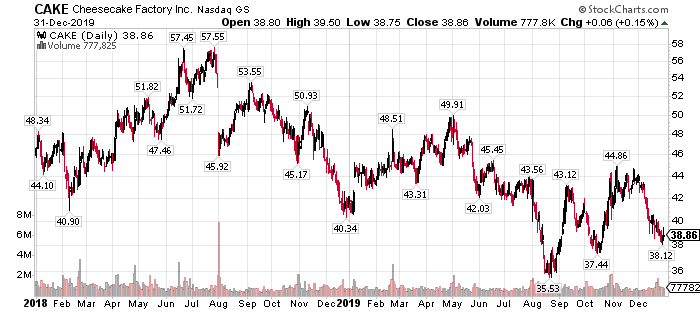

Upscale casual dining chain Cheesecake Factory (CAKE) had a very tough 2019. At a time when the broader market was making new all-time highs, shares of the company finished the year lower than where they began. Investors are presumably worried about the company’s revenue growth runway given the chain’s exposure to traditional malls, but the acquisition of Fox Restaurant Concepts, as well as its own growth plans, should provide plenty of upside momentum for the foreseeable future. This, combined with a very reasonable valuation and a nearly 4% yield, make Cheesecake Factory a strong buy.

Growth has slowed, but management has a plan

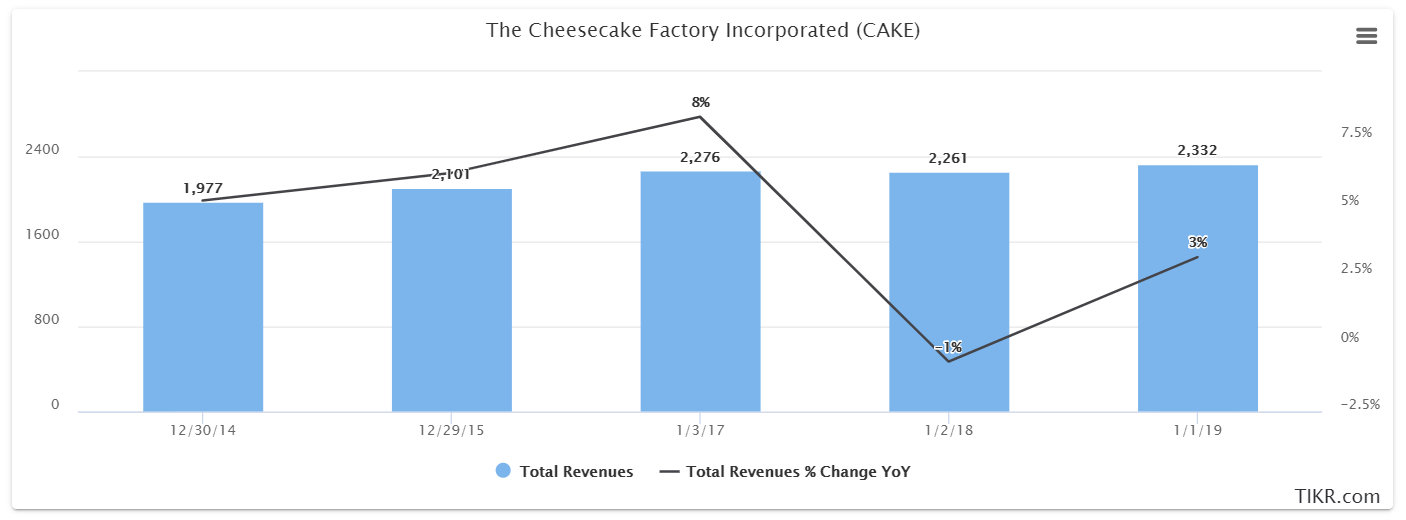

There is no doubting that growth for Cheesecake Factory has slowed in recent years. Revenue, charted below in millions of dollars, has slowed its upward trajectory meaningfully in the past two years.

(Source: TIKR.com)

Cheesecake Factory was accustomed to producing 5-8% total top line growth, thanks to a virtuous combination of new stores and robust comparable sales growth, but that changed dramatically for 2017 and 2018. Last year did see a rebound, but only by 3% – nothing like what the company had been doing in prior years.

