Cenovus Energy (CVE) has benefited immensely from the Alberta curtailment program. Mr. Market would have you believe that is the only reason the company is doing so well this year. The reality is slightly different. The cleanup costs from the joint venture with ConocoPhillips (COP) and the associated property sales are now gone. In place of all that cleanup is now a lot lower costs and much stronger cash flow. The result is a very profitable company that will do as well as any unconventional or conventional company in the business.

Indeed, the company just announced a 2020 free cash flow target of at least C$1 billion. This is in addition to a production growth rate of 7%. This is also one of very few companies that credit agencies see a positive outlook for.

“In the fourth quarter of 2019, Moody’s Investors Service affirmed Cenovus’s Ba1 credit rating and improved its outlook for Cenovus from ‘stable’ to ‘positive’, citing the significant amount of debt reduction the company has achieved. In addition to making progress towards re-establishing an investment grade credit rating at Moody’s, Cenovus remains committed to maintaining its current investment grade credit ratings at S&P Global Ratings, DBRS Limited and Fitch Ratings.”

Source: Cenovus Energy 2020 Budget Guidance Press Release December 10, 2019

The decision to ship products by rail only enhances an already bright profitability picture. More pipelines would certainly help the Canadian industry. But this company is well prepared to work within current industry conditions until Canada properly allocates appropriate resources to the industry (or correctly allows the midstream growth needed).

Management deftly moved to first support a production curtailment that immediately improved pricing. Company profits benefited this deal from the start. What many do not realize is that Pengrowth Energy (OTCQX:PGHEF), which will now be acquired for almost no equity value, and MEG Energy (OTCPK:MEGEF) were far more likely to fail had pricing remained at its fourth-quarter lows. That alone would have brought prices back into line quickly. There were many more weak competitors that would have been quickly been eliminated had the fourth-quarter low pricing remained.

Cenovus Energy is a very low cost producer with a lot of free cash flow. For all the market talk about free cash flow, the healthy industry companies that produce a lot of free cash flow certainly receive no recognition for the accomplishment. The minimum goal of C$1 billion is one of the top percentages of free cash flow compared to cash flow from operating activities in the industry. Not too many oil and gas companies have that percentage of free cash flow after growth plans are included.

The new rail exception announced by the Alberta government allows the company to finish some expansion projects begun under the partnership with ConocoPhillips. This is going to be another exhibit of the company cashing in on the acquisition for yet more profits. What was already a good deal for the company now promises to become materially better. This management has clearly “pushed the right buttons” for a very favorable regulatory environment to avoid some trying times.

The Third-Quarter Results

A year or more after the acquisition of the partnership interest held by ConocoPhillips, the company financial statements are now clear of the acquisition related and corresponding housecleaning entries. The results are materially better.

(Canadian Dollars Unless Otherwise Stated)

Source: Cenovus Energy Third Quarter 2019, Management Discussion And Analysis

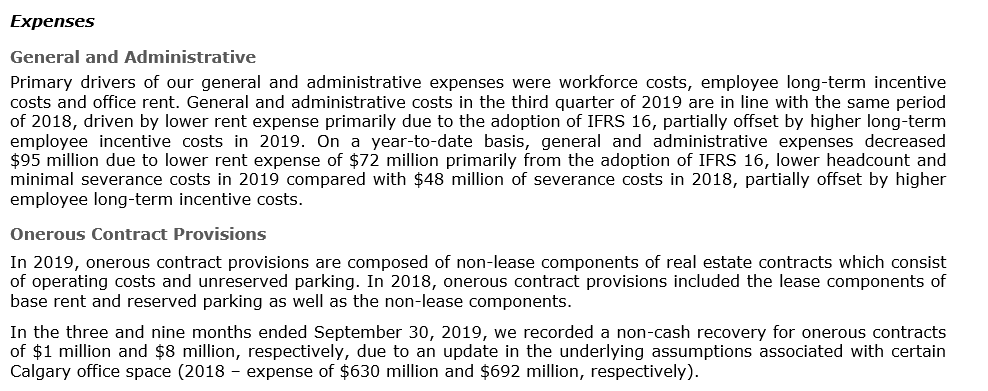

A year ago the company was right-sizing the workforce. In addition, some office space was written off as the company no longer needed the offices. The future rent was appropriately discounted and the value written off. Those expenses were largely absent in the current year. The result was much lower general and administrative costs. Future income will be affected if the company re-leases the spaces that are now vacant. As shown above, that recovery process has now begun with some nominal income amounts recorded.

