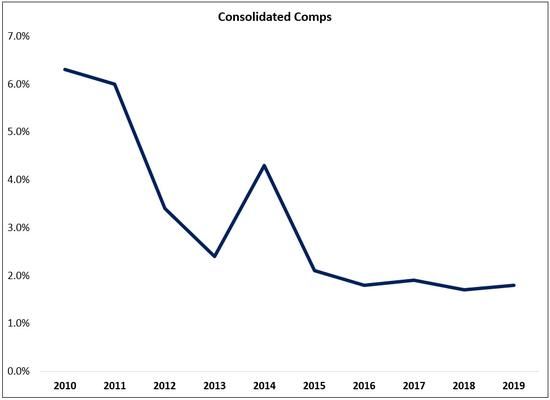

For the quarter, comparable store sales (comps) increased marginally (0.4%), with an increase of 1.5% at the Dollar Tree banner offset by an 0.8% decline at Family Dollar (note that they faced some headwinds in the quarter from a condensed holiday shopping season and the early release of SNAP benefits in the year-ago period). As shown below, consolidated comps in 2019 were comparable to what the company has reported in each of the prior three years – but well below what shareholders were accustomed to in the years before 2016.

A closer look at the two-year stacked comps tells a different story. The chart below shows that there has a deceleration in the growth rate for both banners over the past year. For the company’s flagship banner, the two-year stacked comp has fallen from 7.1% to 4.6% over the past year. And at Family Dollar, despite the significant time and energy focused on trying to turnaround the business, two-year stacked comps in the fourth quarter, at just 0.6%, were at their lowest point in two years (note that this metric is inclusive of the tailwind from the renovated H2 stores, as well as the benefit they receive from closing or rebannering underperforming locations).

Between low single-digit comps and immaterial net unit increases – largely due to a 6% reduction of the Family Dollar footprint – revenues increased 3% for the year to $23.6 billion. Based on guidance, management expects a similar dynamic in 2020 as well.

In addition to lackluster revenue growth, the company is facing material headwinds down the income statement. For the year, gross margins and operating margins contracted 60 basis points and 130 basis points, respectively (on an adjusted basis). In terms of operating margins, that outcome reflects an 80 basis point decline at Dollar Tree (to 13.3%), partly due to the impact of tariffs, and a 180 basis point decline at Family Dollar (to 2.3%). Margin contraction at both banners led to a double-digit decline in adjusted operating income (down 13% to $1.6 billion).

To put the Family Dollar results in context, the banner generated $250 million in operating income this year – a small number relative to the roughly $9 billion paid to acquire the business in 2015. Clearly, the results are not living up to the expectations management had when they agreed to the deal. In addition, it’s clear that the unit economics for this banner are inferior to the results at the Dollar Tree banner. At this point, I think it’s safe to say that this deal has resulted in material per share value destruction for shareholders.

We can see the combined impact of margin contraction at both banners and mix shift to Family Dollar (which has much lower gross and operating margins than Dollar Tree) by looking at the consolidated margins for the company. As shown below, 2019 operating margins are now 500 to 600 basis points lower than what the company reported prior to the Family Dollar deal.

The company continues to reinvest in the business, primarily on the Family Dollar turnaround. Capital expenditures in 2019 exceeded $1 billion, 27% higher than in 2018. In addition, the company guided to $1.2 billion in capital expenditures in 2020 (note that this is leading to a divergence between earnings and free cash flow, with a gap of roughly half a billion dollars likely in 2020). By my estimate, nearly half of the company’s capital expenditures are now being allocated to the Family Dollar banner – investment that comes with a much lower return than what the company has historically attained from adding Dollar Tree units. In addition, there could still be years of investment ahead for Family Dollar: assuming the company hits their target for 1,250 renovations in 2020, they will have upgraded roughly 30% of all locations to the H2 format by year end – leaving them with more than 5,000 units that may still need work.

At the end of the day, shareholders need to decide if they’re comfortable with the strategy. In my opinion, management is as (publicly) committed to the turnaround as they’ve ever been. (Note that activists tried to push management to divest FDO in early 2019, but without any success.)

Conclusion

Despite management’s optimism, market participants appear to believe that the focus on the Family Dollar turnaround is misguided. In addition, the degradation in comp store sales growth at the Dollar Tree banner has raised concerns. The end result is a forward price-earnings ratio of roughly 15 times – well below what Mr. Market was willing to pay for this business a few years ago.

As I’ve said in the past, I believe the Dollar Tree banner alone is worth $80 per share. If you agree with my numbers, then Mr. Market has attributed somewhere between $10 and $40 of per-share value to the Family Dollar banner over the past year (rough numbers). Today, with the stock trading at $80 per share, I would argue that the market is now attributing little to no value to Family Dollar (again, management paid roughly $9 billion for this business five years ago).

I can understand why Mr. Market believes that’s appropriate. The company is allocating capital to less good opportunities (to put it nicely), while also drawng management’s time and attention from its namesake banner.

Based purely on the numbers, I think the stock is reasonably priced. The question investors need to answer is whether management will be rational. If the Family Dollar results underwhelm, are they willing to accept that outcome and make a change? Or will they fight tooth and nail to try and prove a point? Based on what we’ve seen over the past 12 to 18 months, I fear that it may be the latter.

That’s a long way of saying that I think the valuation is attractive, but I’m still moving slowly. There’s not much value in optionality if it seems highly unlikely to materialize. To justify an investment, I need to believe that growing the per-share intrinsic value of the business over the long run is more important to management than protecting their egos. I’m not convinced that’s the case yet.

Disclosure: None.

Read more here:

Not a Premium Member of GuruFocus? Sign up for a free 7-day trial here.

This article first appeared on GuruFocus.