industryview/iStock via Getty Images

On Wednesday, February 9, 2022, midstream giant DCP Midstream, LP (DCP) announced its fourth-quarter 2021 earnings results. The headline numbers were actually quite reasonable as DCP Midstream posted incredibly strong year-over-year revenue growth along with a respectable net income figure. As I have pointed out a few times in the past though, net income is not a particularly important figure for a midstream company because they suffer from substantial amounts of depreciation. Despite the strong year-over-year improvement in the company’s headline financial figure, the company’s actual financial performance was fairly similar to what DCP Midstream had in 2020. This is one of the most important characteristics possessed by midstream partnerships like DCP Midstream. Basically, these companies enjoy remarkably stable cash flows regardless of conditions in the broader economy or changes in energy prices. This is what makes these companies such incredible income vehicles and indeed DCP Midstream’s 5.13% current yield is nothing to sneeze at.

As my long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company’s earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from DCP Midstream’s fourth-quarter 2021 earnings report:

- DCP Midstream reported total operating revenues of $3.477 billion in the fourth quarter of 2021. This represents a 94.79% increase over the $1.785 billion that the partnership brought in during the prior-year quarter.

- The company reported an operating income of $252 million in the most recent quarter. This represents a 460% increase over the $45 million that the company reported in the year-ago quarter.

- DCP Midstream transported an average of 895,000 barrels of natural gas liquids per day in the reporting period. This compares quite favorably to the 692,000 barrels of natural gas liquids per day that the company averaged last year.

- The company reported a distributable cash flow of $219 million in the current quarter. This represents a 23.03% increase over the $178 million that the company reported in the equivalent quarter of last year.

- DCP Midstream reported a net income attributable to its partners of $315 million in the fourth quarter of 2021. This represents a substantial 266.28% increase over the $86 million that the company reported in the fourth quarter of 2020.

It is certainly not news to anyone reading this that energy prices have increased substantially over the course of 2021. At first, one might credit this for the significant improvements that we see in DCP Midstream’s results compared to the prior-year quarter. This would not be a correct assumption, however. In fact, DCP Midstream is minimally affected by changes in energy prices due to the business model that it utilizes. In short, DCP Midstream enters into long-term (typically five to ten years in length) contracts with a customer that requires its midstream services, such as resource transportation. The customer then compensates DCP Midstream based on the volume of the resources that are sent through the infrastructure and not on their value. This business model thus provides a great deal of insulation against changes in commodity prices. We can also see in this model the biggest source of the financial improvements that were in the company’s results. As noted in the highlights, DCP Midstream saw a dramatic increase in its natural gas liquids volumes compared to the year-ago quarter. The volume increase was not limited to the company’s long-haul liquids pipelines either. The company also saw volume increases across its natural gas gathering and processing infrastructure. This was due largely to production increases in both the Permian and DJ Basins. As DCP Midstream makes its money off volumes, we can clearly see that the higher volumes should result in higher overall cash flows.

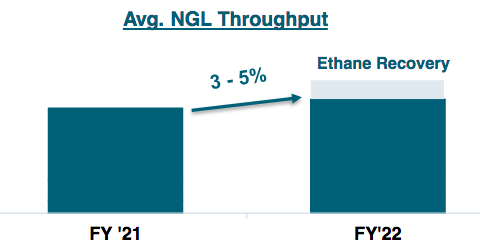

Unfortunately, DCP Midstream’s ability to continue to benefit from volume growth going forward may be somewhat limited over the near term. This is due to the cutbacks in spending that the company made following the commodity price crash in 2020. As I discussed in a previous article, DCP Midstream drastically reduced its spending following that event and canceled or deferred many of the growth projects that it was working on back in 2019. As is the case with any infrastructure, pipelines and other midstream facilities only have a limited amount of capacity that they can handle so in order to significantly increase the volume of resources that it can carry, DCP Midstream needs to construct new facilities. It is not doing that, however. With that said, the company does expect some volume increases in 2022 since not all of its pipelines are currently running at maximum capacity. This is particularly true for the Southern Hills and Texas Express systems that serve the DJ Basin. This basin has begun to see some growth in production recently, which could result in DCP Midstream seeing a small 3-5% volume increase in 2022:

DCP Midstream Q4 2021 Earnings Presentation

It is also somewhat questionable how much volume growth the company will see over a long-term horizon. As I pointed out before, at the Goldman Sachs Energy Conference last month, many shale producers expressed a willingness to allow production to stagnate or even decline slightly despite the sharp increase that we saw in energy prices last year. The reason for this is that shareholders have been demanding that shale energy companies deliver higher returns in order to bring them more into line with other sectors of the market. These demands have led these companies to change their business model from growth at all costs to maximizing cash flow. This is being accomplished by reducing capital expenditures, primarily on production growth spending. However, the business environment has changed somewhat since then and as crude oil prices continue to rise, producers have been finding that they can both generate a high free cash flow and still grow production. For example, Continental Resources (CLR) stated in its earnings report that it expects production growth in 2022. If other companies follow suit, DCP Midstream may need to resume some of its deferred projects and thus return to a state of growth.