Indeed, in the first three quarters of 2019, Cheesecake Factory’s revenue is up only 2.4% on basically flat comparable sales. While the fact that the company’s revenue is still moving in the right direction is a positive, investors have clearly lost patience with the chain and expect more. Otherwise, the share price wouldn’t be languishing near its lows.

The good news is that the acquisition of Fox Restaurant Concepts will provide a much-needed boost to growth over and above what the flagship brand can do on its own in the coming years. Indeed, as we can see below, forecasts are for a lot of growth coming in the next couple of years.

![]()

(Source: Seeking Alpha)

Analysts have revenue up nearly 6% this year followed by 20% for 2020, and another 6% after that in 2021. Obviously, Fox is the reason Cheesecake Factory should see such huge growth in 2020, and indeed, after the acquisition closed early in Q4, that quarter’s revenue growth should be quite strong. Cheesecake Factory is buying not only a significant footprint with Fox, but the ability to scale its concepts – particularly North Italia – across the country. Finally, the company can use Fox’s focus on experiential to enhance Cheesecake Factory’s menu, for instance. I love the acquisition, and I think the market is missing out on a great opportunity by ignoring it.

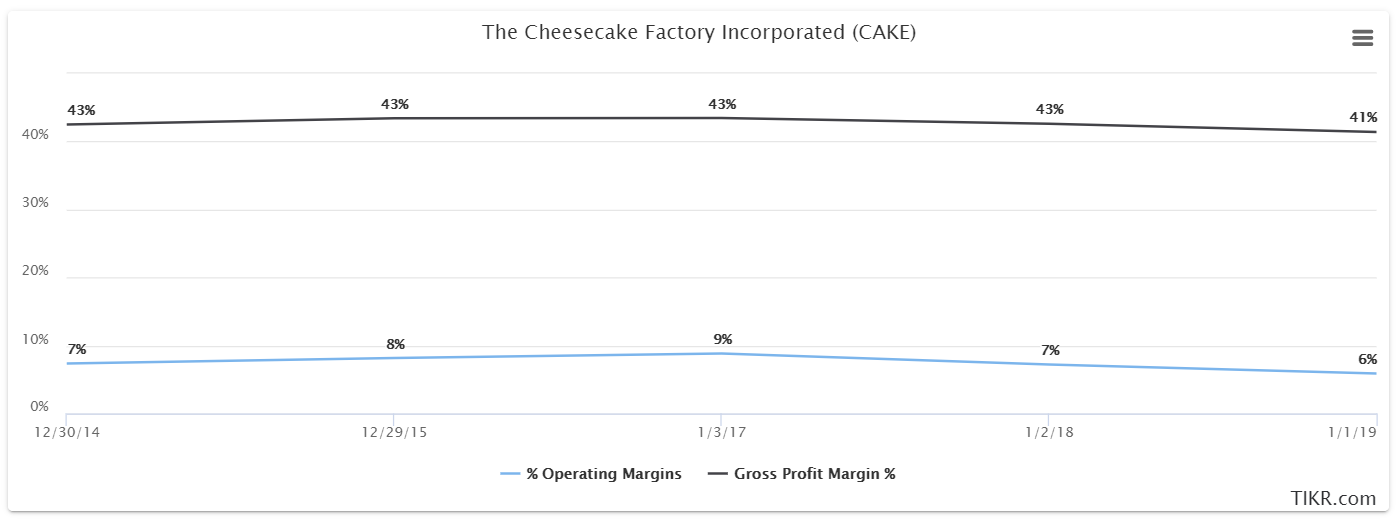

To be fair, relatively weak revenue growth has cost Cheesecake Factory some margin over the past couple of years as well, with that trend continuing this year.

(Source: TIKR.com)

Above, we have Cheesecake Factory’s gross margins and operating margins, showing the relationship between the two. Gross margins have ticked lower in the past couple of years, as it has for many restaurant chains, thanks mostly to higher occupancy costs and labor costs. That has taken a direct toll on the company’s operating margins, which, in turn, crimps profit growth. Cheesecake Factory is certainly not alone with this, but it is painful nonetheless. The good news is that food costs have been relatively steady; it is other operating costs that are hurting the chain.

