This article was highlighted for PRO subscribers, Seeking Alpha’s service for professional investors. Find out how you can get the best content on Seeking Alpha here.

As this is a lengthy article, here’s the thesis for Mexican airport operator Grupo Aeroportuario del Centro Norte (OMAB) in a nutshell:

- The USMCA free trade agreement will drive new manufacturing to Mexico, specifically focusing on the Monterrey area.

- Loss of confidence in China will cause factories to leave that country.

- The slide in the Mexican Peso throws more fuel on these trends.

- OMAB is the best way to profit from these trends.

- It’s also the cheapest Mexican airport operator despite having the best prospects right now.

- OMAB’s fantastic balance sheet makes it immune to the liquidity squeeze hitting most travel stocks during the current pandemic.

- Stock is worth nearly more than double current prices once travel is back to 2019 levels.

- In my base case outlook, OMAB’s shares will be worth 5-7x current prices in 2030.

One of the company’s VIP lounges. Source: Corporate Website

I won’t cover too much backstory on OMAB as I’ve written about the company several times, previously. But for those unfamiliar, OMAB (aka OMA in Mexico) operates 13 Mexican airports, primarily in the northern part of the country:

Source: Wikipedia

Of these, Monterrey (MTY on the map) is the crown jewel, accounting for around half of the company’s revenues and passengers. Northern Mexico is the country’s wealthiest region (excluding the capital city). And it has grown tremendously since the early 1990s, when the original NAFTA treaty was enacted, which created a defined free trade arrangement between Mexico, Canada, and the U.S.

Monterrey is OMAB’s biggest draw, but as you can see, the company has a ton of airports throughout Northern Mexico’s industrial heart. Monterrey is also the regional hub for that area in terms of ground logistics – it has several highways running to various Texan cities. It’s also a major through-point for the primary railroad line running from the U.S. into central Mexico. Thus, not only is Monterrey a massive manufacturing center itself, it’s also a key logistics point for anything else traveling between the U.S. and Mexico.

Looking at a league table, OMAB scores two of the country’s top 10 airports ranked by traffic, with OMAB’s airports in bold:

- #1 Mexico City (not publicly-traded)

- #2 Cancun – ASR

- #3 Guadalajara – PAC

- #4 Monterrey

- #5 Tijuana – PAC

- #6 Los Cabos – PAC

- #7 Puerto Vallarta – PAC

- #8 Merida – ASR

- #9 Leon/Guanajuato – PAC

- #10 Culiacan

Keep in mind that OMAB’s market cap tends to run around half of Pacifico’s (PAC) and Sureste’s (ASR), so it’s not a big concern that OMAB isn’t at the top of the list.

That said, if you want just one airport holding, Pacifico is the easy choice. It owns fully half of Mexico’s top 10 airports and has exposure to big cities (Guadalajara), industry (Tijuana, Leon), and tourism (Cabos, Puerto Vallarta) all under one roof. At its lowest price in many years, Pacifico is an excellent choice, and I’m an active buyer at current prices.

But we’re going for my favorite pick today, and that’s OMAB. You get Monterrey, which has arguably the best growth prospects of Mexico’s big cities. We’ll discuss that more in a minute. And you get a bunch of other airports that are on the U.S. border or near it and, as such, get huge upside from the further industrialization of Mexico. OMAB’s Chihuahua and Ciudad Juarez airports are already just outside of Mexico’s top 10 busiest thanks to sharp increases in population and business activity thanks to 25 years of NAFTA development. And other OMAB cities, like San Luis Potosi, are positively booming right now.

With OMAB, you have a nearly pure-play bet on Mexican manufacturing (yes, OMAB owns Acapulco and Ixtapa which are tourist/beach airports, but neither is a significant traffic driver).

Trade War/COVID: A One-Two Punch To China

The story of the world economy, since the fall of the Soviet Union in 1991, has been one of relentless globalization. As Thomas Friedman said, “The world is flat.” With modern telecommunications and then the internet, everyone could work, compete, and take part in the global economy from anywhere. This relentlessly drove down costs and pushed untold millions of manufacturing jobs to China and surrounding nations.

