DNY59/E+ via Getty Images

Costamare (NYSE:CMRE) reports many years of expertise in the bulk shipping industry. In addition, management is entering new industries like the dry bulk shipping industry. With a significant amount of cash in hand to pay further capital expenditures and perhaps acquisitions, Costamare appears to have a very interesting business story. If the share count does not increase, and the debt level lowers, the expected free cash flow will likely justify an eventual increase in the stock price.

Costamare Is buying Its Own Shares And Entering New Markets

Costamare Inc. presents itself as one of the world’s leading providers of containerships for charter.

Also, with more than 48 years of accumulated expertise in the international shipping industry, in my view, management has accumulated a significant amount of know-how, which will most likely help Costamare navigate in the future.

I believe that it is a good time to review the expectations of Costamare. Management was optimistic about the future and about the year 2022. Keep in mind that Costamare has covered almost all of its container ship open days for 2022. It means that financial analysts do have a lot of visibility about future net revenue and free cash flow for 2022:

We have covered substantially all of our containership open days for 2022 and are in the process of arranging employment for the vessels coming off charter next year. Source: CMRE Earnings release Q4 2021

It is also quite beneficial that Costamare seems ready to enter new markets like the dry bulk shipping business. Management noted that it expects generating healthy returns thanks to acquisitions in this sector:

Regarding our expansion into the dry bulk shipping business, we entered a market with favorable supply and demand dynamics underpinned by a historically low orderbook. Our dry bulk fleet is currently trading in the spot market generating healthy returns, on the back of timely acquisitions. Source: CMRE Earnings release Q4 2021

On the dry bulk side, the market continues to be strong with smaller ships earning a premium to the larger ones, also benefiting from container spillover. Supply and demand dynamics remain healthy underpinned by a historically low orderbook. Source: First Quarter Ended March 2022

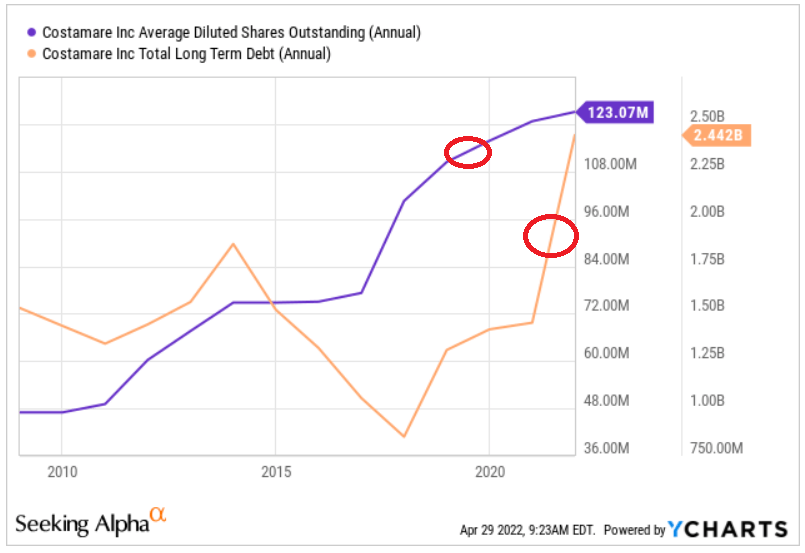

With the previous information, what made me write a report was the fact that Costamare is buying its own shares. In my view, if treasury shares continue to increase, other investors may decide to acquire shares too, which would likely push the stock price up:

On November 30, 2021, we approved a share repurchase program. The timing of repurchases and the exact number of shares to be purchased will be determined by the Company’s management, in its discretion. Source: CMRE Earnings release Q4 2021

