Melissa Kopka/iStock via Getty Images![]()

Beacon Roofing Supply (NASDAQ:BECN), the leading North American roofing materials distributor, currently holds an ~20% share of the $28bn roofing market, although its concentration in re-roofing activity (80%) is a key differentiator given the current inflationary backdrop. In recent years, BECN’s new management has also initiated a positive turnaround, which, combined with cyclical tailwinds, has driven profitability to record levels and allowed for the deleveraging of its balance sheet. With BECN now equipped with ample balance sheet capacity to return meaningful capital to shareholders over time, while also driving growth via M&A, the current trough ~8.5x EV/EBITDA valuation strikes me as unwarranted. As BECN executes on its “Ambition 2025” plan, I expect the stock to re-rate higher.

![]()

Share Gain Initiatives and Pricing Power Support “Ambition 2025” Targets

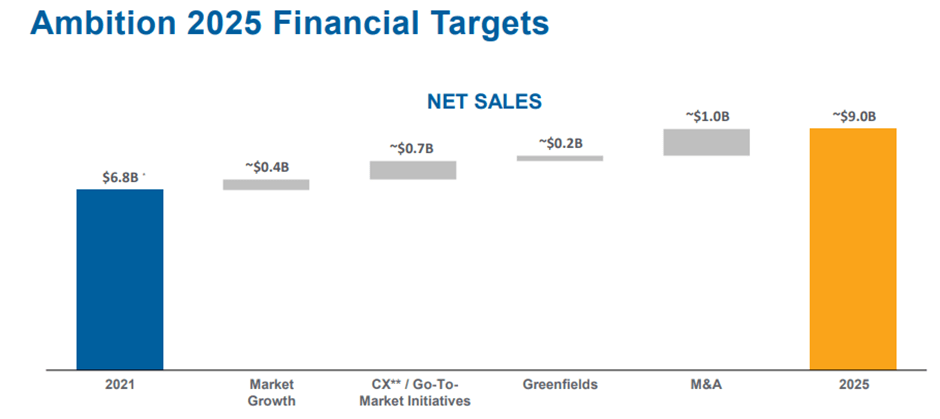

BECN is turning a new chapter with its aptly named “Ambition 2025” targets, headlined by a sales CAGR of ~8% and adjusted EBITDA margins of ~11% over the next four years. This should come as welcome news given it exceeds the prior guidance of mid to high single-digit sales growth with margins also just above 2021 levels. The key driver of the ~$9bn sales target by 2025 (vs. 2022 guidance of $7.1-7.4bn in sales) is $700m from organic market share gain initiatives (2.5% CAGR) based on BECN’s scale advantage and its on-time and complete (OTC) network model, along with its digital and commercial sales center capabilities. All in all, BECN is well-equipped to provide a robust service model in the marketplace to support growth within its existing customer base and to acquire new accounts over the coming years.

Beacon Roofing Supply

Source: Beacon Roofing Supply Investor Day 2022

Even if the current inflationary pressures last for longer than expected, BECN should remain resilient – given roofing products are non-discretionary (i.e., replacing a damaged roof is more of a need than a want), BECN is well-positioned to pass price increases along to its customers. The non-discretionary nature of its revenue stream should thus reduce its exposure to the broader housing market cycle, boosting visibility into its 2025 targets. Plus, the current operating environment favors BECN’s scale as bigger players have the flexibility and negotiating leverage to better mitigate COVID-driven supply chain disruptions. With smaller players also likely to suffer, the current backdrop should allow for consolidation, further helping BECN grow its sales through the cycles.

New Management to Unlock More Margin Upside

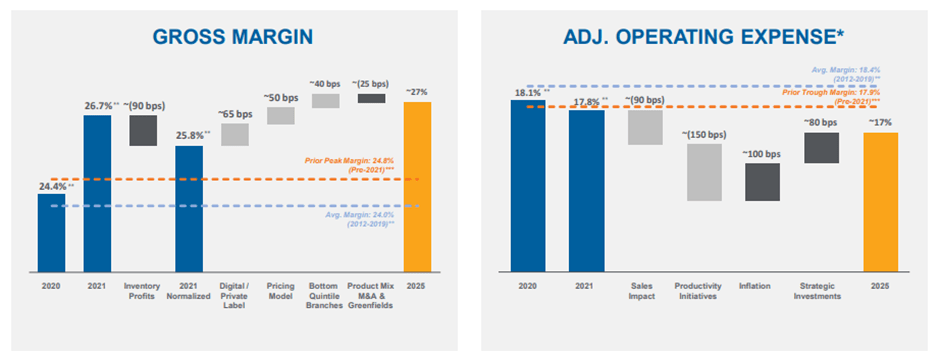

Margin-wise, BECN has a vastly different outlook from when it was a poorly integrated roll-up pre-2020. Since BECN appointed Julian Francis (formerly at Owens Corning (OC)) as CEO and Frank Lonegro (previously CFO at CSX Corporation (CSX)) as CFO, management has impressed in the way they have turned around the business and kept skin in the game (both have been purchasing stock). To recap, BECN’s gross profit margins and operating profit margins have expanded significantly from 2017 to 2021 – gross profit margins are up to 26.5% in 2021 (from 24.6%), and operating profit margins have expanded to 7.1% (from 5.3%). Using the guided $7.3bn revenue base for 2022, every 100bps translates to ~$73m, so the near 200bps expansion is material. Management isn’t done yet – BECN’s investor day commentary indicates there is still further upside left to the margin profile.

