cagkansayin/iStock via Getty Images

The BlackRock Limited Duration Income Trust (NYSE:BLW) is an actively-managed, leveraged corporate bond CEF. BLW’s strong 8.8% distribution yield, 8.7% discount to NAV, and low interest rate risk, make the fund a buy.

BLW is particularly appropriate for income investors and retirees, due to its strong distribution yield. It is also particularly suitable for the current macroeconomic environment of rising interest rates, due to its low interest rate risk. As the fund focuses on comparatively risky, non-investment grade bonds, it is not an appropriate investment for more risk-averse investors and retirees.

BLW – Holdings Analysis

BLW is an actively managed, leveraged corporate bond CEF. It is administered by BlackRock, the largest investment managers in the world.

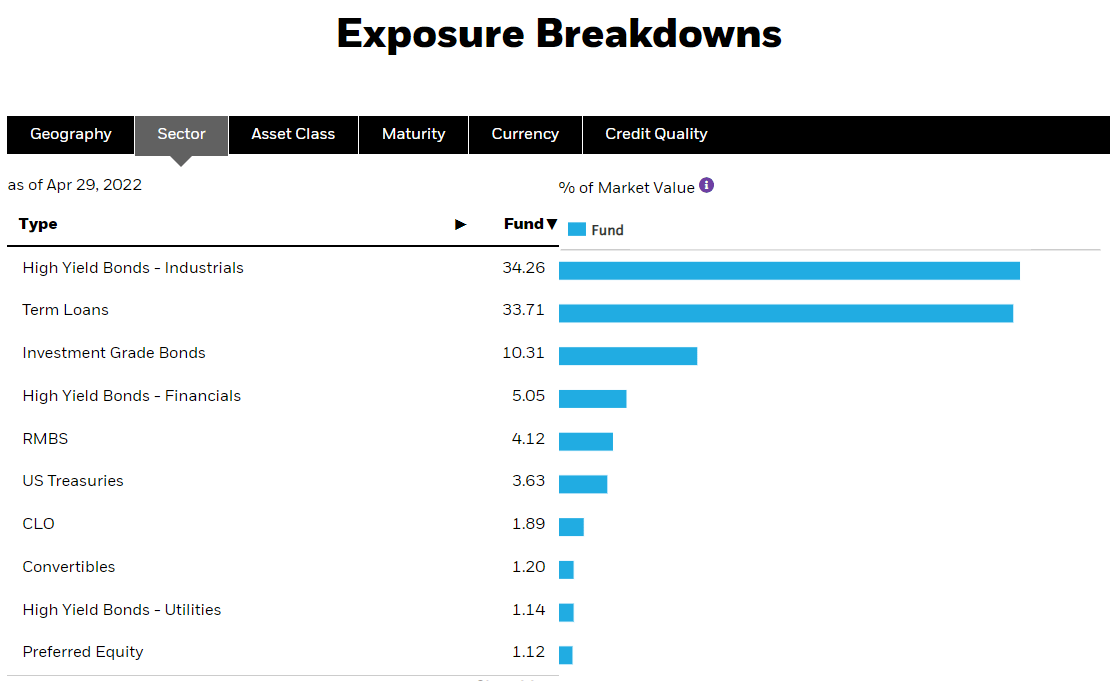

BLW invests in most relevant bond sub-asset classes, including treasuries, investment-grade bonds, mortgage-backed securities, and similar, but clearly focusing on non-investment grade corporate bonds with weak credit ratings. Diversification is reasonably good, although below that of broad-based bond index funds. Sector weights and credit quality are as follows.