For thirty years, this trend ran nearly uninterrupted. Even things like 9/11 and the subsequent military actions in the Middle East failed to significantly alter this trajectory.

While Mexico benefited to a considerable degree from free trade – and particularly the NAFTA agreement of the early 1990s – the past few decades have seen China and several other Asian states enjoy the fastest climbs.

This rise has created more and more consternation in recent years. I’m not interested in debating all the politics around that; I’ll just say that there’s clear anger building up toward the offshoring of jobs among major segments of both American political parties. The Trump Republicans and Sanders Democrats are both driving at the same general discontent with the country’s economic direction over the past 30 years, albeit with different proposed solutions.

Trump galvanized that energy with his trade wars against China from 2018-onward. While the effectiveness of this effort can be debated, it didn’t cause the sort of economic collapse that economists had feared. Heading into 2020, the economy was in fine shape despite several years of troubled relations with a key trading partner.

Now the coronavirus has collapsed the economy, at least for the time being. But that appears to be somewhat on China as well; while we don’t know enough to be certain, it seems plausible that China’s efforts to avoid bad publicity may have allowed the virus to spread far faster than it would have otherwise. In any case, the virus, and China’s handling of it, is now turning into a central 2020 election issue.

The U.S. is hardly the only place this is happening either – populist backlash is building in Europe and also here in Latin America where I live. China-skepticism is mounting. Plenty of other scandals, such as Huawei’s dealings, China’s poor treatment of its Uighur citizens, and accusations of using its tech firms to spy on foreigners only add to these concerns. And then there’s the fentanyl mess; people are quickly coming to the realization that much of the U.S.’s drug overdose problem is due to China producing dangerous pharmaceuticals.

As China Slides, Mexico Will Rise

That last point is particularly important as it relates to Mexico. The fentanyl situation has helped prove that the drug crisis is a complex tangle with many causes; it’s not just a few bad actors coming from Mexico and causing trouble. The more Trump talks about drugs arriving from China, the more it lifts pressure on Mexico.

Source: Wall Street Journal

The illicit drug issue has been a huge relief for Mexico, as it has moved the focus elsewhere. Looking at Mexican economic numbers, the status quo has been fine from a business perspective. But the drug and violence discussions were a massive drag on sentiment and the perception of political risk. Now, however, as we talk about fentanyl, the negative headlines have gone elsewhere.

The same thing happened with trade as well. Back in the 2016 election, Trump was hammering the immigration issue and talking about building a wall in every speech. It’s no wonder the Mexican Peso dove on election night; Trump appeared laser-focused on Mexico. But that was just an appetizer; the main economic battle of his administration has been with China, not Mexico.

In fact, Mexico now already has its new USMCA trade deal with the U.S. and Canada. This secures Mexico’s place as the major assembling ground for North American autos, medical devices, aerospace products, and more. The coronavirus is putting this in stark relief; hypothetically, would Americans rather have the world’s supply of ventilators built in Wuhan, China or in Monterrey, Mexico?

Yes, some folks might answer that they want them built in the U.S. But for many goods, it simply isn’t feasible to build them in the U.S. with $25/hour plus benefits union labor. Trump conceded as much in crafting the USMCA; Mexico had to up its standards in several key areas, and in return, it’s no longer under heavy fire from the trade skeptics in the U.S.

Long story short, manufacturing from Asia returns to North America, with inputs and basic labor handled in Mexico, and more skilled positions settling in Canada and the U.S. All three countries get more jobs, citizens are happier, and safety concerns (particularly for medical devices) are cleared up. The framework is already there. USMCA is settled policy, whereas anyone setting up supply chains in Asia has zero idea what the regulatory scheme will look like in a couple years. Obvious advantage to North America.

For the Mexican side of that, all roads lead to Monterrey. Literally. The country’s main highways for exporting onward to Texas pass through Monterrey. As does the main railroad. And Monterrey itself is the biggest manufacturing and logistics hub.

Monterrey, Mexico’s skyline at night, 2016. Source: Wikipedia

For OMAB, What Could Go Wrong?