Beacon Roofing Supply

Source: Beacon Roofing Supply Investor Day 2022

To a certain extent, the margin improvement is attributable to cyclical tailwinds, with transitory inventory benefits and mid-teens residential growth supporting several price increases (ranging from 5-30%). That said, I think the structural margin improvement thus far is clear and, crucially, remains in the early innings. Underlying the net expansion guidance to ~27% gross margin by 2025, for instance, is BECN’s digital and private label initiatives which are set to generate ~65bps of expansion, followed by its pricing model (~50bps) and enhancements to its underperforming branch (~40bps). The accretion potential of digital sales is particularly compelling – assuming sales roughly doubles in 2025 to ~25% of total sales (from 13.5% in 2021), this entails ~$30m of incremental EBITDA generation given digital sales margins are ~150bps higher than offline. Meanwhile, private label sales (via the TRI-BUILT brand) are also guided to be net accretive, with the $1bn in 2025 sales (vs. ~$600m in 2021) translating into ~$40bn of incremental EBITDA.

Cleaner Balance Sheet Supports Capital Allocation Upside

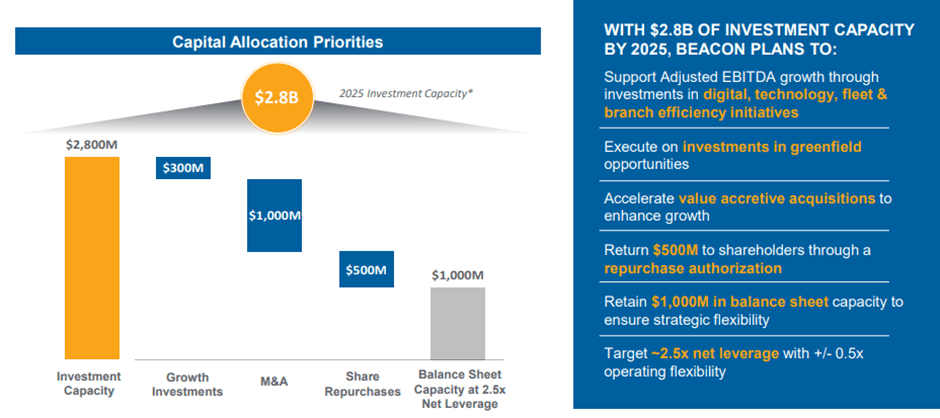

Pre-2020, BECN had been plagued by balance sheet concerns – not only from the COVID impact, but also as the integration of Allied Building Products was weighing on margins. Since 2Q20, however, when net debt/trailing adjusted EBITDA was at ~6x, leverage has since declined significantly to ~2x as of Q4 2021. The de-levered balance sheet has allowed BECN to refinance existing debt in 2021 and extend its debt maturities (the nearest maturity is now for a $300m tranche due in 2026). Following the 2022 investor day, the leverage target now stands at 2-3x, and the company is restarting some tuck-in acquisitions. Per BECN estimates, it will generate $2.8bn of cumulative investment capacity by 2025, of which ~$1 billion will be deployed towards M&A, ~$500 million towards buybacks, and ~$300m towards growth investments (comprising digital, technology, fleet and branch efficiency initiatives). Assuming the midpoint net leverage target of 2.5x, this implies $1.0bn of remaining investment capacity, which could support balance sheet flexibility for incremental investments or shareholder return. So, while the current plan earmarks ~$500m for share repurchase, the new CFO’s track record of being aggressive on buybacks at CSX indicates upside optionality on capital returns, in my view.

Beacon Roofing Supply

Source: Beacon Roofing Supply Investor Day 2022

Turnaround on Track but Valuation Remains at Trough Levels

BECN looks to have turned a corner in recent years, with the combination of new management and cyclical tailwinds driving profitability to record levels. While bears might contend that BECN is over-earning on the back of cyclical tailwinds, I think this view likely underestimates the structural growth and margin expansion opportunities available to the company. Assuming management executes to plan with modest margin improvement of ~100 bps and around half of the FCF is funneled toward buybacks while staying at 2.5x leverage, BECN could retire a significant portion of its shares outstanding in the coming years. With ample growth opportunities also available (organic and inorganic), BECN stock presents investors with many ways to win at the current 8.5x EV/EBITDA valuation.