marchmeena29/iStock via Getty Images

Written by Nick Ackerman, co-produced by Stanford Chemist

Calamos Convertible and High Income Fund (CHY) has been treating its investors well over the years. The sister fund, Calamos Convertible Opportunities & Income Fund (CHI), has also provided similarly attractive returns to shareholders. This is the case because they are invested mainly in the same assets.

CHY currently has a bit lower of a premium than CHI, which translates into a slightly higher distribution yield for shareholders too. Both funds pay monthly, which is quite attractive for income investors. These funds had particularly strong performances in 2019 and especially in 2020. 2020 saw the boom of many convertible offerings, and demand for these securities exploded. 2021 also wasn’t a bad year. It was enough to cover their distributions but not much more than that.

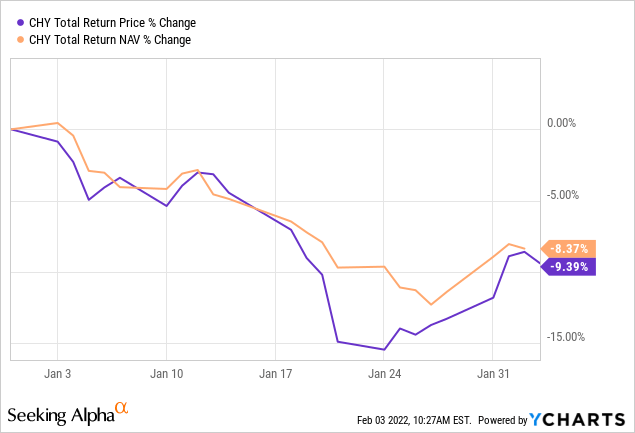

So far in 2022, they have been battered. This is due to the overall correction the market experienced in the first month of the year. It was further fueled by the hit to tech stocks more specifically. Since convertible investment prices will correlate with how well the equity stock price is doing, these too have taken a hit. Since CHY invests more heavily in tech stocks, that’s why we can see a general weakness there.

On a total share price basis, CHY is down 9.39%, with the total NAV return coming in at a decline of 8.37%. As is often the case, we see the price falling faster than the NAV. An investor could have picked this fund up for a discount if they were quick enough. For several days it traded at a fairly shallow discount.

Ycharts

The Basics

- 1-Year Z-score: 0.87

- Premium: 2.18%

- Distribution Yield: 8.28%

- Expense Ratio: 1.23%

- Leverage: 33.24%

- Managed Assets: $1.746 billion

- Structure: Perpetual

CHY “seeks total return through a combination of capital appreciation and current income.” They attempt to achieve this through “investing in a combination of convertibles and high yield bonds.” They highlight that it “provides an alternative to funds that invest exclusively in investment-grade fixed-income instruments, and it seeks to be less sensitive to interest rates by investing in lower duration asset classes.”

The fund is quite large, and that means trading volume isn’t generally a problem for investors when buying and selling. The high amount of leverage might be a deterrent to some investors. However, since they invest in convertible bonds, these are generally safer than equity positions. Though not too safe, they are often issued to companies with below-investment-grade credit ratings.

The fund’s expense ratio comes to 1.23%. This climbs to 1.84% when including the leverage expenses. The leverage here is something to watch when interest rates rise. The reason being is that a sizeable portion is based on floating rates. The fund last reported having borrowings of $435.4 million with a net interest rate of 0.51%. That is based on overnight LIBOR plus 0.80%. Apparently, overnight LIBOR rates were negative by quite a bit.

However, they have another $181.5 million in mandatory redeemable preferred shares that they utilize. This is also a form of leverage. In this case, though, it is fixed at a specific dividend rate. The preferred leverage can be a more expensive form of leverage, but it also comes with some benefits.

There is greater flexibility when it comes to deleveraging during market panics. The fixed-rate is also a benefit. It wasn’t beneficial since these rates are between 2.68% and 4.24%. In the future, that could be a different story. The first of these preferred to come up for redemption on September 6th, 2022. That one has a 3.7% dividend rate.

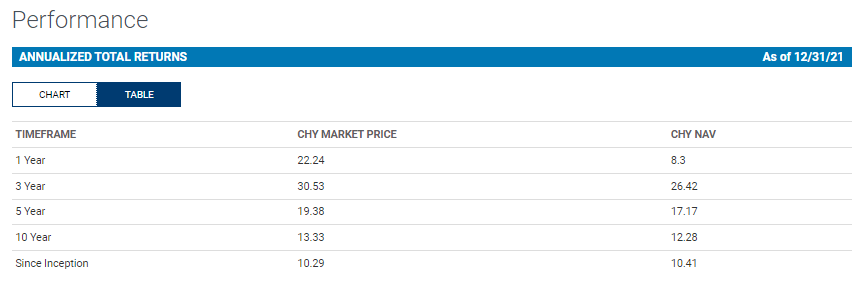

Performance – Long-Term Solid Results

We touched on the returns on a YTD basis so far and how weak those have been. However, the longer-term track record has been quite solid. The annualized returns they provide are for the end of 2021. So they’d be a bit lower at this point now if these were updated daily.