Food costs so far this year are about flat, but labor expenses have risen 60bps and other operating costs are up a further 80bps. This margin deterioration continues to hurt profitability, and with no catalysts in sight to improve labor and operating costs, the chain will need to rely mostly upon revenue growth for EPS expansion.

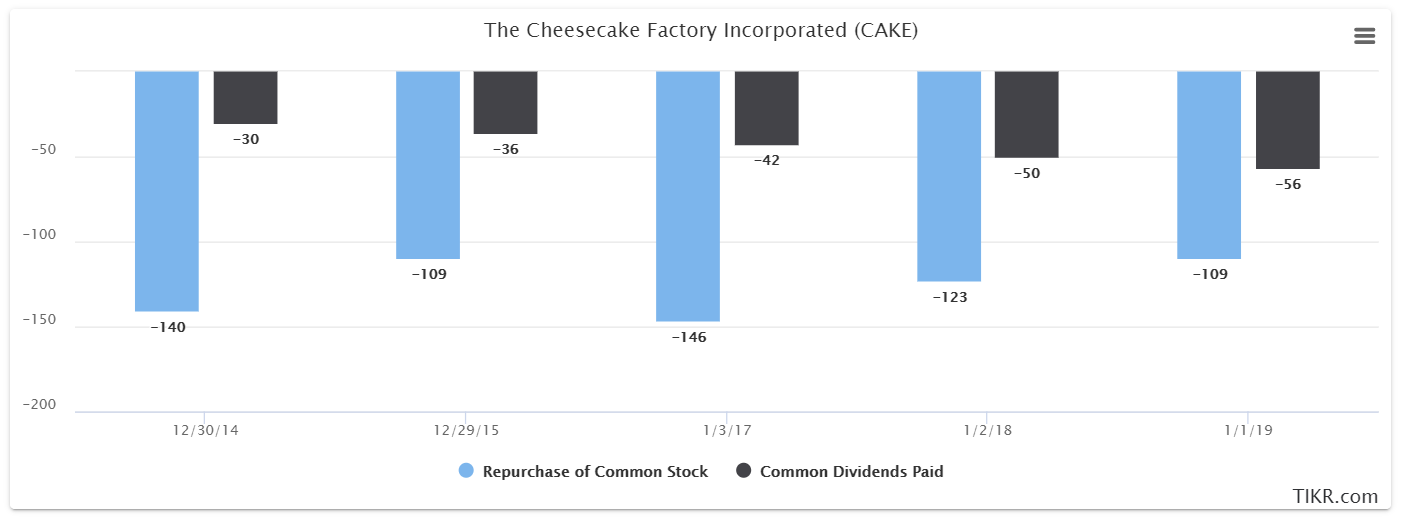

Apart from hot revenue growth for 2020, owners of Cheesecake Factory get strong capital returns via dividends and buybacks. Below, we can see capital returns in millions of dollars for the past few years, and the amount the company has spent is sizable, to say the least.

(Source: TIKR.com)

Dividend growth has been robust, with the amount the company spent per year nearly doubling from 2014 to 2018. The current payout is worth 3.7% annually, which is nearly double the broader market yield, and strong, to say the least.