Beneficial Estimates

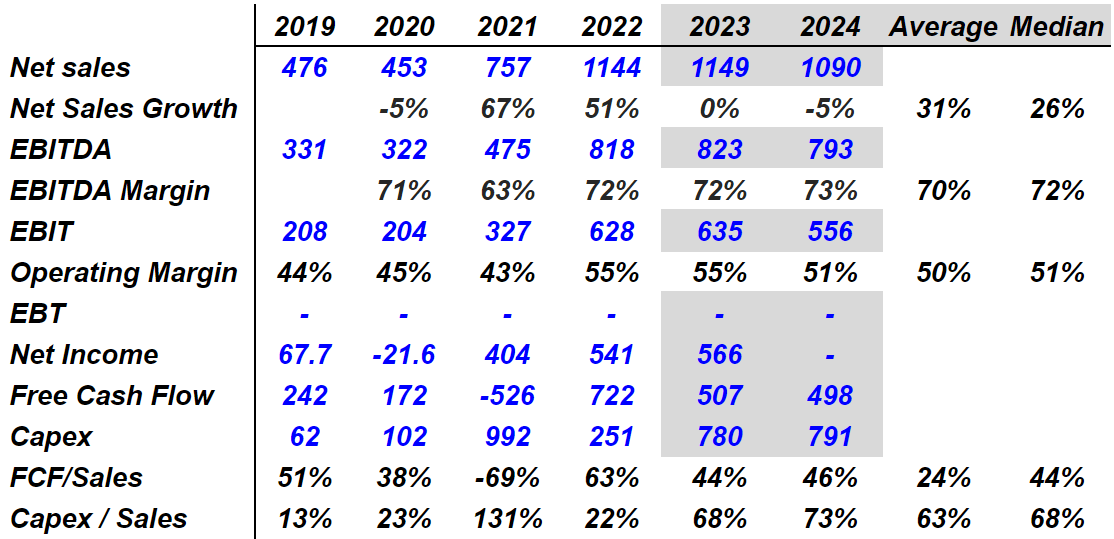

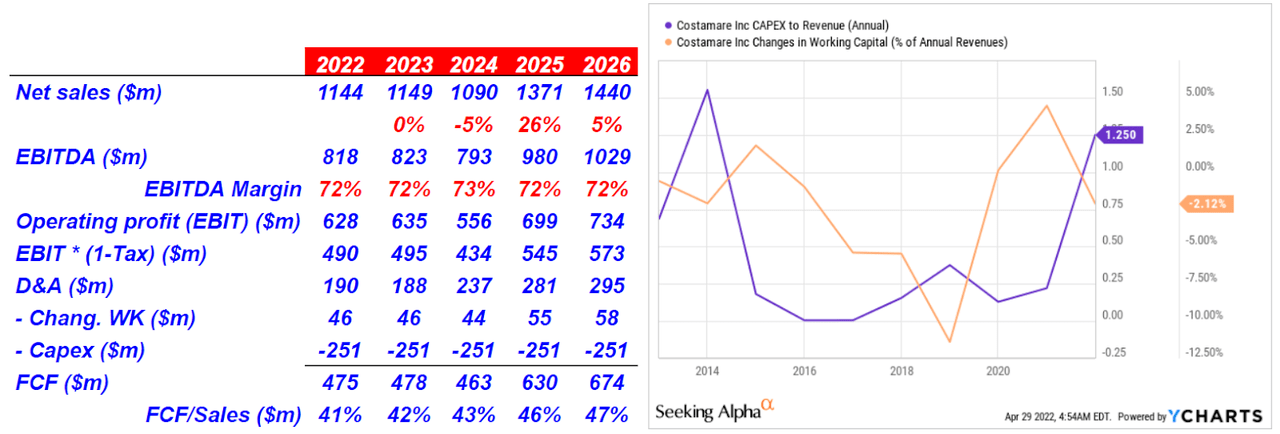

After massive sales growth of 67% in 2021 and 51% in 2022, estimates include a decline in sales growth in 2023 and 2024. With that, it is quite beneficial that the EBITDA margin will stand at a median close to 72%, and the median operating margin will not be lower than 51%. If we also mention that the free cash flow will likely increase because of the expected decrease in capex, in my view, Costamare becomes very interesting.

