designer491/iStock via Getty Images

Author’s note: This article was released to CEF/ETF Income Laboratory members on February 14th, 2022.

The BlackRock Investment Quality Municipal Trust (BKN) is a diversified, actively-managed, leveraged municipal bond CEF. BKN offers investors a strong, tax-exempt 5.3% distribution yield, and industry-beating returns. The fund is a buy, and particularly appropriate for income investors and retirees.

BKN – Overview

BKN is a diversified, actively-managed, leveraged municipal bond CEF. It is administered by BlackRock (NYSE:BLK), the largest investment manager in the world.

BKN invests in tax-exempt municipal bonds, with these comprising at least 80% of the value of the fund, usually more, with cash and cash equivalents comprising the rest. BKN’s tax-exempt 5.3% yield is the fund’s key benefit and differentiator, and particularly important for income investors and retirees in higher tax brackets. The exact impact of said benefit depends on the individual circumstances of each individual investor, and is therefore outside the scope of this article. Still, thought to include a quick table that might help quantify the said impact. The table below compares a tax-exempt yield, BKN’s yield highlighted in yellow, with the equivalent taxable yield.

Russell Investments

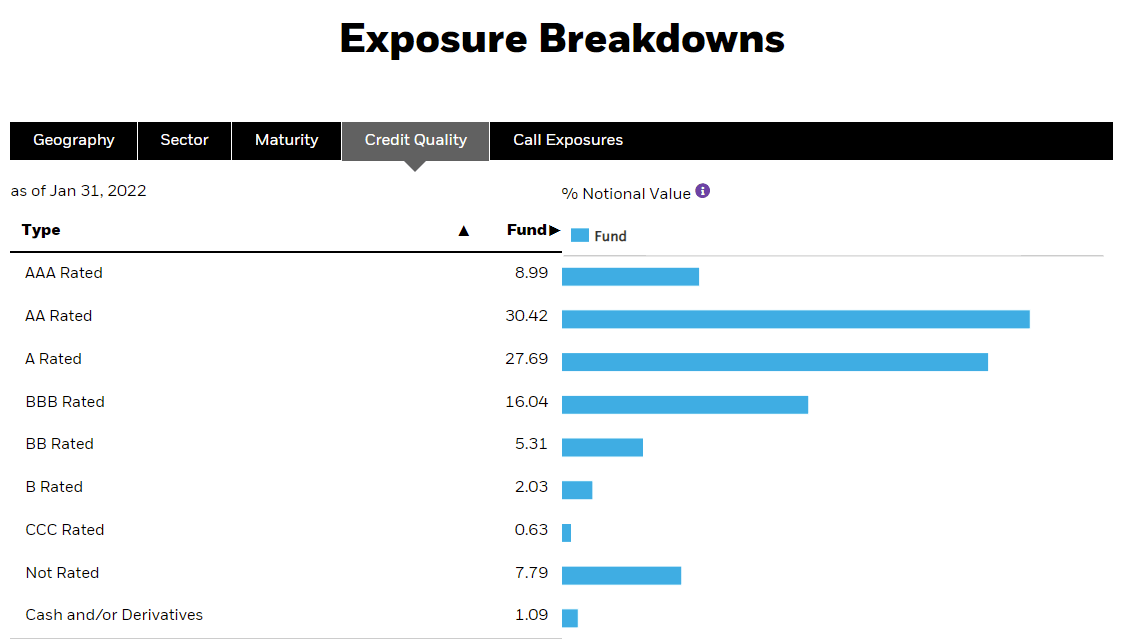

BKN focuses on high-quality municipal bonds, with an average credit rating of A, and low-single-digit allocations to bonds with non-investment grade ratings.

BKN Corporate Website

BKN’s credit ratings are reasonably strong, which should help minimize losses during downturns and recessions. This was the case during 1Q2020, the onset of the coronavirus pandemic, during which BKN posted losses of only 4.0%, versus 19.6% for the S&P 500.

On the other hand, BKN’s holdings are somewhat riskier relative to most municipal bond index ETFs. As an example, the iShares National Muni Bond ETF (MUB), the industry benchmark, invests in holdings with an average credit rating of AA, and holds effectively no non-investment grade bonds. BKN’s holdings have lower credit ratings than the benchmark, and the most relevant index ETFs.