(Canadian Dollars Unless Otherwise Stated)

Source: Cenovus Energy Third Quarter 2019, Management Discussion And Analysis

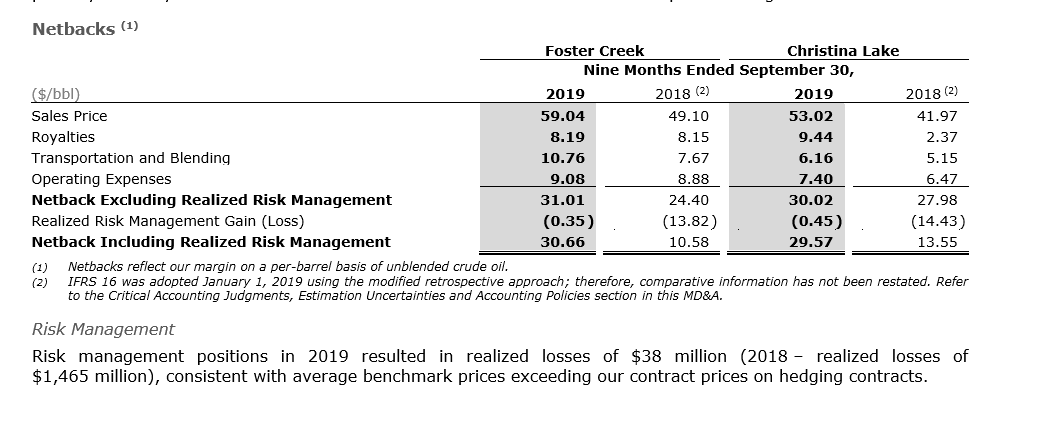

The above results are for the thermal business which still dominates the financial statements by a large margin. Notice that Christina Lake production royalties increased tremendously from a year ago. Yet the absence of the large hedging losses from the previous year allow margins to improve considerably this fiscal year.

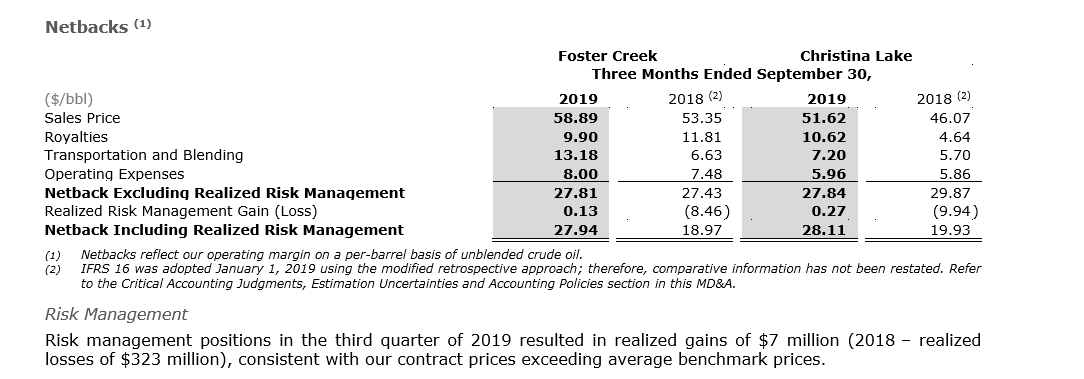

Transportation costs have risen considerably because the rail costs are significantly above the pipeline transportation despite the fact that no diluent is currently necessary for rail transportation. The management gamble is that transportation to the Southern Unites States would result in favorable pricing that will more than offset the increased costs for the foreseeable future.

(Canadian Dollars Unless Otherwise Stated)

Source: Cenovus Energy Third Quarter 2019 Earnings Press Release

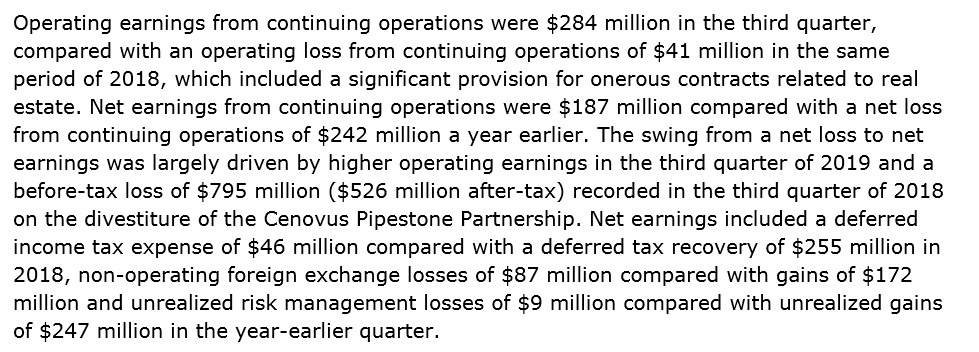

The last major significant non-cash writeoff was the $795 million loss on the sale of the Pipestone Partnership. This is the primary reason for the large swing from a loss to a profit while the cash flow comparisons remained relatively flat. The company had the lack of hedging losses to offset some increasing operating costs due to the lack of takeaway capacity and other issues.