marketscreener.com

Balance Sheet

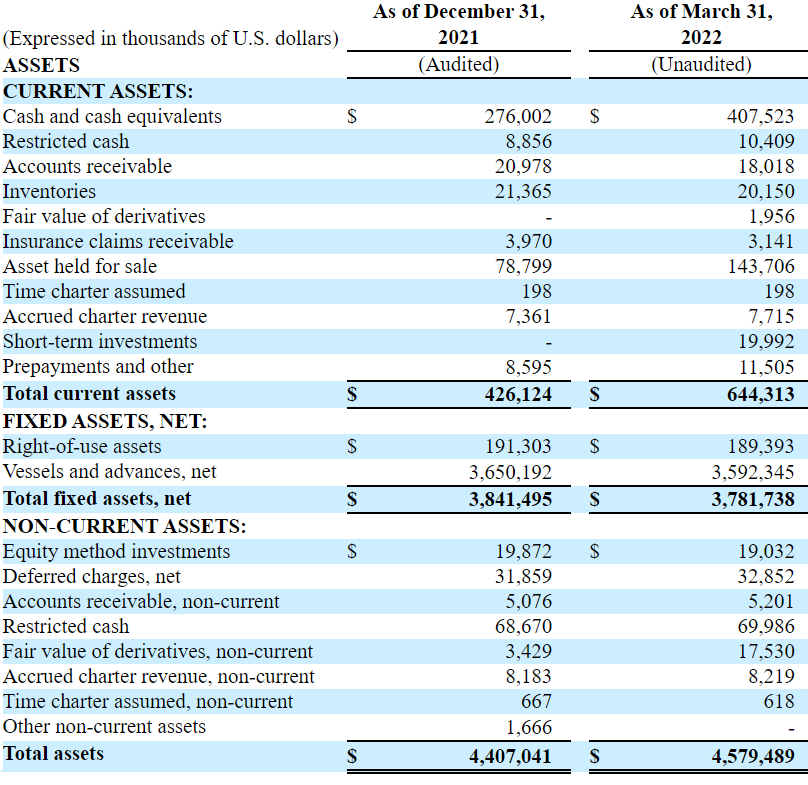

As of March 31, 2022, Costamare reported $407 million in cash and vessels worth $3.6 billion. In my view, the company has a significant amount of cash, which will help management enter new markets and acquire competitors. In my view, the company’s financial situation appears healthy:

Balance For March 31, 2022

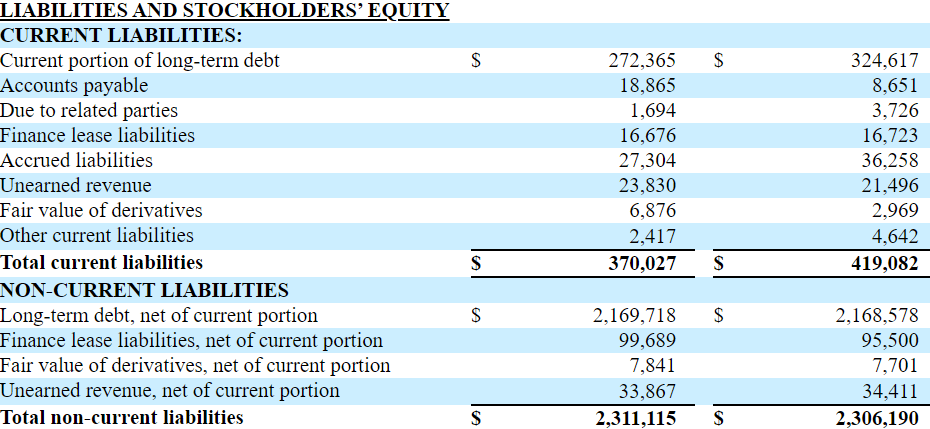

The total amount of debt is equal to $2.1 billion, which is not a small amount. However, with more than $3.5 billion in the form of vessels, I wouldn’t worry about the financial debt. If the company needs to pay lenders, it will most likely sell some fixed assets. In this regard, keep in mind that Costamare has several vessels for sale:

During the year ended December 31, 2021, the container vessels Messini, Sealand Illinois, Sealand Michigan and York were classified as vessels held for sale. No loss on vessels held for sale was recorded since each vessel’s estimated fair value less costs to sell exceeded each vessel’s carrying value. During the year ended December 31, 2020, the container vessel Halifax Express was classified as a vessel held for sale and we recorded a loss on vessels held for sale of $7.7 million, which resulted from its estimated fair value measurement less costs to sell, during the year. Source: 20-F

Balance For March 31, 2022

If The Company Continues To Buy Vessels, Reduces Debt, And The Share Count Does Not Increase, The Fair Price Could Reach $29

Under normal conditions, I wouldn’t expect significant sales growth declines in 2023 and 2024 because the company has already signed a lot of agreements with clients in the future. In my view, most financial advisors will likely appreciate the following table, where management reported that even in 2025 the container ship contracted/total container ship days ratio stands at more than 57%.