BLW Corporate Website

BLW Corporate Website

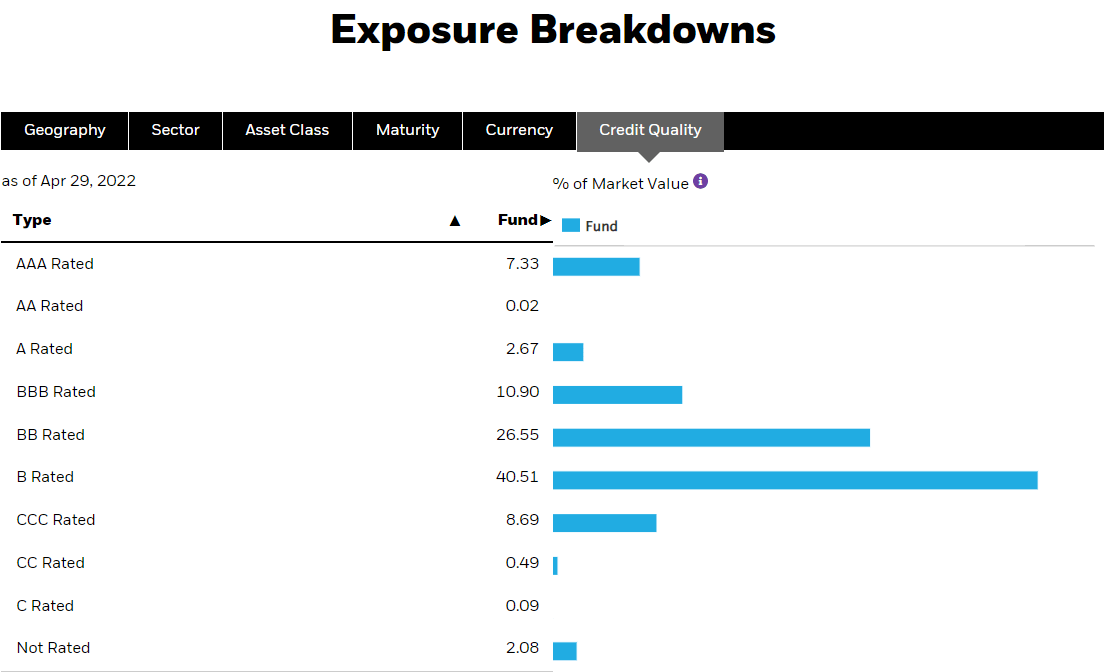

BLW’s holdings are generally of very low credit quality, with the fund’s underlying holdings sporting an average credit rating of B. Bonds with these ratings are issued by companies with comparatively weak financials and balance sheets, and are relatively risky, speculative securities. Defaults are somewhat common, and spike during recessions and downturns, leading to lower bond prices and capital losses. Expect moderate / high losses during downturns and recessions, amplified by the fund’s 1.60x leverage ratio.

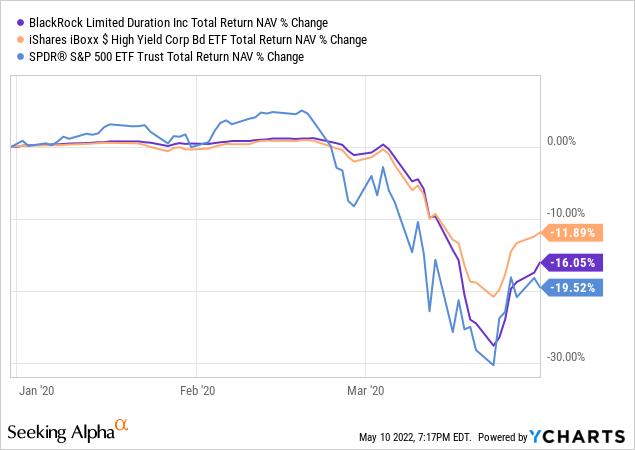

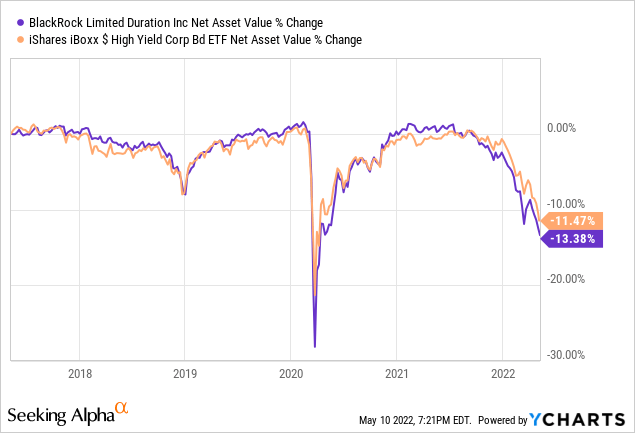

As an example, the fund suffered NAV losses of 16% during 1Q2020, the onset of the coronavirus pandemic, and the most recent economic downturn. Losses were significantly higher than that of most broad-based bond indexes, due to BLW’s comparatively risky holdings. Losses were slightly higher than those of most non-investment grade corporate bond indexes too, due to BLW’s leverage. Losses were slightly lower than those of equity indexes, as bonds are broadly safer investments than equities.

