This article was highlighted for PRO+ subscribers, Seeking Alpha’s service for professional investors. Find out how you can get the best content on Seeking Alpha here.

CVD Equipment (CVV) can revive its fortunes on the back of increasing material sales and a resurgence in equipment sales.

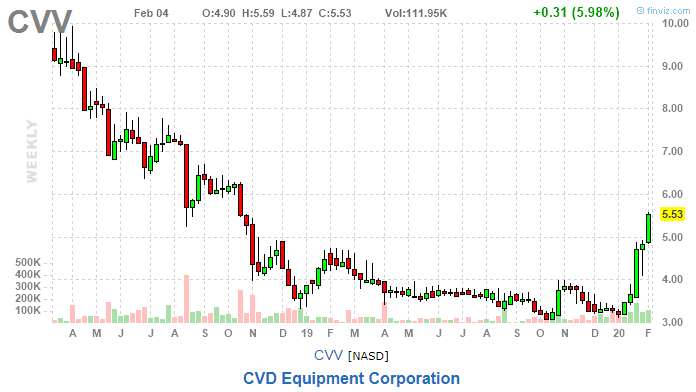

The shares of CVD Equipment have been lingering for years, only to be suddenly waking up in January:

The stock chart is merely following company developments, as they usually do:

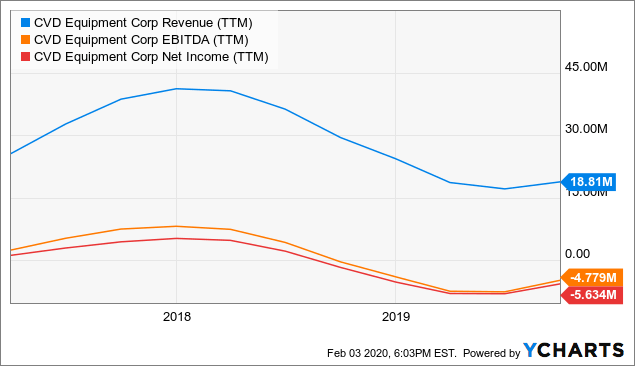

Data by YCharts

Data by YChartsBut there are definitely signs of stabilization and even some operational improvements, but nothing spectacular, at least not yet. So we ask whether the stock is running ahead of itself, or whether there is mileage in this rally still.

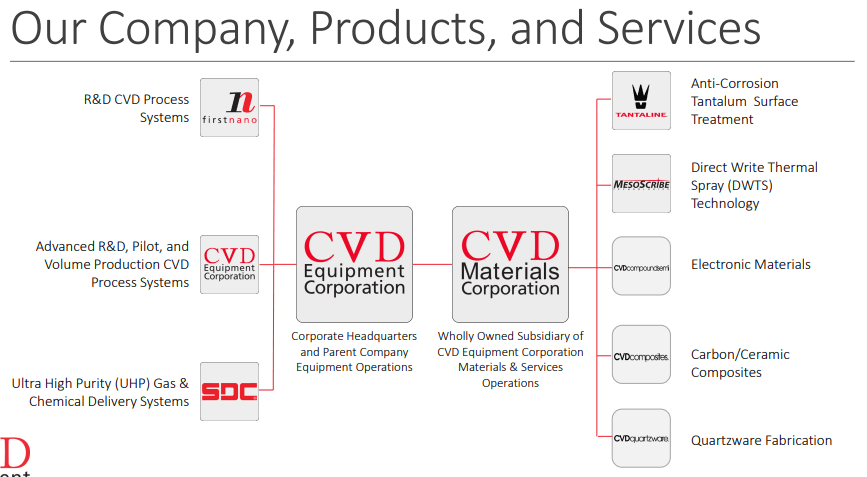

The Company operates through three segments:

- CVD: CVD Equipment Corporation (CVD or chemical vapor deposition equipment manufacturing).

- SDC: stainless Design Concepts, the Company’s ultra-high purity manufacturing division in Saugerties, New York for gas control systems.

- Materials: the Materials segment was established to provide quartzware and material coatings for aerospace, medical, electronic and other applications.

Here are the Q3 results per segment, from the Q3 10-Q:

So it’s clear that CVD is still by far the biggest segment. Q3 combined revenue looks like a really nice 41.6% jump y/y but when taken over the first nine months of the year the picture changes quite a bit (a decrease of 28.1%).