20-F

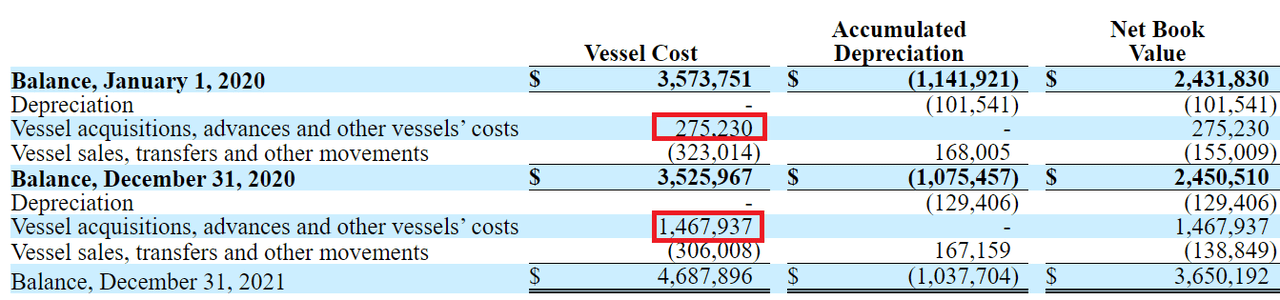

In my view, if Costamare continues to acquire new vessels like in 2020, revenue expectations will most likely trend north. Under normal conditions, if sufficient equity researchers do note the increase in vessels, their free cash flow expectations will increase. As a result, management may enjoy stock demand, which could lower the cost of equity, and push the company’s stock valuation north.

20-F

In this scenario, I expect management to try to decrease its debt levels. If interest rates increase, Costamare may have to pay a fortune in interest expenses, or the weighted average cost of capital would increase significantly. I would also expect that the shares outstanding may decrease or stay at the same level. Keep in mind that a gradual increase in the share count would lead to a decrease in the company’s fair price.

YCharts

Under normal conditions, I assumed a decline in sales growth in 2024, and then a rebound in activity in 2025 and 2026. Also, with an EBITDA margin close to 72% and assuming an effective tax of 21%, the free cash flow should grow from $475 million in 2022 to around $677 million in 2026. Note that like other analysts, I am not expecting an increase in capital expenditures from 2023.

Author’s Compilations

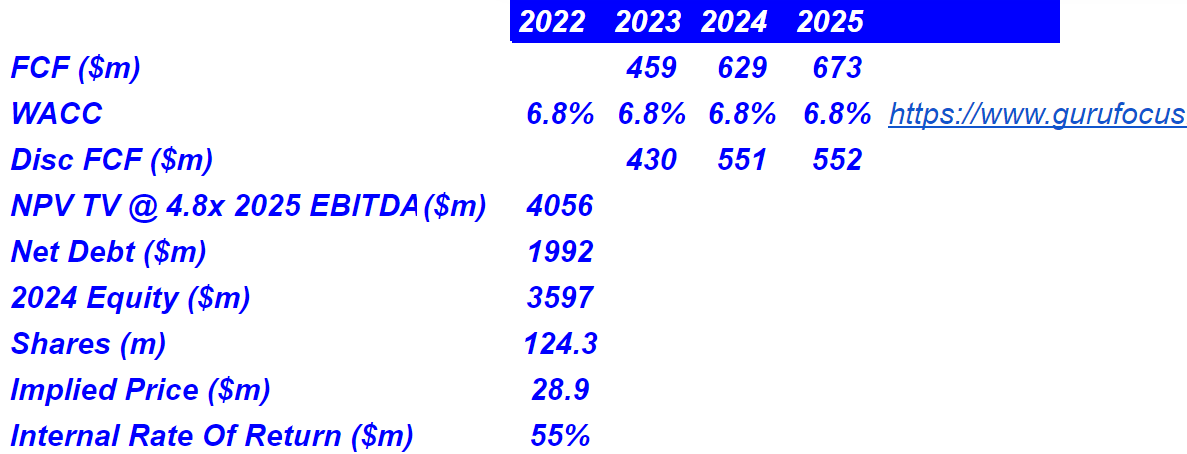

I also assumed a discount of 6.89%, which is pretty much what other analysts are using, and an exit multiple of 4.8x EBITDA. Let’s note that the valuation in the industry stands at more than 10x EBITDA. In my view, I am quite conservative in this case. My results include an implied price close to $29, and an equity valuation of around $3.6 billion.

Author’s Compilations

Risks

If the charter rates in the shipping industry decline, Costamare will suffer significantly. Unfortunately, management cannot do a lot against a decline in the activity in the market. Under this case scenario, I expect a decline in revenue caused by these matters:

Our profitability will be dependent on the level of charter rates in the international shipping industry, which may be volatile due to the cyclical nature of the industry. Source: 20-F

In line with the previous commentary, it is worth mentioning that analysts like Clarkson Research are already claiming that there may exist a certain oversupply in the industry. In the worst-case scenario, I would expect a decrease in charter rates if oversupply becomes a reality.

