Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Creative Peripherals and Distribution Limited (NSE:CREATIVE) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Creative Peripherals and Distribution

What Is Creative Peripherals and Distribution’s Debt?

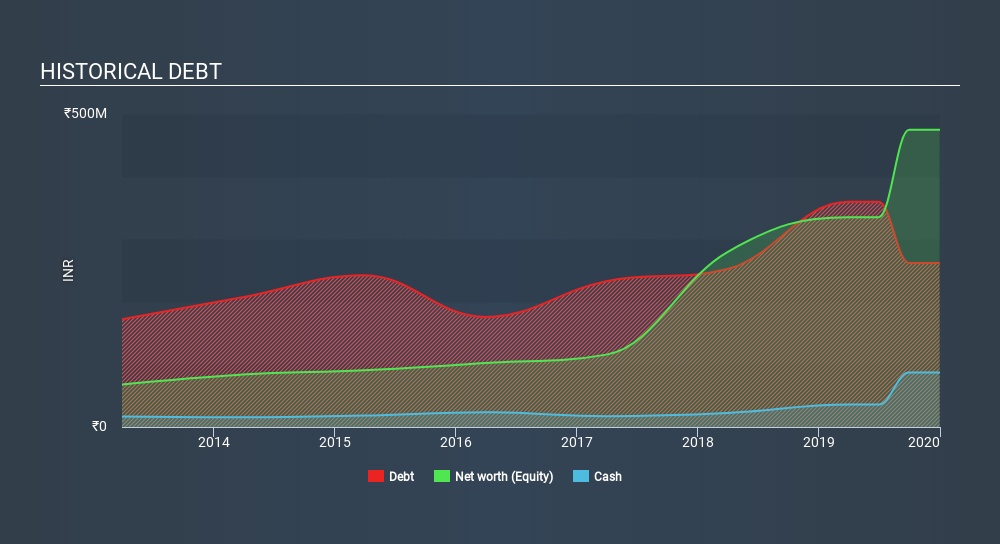

As you can see below, Creative Peripherals and Distribution had ₹262.1m of debt at September 2019, down from ₹359.7m a year prior. On the flip side, it has ₹86.9m in cash leading to net debt of about ₹175.2m.

A Look At Creative Peripherals and Distribution’s Liabilities

The latest balance sheet data shows that Creative Peripherals and Distribution had liabilities of ₹792.5m due within a year, and liabilities of ₹11.0m falling due after that. Offsetting these obligations, it had cash of ₹86.9m as well as receivables valued at ₹463.8m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹252.8m.

Creative Peripherals and Distribution has a market capitalization of ₹1.18b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Looking at its net debt to EBITDA of 1.2 and interest cover of 3.6 times, it seems to us that Creative Peripherals and Distribution is probably using debt in a pretty reasonable way. So we’d recommend keeping a close eye on the impact financing costs are having on the business. Importantly, Creative Peripherals and Distribution grew its EBIT by 60% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is Creative Peripherals and Distribution’s earnings that will influence how the balance sheet holds up in the future. So if you’re keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Creative Peripherals and Distribution burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Creative Peripherals and Distribution’s conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered were considerably better. In particular, we are dazzled with its EBIT growth rate. When we consider all the factors mentioned above, we do feel a bit cautious about Creative Peripherals and Distribution’s use of debt. While we appreciate debt can enhance returns on equity, we’d suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Consider for instance, the ever-present spectre of investment risk. We’ve identified 2 warning signs with Creative Peripherals and Distribution (at least 1 which doesn’t sit too well with us) , and understanding them should be part of your investment process.

If, after all that, you’re more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at [email protected]. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

The easiest way to discover new investment ideas

Save hours of research when discovering your next investment with Simply Wall St. Looking for companies potentially undervalued based on their future cash flows? Or maybe you’re looking for sustainable dividend payers or high growth potential stocks. Customise your search to easily find new investment opportunities that match your investment goals. And the best thing about it? It’s FREE. Click here to learn more.