kynny/iStock via Getty Images

With the ongoing war in Ukraine, lockdowns in China, and persistently high commodity prices, many economists predict that the supply chain crisis will last at least until the end of 2022, and probably well into 2023. In this article, we will explore why I believe Desktop Metal, Inc. (NYSE:DM) is an interesting buy in such an environment.

Company Mission

Desktop Metal is a global provider of Additive Manufacturing technologies, across multiple industries and with an extensive portfolio of products and services. Their main mission is to have a double-digit share in this Additive Manufacturing market by 2030, which is expected to reach US$100BN+ in market size.

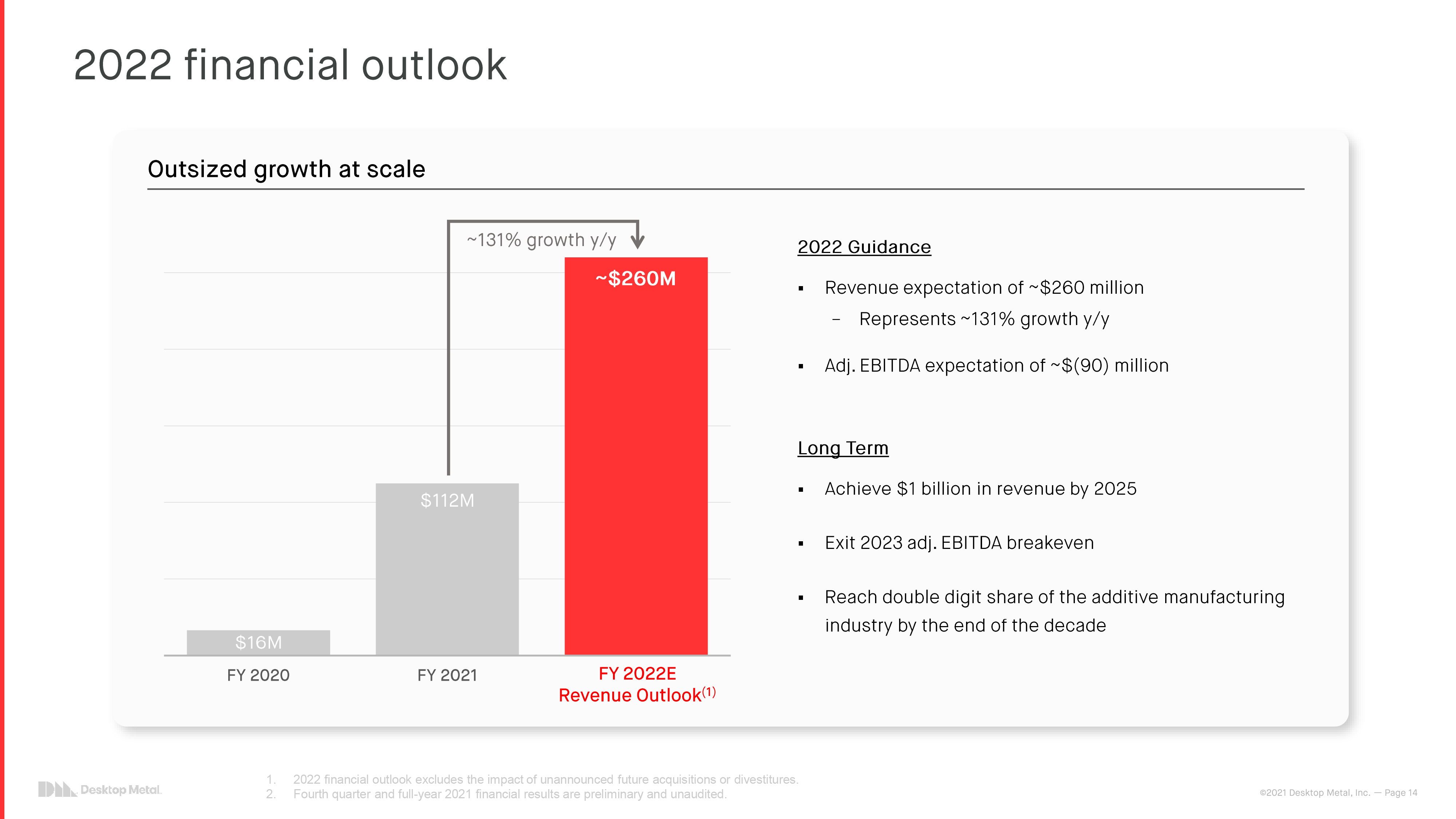

Notably, they managed to bring in US$112M of revenue before year-end 2021, representing a staggering 583% YoY revenue growth compared to 2020. In addition, they built a portfolio of 20 printing platforms with over 650+ issued patents and patent applications with a multitude of different materials to print in. With projected revenue of 260 million by the end of 2022, in an industry with a 15% – 25% CAGR, Desktop Metal is well positioned for growth.

Desktop Metal’s 2022 Financial Outlook (Desktop Metal IR)

Their goal is to capture this market by developing printers, materials and applications to address current problems in the mass production of end-use parts. These problems include, but are not limited to, the lack of supply chain flexibility, geometry limitation, production waste, energy consumption and cost barriers. They operate in a variety of environments, including automotive, healthcare/dental, aerospace, defense and more.

Products

Desktop Metal’s current flagship product is the P-50 production system, which was recently developed as a successor to their previous P-1 machine. After a 4-year development program, during which nearly US$100M was spent on R&D, the company has a workhorse of a machine that can print tens of thousands of pars per day, at 1/20th the price of other laser-driven bed fusion technologies and up to 100x the speed.