According to Clarkson Research, as of December 2021, the containership order-book represented 23.1% of the existing fleet capacity, 73% of which was for vessels with carrying capacity in excess of 12,000 TEU. An oversupply of large newbuild vessels and/or re-chartered containership capacity entering the market, combined with any decline in the demand for containerships, may reduce available charter rates and may decrease our ability to charter our containerships when we are seeking new or replacement charters other than for unprofitable or reduced rates, or we may not be able to charter our containerships at all. Source: 20-F

There is another clear caveat to keep in mind. Costamare needs to invest a significant amount of dollars in capital expenditures in order to maintain the same capacity. If capital expenditures increase in the near future, the free cash flow will likely decline:

We must make substantial capital expenditures to maintain the operating capacity of our fleet, and these amounts may increase as our fleet ages. Source: 20-F

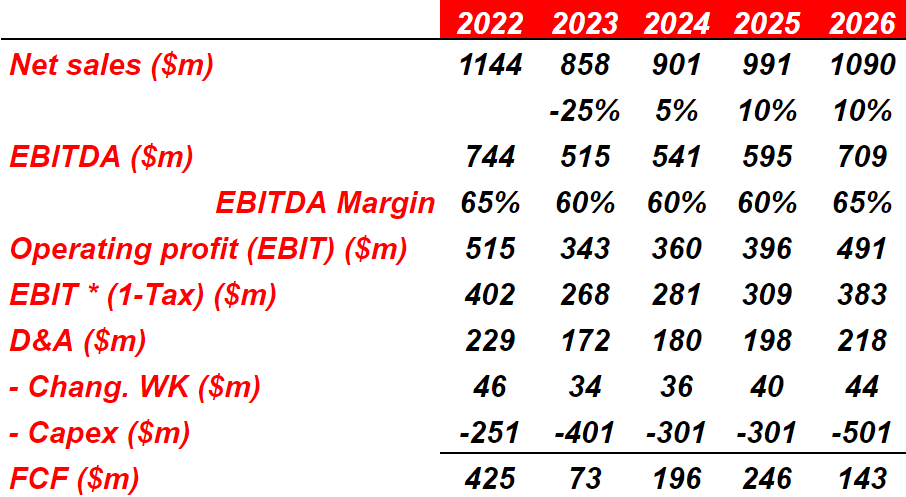

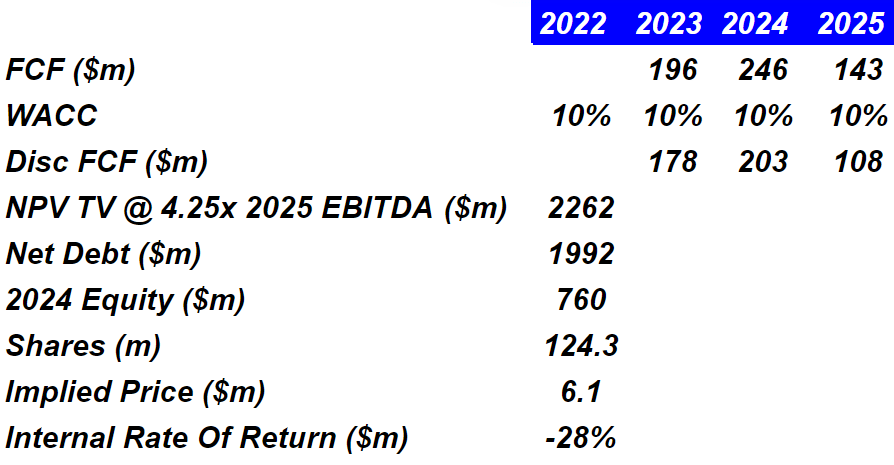

Under the worst-case scenario, I assumed a net revenue decline of 25% in 2023, and 5%-10% sales growth in 2024, 2025, and 2026. With a smaller EBITDA margin close to 60%, operating margin of 40%, and conservative changes in working capital and D&A, 2026 free cash flow should stay close to $145.

Author’s Compilations

Now, with a weighted average cost of capital of 10% and an exit multiple of 4.25x EBITDA, the implied fair price should be close to $6.5.

Author’s Compilations

Takeaway

With Costamare buying its own shares and the value of the company’s vessels growing, I would be expecting sales growth in the next five years. Under the best-case scenario, I believe that a reduction in debt and a decrease in the shares could be ideal. Besides, if Costamare continues to enter new markets like the dry bulk shipping industry and diversifies, revenue growth may not be volatile. There are serious risks coming from oversupply or a decrease in the charter rates. Besides, an increase in interest rates may be detrimental for the company’s free cash flow margins. With all these being said, I do see more upside potential in the stock price than downside risk for Costamare.