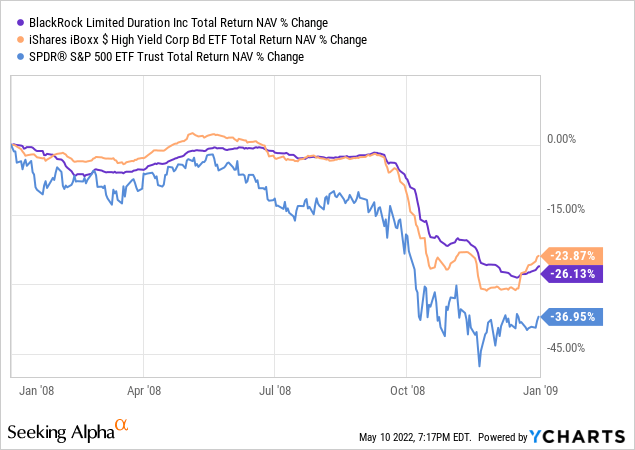

BLW’s performance was broadly similar during 2008, the past financial crisis / housing bubble. The fund slightly outperformed its index, significantly outperformed the S&P 500, and recovered quite a bit faster as well.

In my opinion, and considering BLW’s underlying holdings and performance track-record, the fund is a relatively risky investment, but not excessively so. Large losses during downturns are to be expected, but these should be recoverable, and smaller than those of equity indexes.

BLW – Distribution Analysis

BLW currently sports an 8.8% distribution yield. It is an incredibly strong yield on an absolute basis, and significantly higher than that of most bond indexes, including those focusing on high-yield corporate bonds. Strong yields are almost always a benefit for a fund and its shareholders, and BLW is no exception.

BLW’s strong distributions are mostly the result of focusing on relatively risky, low-quality bonds, but the fund’s use of leverage and discount to NAV boost distributions further.

BLW’s distribution growth track-record is mixed. The fund’s distributions tend to see fluctuations every year: hikes and cuts are both common. Distributions were cut in the aftermath of the financial crisis, soon recovered, and were then cut again a few years later. Distributions stabilized in 2017 and have grown since. In my opinion, current distribution stability / growth is more relevant than old distribution cuts, but thought investors should have the whole picture.

Seeking Alpha

BLW’s distributions are reasonably well-covered by underlying generation of income, with the fund sporting an 85% distribution coverage ratio.

BLW Corporate Website

The small portion of the fund’s distribution which is not covered by income could easily, plausibly be covered by capital or trading gains, and so do not imply ROC distributions or declining NAVs. This has mostly been the case in the past, with the fund’s NAV remaining mostly stable for the past decade or so. NAVs have decreased by quite a bit in the past few months, in-line with high-yield indexes, as interest rates pressure bond prices, but there have been no sustained, consistent reductions in the fund’s NAV which would indicate an unsustainable distribution.

BLW’s strong 8.8% distribution yield is a significant benefit for the fund and its shareholders, and its core investment thesis. This is an income vehicle, which investors buy for the yield.

BLW – Discount Analysis

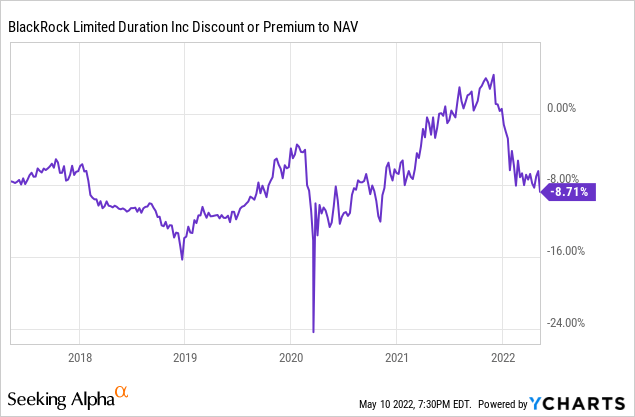

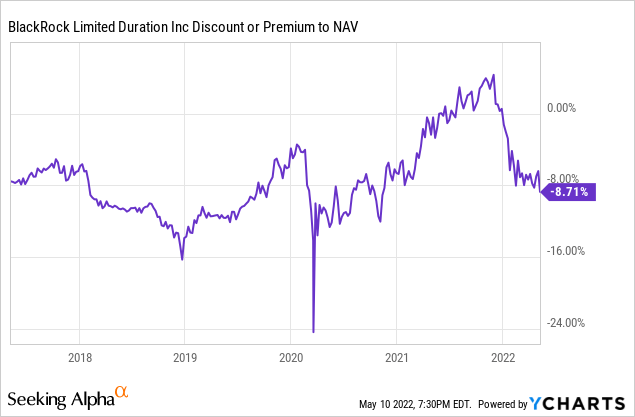

BLW currently trades with an 8.7% discount to NAV. It is a reasonably large discount, largest post-pandemic, although the fund did trade with a moderately larger discount from mid-2018 to mid-2019.

Discounts benefit investors in two key ways.