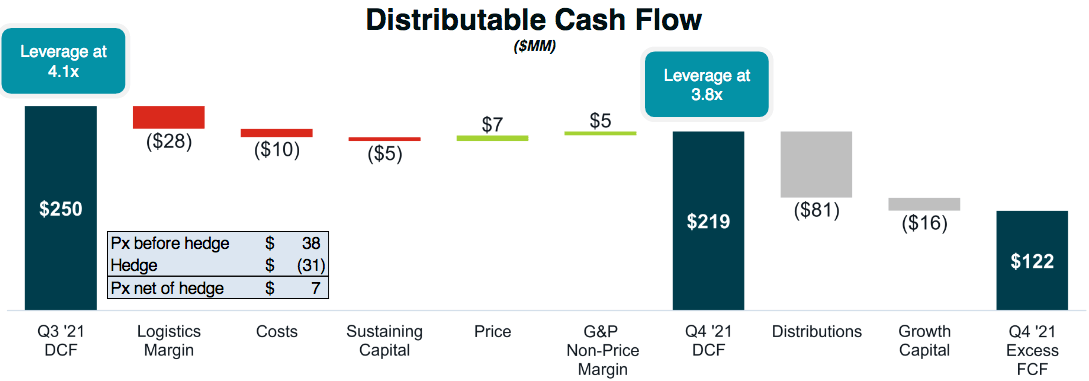

As already mentioned, one of the defining characteristics of midstream companies is that they tend to enjoy remarkably stable cash flows regardless of resource prices or macroeconomic conditions. The company’s 2020 distribution cut may seem to be at odds with this but in fact, DCP Midstream did not technically have to cut the distribution at that time. The primary purpose of the cut was to improve the company’s financial self-sufficiency by providing it with a significant amount of free cash flow above what it pays out to investors. In the fourth quarter of 2021, DCP Midstream had $122 million in cash flow beyond its distribution payments and a small amount of capital devoted to growth spending:

DCP Midstream Q4 2021 Earnings Presentation

This excess cash flow allows the company to accomplish a variety of other tasks. The most important of these may be debt reduction, which DCP Midstream has been focusing a great deal of effort towards lately. We can see this by looking at the company’s leverage ratio, which is also known as the net debt-to-adjusted EBITDA ratio. This ratio basically tells us how long it would take the company (in years) to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task. At the end of the fourth quarter of 2021, this ratio stood at 3.8x, which is significantly better than the figure held at the end of 2020. This improvement has made management optimistic that the company will be able to shortly get this ratio down to 3.5x, which is the company’s long-term target. This target would give DCP Midstream a very attractive ratio for a midstream company, one that is significantly below the 5.0x that analysts generally consider to be reasonable so this is something that any investor should be able to appreciate.

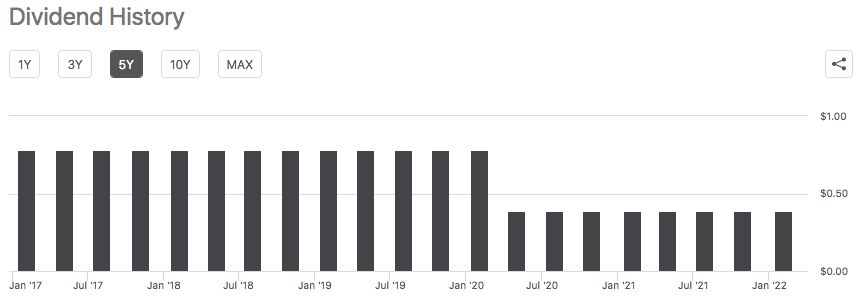

One of the biggest reasons why investors buy into midstream companies like DCP Midstream is that they typically have higher yields than most other things in the market. DCP Midstream is certainly not an exception to this as its common equity yields 5.13% as of the time of writing. Unfortunately, the company has not always been consistent with its payout as it cut the distribution back in 2020:

Seeking Alpha

While this distribution cut is no doubt disheartening, it is important to keep in mind that the current distribution is what someone buying today would receive. As such, the current distribution is the most important thing so let us ensure that the company can actually afford it. After all, we do not want the company to be forced to reverse course and cut the distribution again. That scenario would, of course, reduce our incomes and almost certainly cause the unit price to decline. The usual way that we judge a company’s ability to pay its distribution is by looking at its distributable cash flow, which is a non-GAAP metric that theoretically tells us the amount of cash that was generated by the company’s ordinary operations that is available for distribution to the limited partners. As stated in the highlights, DCP Midstream reported a distributable cash flow of $219 million in the fourth quarter of 2021. However, the distribution only costs the company $81 million at the current level. Thus, the company has sufficient cash flow to cover its distribution 2.70 times over. Analysts generally consider anything over 1.20x to be reasonable and sustainable so we can clearly see that DCP Midstream should have no trouble maintaining its current distribution going forward and indeed has some headroom to increase it. The company’s management suggested that it might do just that during the fourth-quarter conference call, once the debt reduction goal has been achieved.

In conclusion, this was quite a respectable quarter for DCP Midstream, although it was perhaps not quite as impressive as the headlines would lead someone to indicate. We can see though that the industry has begun to return to its former glory. It is uncertain whether or not the company will ever have the growth potential that it did prior to the pandemic but the reduction in leverage could lead it to boost the distribution, which should appeal to income investors. Overall, this company is looking better and better.