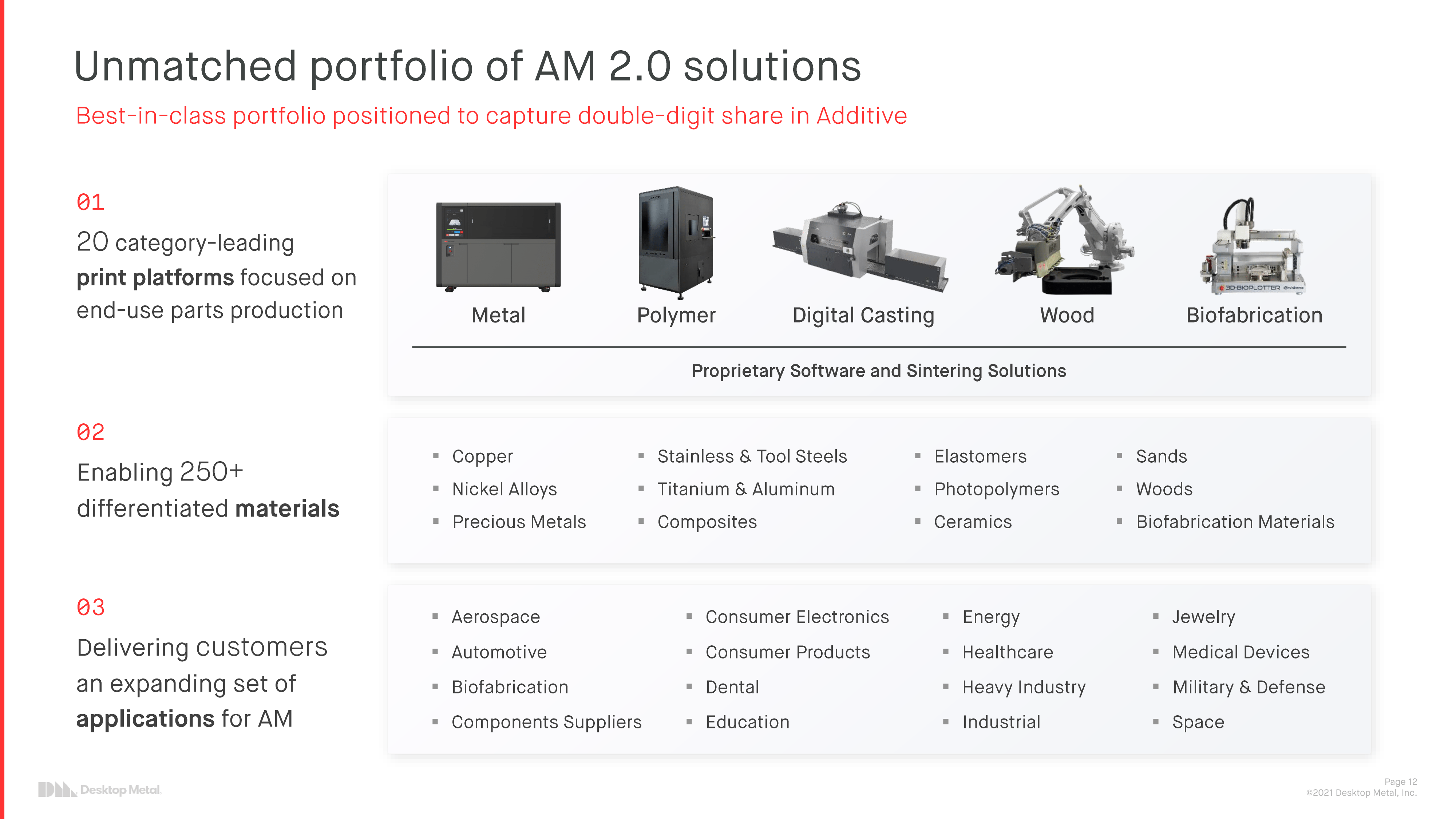

However, Desktop Metal is not only an additive manufacturing company in metals. They also offer various solutions in polymer production, digital casting, wood and biofabrication. One of their most pioneering technologies in polymers is the Xtreme 8K platform, the world’s largest high-speed direct light processing printer with a huge build volume of 71 liters.

Desktop Metal’s Product Portfolio (Desktop Metal IR)