Investors should keep in mind that with equipment sales, which is still by far the biggest revenue source, quarterly results can be quite lumpy so it’s more meaningful to look at 12 month trends. Here is what the company does, from the October 29 Investor Day Presentation:

Growth

- Equipment revival

- Materials

Materials

While starting from a very small base, their materials segment actually contains considerable hope for adding to a revival of the company’s fortunes as it serves multiple needs, from the Q3CC:

The expanded material operations will enhance our capabilities in providing corrosion resistant coatings through Tantaline for medical, pharma, oil and gas applications; sensors through MesoScribe for defense, aerospace and turbine applications; and through our CVD Materials subsidiary for carbon composite materials, medical coatings, electronic substrate materials and further expansion into other coatings for defense, aerospace and industrial applications.

And of course, there are additional benefits, like higher margins and less quarterly volatility (Q3CC):

We anticipate the high margin growth markets in materials for corrosion resistance, medical, aerospace and defense coatings will help flatten the uneven levels of our equipment sales.

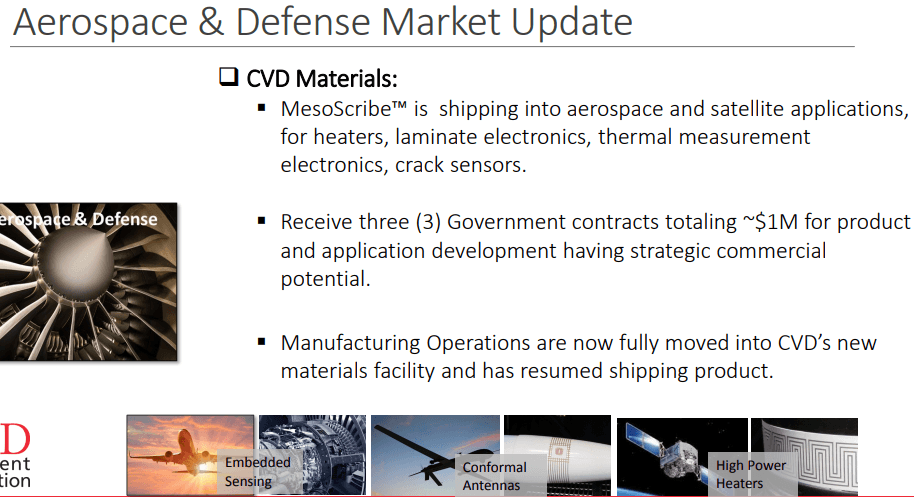

In November 2017, the company acquired the assets of MesoScribe, from the PR:

MesoScribe™ specializes in the manufacturing of harsh environment sensor products and structurally integrated electronics based on its proprietary Direct Write Thermal Spray (DWTS) Technology. Direct Write devices are robust and reliable, and integrated process automation enables precision manufacturing and high throughput production for cost-effective implementation. MesoScribe’s focus is on developing innovative sensor prototypes and manufacturing Direct Write devices in production quantities for advanced sensing and communications.

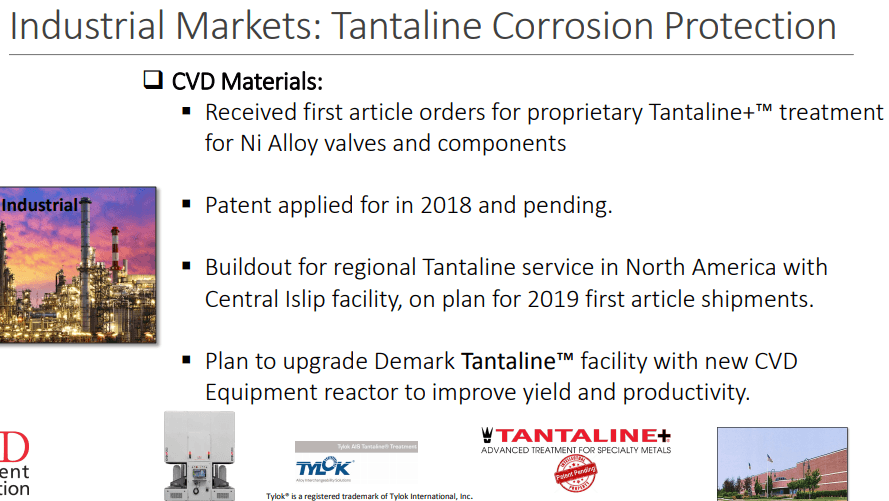

The acquisition basically gave CVD access to another deposition technology complementing their Tantaline CVD Tantalum deposition technology acquired the year before.

Revenues are still tiny because the facility to produce MesoScribe has been moved from California to Long Island New York and it has just come online. The facility to produce Tantaline, while up, is still in testing phase and it won’t be fully up until after H1 2020.