MUB Corporate Website

BKN’s comparatively risky holdings should cause the fund to underperform relative to its benchmark during downturns and recessions. The fund’s use of leverage, with BKN sporting a massive 1.63x leverage ratio, would magnify any possible losses further. BKN is still a reasonably safe fund, and generally safer than broad-based equity index funds, but it is also less safe than its benchmark or than most municipal bond index ETFs.

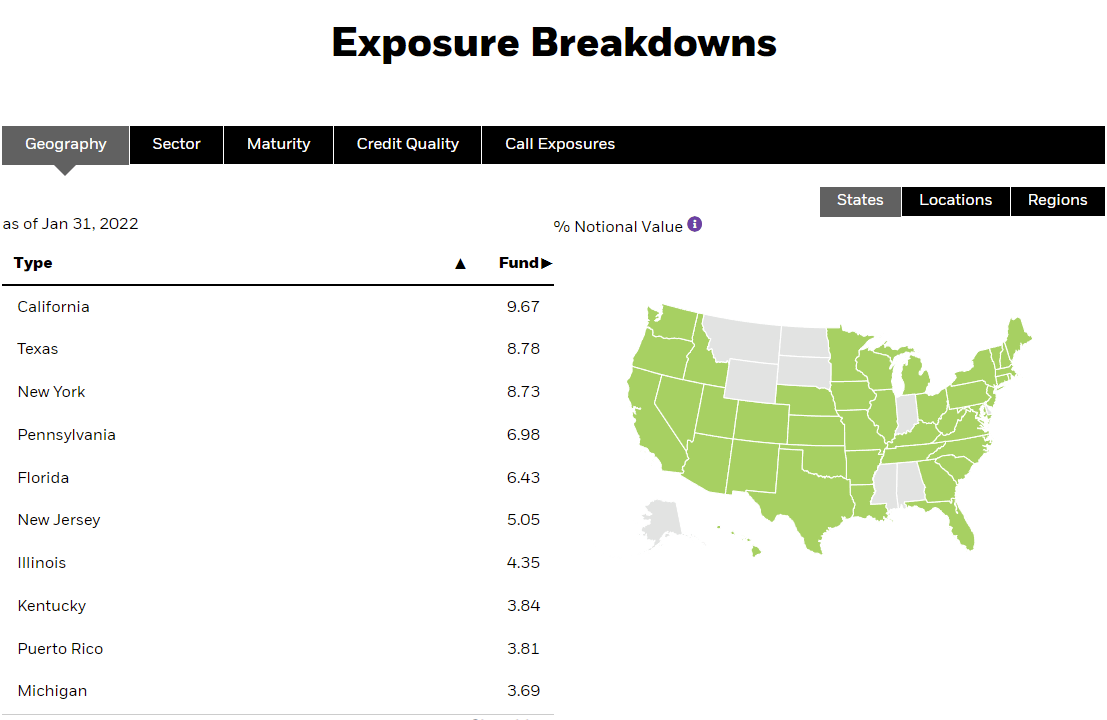

BKN’s holdings are reasonably well-diversified across states, with investments in 42 states, and Puerto Rico. Diversification reduces portfolio risk and volatility, minimizes losses from any one individual default, and is a benefit for the fund and its shareholders.

BKN Corporate Website

BKN is a diversified tax-exempt municipal bond CEF, and its holdings reflect that.

With the above in mind, let’s have a look at the fund’s investment thesis.

BKN – Investment Thesis and Benefits

BKN’s investment thesis is quite simple: the fund offers investors a strong, tax-exempt 5.3% distribution yield, and a comparatively good performance track record. Said combination makes for a strong fund and investment opportunity, and one which is particularly appropriate for income investors and retirees. Let’s have a look at these two points.