The most obvious headline risk with OMAB is narco-problems. In fact, given popular perceptions, this is what I spent the most time discussing when I originally wrote the stock up as an investment idea in 2016. Given past events, it’s not surprising that foreign investors are particularly concerned about this factor. And sure, the company operates several airports, including its second-largest airport overall, in Sinaloa (Culiacan city airport). Sinaloa is one of Mexico’s most dangerous states. While traffic numbers have been strong from these airports, there’s still a higher risk factor on them given local conditions.

Several other OMAB airports are in areas that are or have recently had massive cartel problems, such as Ciudad Juarez. Ciudad Juarez, though it has improved recently, was described as the murder capital of the world less than a decade ago. And even the main asset here, Monterrey, is relatively unsafe by big Mexican city standards. So it’s definitely a valid risk.

The question is: At what point does violence and cartel presence become a problem for OMAB shareholders? The answer may be “never.”

The company has been publicly-listed since 2006, and despite a significant rise in cartel violence during stretches of the past 14 years, it’s never meaningfully impacted the company’s results. The company has been paying rising dividends and has showed double-digit EBITDA growth for more than a decade despite the safety situation; at what point do investors stop fretting about the headline risk?

Admittedly, as long as Netflix (NFLX) keeps pumping out crime documentaries, this may remain a leading concern – but I think most people are overestimating the risk. I lived in Mexico almost three years, and narco-violence (and violence in general for that matter) was not a major factor in day-to-day life. And many of the worst areas have gotten much better; Ciudad Juarez used to have so many murders that the police would only investigate 5% of them; now the murder rate there has declined by half over the past decade.

I’m always watching trends – and if we see something developing it’s worth paying attention to, I’ll point it out. Cancun, for example, has seen a big uptick in crime that has hit tourist traffic, as I documented in discussing a hotel chain there last year. As far as OMAB goes, as long as their areas are stable or improving, crime is not a deal-breaker at this point.

Financial Situation: OMAB Can Outlast Even A Brutal Depression

Switching gears, COVID-19 brings its obvious risks to the airline industry. In fact, you might have been reading the risks section wondering why I was going on about cartels and globalization when people only care about debt at the moment.

And sure, it’s important. But I’m talking about OMAB as a long-term investment – how much money it loses in 2020 thanks to COVID-19 won’t matter to an investor in, say, 2025. As long as a travel company has the liquidity to make it through the current mess without impairing the equity and its long-term growth remains in place, there’s no need to worry.

And let me be clear: OMAB is as well-capitalized as you could possibly hope for going into the coronavirus downturn.

