Editor’s Note: This content is provided courtesy of Independent Commodity Intelligence Services (ICIS). Visit natgasintel.com/icis for more information.

HOUSTON (ICIS) – Asia spot LNG prices have fallen this week, with the September ’22 ICIS East Asia Index (EAX) down more than 9% on 21 July from one week ago. The EAX has declined in recent days after peaking above $40/MMBtu.

Natural gas flows along the Nord Stream pipeline from Russia to Germany resumed after planned maintenance, initial operator data showed on 21 July.

Uncertainty over Nord Stream flows also saw the ICIS TTF benchmark firm in recent days, while hot weather across Europe continues to raise energy demand for cooling systems. As market uncertainty deepens, the risk of volatility continues to be high.

While the supply issue in Europe is critical, Asian demand has been impacted as well due to a knock-on effect, traders said.

Winter Outlook

Traders have expressed concern over winter cargo availability looking ahead.

The southeast Asian production complex could be facing a challenging winter, as it could be in discussion to reduce its exported volume over November-January, traders said.

LNG supply from Indonesia is also forecast to be tight for the year, according to energy regulator SKK Migas.

Tangguh LNG and Donggi Senoro LNG are unlikely to produce spot cargoes in 2022, while lower feedgas levels at Bontang in recent months could shelve any earlier plan to market spot cargo, traders said.

Some Chinese market participants have also started checking winter cargo availability with several suppliers, although initial chatter suggests that certain national oil companies are unlikely to issue large buy tenders for this winter unlike previous years.

Tender Buzz

Singapore energy trader Pavilion Energy issued a buy tender into the Singapore LNG terminal for 28 August-15 September based on a link to a northeast Asian marker, trade sources said.

Taiwan’s state-owned CPC is seeking a cargo on a DES basis with a relatively wide delivery window that extends from end-September into October.

Indian state-owned energy company Gujarat State Petroleum Corp. (GSPC) likely awarded its 2 September DES buy tender to the Dahej or Mundra terminals around $36.00/MMBtu, but did not award the 25 September cargo, according to sources.

Argentina Award

Argentina’s state gas distributor IEASA declined to award any cargoes in its most recent buy tender for four August cargoes, which closed on 12 July.

PetroChina, Trafigura, TotalEnergies and Vitol were among the sellers that offered cargoes.

Exact offer levels were not confirmed but market sources said prices between $45/MMBtu and $50/MMBtu were plausible.

IEASA sought three cargoes for Bahia Blanca and one cargo for Escobar. It is unclear whether IEASA will re-tender, but it is likely that the buyer will opt not to tender again for August deliveries.

Prelude Lockout

Shell will resort to lockouts at its Prelude floating LNG plant, meaning that staff will no longer be paid if they are not mobilized to the facility, a company spokesperson said on 20 July.

Shell said the move was in response to protected industrial action, which meant it could no longer continue to find options to work around bans and stoppages.

Shipments from Prelude have been suspended since 11 July, with the last vessel departing on 7 July.

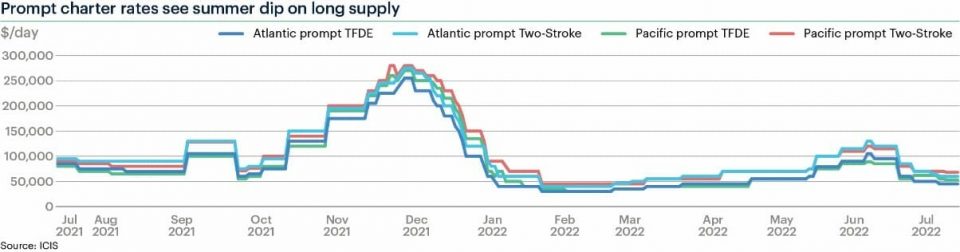

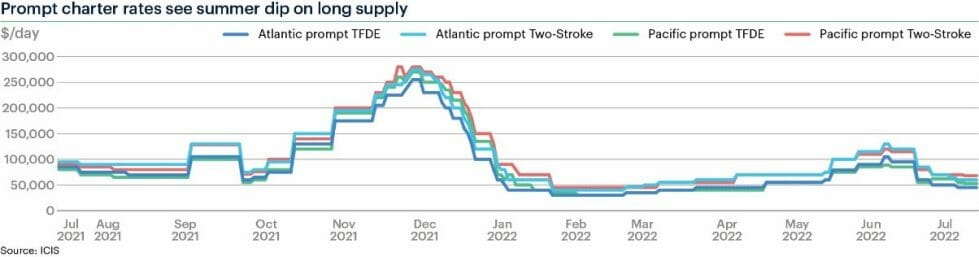

Shipping Rates

In the shipping charter market, sources said vessel availability has lengthened for steam and TFDE vessels this week, as demand for LNG continues to be directed at Europe.

However, while some said they saw rates holding steady, others said that rates had fallen. But a lack of requirements is making a corresponding drop hard to pin down.

Term freight rates are also dropping on expectations of late Freeport LNG ramp up.