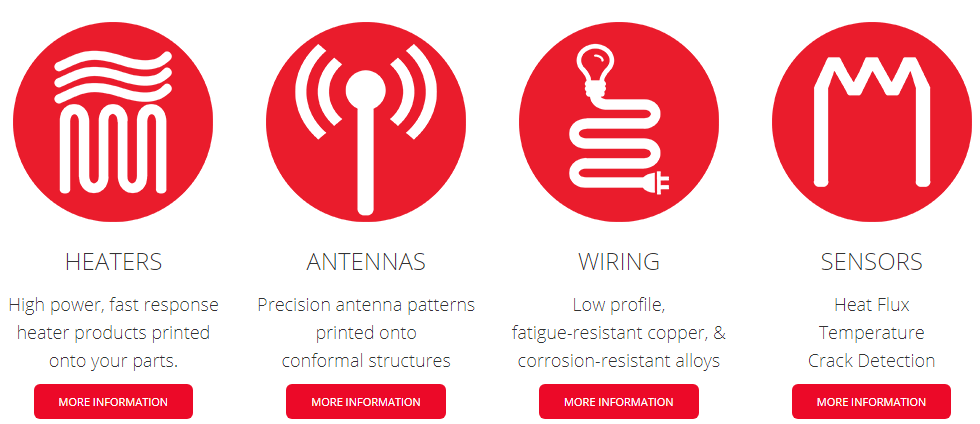

MesoScribe direct write printed electronics have applications in multiple industries, from the company website:

And some recent orders in the defense market, from the October 29 Investor Day Presentation:

So there is some momentum developing here.

Tantaline offers industrial grade corrosion protection, from the October 29 Investor Day Presentation:

When asked on the Q3CC by a private investor whether the materials segment could be a $5M, $10M, $20M business in 3-5 years, the answer from management was an emphatic yes.

In the short-term, not too much can be expected as it starts from a very low base, but the coming quarters are going to provide at least some indication as the new plants become fully operational.

Equipment sales

While materials come from a small base and need to ramp, for more immediate prospects equipment sales are paramount. While the first nine months of the year were disappointing, with sales declining by $5.5M (-28.1%), Q3 figures produced a recovery both y/y ($1.7M or +41.6%) and sequentially ($0.8M or +16.3%).

And more importantly still, backlog is also improving (Q3CC):

during the third quarter, we received orders of approximately $7.9 million, as compared to $3.3 million in Q2 and $6.5 million in Q1 of 2019. This lifted order backlog, which at September 30 was $6.7 million as compared to $4.5 million at June 30, an increase of $2.2 million or 49%.

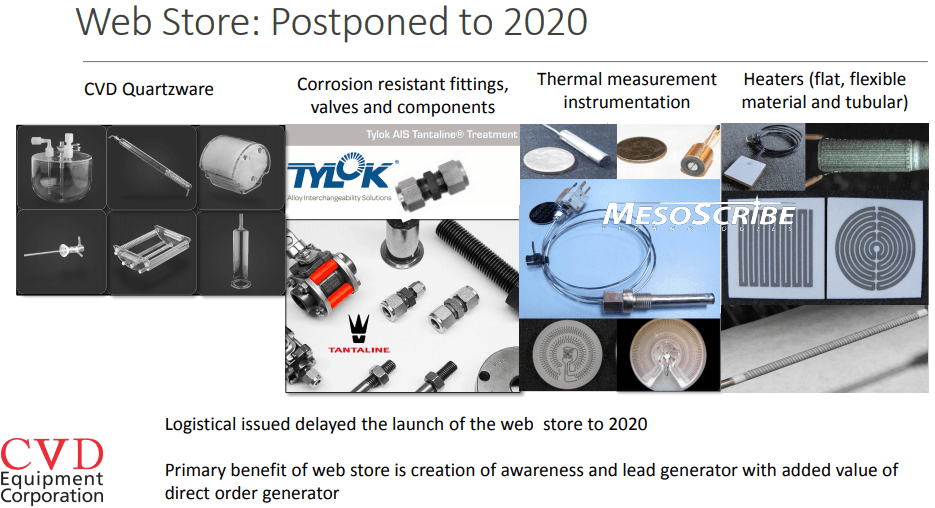

Another avenue for increased sales is online, but there has been a snag here, with capabilities only coming online this year, from the October 29 Investor Day Presentation:

Q3 results

We’ve already given the segment results and backlog and below are margins and cash flow. There is improvement but the curious thing is that the shares didn’t jump on the Q3 results mid November, the rally started only in January. There was a 15% jump mid October on the Q3 order figure, but that rally faded pretty fast.