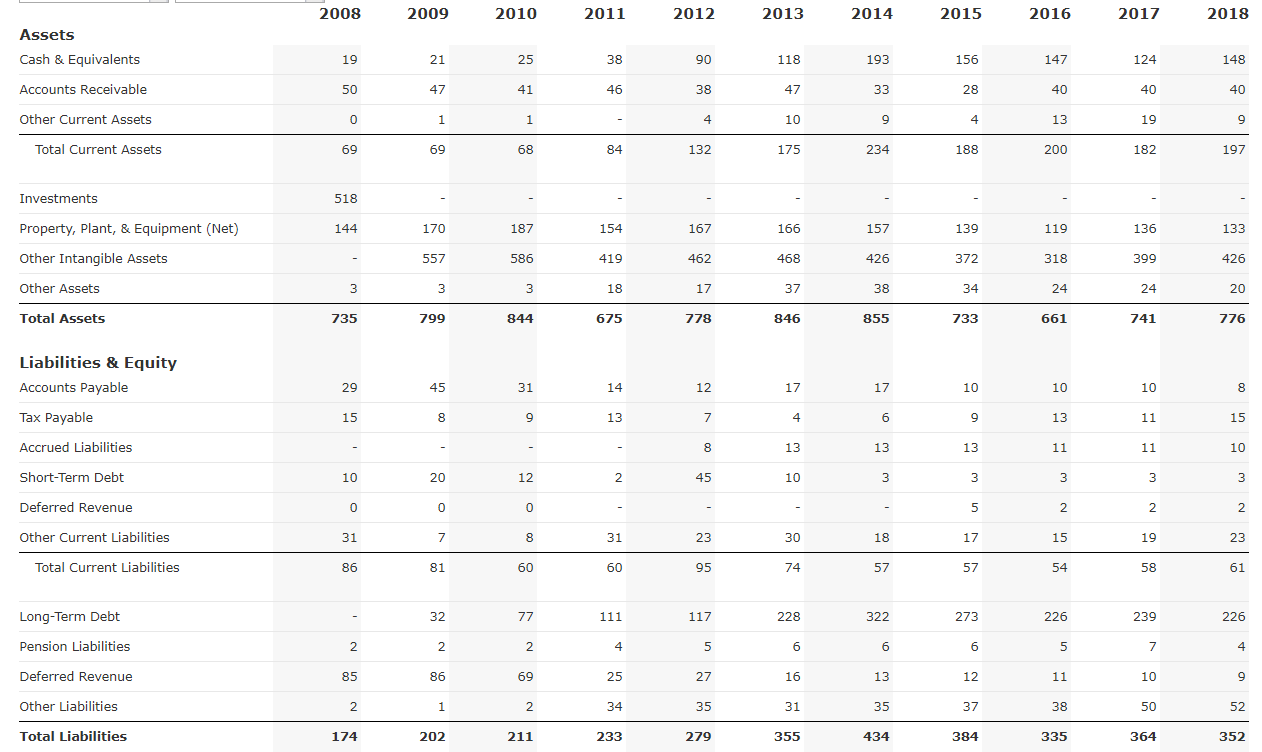

While all the Mexican airport operators run with fairly conservative balance sheets, OMAB has the best by far. The company always keeps far more cash on hand than it has in short-term expenses. And it never holds more than one year’s EBITDA in long-term debt. As a result, OMAB can afford to run for many quarters in maintenance mode, only earning modest revenues from cargo flights and a bare-bones domestic Mexican passenger flight schedule.

The company’s prudence isn’t a new feature; OMAB has always run itself with minimal leverage. Here’s 10 years of annual year-end balance sheet data:

All figures expressed in millions of U.S. Dollars. Source: QuickFS

All figures expressed in millions of U.S. Dollars. Source: QuickFS

As you can see, the company carries essentially no short-term liabilities at any given point in time, and they easily cover them several times over with cash. The long-term debt is also minimal – less than one turn of EBITDA. Importantly, the debt is denominated in Pesos, so the recent currency devaluation in Mexico doesn’t significantly harm their financial standing.

If you want another demonstration of how minuscule the debt load is, consider that OMAB paid 205 million pesos ($8 million) of net interest expense last year. Meanwhile, it earned 5.3 billion pesos in EBITDA ($214 million). Needless to say, it can most easily handle the debt.

In 2019, S&P Global rated OMAB’s debt mxAAA, which is the highest rating that a Mexican company can obtain. In its rating action, S&P approvingly noted the more than 12x interest coverage and less than 1x Debt/EBITDA ratios in giving OMAB its highest rating.

Don’t underestimate how much OMAB’s bulletproof balance sheet is worth. Already, we saw Auckland International Airport (OTCPK:AUKNY) substantially dilute its shareholders to raise funds. And other big operators like Sydney Airport (OTC:SYDDF) have jaw-dropping levels of debt. Sydney pays out nearly half its operating income in interest expense every year thanks to otherworldly 7.4x Debt/EBITDA ratio (remember, OMAB is under 1x). Needless to say, an airport operator like Sydney simply has zero margin for error if anything goes wrong with the economic reopening this summer. In the Americas, while Corporacion America Airports (CAAP) has much less debt than Sydney, it still has substantially more than the Mexican operators, which is why I’m not buying more of CAAP stock yet.

The more risk you take of large equity dilutions and/or bankruptcy, the more upside the stock has to offer to justify the risk. With OMAB’s balance sheet in mint condition, the downside risk is minimal on that front. It’s not hard to imagine a world in which shares of OMAB, Sydney, and CAAP all triple in a few years. However, on the flip side, if aviation remains grounded into 2021, the latter two could lose most of their (remaining) value, whereas OMAB would still be in fine shape.