CHY Annualized Returns (Calamos)

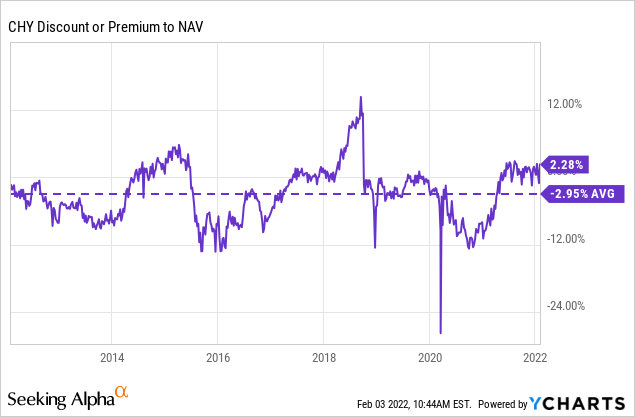

This has pushed CHY to trade at a fairly rich premium to its NAV on several occasions. What is noteworthy for CHY is just how erratic the premium/discount has been in this fund over the years. It makes it difficult to gauge a regular historical range since it goes from a 10% discount to 5%+ premium on several occasions.

Over the last year, the fund has averaged a discount of 0.65%. Based on the 2.28% premium at this time, that could be considered on the more expensive side. This is reinforced by the 1-year z-score of 0.87. Though that isn’t overly expensive in the grand scheme of things either. In January, the fund reached a 4.07% discount on January 24th, 2022. So far, that has been the low presented in many closed-end funds. After that date, we’ve seen premiums/discounts bounce back.

If we look back over the last 10 years, the average discount of the fund comes to nearly 3%. That also makes the current premium on the more expensive side. Yet, at the same time, CEFs are generally pricier than they have been. This could be a new normal for CHY. I believe it puts it in a situation where it isn’t a screaming deal but also could be worth dollar-cost averaging into a position.

Ycharts

Distribution – Attractive 8.28%

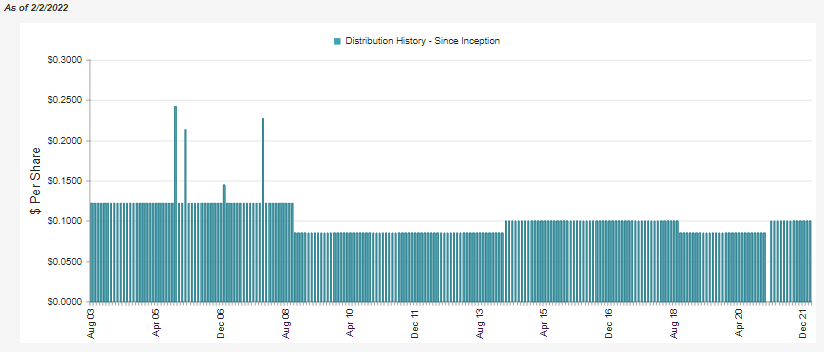

The monthly $0.10 payout to shareholders works out to a distribution yield of 8.28%. Due to only the small premium, that would mean the NAV distribution rate is a similar 8.46%. This makes it quite attractive, but historically, CHY isn’t free from adjustments. The $0.10 was actually an increase in 2021 from the $0.085 the fund was paying.

The current payout is also lower than the high water market that it was at after its inception of $0.1219. At the same time, the NAV and share price are almost equal to the fund’s inception in 2003. This could be due to lower rates overall. Since it holds convertible bonds and high yield bonds, rates play a role in the fund’s earnings.

CHY Distribution History (Calamos)

Interest rates aren’t what they used to be. However, that could be changing when the Fed is expected to increase rates through 2022, four or five times potentially. That won’t get us to where we were before but should help increase yields. It can provide some pain before normalizing in the short term, so that should be noted.