Margins and Profitability

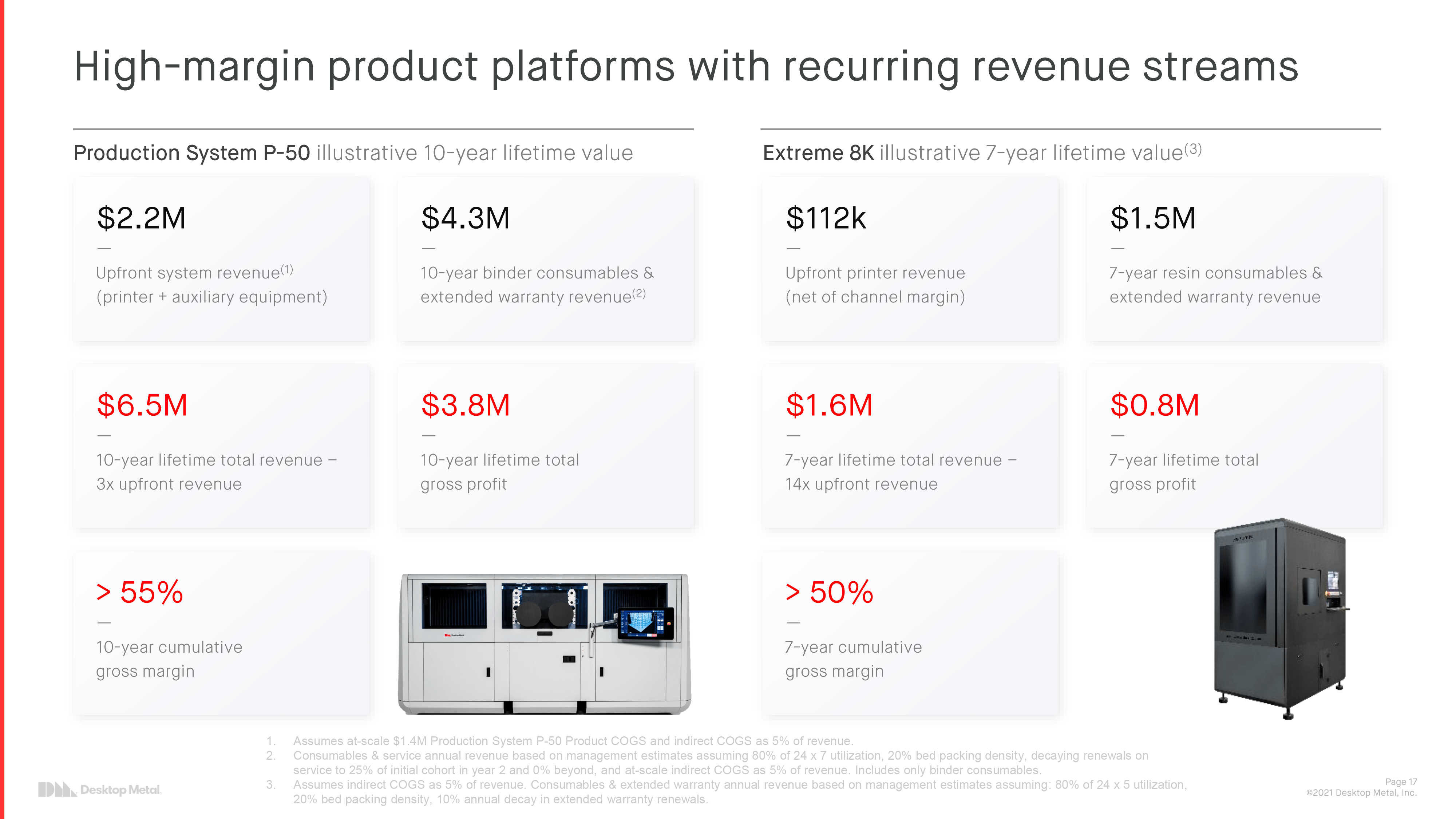

What I always look for in growth companies are products that either have high margins or are expected to have high margins in the future. Looking at both the P-50 and the Xtreme 8K, it seems that Desktop Metal operates on a razor-razor blade business model, with most of its revenue coming from consumables and extended warranty income rather than upfront revenue.

In this example, Desktop Metal estimates that a P-50 machine will generate US$2.2M in revenue at scale, with US$1.4M COGS and an indirect COGS as 5% of revenue, leaving them with less than US$700K in gross profit from the initial sale of the machine. Almost US$2.9M of the gross profit will come from the consumables and extended warranty, which have a higher profit margin. This means that Desktop Metal ought to see a passive growth in their revenue after the initial sale of their machines.

Desktop Metal’s Product Margin (Desktop Metal IR)

This also may account for the improving gross profit margin, since most of the revenue is realized on a long-term basis. The P-50 machine is estimated to generate a total of US$3.8M in gross profit on a 10-year basis, compared to US$800K for the Xtreme 8K on a 7-year basis.