How Fast Will The Business Bounce Back?

This brings us to the other COVID-related risk for OMAB. Sure, the company itself has enough money to endure a punishing multi-wave viral outbreak, if it comes to that.

But what good are airports if no one flies to them? At some point, the airports need to start seeing good traffic again – if it takes five years or more, let’s say, to get back to former demand levels, then we could still see a considerable hit to our investment even though there’s negligible bankruptcy risk. There’s still a discount rate for money after all – profits (and dividends) a decade from now are worth far less than getting paid today.

The thing is, I see folks saying “aviation will never be the same” or the like, and I just don’t buy it. Not even for a second. You’re going to have super cheap flights in a year or two. Oil is around $20/barrel as I’m writing this. Jet fuel used to be a huge component for flights – it won’t be at current levels. And sure, jet fuel could go way back up, but if it does, it probably is due to an economic recovery that lifts passenger demand. So that balances out.

On the labor side, having some airlines go bust – which we certainly will – lowers the cost of labor for others. Unions in particular have minimal bargaining power when tons of skilled workers are waiting in the wings to take lower-paying employment and/or break strikes.

Similarly, you’ll see a flood of used planes on the market assuming a number of airlines go bust. Aircraft lessors in particular seem to have major problems ahead of them. They’ll be desperate to get new paying customers for their jets.

What’s the answer? More airlines, of course. We’ve seen this cycle countless times since U.S. deregulated its airline industry in 1978. A few major carriers go bust, and then a ton of discounters spring up to replace them. The same happened in Mexico; in 2010, Mexico’s then second-biggest carrier failed. By year-end 2012, upstart discount carriers replaced all the lost traffic and more.

That said, in this case, I don’t think OMAB will even lose that much of its connections. Legacy carrier Aeromexico isn’t in terrible shape, and I suspect they’ll have access to capital when needed. Leading Mexican discounter Volaris (VLRS) is one of the best-positioned carriers to ride out the downturn and isn’t in imminent danger.

The other two discount carriers, Interjet and VivaAerobus are less certain, but at least one of them should make it, particularly as if one fails, it will encourage investors to support the other given the enhanced competitive position.

And on the U.S. side, Southwest (LUV) has made huge strides in flying to Mexico and it’s the strongest of the U.S. carriers so that should keep tourist flights available at good rates. And the legacy U.S. carriers appear headed toward endless dilution, rather than liquidation, so those airport clients are probably sticking around as well.

As soon as it’s practical to fly again and people leave their homes, I expect a reasonable amount of traffic to start heading toward OMAB airports again, particularly if jet fuel is close to free. OMAB gets a ton of industry traffic on flights from places such like Detroit as American auto executives come to visit their assembly plants in Mexico. I don’t think that traffic will switch to Zoom (ZM) video calls for long.

OMAB: My Outlook

{kind=link}

Source: Finviz

For historical perspective, OMAB’s stock lost roughly three-quarters of its value in 2007-9, despite traffic only dropping by low double digits then. OMAB’s stock fell roughly two-thirds peak-to-trough this time around, and remains down more than 50% from its recent peak. So on that basis, perhaps OMAB has farther to fall, given that the traffic losses over the next six months or so will be worse than during the Financial Crisis.

That said, the company’s balance sheet is in better shape now, and the company also has a more established shareholder base, whereas it was a new and unknown company with little operating history ahead of the Financial Crisis. Then you’ve got all the positives around the boom in Northern Mexico and the investment that was already in progress thanks to the recent USMCA trade deal approval.