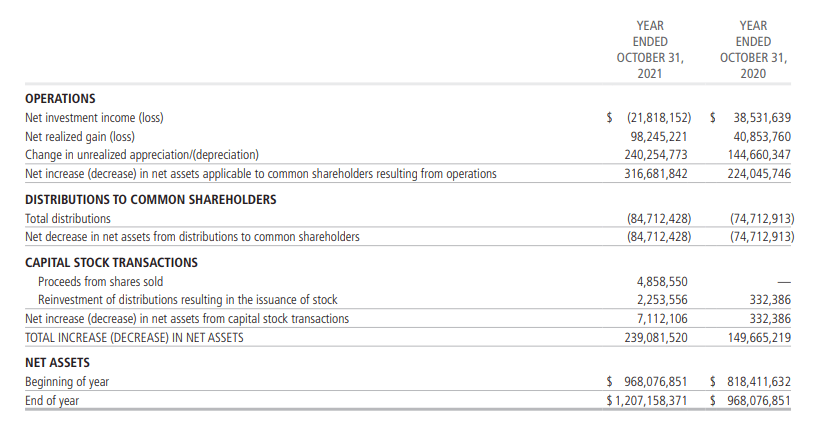

For CHY, after their expenses to management, interest expenses and preferred dividend expenses, the fund is left with a net investment income loss.

CHY Annual Report (Calamos)

The above is from their latest Annual Report. This all means that they had relied entirely on capital gains. As we know, those can be pretty unpredictable. Total income in fiscal 2020 equaled $57.7 million. After rounding up, total interest and dividends for fiscal 2021 declined to only around $38 million. One of the factors for why their income took such a hit was due to “(Amortization)/accretion of investment securities” of $38.484 million. This wasn’t present in the previous years.

Betting on CHY to maintain their current distribution suggests that they can earn 8.46% from this point forward as that’s the NAV rate. I believe that is an achievable amount. They’ve been able to do that and more going back to their inception. However, it isn’t a big cushion if 2022 proves to be a more challenging year.

The tax classification for the fund’s distribution was attributed entirely to ordinary income despite the NII loss. This appears to be due to mostly short-term capital gains. Some of the distributions were considered qualified dividends. Those can reduce a tax obligation but overall, it would appear CHY would be better in a tax-sheltered account.

CHY Annual Report (Calamos)

CHY’s Portfolio

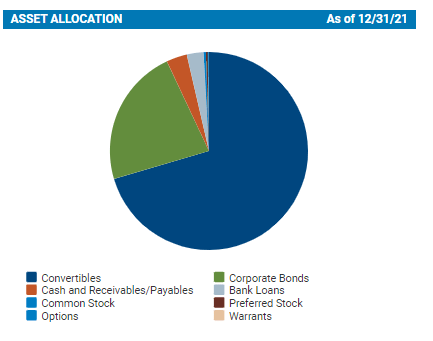

CHY is mostly invested in convertible securities. However, high-yield corporate bonds also make up a fairly sizeable chunk of their underlying assets. Bank loans and cash make up some of the portfolio but not a meaningful amount at the end of 2021.

CHY Asset Allocation (Calamos)

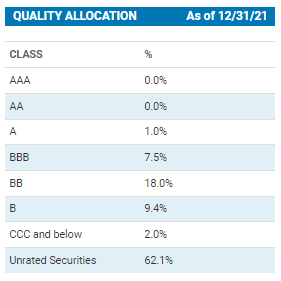

Convertible bonds often go unrated. However, they are typically issued by below-investment-grade companies. In addition to that, we know that the high yield bonds that make up the other sizeable portion of the fund’s portfolio is also junk-rated.

One of the main reasons convertibles go unrated is to save on the costs and time of issuing them. Since qualified institutional buyers buy convertibles, they don’t need to pay to have them rated. That also saves time to get them issued faster as well. The buyers themselves are large enough to have their own internal ratings to know if they are worth buying or not.

That’s why we see below that 62%+ of the fund is “unrated.” The other highest allocation is to BB at 18%. Which is below investment grade, only a small portion of the portfolio is considered investment grade at BBB and above.

CHY Credit Quality (Calamos)

Being that the fund is dedicated to primarily debt securities, one other area to look at is the fund’s duration. The effective duration for CHY comes to 2.7 years. That means it is relatively less interest-rate sensitive than some other fixed-rate counterparts. The reason for this is that the underlying portfolio will be more dependent on the prices of the underlying common stocks than actual interest rates.

Still, the role of interest rates in CHY isn’t completely lost. Higher rates would mean that the convertible issued should yield a bit more. Anything could be better than the 0% yield issues we saw come to market throughout 2020 and 2021.

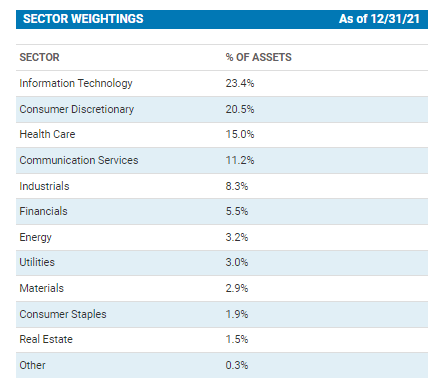

The sector weightings of CHY have stayed relatively similar since we last covered the fund. However, tech’s allocation has inched up. The tech sector was already the largest concentration of the fund. At that time, we were looking at data for the end of July 31st, 2021.

