Steven Grey is CEO and chief investment officer of Grey Value Management, an investment firm. Avaya did not respond to a request for comment.

Only a month after issuing about $600mn in debt, telecom company Avaya on July 28th suddenly slashed its forecasts by two-thirds and ejected its CEO. Earlier this month Avaya admitted that there was “substantial doubt about the company’s ability to continue as a going concern”, revealed an internal investigation into its financial results and the emergence of an apparent whistleblower inside Avaya.

It is no surprise that Avaya’s stock is now almost worthless and that the notes issued in June have lost about half their value. We have one piece of advice for anyone who bought that debt: Pray that the company’s investigation finds evidence of wrongdoing. It may not soften the financial hit, but it might at least offer an excuse and salvage some careers.

But here’s the problem: what if any hypothetical wrongdoing is effectively irrelevant? That is to say, what if the company’s current crisis was telegraphed by its reported performance many, many months before its recent implosion?

By way of background, Avaya is a global leader in the contact centre market and focuses on “unified communications” (UC) — helping businesses integrate all of their communication capabilities. Originally spun off from Lucent in 2000, Avaya was subsequently taken private, and after undergoing bankruptcy reorganisation in 2017, it emerged with a much cleaner balance sheet and perfectly positioned to benefit from the accelerating adoption of UC.

What seemed on its face to be an attractive business became all the more alluring in October 2019 when, following a deal with RingCentral to exchange 6 per cent of its equity for $500mn, Avaya announced plans to take $500mn out of its cash reserves to buy back shares. With a market cap under $1.5bn at the time, this translated to approximately 35 per cent of Avaya’s outstanding shares — a sure boost to the stock price. When only a few months later the pandemic struck, a share price already supercharged by the migration of commerce online caught the mother of all tailwinds.

Avaya wasn’t shy about promoting its results, particularly as measured by their own non-GAAP metrics. Management — led by recently deposed CEO Jim Chirico — was effusive when it came to their performance. You can see his appearance on Jim Cramer’s Mad Money here.

And we were at least sipping the Kool-Aid; by 2021 the equity position we’d begun building in 2018 comprised a significant percentage of our fund’s holdings.

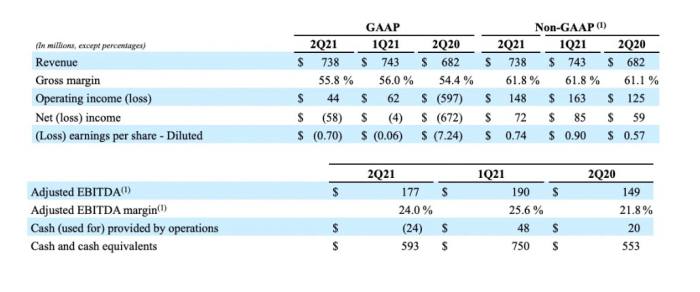

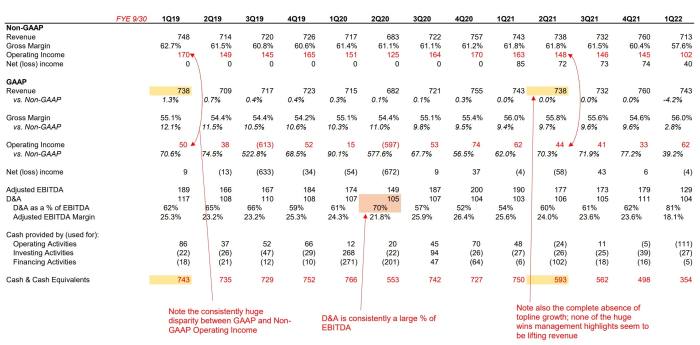

For us the spell broke with Avaya’s second-quarter 2021 earnings announcement. Given the tremendous demand for UC catalysed by Covid-19, the company should have been killing it. And once again, according to their own metrics they were. And yet in GAAP terms their results were oddly anaemic.

For example, ARR (annual recurring revenue — a management metric) grew to $344mm in the second quarter of 2021, up 31 per cent sequentially and nearly 400 per cent from the prior year. And yet total revenue increased by only 8 per cent year-over-year.

The numbers at the operating level exhibited a similar quality — exceeding management’s bespoke benchmarks, but strangely feeble when viewed through GAAP-calibrated lenses.

Why was the company having such difficulty increasing actual revenue and translating that revenue into cash, despite a pandemic that should only have benefited them?

The more we dug into the numbers, the more obvious it became that we had mistaken a rising share price as validation of our investment thesis. Within two weeks we had exited our entire position. Will Rogers once observed that “nothing ruins a good story like an eyewitness.” In this case, the party crasher was GAAP accounting.

If material wrongdoing has actually occurred, then those who bought the debt recently issued by Avaya can credibly claim to have been duped. And should bankruptcy follow, the underlying assets — such as the contact centre business — have substantial value.

But whatever investors may recover after the fact, the red flags for the train wreck they’re now found themselves in were visible long before the June debt offering.