BKN – Distribution Analysis

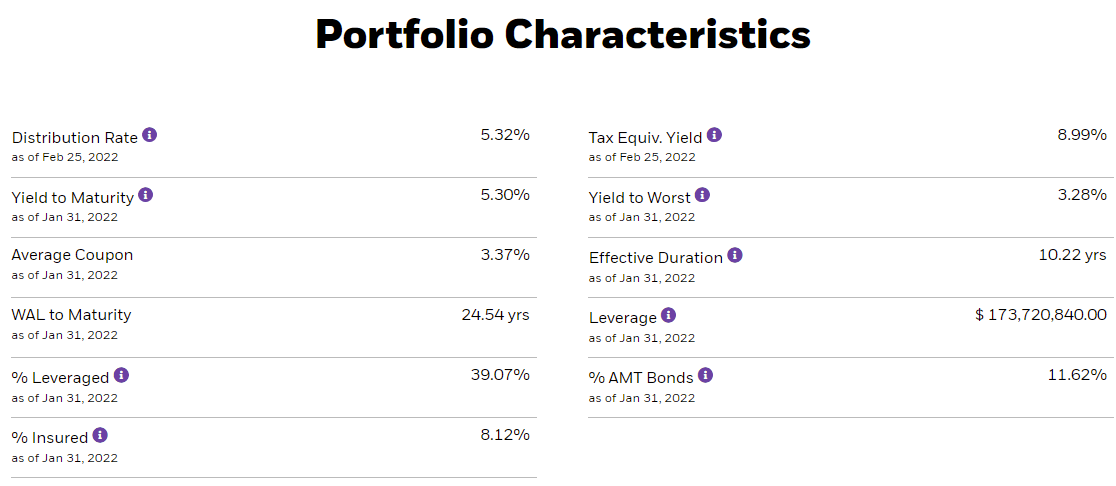

BKN’s 5.3% distribution yield is reasonably good on an absolute basis, and higher than that of most relevant bond indexes. The fund’s comparatively strong yield is partly the result of leverage, debt means more assets which means more income which means higher yields, and active management, with the fund’s managers focusing on higher-yielding bonds.

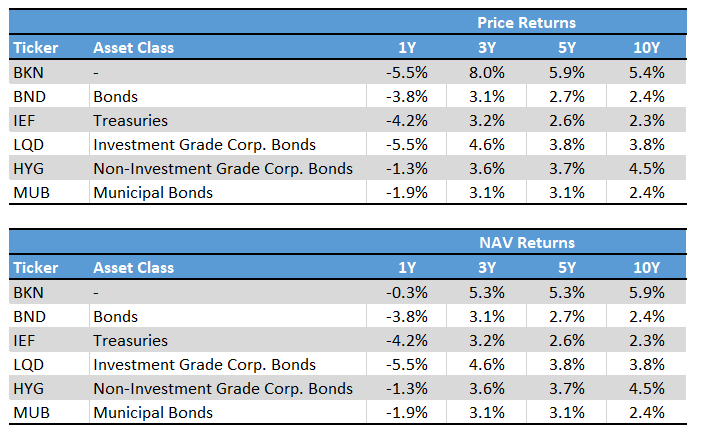

The fund’s yield compares particularly well with the 1.8% yield of MUB, the municipal bond benchmark. BKN also yields slightly more than high-yield corporate bonds, even as the fund is significantly safer than said securities. For reference, the performance of these two funds/asset classes during 1Q2020, the most recent downturn.

BKN’s distribution yield is particularly attractive due to its tax-exempt status. In general terms, investors don’t pay tax on BKN’s 5.3% yield, but they do pay tax on the distributions of its lower-yielding peers. This increases the attractiveness of the fund relative to its peers, especially for investors in higher tax brackets.

Higher yields directly increase total shareholder returns and are almost always a benefit for investors, as is the case for BKN.

On a more negative note, the fund’s distributions fluctuate year to year, with a clear downwards trend. BKN’s distributions have gone down by about 20% in the past decade, although there has been some growth/recovery in the past four years or so. Distributions are down due to declining interest rates, but could see some long-term growth as the Federal Reserve hikes rates. On a more positive note, the fund’s distribution cuts have allowed the fund’s NAV to remain stable, even grow a tiny bit, since inception, and for most relevant time periods too. Distributions cuts are obviously a negative, but the alternative, declining NAVs and capital losses, are worse, and the fund does avoid these more significant issues.

BKN – Performance Track Record

Strong distribution yields sometimes come at the expense of capital gains or total shareholder returns, but that is not the case for BKN. The fund has outperformed all relevant bond indexes since inception, on both a price and NAV basis, and by a reasonably good 1-3% amount annually. BKN’s returns mostly consist of distributions, with extremely low, inconsistent, but positive capital gains.

Seeking Alpha – Chart by author

BKN’s strong performance track record is a benefit for the fund and its shareholders, and a core part of its investment thesis. BKN’s investors receive a strong, tax-exempt 5.3% distribution yield, and do not sacrifice total returns or invested capital to do so.

On a more negative note, the fund has significantly underperformed on a price basis this past year. Underperformance is mostly due to declining premiums. BKN’s premium has decreased from a historical high of +15% in May-June of 2021, to a 1% discount as of late February of 2022. Declining premiums meant significant capital losses for past shareholders, and were broadly harmful for these. Declining premiums mean the fund (finally) presents a reasonable entry point for new investors, and are broadly beneficial for these.