Discounts can always narrow, leading to capital gains. This has been the case for BLW in the past, with the fund seeing strong capital gains when discounts last fell to these levels, in early 2020.

Discounts are analogous to lower share prices, and lower share prices means higher distributions yields. These are a direct, straightforward benefit for investors, and one which is not dependent on investor sentiment or narrowing discounts to materialize. Discounts mean higher distributions which means higher returns even if discounts never narrow.

As an example, BLW’s discount is very slightly down from five years ago, although there have been many fluctuations along the way.

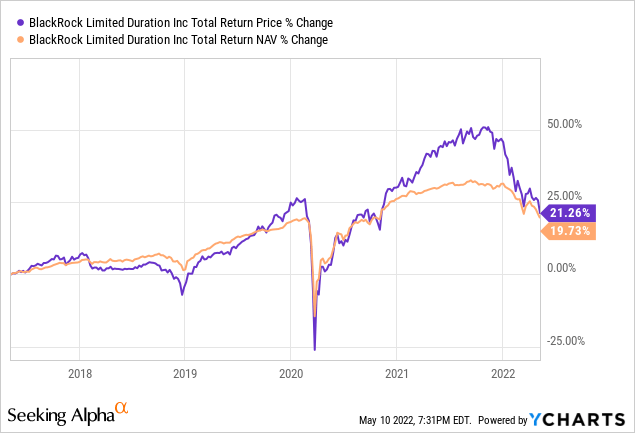

Even though discounts have not narrowed, BLW’s total price returns have outpaced its total NAV returns by about 1.5% in the past five years, or 0.3% per year.

BLW’s price returns outpaced its NAV returns due to the higher distributions from trading with a discount. BLW’s 8.7% discount to NAV means distribution yields are 8.7% higher than if the fund traded at NAV, which means higher realized returns for shareholders. These excess returns might not be particularly significant benefits, but they are benefits, and not reliant on market sentiment or uncertain possibilities of narrowing discounts.

BLW – Interest Rate Risk Analysis

BLW’s distribution yield and discount to NAV are both reasonably strong figures, but not terribly uncommon in the high-yield leveraged bond CEF world. BlackRock, for instance, has several funds with these characteristics, including the BlackRock Multi-Sector Income Trust (BIT) and the BlackRock Credit Allocation Income Trust IV (BTZ). PIMCO has close to a dozen similar funds, all with strong yields, although rarely with discounts.

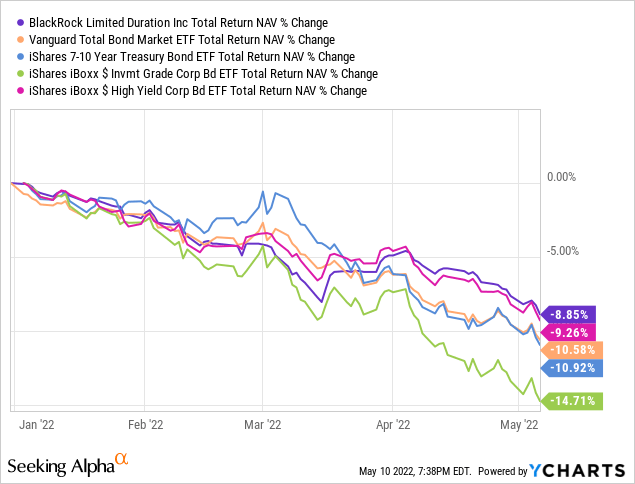

What really sets BLW apart from these other funds is its low interest rate risk. BLW focuses on short-term bonds, with low maturity dates and duration. These bonds mature relatively quickly, and so can be replaced relatively quickly, allowing the fund to benefit from rising interest rates. BLW’s holdings also include derivatives meant to decrease interest rate risk further.

Most bond funds focus on comparatively higher-maturity bonds, which are adversely affected by rising interest rates. Investors have been selling these bonds for quite a few months ago, to replace them with higher-yielding issues once the Federal Reserve finishes hiking rates. Selling pressure has caused bond prices to significantly decrease for quite a while, with long-term bonds being particularly hard-hit. BLW has weathered these issues comparatively well due to its low interest rate risk / exposure, outperforming all relevant bond indexes YTD. Results have been particularly good considering the fund’s leverage and relatively risky holdings. Both magnify losses, but have been more than completely neutralized by the fund’s low duration.

BLW’s low interest rate exposure minimizes losses when interest rates are rising, as they currently are.

Conclusion

BLW’s strong 8.8% distribution yield, 8.7% discount to NAV, and low interest rate risk, make the fund a buy.