Lemon_tm/iStock via Getty Images

Black Stone Minerals (BSM) appears capable of generating $1.69 per unit in distributable cash flow in 2022 at current strip prices (including roughly $80 WTI oil and $4.20 NYMEX gas).

Beyond 2022, it may be able to generate $1.54 per unit in distributable cash flow at long-term prices $65 WTI oil and $3.25 NYMEX gas. It looks capable of paying a $0.35 per quarter distribution ($1.40 per year) going forward while also maintaining distribution coverage of 1.2x for 2022 and 1.1x after 2022.

This assumes that production remains stable at around 38,000 BOEPD.

Production Volumes

Black Stone’s total production appears to be holding steady at around 38,000 BOEPD. Black Stone’s mineral and royalty production has been increasing while its working interest production has been decreasing due to its decision to farm out its working-interest participation to third-party capital providers.

| Q4 2020 | Q1 2021 | Q2 2021 | Q3 2021 | |

| Mineral and Royalty Production (MBoe/d) | 32.0 | 31.1 | 32.5 | 33.0 |

| WI Production (MBoe/d) | 7.0 | 5.8 | 5.7 | 5.1 |

| Total Production (MBoe/d) | 39.0 | 36.8 | 38.2 | 38.0 |

Black Stone mentioned that it expects its total production for 2021 to be at or near the high end of its revised guidance range of 34,500 to 37,000 BOEPD. It seems likely to end up averaging above 37,000 BOEPD for the full year since getting to a 37,000 BOEPD average for 2021 would only require 35,000 BOEPD in production in Q4 2021.

2022 Outlook

Current strip for 2022 is around $80 WTI oil and $4.20 NYMEX gas. If production remains around 38,000 BOEPD (with 73.5% gas and 26.5% oil), Black Stone Minerals would be expected to generate $564 million in revenues before hedges.

Black Stone’s 2022 hedges have around negative $77 million in value at those oil and gas prices.

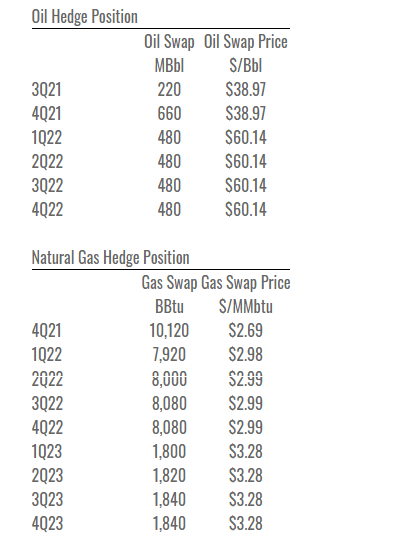

Black Stone’s hedging position

It has around 52% of its oil production hedged at $60.14 per barrel and 52% of its natural gas production hedged at $2.99. This is much improved from its 2021 oil hedges at under $40 per barrel.

|

Type |

Barrels/Mcf |

Realized $ Per Barrel/Mcf |

Revenue ($ Million) |

|

Oil (Barrels) |

3,675,550 |

$78.50 |

$289 |

|

Natural Gas [MCF] |

61,166,700 |

$4.25 |

$260 |

|

Lease Bonus and Other Income |

$15 |

||

|

Hedge Value |

-$77 |

||

|

Total |

$487 |

This scenario would result in Black Stone Minerals having approximately $133 million in cash expenditures in 2022, inclusive of preferred distributions. It would be projected to end up with $354 million in distributable cash flow. This is approximately $1.69 per common unit.

|

$ Million |

|

|

Lease Operating Expense |

$13 |

|

Production Costs And Ad Valorem Taxes |

$58 |

|

Cash G&A |

$38 |

|

Cash Interest |

$3 |

|

Preferred Distributions |

$21 |

|

Total Expenses |

$133 |

Black Stone Minerals could end up with a distribution of $0.35 per quarter in 2022. This would be a coverage ratio of 1.2x and may allow Black Stone to pay its net debt down to around $25 million by the end of 2022.

Long-Term Scenario At $65 Oil and $3.25 Gas

If Black Stone Minerals has production stabilize at 38,000 BOEPD going forward, then it would generate approximately $442 million in revenue at $65 WTI oil and $3.25 NYMEX gas after 2022.

|

Type |

Barrels/Mcf |

Realized $ Per Barrel/Mcf |

Revenue ($ Million) |

|

Oil (Barrels) |

3,675,550 |

$63.50 |

$233 |

|

Natural Gas [MCF] |

61,166,700 |

$3.25 |

$199 |

|

Lease Bonus and Other Income |

$10 |

||

|

Total |

$442 |

Black Stone Minerals would have around $324 million in distributable cash flow per year in this long-term scenario, or $1.54 per common unit with around 210 million common units.

|

$ Million |

|

|

Lease Operating Expense |

$13 |

|

Production Costs And Ad Valorem Taxes |

$47 |

|

Cash G&A |

$36 |

|

Cash Interest |

$1 |

|

Preferred Distributions |

$21 |

|

Total Expenses |

$118 |

Black Stone Minerals should be able to support a $0.35 per quarter distribution at $65 WTI oil and $3.25 NYMEX gas. This would result in a 1.1x coverage ratio.

Since Black Stone’s net debt would be relatively minimal in this situation, it could put some of its extra funds towards unit repurchases.

Notes On Valuation

I can see Black Stone Minerals being worth around $13.25 per unit at long-term (beyond 2022) $65 WTI oil and $3.25 NYMEX gas. It would be able to pay an annual distribution of $1.40 per unit, resulting in a 10.6% yield at $13.25 per unit, while keeping distribution coverage at around 1.1x or better.

At long-term $70 WTI oil and $3.50 NYMEX gas, Black Stone’s estimated value improves to $14.55 per common unit.

Conclusion

Black Stone Minerals should be able to support a $0.35 per unit quarterly distribution based on current 2022 strip prices and assuming longer-term $65 WTI oil and $3.25 natural gas after 2022. Black Stone Minerals would also be able to pay down its net debt to around $25 million by the end of 2022 and then have close to $30 million per year (in excess of distributions) to put towards unit repurchases and other purposes in a $65 WTI oil and $3.25 NYMEX gas environment.