BKN – Risks and Drawbacks

BKN is a strong fund and investment opportunity, but it is not one without risks or drawbacks. One stands out.

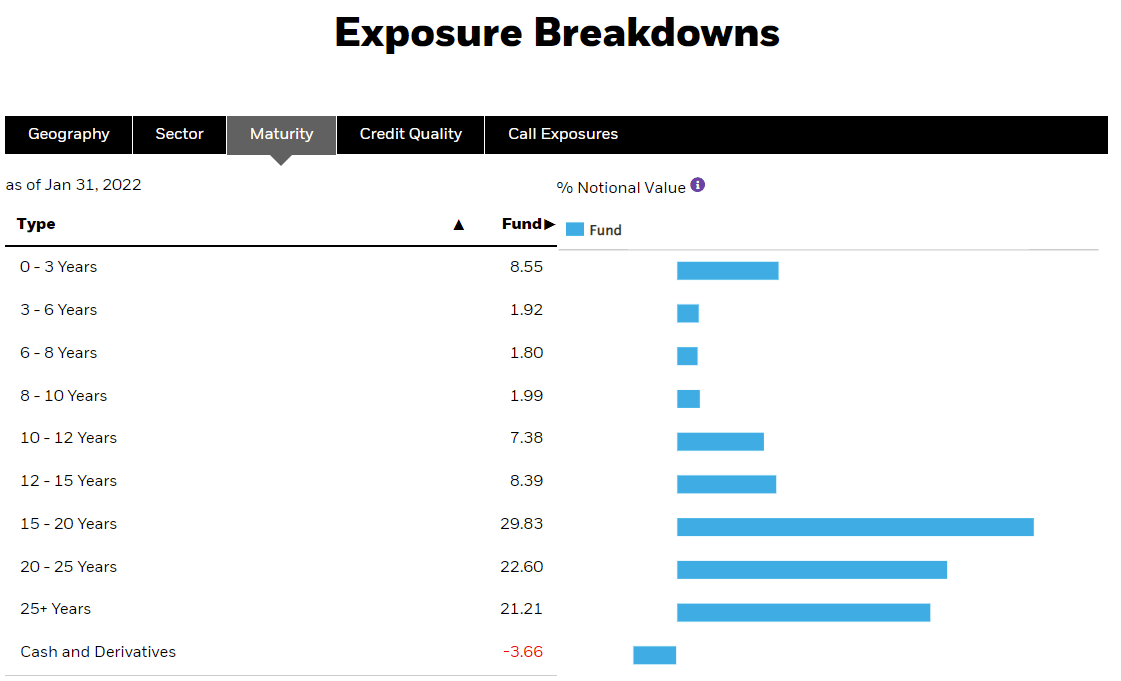

BKN focuses on long-term bonds, with maturity dates in the decades.

BKN Corporate Website

These long-term bonds generally carry comparatively low interest rates, as the Federal Reserve has kept interest rates near zero for quite a few years. If interest rates were to rise, as seems exceedingly likely, investors would sell these old, lower-yielding bonds to buy newer, higher-yielding alternatives. This would lead to lower prices for these older bonds, and capital losses for bondholders, including BKN and its investors. Losses would be magnified by BKN’s use of leverage: debt means more assets which means more losses when asset prices go down. BKN’s investors would see mounting losses if rates were to significantly increase. As per BKN’s management, the fund sports a duration, a measure of interest rate sensitivity, of 10y. This means the fund should see 10% in capital losses for every 1% increase in interest rates. Large losses for small increases in interest rates are obviously not ideal.

BKN Corporate Website

From what I’ve seen, the fund does perform as implied by its duration. As an example, the 10-year treasury rate is up by about 0.7% these past twelve months.

BKN’s NAV is down by about 8%, 10 times as much as the change in treasury rates, as expected from a fund with a duration of 10 years.

BKN’s strong sensitivity to interest rates is the fund’s most significant negative. In my opinion, and considering the long-term secular decline in interest rates, this isn’t a significant long-term issue, but it is definitely a negative. As such, investors more concerned about the possibility of higher interest rates should consider alternatives to BKN.

Conclusion – Buy

BKN’s strong, tax-exempt 5.3% distribution yield and industry-beating returns make the fund a buy, and one which is particularly appropriate for income investors and retirees.