The below table breaks down revenue from contracts with customers and how they are distributed among different industries, from the Q3 10-Q:

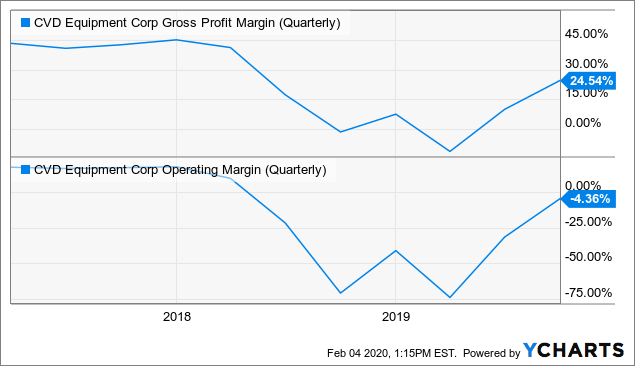

Margins

There was quite a notable recovery in margins in Q3:

Data by YCharts

Data by YChartsThis was the result of increased sales and resulting operating efficiencies, product mix and cost cutting but at least the GAAP version of operating margin is inflated by a one-time $200K recovery of the final contingent earn-out related to our MesoScribe acquisition, but there was still $188K in permanent reduction of OpEx.

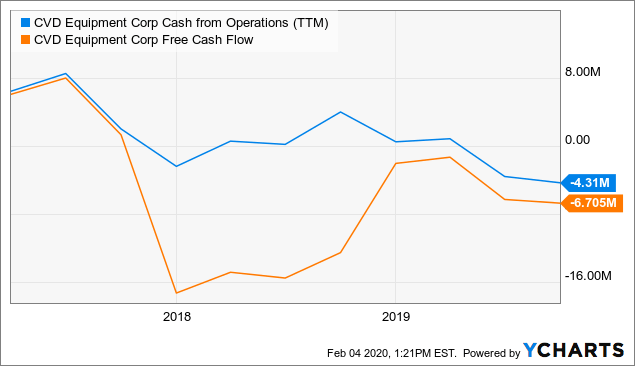

Cash

Data by YCharts

Data by YChartsEven operational cash flow has now moved negative, but at least it’s quite likely CapEx will decline going forward (Q3CC):

The company has invested $2.5 million during 2018 in building improvements, machinery and other expenses related to CVD Materials, and $2.1 million in the first nine months of 2019.

With the MesoScribe facility moved completed and the Tantaline plant having started production in Q4 CapEx needs are likely to become less going forward.

Data by YCharts

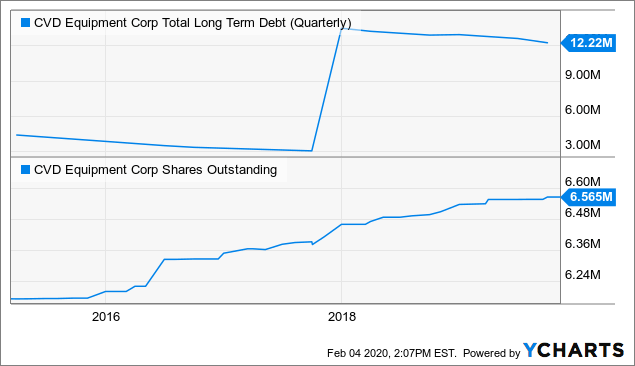

Data by YChartsThe company still has $11.5M in long-term debt and $6.7M in cash and equivalents. Dilution has been fairly minimal.

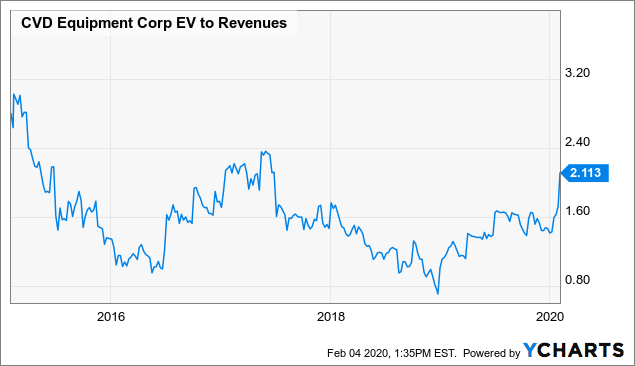

Valuation

Data by YCharts

Data by YChartsWith little growth and barely 25% gross margin the shares aren’t all that cheap. We have to get back to 2017 when the company earned a profit with an EPS of $0.87 but despite the expected progress that seems a bit of a stretch for next year.

Conclusion

A revival of orders in Q3 together with putting the materials plants in operation, cost cutting and lower CapEx is brightening the outlook for the company.

While all this basically old news known by mid-November as a result of the Q3 figures, the stock price only now reacts, and it does so with considerable vigor.

While that is somewhat curious, perhaps tax loss selling prevented the rally at the end of last year, and January has a habit of being friendly for small cap stocks. We haven’t come across any more recent bullish news, we have to admit.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.