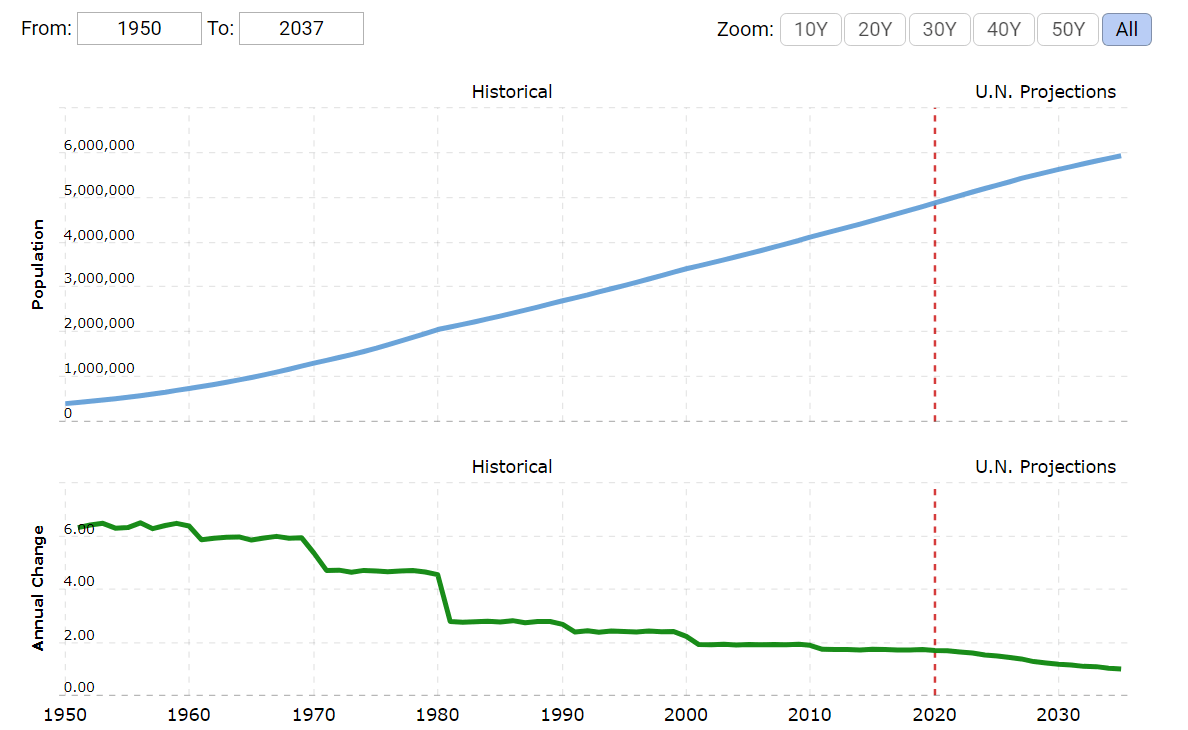

Monterrey population and growth rate data and projections, 1950-2037. Source

As you can see, the Monterrey metro area’s population has soared from just a few hundred thousand people in 1950 to 4.3 million at present. It’s set to hit 6 million within 20 years, firmly cementing it as Mexico’s third-largest city and economic area. Not only are you getting Mexico’s leading industrial hub, you’re also getting an emerging big city in its own right.

A city of six million with robust cultural, geographic and migratory ties to Texas will attract huge flows of international traffic. Go to a Mexican sports bar on a Sunday and witness all the Dallas Cowboys fans – the cross-border cultural ties are already significant and will only continue to expand; OMAB is a fantastic asset to ride the Mexican-American demographic wave as friends & family travel soars.

So, to be clear, I reject out of hand the idea that OMAB won’t return to 2019 levels of prosperity. Maybe if you own airports in a country with a falling population like Japan or Russia, you won’t see the airline business get back to the old peak.

But Monterrey adds nearly 100,000 new residents every year – the demand base grows tremendously from that, plus as wages rise, more and more of the population can travel frequently. And no, the middle and upper class aren’t going to take cross-border buses to get to Texas; with cartel activity, it’s far safer to go by air. There’s also the booming domestic flights to Mexico City and Guadalajara as both business and leisure traffic grows between Mexico’s three massive urban areas.

Maybe the overall level of business travel is permanently reduced 10 or 20% per unit of economic output as a result of the virus. But Monterrey adds 10 or 20% to its industrial base every couple of years. A few new auto, aerospace, or medical plants will make up for the lost traffic in no time.