Basically there were a lot of issues that are not recurring in the current fiscal year that have led to some better results. In the meantime, management has focused upon reducing costs and repositioning the Deep Basin operation for a profitable future. Mr. Market may not care because he is focused on the Alberta government intervention. But Cenovus is now positioned to do just fine without the government interference.

Interestingly, the budget for the next fiscal year projects a continuing drop in most costs. The only costs increasing are the Deep Basin costs. That is due to a lack of drilling in the Deep Basin. The arrival of two rigs to begin drilling for liquids in the second half of 2020 could rapidly change the cost picture in the deep basin.

Financial

Management expressed its confidence in the future by increasing dividend 25%. This stock has never been an income play. But this increase signals the beginning of a return to the growth of years past (only this time with a whole lot more profits).

Operating costs have never been lower. But like much of the unconventional industry, this company does not appear to have gotten to the end of well improvements and other cost cutting measures.

There was a time when the different players in the industry were “stuck” in a spot. Now the continuing technology revolution has made thermal very competitive with other types of oil.

Thermal still requires a relatively large cash investment upfront. But the breakeven for these projects has lowered to prices unimaginable just a few years back. It appears that Cenovus gained material thermal production just in time to lower the costs of that thermal production materially. This is very good news for shareholders.

Conclusion

A lack of hedging issues combined with a lack of consolidation and subsequent non-core sales unleashed the company’s cash flow potential.

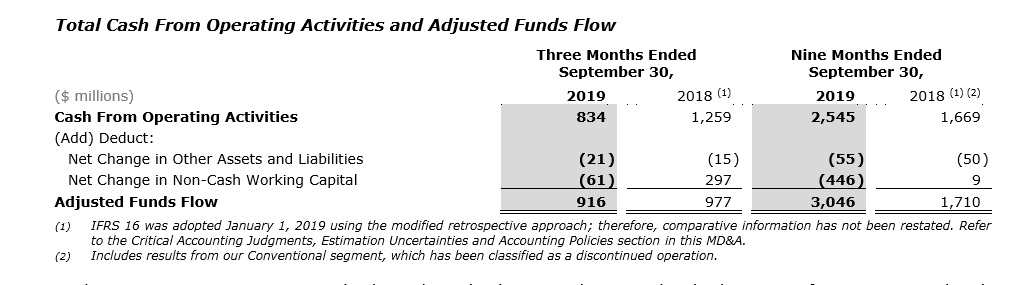

(Canadian Dollars Unless Otherwise Stated)

Source: Cenovus Energy Third Quarter 2019, Management Discussion And Analysis

Cash flow as shown above should easily head past the C$1 billion quarterly mark in the next fiscal year. Only a sustained drop in oil prices would prevent the achievement of that significant goal. This company has quadrupled the quarterly cash flow since the acquisition. Management was helped by completing projects begun under the joint venture, and some significant cost cutting as industry technology continues to improve.

Debt repayment continues. However, management has delivered the deleveraging as promised post acquisition. Now profit margins are as good as many unconventional competitors.

Still, the company does sell a discounted product. Therefore expanding the protection provided by the refineries in the joint venture is probably essential. Management should also probably consider the ability to do on-site upgrading.

In the meantime, the promised conclusion of some more expansion projects should provide still more production. If at any time, the promised extra construction of midstream capacity completes, that completion would provide still more pricing certainty in the future.

This stock is fairly cheap compared to many others trading out there. The current hostile industry conditions pricing the stock should indicate that the market is closer to a bottom than a top. Therefore, the stock is likely to provide an asymmetric return probability in the future. The risk for future long-term principal loss in this investment is minimal. Meanwhile, the recovery potential has been considerably enhanced by the acquisition and sizable free cash flow.

I analyze oil and gas companies like Cenovus Energy and related companies in my service, Oil & Gas Value Research, where I look for undervalued names in the oil and gas space. I break down everything you need to know about these companies — the balance sheet, competitive position and development prospects. This article is an example of what I do. But for Oil & Gas Value Research members, they get it first and they get analysis on some companies that is not published on the free site. Interested? Sign up here for a free two-week trial.

Disclosure: I am/we are long CVE. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Disclaimer: I am not an investment advisor, and this article is not meant to be a recommendation of the purchase or sale of stock. Investors are advised to review all company documents and press releases to see if the company fits their own investment qualifications.