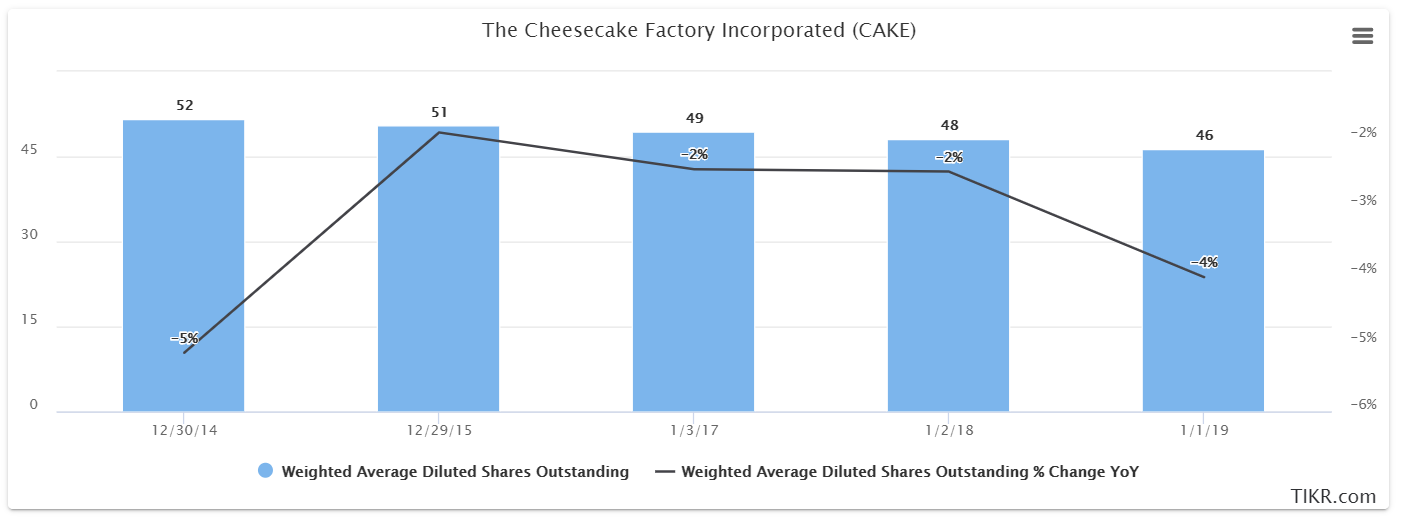

In addition, Cheesecake Factory has spent more than $100 million annually on buybacks, reducing the float and expanding EPS in the process. Unfortunately, due to the languishing share price, many of these purchases were made at prices much higher than today. Still, as we can see below, the company has achieved a lot with its buyback dollars.

(Source: TIKR.com)

The weighted average diluted share count fell from 52 million to 46 million in the past five years, and today, is down to 44 million after more repurchases. All else equal, this mid-single digit tailwind provides a nice gain to EPS each year with excess capital the company doesn’t need anyway. Repurchases will likely slow a bit for the near term given the ~$300 million purchase price for Fox, but the additional revenue growth should help the company pick up the pace again in the relatively near future.

Lots of growth for a reasonable price

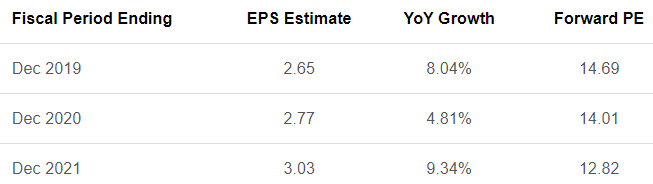

The interesting thing is that analysts aren’t that bullish moving forward, which I think provides an opportunity should the Fox acquisition work out – as I believe it will.

(Source: Seeking Alpha)

After 8% EPS growth this year, analysts see just 5% expansion in 2020 despite a 20% gain in revenue. We know the company is going to see a huge boost in revenue around 20%, implying the combination of share repurchases and margins will provide a headwind of 15% to EPS. While Cheesecake Factory will incur some acquisition costs – including the potential for more than $40 million in earn-out provisions – for Fox, margins have largely stabilized for 2019, and the additional ~$500 million in revenue for 2020 will help leverage down SG&A costs.

In total, with Cheesecake Factory you get a stock with a 3.7% yield, strong EPS growth potential, and a reasonable valuation of just 14 times 2020 earnings. The Fox acquisition is transformational for Cheesecake Factory, bolstering the company’s revenue growth runway, which was its Achilles’ heel. With that solved, I think the upside potential for the company includes higher EPS estimates as well as a higher P/E ratio. The stock’s combination of growth potential thanks to Fox, as well as its yield of nearly 4%, make it too good to pass up.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in CAKE over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.