David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that AVG Logistics Limited (NSE:AVG) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

View our latest analysis for AVG Logistics

How Much Debt Does AVG Logistics Carry?

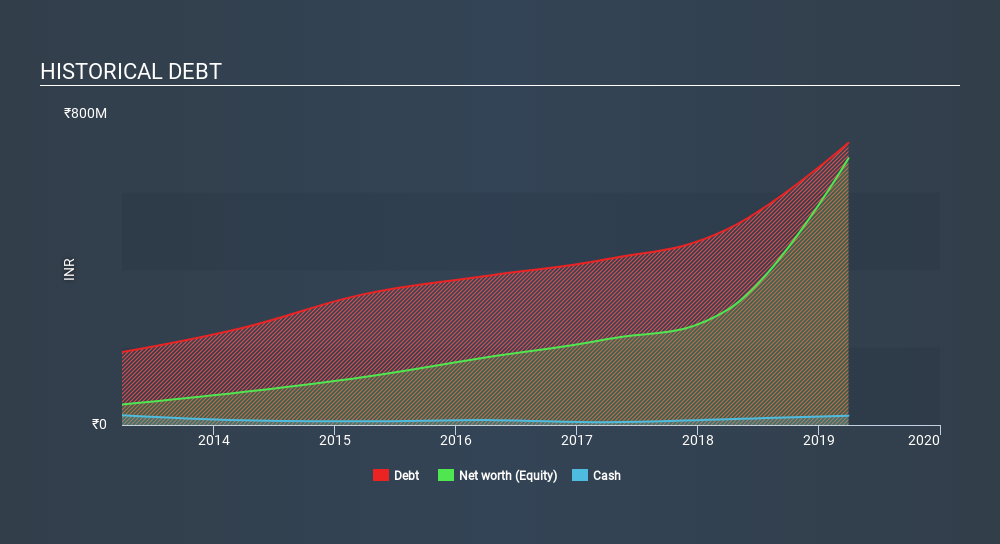

You can click the graphic below for the historical numbers, but it shows that as of March 2019 AVG Logistics had ₹726.0m of debt, an increase on ₹503.7m, over one year. However, because it has a cash reserve of ₹23.6m, its net debt is less, at about ₹702.5m.

How Healthy Is AVG Logistics’s Balance Sheet?

According to the last reported balance sheet, AVG Logistics had liabilities of ₹734.7m due within 12 months, and liabilities of ₹326.9m due beyond 12 months. On the other hand, it had cash of ₹23.6m and ₹799.1m worth of receivables due within a year. So its liabilities total ₹238.8m more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because AVG Logistics is worth ₹620.5m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

AVG Logistics’s debt is 2.5 times its EBITDA, and its EBIT cover its interest expense 3.3 times over. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. If AVG Logistics can keep growing EBIT at last year’s rate of 11% over the last year, then it will find its debt load easier to manage. When analysing debt levels, the balance sheet is the obvious place to start. But you can’t view debt in total isolation; since AVG Logistics will need earnings to service that debt. So if you’re keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, AVG Logistics basically broke even on a free cash flow basis. While many companies do operate at break-even, we prefer see substantial free cash flow, especially if a it already has dead.

Our View

While AVG Logistics’s interest cover makes us cautious about it, its track record of converting EBIT to free cash flow is no better. But its not so bad at growing its EBIT. When we consider all the factors discussed, it seems to us that AVG Logistics is taking some risks with its use of debt. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 5 warning signs we’ve spotted with AVG Logistics (including 3 which is make us uncomfortable) .

When all is said and done, sometimes its easier to focus on companies that don’t even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you spot an error that warrants correction, please contact the editor at [email protected]. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

The easiest way to discover new investment ideas

Save hours of research when discovering your next investment with Simply Wall St. Looking for companies potentially undervalued based on their future cash flows? Or maybe you’re looking for sustainable dividend payers or high growth potential stocks. Customise your search to easily find new investment opportunities that match your investment goals. And the best thing about it? It’s FREE. Click here to learn more.