Long story short, OMAB has grown revenues more than 10%/year compounded for the past decade, and grows earnings and dividends even faster since it has enormous scale benefits. It can keep ramping more and more traffic through the airports at little additional cost. It earns a jaw-dropping 71% EBITDA margin (highest of the Mexican operators) and has averaged a stunning 30% free cash flow margin over the past ten years.

If OMAB stock were still trading at $65 like it was recently, we could debate valuation more. At $30, it’s pretty simple. The company is recession-proof thanks to the triple-AAA balance sheet. Traffic will keep growing, probably dramatically, as it is hitched to numerous favorable long-term trends. And the company has an excellent cost structure, so that growth will translate directly into more cash flow and – thus – dividends since it pays nearly all of cash flow out to shareholders.

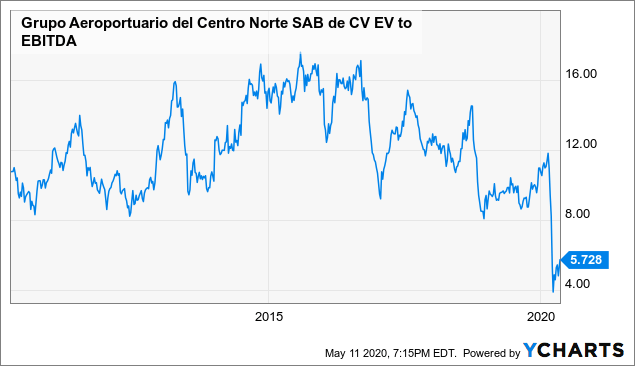

What should it be worth? On a return to 2019 EBITDA, which I suspect we’ll see in 2022, the stock should have a minimum of 50% upside, as that’d get it back to a barebones 8x EV/EBITDA:

Data by YCharts

Data by YCharts

Please remember to evaluate airports on EV/EBITDA – these are like REITs in that depreciation is a huge expense that isn’t particularly relevant so don’t rely on P/E. Yes, OMAB is at 11x trailing P/E, but even that makes OMAB’s stock look much more expensive than it is, since it includes major depreciation expenses for airports that aren’t actually losing value.

8x EV/EBITDA is still way too cheap in my opinion, but that’s where OMAB’s stock bottomed on various other occasions in the 2010s, so that area, around $45, is an absolute floor for what the stock is worth. You get to the $50s on a 10x EV/EBITDA, and back over $60 on a return to where we were earlier this year.

On the upside, OMAB could easily trade to 15x EV/EBITDA in the next Mexican bull market – remember, Mexico’s equity market has been in a bear since 2013 now! 15x EV/EBITDA would cause the share price to triple, even assuming EBITDA hasn’t gone up any more yet. And, traditionally, OMAB’s EBITDA compounds at a double-digit rate, so by 2023 or 2024, we could be looking at a substantially higher denominator here.

Over the next decade, if EBITDA only grows at 7%/year – a number that would have been extremely pessimistic pre-COVID but is now a reasonable estimate – EBITDA doubles by 2030. On a 15x EV/EBITDA ratio, that would lead to a 500% share price appreciation in 10 years – throw in the traditional 4-5% annual dividend yield on top of that and total returns would be substantially better.

There’s some napkin math to those assumptions, and I’m happy to discuss/debate them in further detail. Regardless of how you run the numbers, upside here is tremendous. If things are substantially worse than I estimate now, maybe the stock goes up 3-4x over the next decade instead of going producing something closer to my baseline 5-7x return expectation.

In any case, as long as the basic assumptions are correct – the company’s balance sheet is bulletproof, Mexico’s manufacturing traffic booms in the 2020s, and people use planes instead of cars to get around, OMAB’s stock will be going to the stratosphere in coming years.

This is an Ian’s Insider Corner report published April 29th for our service’s subscribers and subsequently updated to reflect current events. If you enjoyed this, consider our service to enjoy access to similar initiation reports for all the new stocks that we buy. Membership also includes an active chat room, weekly updates, and my responses to your questions.

Disclosure: I am/we are long OMAB,ASR,PAC,CAAP. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.