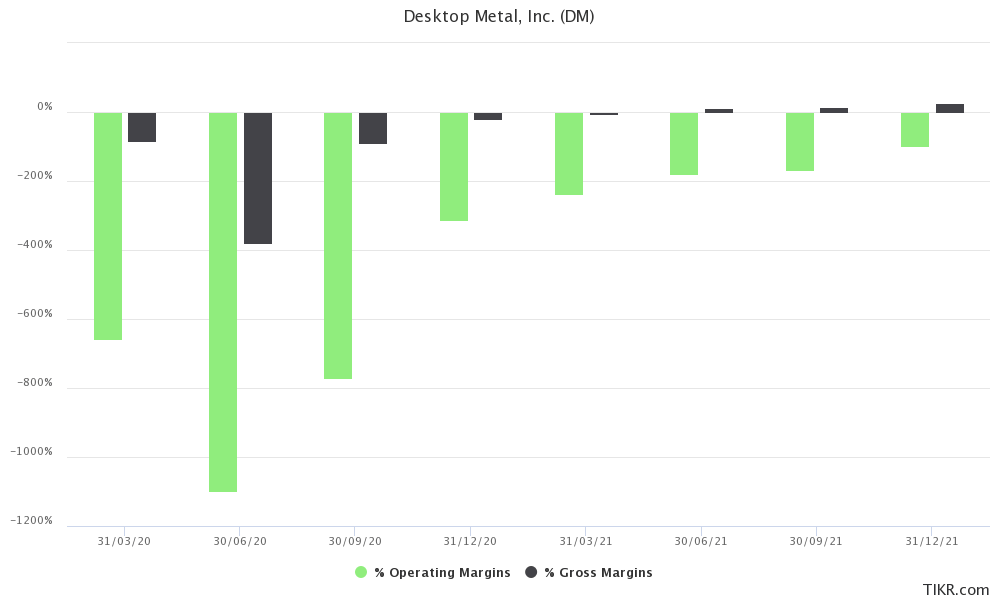

However, they are still far from achieving these targets, as their GAAP gross profit margin is currently 22% according to their latest fourth quarter filing, compared to the expected gross profit margin of 50-55%.

Desktop Metal’s Margin Evolution (TIKR Terminal)

Management and Human Capital

The CEO, Fulop Ric, also seems optimistic about the company’s future, after adding another US$525K to $DM shares on March 16 according to insider trading. He has an extensive track record in the manufacturing industry, and sits on multiple boards of other startups, including some that were acquired by Google and Oracle.

Mr. Fulop is one of the original co-founders, dating back to the start of the company in 2015. He has a lot of power as he holds both the position of chairman of the board and CEO. He was also on the board of a current competitor, Markforged (MKFG) from 2013 to 2015 and led their seed investment round and Series A funding, which I will revisit later.

What’s also great about a growth company is having a go-to-market plan with a comprehensive sales team like Desktop Metal, especially since generating initial sales is so important, in order to subsequently generate passive revenue. They currently have over 200 partners and over 100 support representatives in over 65 countries.

Desktop Metal’s Management With Ric Fulop (Left Pircure) (Desktop Metal Press Kit)

Competition & USP

As Desktop Metal aims to capture a market share of as much as 10% in the Additive Manufacturing market by 2030, it’s a good idea to take a look at where its competitors stand and what they’re doing.

Some of Desktop Metal’s biggest competitors include 3D Systems (DDD), Stratasys (SSYS), EOS (privately held), GE Additive (GE), Materialise (MTLS), Markforged (MKFG) and others. Management also recently acquired one of their competitors, ExOne. The management also recently acquired one of their competitors, ExOne. Unlike other companies in the industry, Desktop Metal has generated stunning revenue growth by employing an aggressive merger, acquisition and R&D strategy.

In fact, Desktop Metal’s positioning is also profoundly strategic, as the company’s primary focus is on end-use components, which according to research will show the strongest growth, from US$2.8BN today to approximately US$19BN in 2030.

Desktop Metal’s USP (Desktop Metal IR)

Compared to Stratasys, 3D Systems and General Electric, Desktop Metal is still in the early stages of its growth. Revenues are still growing exponentially at 583% year-over-year and gross margin is rising, indicating the potential for future profitability. A good competitor to keep an eye on is Markforged, an additive manufacturing company that is also in the early stages of development. They are showing steady growth and an increasing gross margin that is currently above 55%.