CHY Sector Allocation (Calamos)

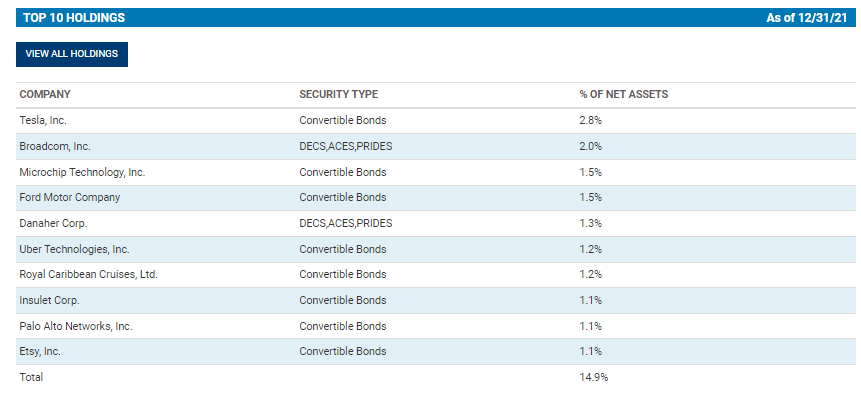

Tesla (TSLA) continues to be in the top position of this fund as well. However, the allocation has come down slightly from the 3.1% it previously was at.

CY Top Ten (Calamos)

The top ten account for 14.9%. That is an increase from the 14.2% earlier in 2021. That being said, it hasn’t become overly concentrated or has that shift really drastically changed CHY in any way.

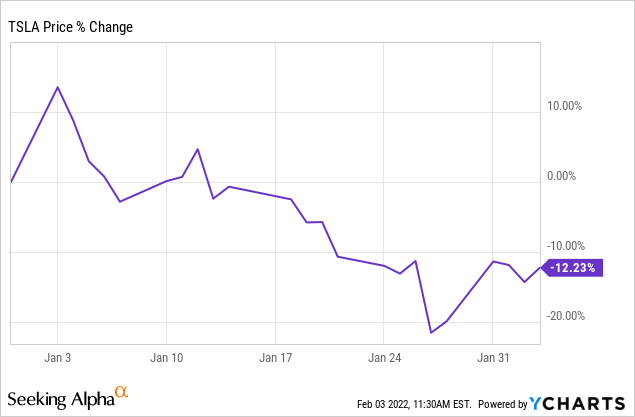

TSLA has been one of the stocks bringing the market down with it along with CHY on a YTD basis. It was included in the S&P 500 at the end of 2020, so it has an impact on the broader market. This stock continues to remain a polarizing investment with investors. On the one hand, it is a costly stock. On the other, it has been growing rapidly and represents the future.

Ycharts

Conclusion

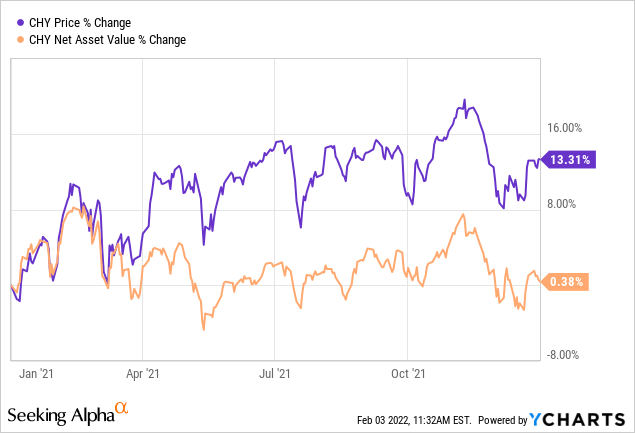

CHY has delivered solid results to shareholders, and while 2021 wasn’t a blowout, it was enough to cover the fund’s distribution. For income investors, that’s really what counts. Below is the price and NAV change only. The NAV having almost no move for 2021 means the payout was covered.

Ycharts

It was off to a rough start in 2022 so far, but that was along with the rest of the market. If you were quick enough, you might have been able to snag a position in CHY at a greater than 4% discount. Historically speaking, that would have been a fairly attractive buying entry if its average is any guide. However, we also touched on how erratic the fund swings from discounts to premiums, making its historical gauge a bit more limiting.

All that being said, CHY seems to be a fairly attractive investment for income investors that want monthly income. It isn’t a screaming deal, but taking some small position at this time to dollar-cost average in can make sense.