In contrast to other companies, Desktop Metal has its own product lines, Desktop Health and Forust, which are heavily focused on the healthcare/dental and 3D wood printing industries. This allows Desktop Metal to target a larger market segment and compete by disrupting the industry with innovative manufacturing technologies.

Market Analysis

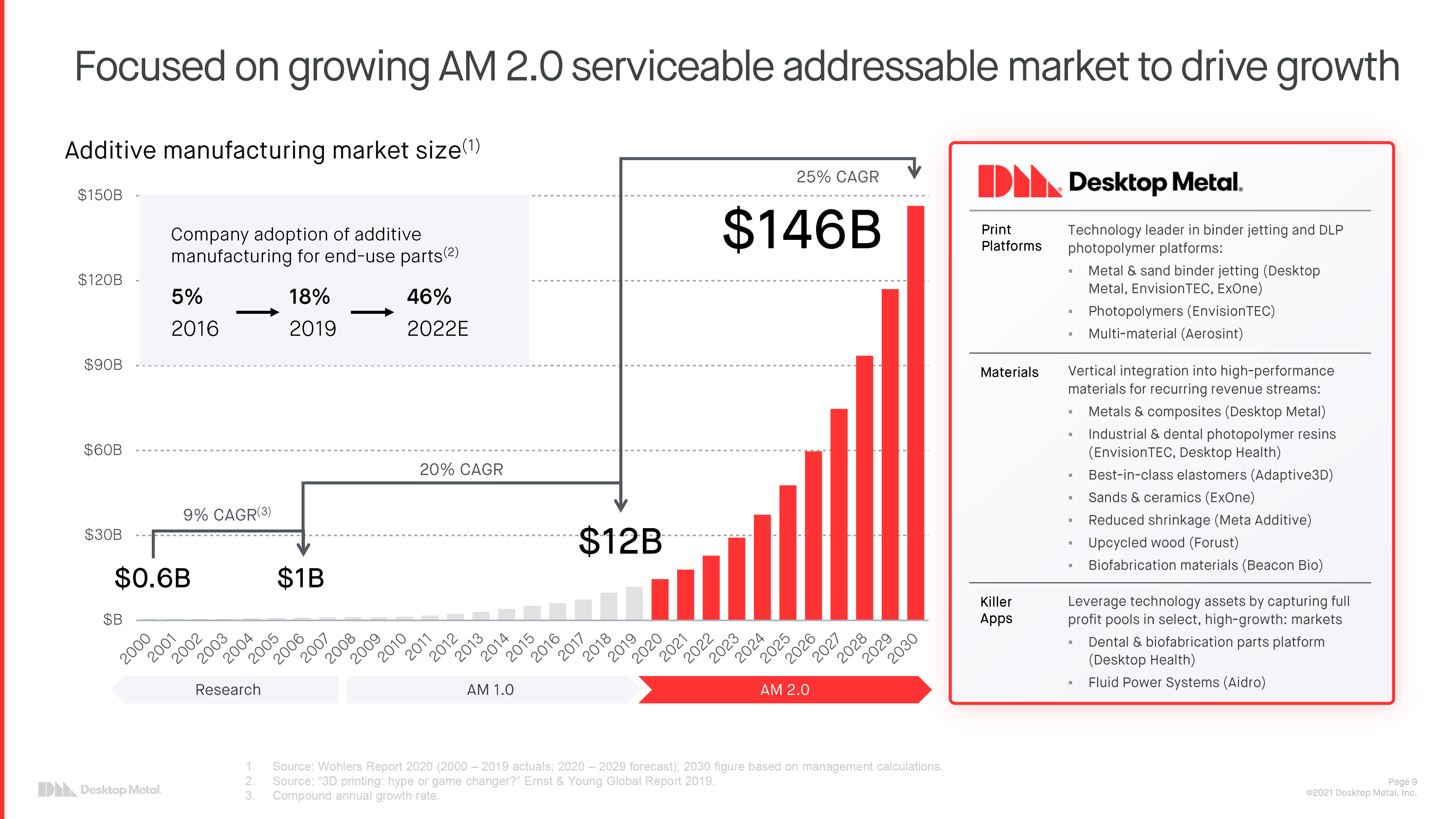

The Additive Manufacturing industry is expected to grow exceedingly fast, with a CAGR between 15% and 25%. Estimates of how big the market will become by 2030 range from US$51BN to US$115BN, although Desktop Metal’s management seems to regard it as a US$146B opportunity, based on their own 2030 calculations.

This broader market scope may be warranted, as the company is also active with Desktop Health, which offers an additional US$30B opportunity in the dental industry. Along with another entity of the company, called Forust, which focuses on high-volume 3D printing of wood, providing an opportunity to disrupt the global finished wood products market worth US$1.3T.

Additive Manufacturing Market Growth (Desktop Metal IR)

According to global consulting firm A.T. Kearney, 3D printing will disrupt a manufacturing market estimated at US$12T. Even at 1% market penetration, the 3D Printing industry would have an opportunity to capture a US$120 billion market share, compared to about US$25 billion today.

Valuation

Giving a valuation to Desktop Metal remains a tedious task, as there are many variable parameters involved, such as future operating expenses, management performance, market growth, so on and so forth. As a proxy, I will use the average P/S ratio of the S&P 500, which is currently averaging 3.04.

Desktop Metal’s management has given the target of achieving sales of approximately US$1BN by 2025, which they still stand behind as of December 2021. Assuming an average P/S ratio of 3.04, Desktop Metal should exhibit a market capitalization of US$3.04BN by 2025, or approximately US$9.73 per share, up 166.58% from US$3.65 per share.

While this seems like a great opportunity, we don’t yet know if Desktop Metal will be able to generate enough net income by 2025 to meet such expectations. Based on S&P’s current average P/E ratio of 21.67, Desktop Metal would need to generate approximately US$140.29M in annual net revenue to live up to its US$3.04BN market capitalization, from which they are still a long way off.

But that does not diminish the long-term vision of Desktop Metal’s management, which aims to capture a market share of more than US$10BN by 2030. Even assuming low margins and a P/S ratio of merely 1, the company would still have a market capitalization of US$10B by 2030. This translates into a price of US$32 per share, up 776.71% from today. However, it remains to be seen whether it will be possible for management to deliver on these lofty promises.

No Risk, No Reward?

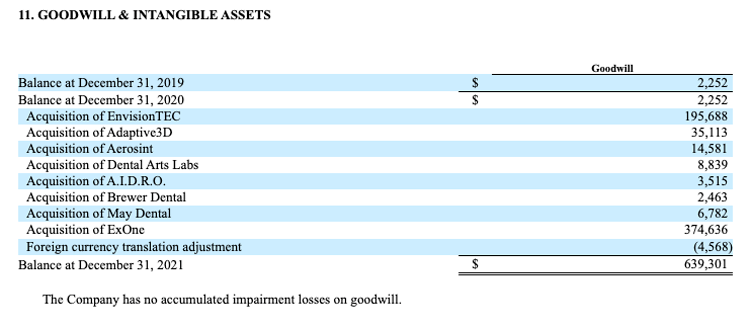

One of the other major risks may include the amount of money Desktop Metal’s management has spent on acquisitions in the past. According to the latest 10-K, the company has amassed a total of more than US$639M in goodwill, almost all of which comes from acquisitions made in 2021. Last November, for example, management paid a hefty price tag for ExOne, for a total of US$613.0M consisting of US$201.4M in cash and US$411.6M in common stock compensation.

Desktop Metal’s Goodwill Breakdown (Desktop Metal 10-K, SEC)

It comes as no surprise that much of this was funded by issuing more shares, diluting current shareholders, to partially fund these acquisitions. Since the third quarter of 2020, the number of shares outstanding has increased from 226.7 million to 312.2 million in the fourth quarter of 2021, resulting in a 37.72% dilution of the existing shareholders.

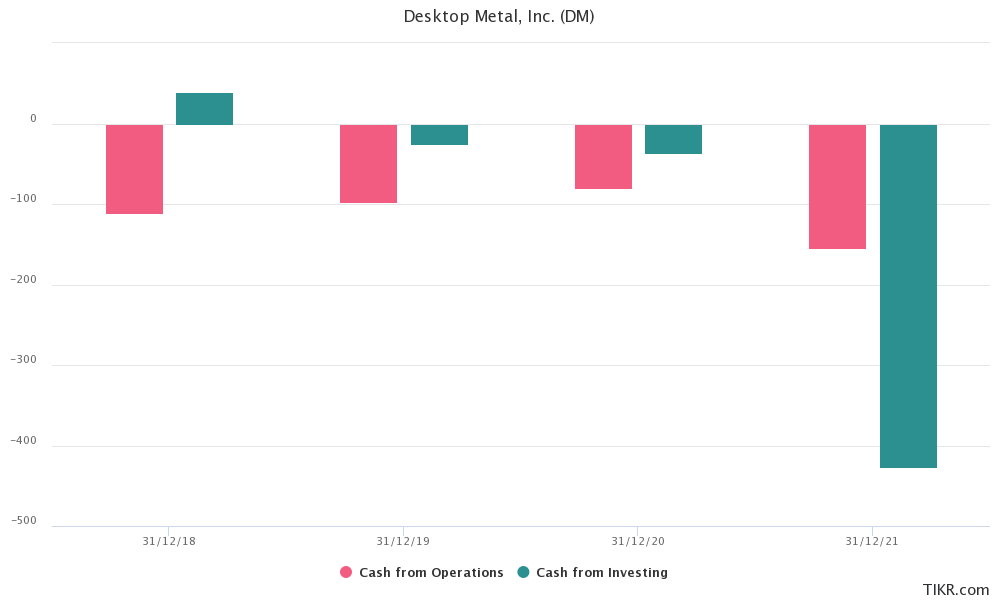

Another question that arises is whether Desktop Metal will need to raise more money in the future, and if so, how much. Their cash flow statement shows that Desktop Metal has spent over US$155M in cash on operating activities. According to their balance sheet, they currently have US$271.7M in cash, cash equivalents and short-term investments as of the fourth quarter of 2021.

Desktop Metal’s Cash Flow Highlights (TIKR Terminal)

In their forecast for 2022, management expects adjusted EBITDA of negative US$90M, compared to adjusted EBITDA of negative US$96.09M in 2021. Absent other acquisitions or unplanned expenses, we can expect Desktop Metal to survive 1-3 years before raising more cash or becoming profitable. Currently, management is targeting 2023 to become EBITDA profitable, which would leave the prospect of no further dilution on the table.

According to Seeking Alpha’s Quant Rating, Desktop Metal appears to be severely lacking in terms of profitability and momentum, but receives a positive rating in terms of growth and valuation. Currently, the Quant Rating for Desktop Metal is labeled as “sell”. View Seeking Alpha’s complete Quant Rating for Desktop Metal here.

Conclusion

In my opinion, the company may incur larger losses in the near term due to uncertain macroeconomic sentiment and the risk-off environment. Especially after the inversion of the yield curve, which has signaled recessions in the past, plus negative outlook for GDP growth and hot CPI data.

Since Desktop Metal does not yet have a strong FCF, a high cash burn of US$150M+ and elevated fundamentals, it is susceptible to more selling pressure in the near term. Looking ahead, however, Desktop Metal may be well on its way to outperforming the broad benchmarks if they maintain their current rate of growth.

Is this company capable of becoming a 10-Bagger in the future? Possibly. Is it risk-free? Not really. That’s why I currently have a small portion of my portfolio dedicated to the company, to weather the storm.